FPD設備投資&製造装置調査レポートの分析ダイジェスト~製造装置メーカー2021年ランキングを発表

冒頭部和訳

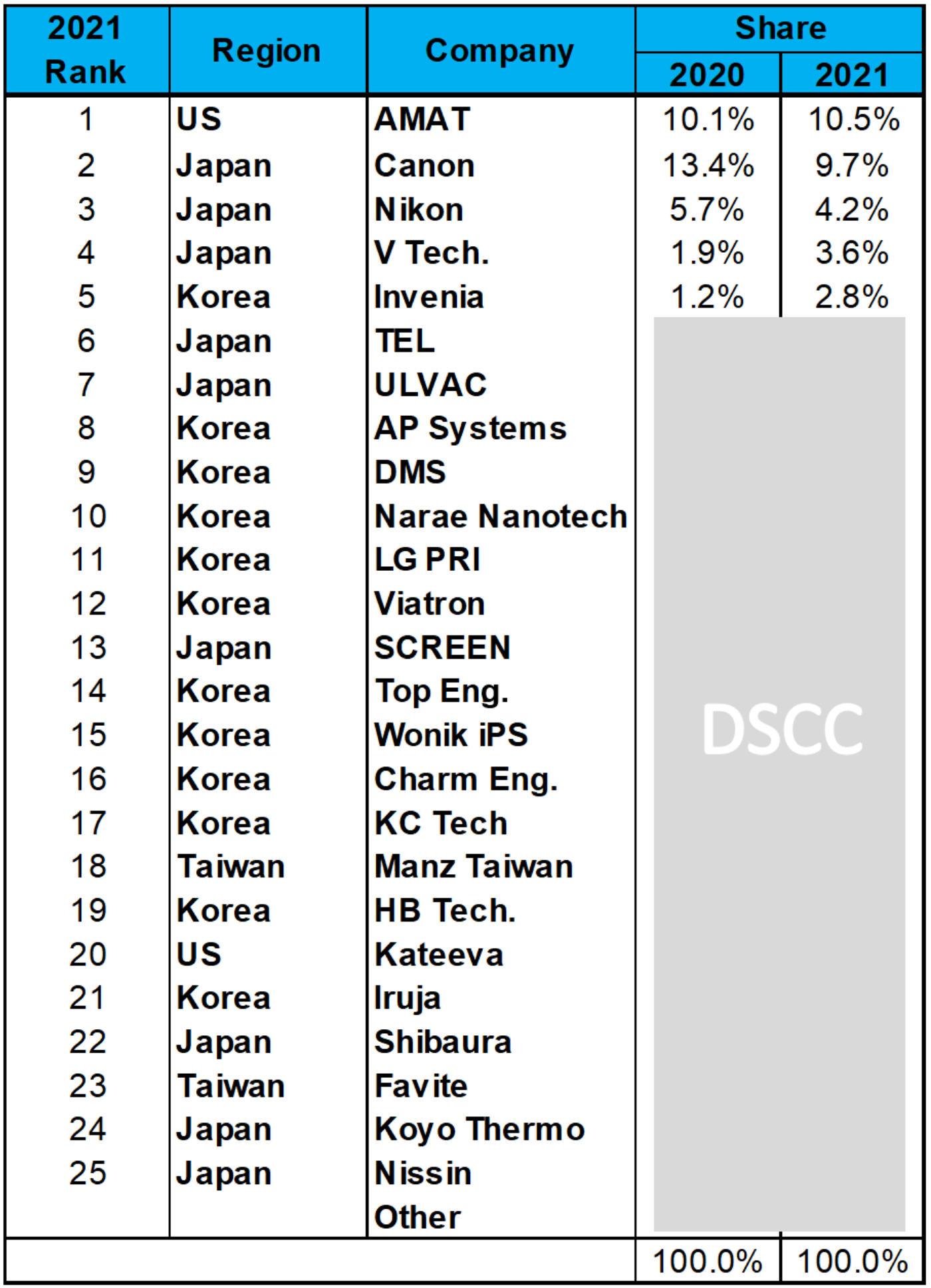

DSCCの Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) の最新刊では装置メーカーの2021年市場シェアについて、装置タイプ別、プロセスタイプ別、および全体の最終結果を明らかにしている。

市場全体では、サービス収益を除く納入ベースで、Applied Materials (AMAT) が前年比13%減ながら2020年の2位から1位に浮上した。Canon/Tokkiは同39%減だった。AMATは5年連続で全体シェアを伸ばしシェア10.5%に到達した。

AMATの装置タイプ別の結果は以下の通り:

• カラーフィルタースパッタリング市場でシェア100%

• CVD市場 (8億5500万ドル規模) でシェア97%と圧倒

• 無機TFE (薄膜封止) 市場 (2億1200万ドル規模) でシェア88%と圧倒

• バックプレーンPVD市場 (6億3500万ドル規模) でシェア37%。HKCとChina Starからの取引獲得で出荷金額が100%以上成長

• SEM市場でトップシェア

AMATは67億ドル規模のTFTバックプレーン市場で2年連続となる首位を獲得、PVD分野のシェア上昇が同社のシェアを13%から17%に押し上げる結果となった。AMATは14億ドル規模のOLEDフロントプレーン市場ではシェアを15%から13%に下げたものの第2位を維持、12億ドル規模のカラーフィルター装置市場ではシェア6%で第2位だった。

DSCC Releases Final Equipment Market Share Results for 2021 and Latest 2022-2025 Outlook

As part of our latest Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします), we released final market share results by equipment type, by process type and overall.

