FPD設備投資&製造装置調査レポートの分析ダイジェスト~スマホ用投資に代わりG8.5 IT用OLEDラインの投資が活発化

冒頭部和訳

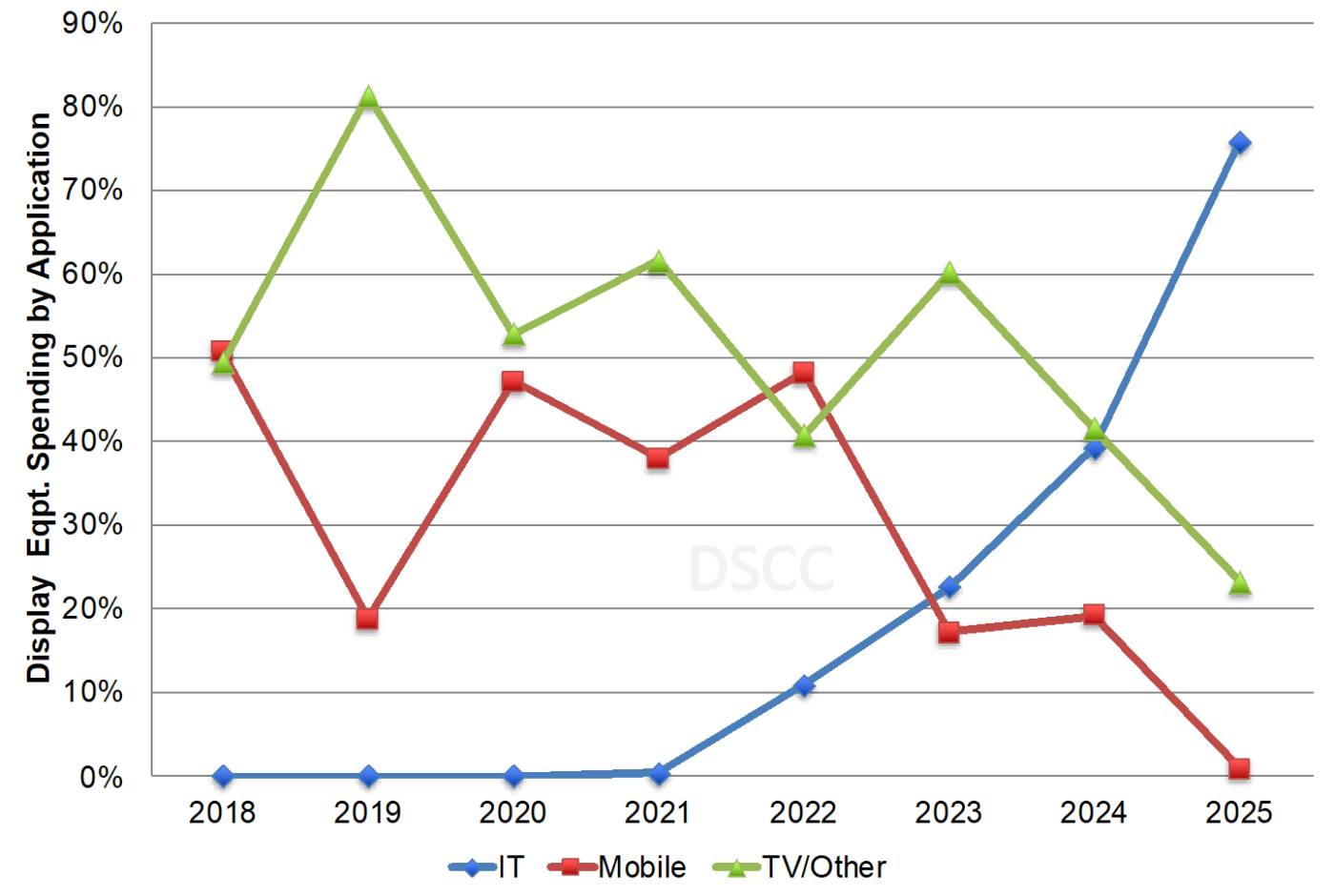

DSCCが四半期毎に発行する Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) の最新刊であるQ1’22版がリリースされた。現在開発が進んでいる15K G8.5/G8.6 IT用OLED生産ラインは11ラインあり、各ラインの時期と設備投資に関するデータが同レポートで明らかになっている。IT用ライン向け設備投資は2021年から2025年まで毎年増加し、2024年と2025年のOLED設備投資、および2025年のLCDとOLEDを合わせた設備投資をリードすると予測される。BOEとVisionoxは両社とも次期スマートフォン用ラインをコスト面で最適化されたIT用RGB OLEDラインに切り替えた。これらのラインはノートPCやその他のアプリケーションでLCDとのコストギャップを縮めるものと期待されている。SDCとLGDでも同様のラインが設置される見通しだ。バックプレーンをLTPSまたはLTPOからマスク数がはるかに少ないIGZOへ変更することで、コスト削減のチャンスが生まれる。

DSCC’s Latest Capex Report Shows 11 G8.5 IT OLED Lines Under Development as Smartphone Spending Stalls

In our just released Q1’22 Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします), we reveal that there are now 11 different 15K G8.5/G8.6 IT OLED lines under development and provide the timing and equipment spending for each. IT fab spending is expected to increase every year from 2021 to 2025 and lead OLED spending in 2024 and 2025 and LCD + OLED spending in 2025. Both BOE and Visionox have switched their next smartphone fabs to these cost optimized IT RGB OLED fabs, which hope to narrow the cost gap with LCDs in notebooks and other applications. SDC and LGD are also expected to build these lines. The cost reduction opportunities lie with changing the backplane from LTPS or LTPO to IGZO, which has many fewer masks. There are additional cost savings expected by switching from a flexible substrate to a rigid + TFE substrate which should reduce the capex and process steps from the PI coating, PI curing, additional CVD barrier layer and laser lift-off (LLO) steps and also boost yields. Furthermore, there are additional productivity/depreciation expense gains from using G8.5 equipment rather than G6 equipment as although the glass size is around 2X larger, the equipment cost is usually much less.

LCD and OLED Equipment Spending by Application

