FPD用ガラス出荷面積は2021年に過去最高を記録、Q1’22年も堅調

冒頭部和訳

DSCCが先週リリースした Quarterly Display Glass Report (一部実データ付きサンプルをお送りします) 最新号によると、大画面LCDパネルに対する強力な需要にけん引され、2021年のFPD用ガラス出荷面積は前年比13%増の6億8700万㎡に到達、過去最高を記録した。Q4'21のFPD用ガラス出荷面積は前期比2%減の1億7450万㎡だった。Q1’22は前期比1%増の1億7600万㎡になると予測される。パネルメーカーの稼働率低下を能力拡張が埋め合わせることがその要因である。

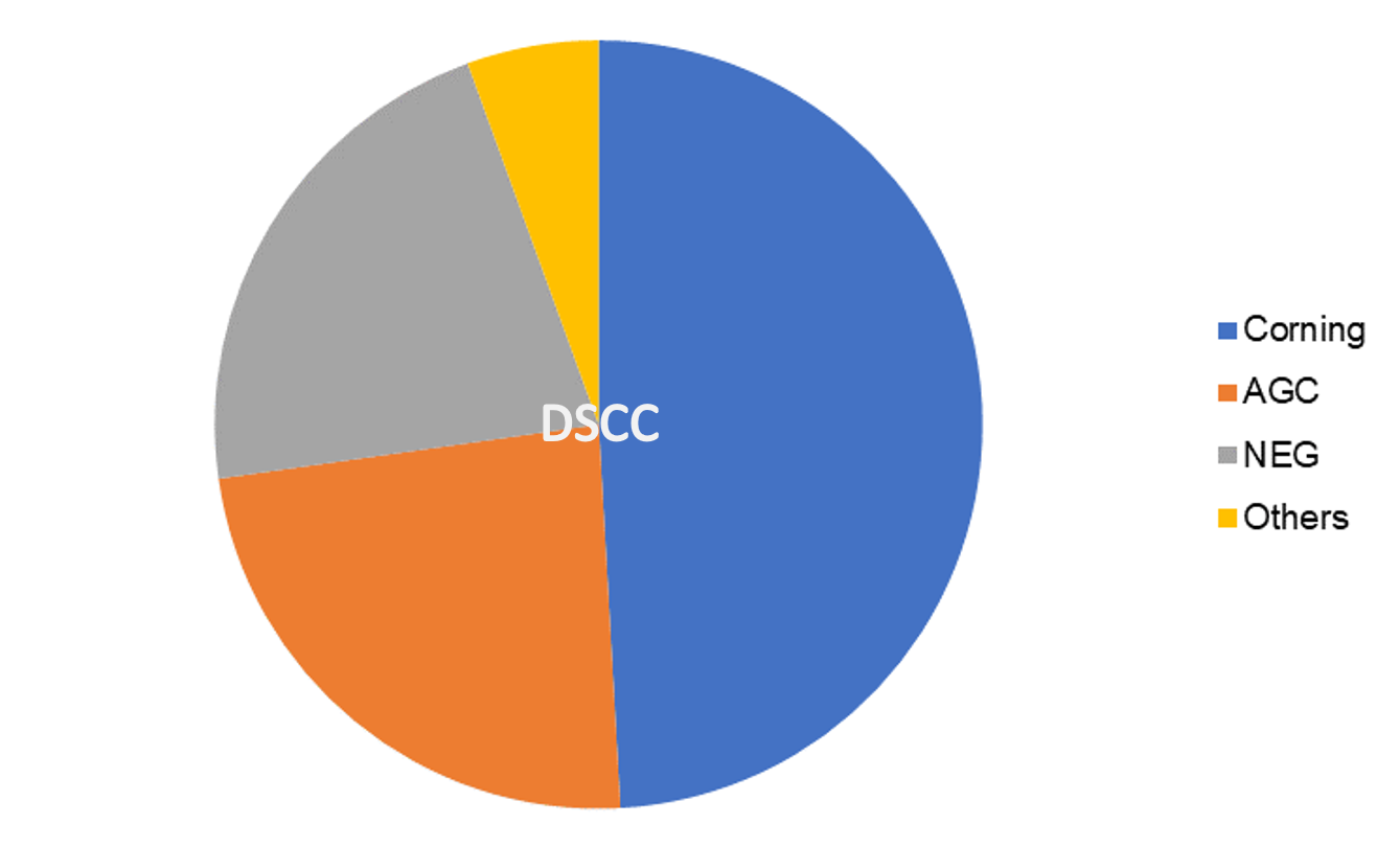

Display Glass Reportは、すべてのLCDおよびOLEDディスプレイ生産ラインを対象に、主要ガラスメーカー全社のガラス能力と出荷を追跡している。DSCCが誇る、ディスプレイ業界の能力と稼働率に関する包括的インサイトと、FPD用ガラスとそのサプライチェーンに関する深い理解を組み合わせたレポートである。レポートでは、FPD用ガラス生産4ヵ国 (日本、中国、台湾、韓国) それぞれの能力を概説するとともに、第1世代から第10.5世代までガラス出荷を追跡している。さらに、ディスプレイ業界向けの3大サプライヤーであるCorning、AGC、NEGと、その他のガラスメーカーからのガラス出荷について詳しく解説している。レポートには、パネルメーカー26社を対象とした調達相関図も掲載している。

業界全体のFPD用ガラス能力に目を向けると、Q4’21は前期と変わらず1億8000万㎡だった。Corningが北京の同社施設の停電から回復した一方で台湾と韓国ではタンクを修理したことによる。DSCCの推定では、2021年のガラス能力は前年比9%増の7億1200万㎡に到達、中国に第10.5世代ラインを追加したCorningが最大の成長率を記録している。

Display Glass Shipments Hit New Record in 2021, Continuing Strong in Q1’22

Pulled by strong demand for large-screen LCD panels, display glass shipments increased by 13% in 2021 to an all-time high of 687M square meters, according to the latest update to DSCC’s Quarterly Display Glass Report (一部実データ付きサンプルをお送りします), released last week. Glass makers shipped 174.5M square meters of display glass in Q4’21, a 2% decrease Q/Q. Shipments are expected to increase by 1% Q/Q in Q1’22 to 176M square meters as higher capacity offsets slower panel maker utilizations.

The Display Glass Report tracks glass capacity and shipments for all major glass makers across all LCD and OLED display fabs. The report combines DSCC’s comprehensive insight into industry capacity and utilization with an in-depth understanding of display glass and the supply chain. The report outlines capacity by region in each of the four countries of display glass production: Japan, China, Taiwan and Korea, and covers glass shipments in Gen sizes from 1 to 10.5. The report details glass shipments for the three major suppliers to the display industry, Corning, AGC and NEG, along with other glass suppliers. The report includes a supply matrix covering 26 panel makers.

Industry Capacity for display glass was flat Q/Q in Q4’21 at 180M square meters as Corning recovered from a power outage at its Beijing facility but repaired tanks in Taiwan/Korea. DSCC estimates that glass capacity in 2021 increased by 9% compared to 2020 to 712M square meters, with Corning showing the biggest increase based on Gen 10.5 additions in China.