Overall, on a delivery basis with service revenues excluded, we show Applied Materials (AMAT) as #1, up from #2 in 2020, on a slower 13% decline than Canon/Tokki with a 39% decline. AMAT increased its overall share for the fifth straight year reaching 10.5%. It had:

- A 100% share of the color filter sputtering market;

- A dominant 97% share of the $855M CVD market;

- A dominant 88% share of the $212M inorganic thin film encapsulation (TFE) market;

- A 37% share of the $635M backplane PVD market on more than 100% growth helped by wins at HKC and China Star;

- The top share of the SEM market.

AMAT was #1 in the $6.7B TFT backplane market for the second straight year and boosted its share from 13% to 17% on its PVD share gains. It remained #2 in the $1.4B OLED frontplane market with a 13% share, down from 15%, and was #2 in the $1.2B color filter equipment market with a 6% share.

Display Equipment Supplier Revenue Share (Delivery Basis, excludes Service)

Canon fell to #2 with a 10% share, down from 13%. It gained share in lithography with its revenue share rising from 48% to 58%. As a result, it rose from #3 to #2 in total TFT backplane equipment spending reaching an 11% share and overtaking Nikon. It maintained a 100% share in the FMM VTE market in 2021, but the number of systems delivered fell by 40% in an off year for mobile OLED spending. It also didn’t see a repeat order in open mask VTE systems after installing a system at SDC in 2020.

Nikon remained #3 with its share falling from 5.7% to 4.2% on a 39% decline. It lost its revenue leadership in the backplane litho market as it shipped less than half as many expensive G10.5 tools in 2021 vs. 2020. As a result, it fell from #2 to #3 in TFT backplane spending.

V Technology rose from #7 to #4 on strong CF exposure growth and share gains. It also gained share in repair.

INVENIA rose from #11 to #5 on dry etch share gains in both LCDs and OLEDs. Its LCD dry etch share more than doubled on wins at HKC and China Star allowing it to lead the dry etch market in 2021.

Other highlights include:

- Although the market declined in 2021, the following companies saw Y/Y growth in the top 15:

- V Technology up 59% on CF exposure and repair business;

- INVENIA up 86% on dry etch wins;

- ULVAC up 4% on significant sputtering wins;

- Narae Nanotech up 30% on CF coater, coater/developer and PI coater wins;

- LG PRI up 56% on wins for CF exposure, organic TFE and lamination;

- Viatron on furnace/PI curing business;

- Top Engineering on significant scriber wins as well as seal dispense and LC insertion business.

- In the case of the top 25 by country, there were 12 suppliers from Korea, nine from Japan and two each from the US and Taiwan.

In 2022, we currently see Canon regaining the top spot in a stronger year for OLED spending along with litho share gains and a large jump in color filter litho sales. If Canon and Tokki were treated as separate companies, Canon would be #2 in 2022 with Tokki #3. AMAT is expected to fall to #2, Nikon is expected to remain #3 helped by color filter litho sales. ULVAC is expected to rise from #7 to #4 on 21% growth thanks to an FMM VTE win at EDO, CVD wins at AUO and LGD and increased ITO/IGZO business offsetting share losses in OLED metal sputtering. TEL is expected to rise from #6 to #5 on 14% growth on significant LCD and OLED dry etch share gains with HKC’s spending declining. The dry etch gains should offset share losses in coater/developers. Of the top 25, we see 11 from Japan, 10 from Korea and two each from the US and China.

DSCC’s Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) reveals spending by fab by tool type for over 70 different types of tools through 2025. The report reveals the latest fab schedule changes including:

- New LCD and OLED investments;

- Accelerated LCD and OLED investments;

- Canceled/delayed/downsized LCD and OLED investments.

It also reveals new applications and design wins for IJP, new design wins for G8.5 implant, an overview of TFT and OLED manufacturing and insights into advanced AMOLED processes including Touch on TFE, LTPO, CoE, MLP, IGZO advances, tandem structures and the latest in WOLED, QD-OLED and IJP RGB OLED processes as well as a database of LCD and OLED capacity forecasts by manufacturer, glass size, technology, etc. For more information, please contact info@displaysupplychain.co.jp.