These new fabs will bring some significant changes to OLED manufacturing. First, we will likely see a full G8.5 vertical FMM VTE system in the market as opposed to existing ½ G6 horizontal systems. Both the substrate and FMM are held vertically inside the chamber and the evaporated molecules are made to travel horizontally rather than up. Mask sag issues, which have limited glass/tool size, should be minimized with the new configuration, but there are also concerns with particles, yields, process control, etc., that must be overcome. A ½ G8.5 system may be an option and equipment companies are exploring both horizontal and vertical solutions along with thinner FMMs with less sag. However, depending on the panel size, it could result in fewer cuts per substrate making it less efficient and cost effective as a full G8.5 system.

We are also now expecting to see ion implant tools scaled up to G8.5 for use in the IGZO process. Implant steps can reduce sheet resistance and channel length and boost mobility and resolution. Panel manufacturers are furiously working on boosting IGZO mobility with Sharp targeting 40-80 cm2/Vs through its IGZO8 project. By achieving mobilities that high, IGZO panels could target applications currently dominated by higher mobility LTPS panels. Smartphones become an option for IGZO fabs, especially with OLED smartphone resolution focusing more on FHD+ these days, with a majority of OLED smartphones produced at under 450 PPI. The variable refresh that IGZO can achieve is also valuable to smartphones without requiring LTPO. It is also attractive for notebooks, tablets, monitors and TVs.

Interestingly, if implant can scale to G8.5, then LTPS and LTPO can also scale to G8.5 as Coherent and JSW have already demonstrated ELA solutions at G8.5 and even G10.5. There may be applications that demand LTPS at larger sizes but would not expect the kind of mass adoption that we are seeing in IGZO for cost reasons.

It will be very interesting to watch these developments over the next 12 months with initial POs expected from SDC this year for its first IGZO G8.5 IT OLED line.