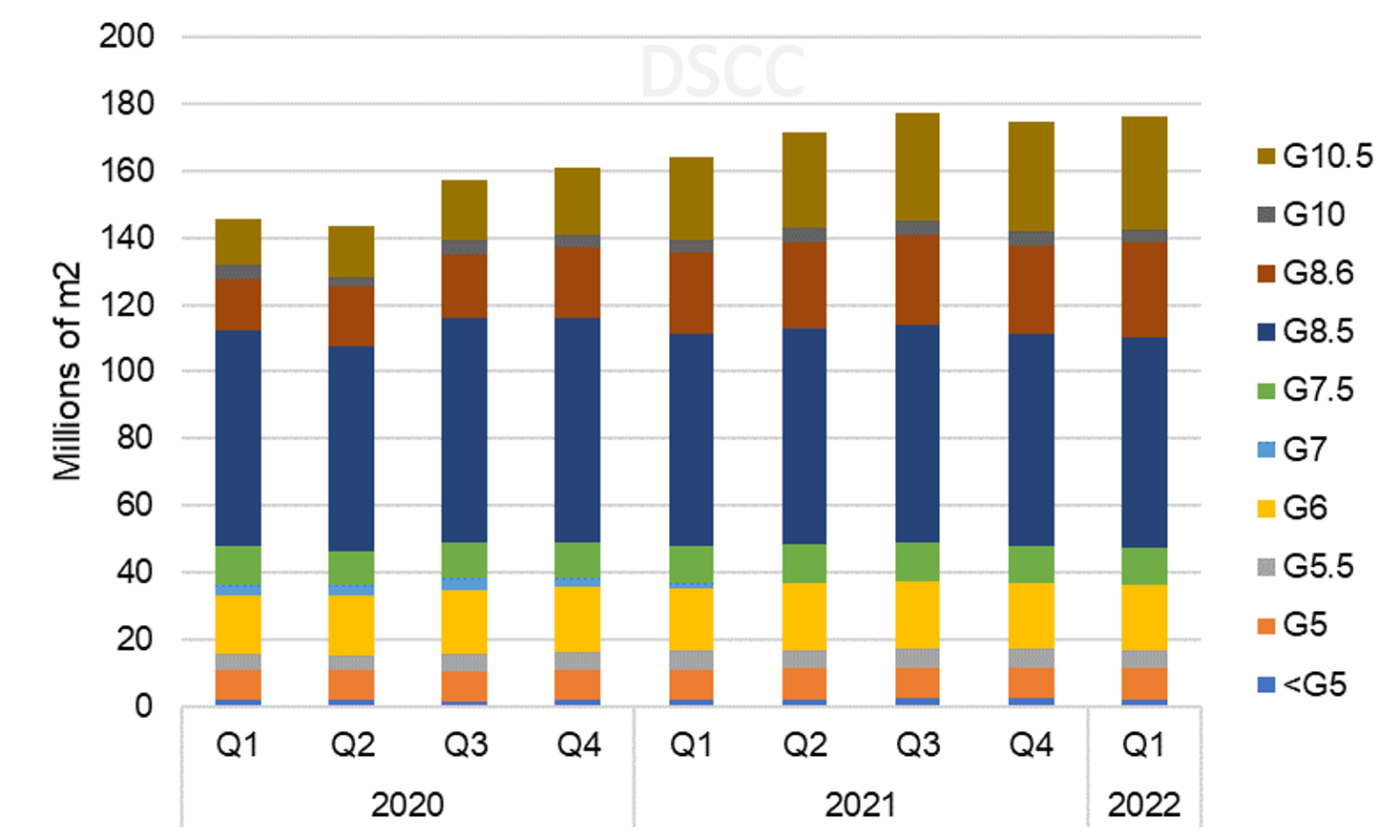

Display Glass Shipments by Gen Size, 2020-2022

Looking at the glass market by gen size in the first chart here, the market in Q4’21 was down 2% Q/Q overall with some slowdown in Gen 8.5 and Gen 8.6 as panel makers attempted to alleviate price declines (without success). While Gen 8.5 glass represented more than half of the industry in 2018, the share of Gen 8.5 in the industry is declining, and growth is coming from Gen 8.6 and Gen 10.5 glass added in China. Gen 8.5 represented only 36% of glass demand in Q4’21, while Gen 10.5 glass increased its share to 19%. Glass shipments in Q1’22 are expected to increase by 1% Q/Q and 7% Y/Y, with increases concentrated in Gen 8.6 and Gen 10.5.