In terms of the market for all these G8.5 IT OLED panels:

- Notebooks are likely the initial target as it is a huge market, around 280M panels in 2021, with minimal OLED penetration, ~6M panels or 2% penetration in 2021. However, there are some obstacles for OLED penetration into notebooks which include:

- A single dominant panel supplier – SDC;

- Higher power consumption than LCDs, excluding MiniLEDs. OLED power consumption could come down significantly though through the use of an auxiliary electrode, color on encapsulation, variable refresh with IGZO, a more efficient blue emitter, etc.;

- The lack of rigid + TFE capacity;

- The lack of IGZO backplanes;

- The lack of tandem OLED lines to boost brightness, efficiency and lifetimes.

However, most of these obstacles will be overcome in the next few years. If we assume 10 of these lines are in mass production in 2026, these 10 lines could produce 91M 16.2” notebook panels per year at 80% yields. It is unlikely 1/3 of the notebook market will go to OLED, but it is important to know that there will be capacity in place for that to happen. Of course, if the market develops more slowly than expected for OLED notebooks, the pace of these new fabs could slow. There is also the potential for these fabs to use a flexible substrate and target the foldable notebook market and we are even hearing about one major notebook brand making plans for a 20” foldable notebook in a few years. IGZO enables lower process temperatures than LTPS/LTPO which would help with the adoption of certain materials.

Tablets are another natural opportunity for these fabs which should be able to bring down costs vs. flexible G6 OLED lines. OLED penetration into tablets has also been pretty minimal to date, limited to just SDC and EDO and achieving around 2.7M or 1.1% penetration of the ~230M tablet panel market in 2021. OLEDs are a natural fit for tablets due to their excellent viewing angles, thin form factor, light weight, low power helped by dark mode, etc. The tablet opportunity will also benefit from more suppliers, lower costs from IGZO and rigid + TFE, tandem structures to boost brightness, efficiency and lifetimes, etc. However, existing G6 fabs will also remain viable as they will become fully depreciated and offer the benefit of even lighter weight and reduced thickness. Panel suppliers will likely allocate certain fabs for different sizes based on glass efficiency, etc. IGZO is better suited to larger sizes than ELA, etc.

Monitors are another possibility for these fabs. LCD monitors using a-Si panels are quite aggressively priced, so OLEDs will be better suited for the high-end of the monitor or the gaming monitor market which demands high refresh rates and is less cost sensitive. OLEDs are well suited for gaming due to their inherently faster response times than LCDs. In addition, these RGB OLEDs are much better suited for monitors than the QD-OLED and WOLED solutions we see out there now, due to the ability to achieve higher brightness and higher resolution. At large enough sizes, they are also well suited for dual use as a TV. We are not seeing 4K monitors from WOLED or QD-OLED, so this is an opportunity for these fabs. Monitors were around a 180M panel market in 2021 and less than 100K were OLED. We would expect to see this number grow as optimized RGB OLED G8.5 fabs and manufacturers diversify away from notebooks and tablets.

We may also see an application emerge which we call mirror displays that would be a portable monitor that would mirror a notebook or extend its screen. Some panel suppliers have ambitious plans for this category which already exists. It will certainly get a boost from lower costs enabled by the larger glass sizes with lower cost IGZO backplanes.

As mobility continues to improve, we may still see smartphones made on G8.5 RGB OLED lines if demand outstrips supply at G6. In addition, TVs are another big opportunity if the FMMs can be extended without issues at larger sizes. TVs made with RGB OLEDs should be brighter than WOLED or QD-OLED and should be able to easily achieve 8K, 16K or beyond. Perhaps panel suppliers will target 8K and higher resolution TVs for that reason. While they may start out as a niche, we may see the need for a growing number of these fabs as 8K and beyond evolves.

A final comment on these fabs is that by targeting multiple applications from a single G8.5 fab, they will have much less seasonality than current G6 OLED fabs which are very dependent on Apple’s seasonality. Thus, they will have similar utilization patterns as existing G8.5/G8.6 LCD fabs which would be very positive for OLED suppliers.

For more insight on the latest equipment spending outlook, please see our Quarterly Display Capex and Equipment Market Share Report and for more insight into the implications of G8.5 IT RGB OLED fabs on display technology and markets, please see our Future of OLED Manufacturing Report (一部実データ付きサンプルをお送りします). In addition, for more insight into the cost outlook for different panels made on these fabs, please see our Biannual IT Panel Cost Report (一部実データ付きサンプルをお送りします).