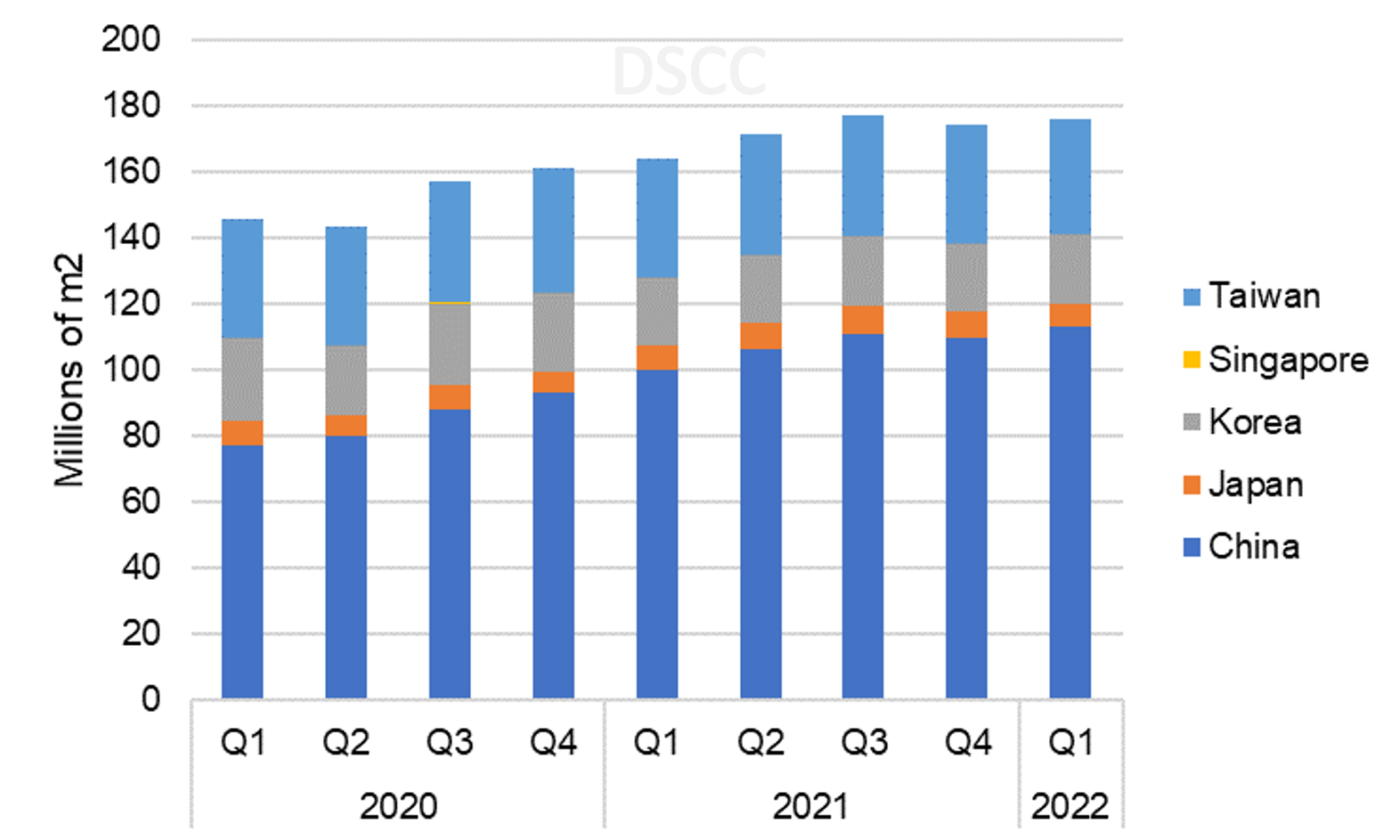

A view of the market by region demonstrates the increasing dominance of the display industry by China panel makers. China’s share of the display glass market was only 40% in Q1’18 but will increase to 64% in Q1 2022; Korea’s share was 27% at the beginning of 2018 but will decline to only 12% in the first quarter of this year.

Display Glass Market by Region, 2020-2022

The report gives a split of the glass market by backplane type, showing the importance of more advanced backplanes in the display industry. Both Corning and AGC in 2019 announced new glass products designed for use in oxide TFT fabs, and those two makers plus NEG have special glass products focused on LTPS backplanes. Despite the growth of OLED, the industry workhorse amorphous silicon (a-Si) glass substrates continue to make up close to 90% of display glass demand, and this share is declining but slowly because of high fab utilization and continued a-Si additions in Gen 10.5 fabs.

The report provides tables of glass prices by Gen size for a-Si and LTPS glass. Glass is priced in Japanese yen across the industry, and while glass prices in the display industry vary by volume and by customer, the report provides average prices. High volume customers with strategic relationships (NEG: LGD, AGC: CSOT, Corning: Samsung, BOE) get the lowest prices, slightly lower than the average, while lower volume customers get higher prices. Glass prices in Q4 2021 averaged ¥1174 (US$10.67) per square meter, up 6% in yen terms Y/Y, but down 3% in US dollar terms as the yen weakened during 2021. Since LCD panels are priced in dollars, the dollar equivalent may be more meaningful to panel makers and may have made the (yen-based) price increases of 2021 more palatable.

The resulting outlook for industry revenues is shown in the final chart here, with revenues by glass maker in Q4 2021. Note that for glass joint ventures, we attribute revenues to the company with melting and forming. NEG has a joint venture with Tunghsu and Corning has a JV with Irico, and we attribute revenues from these JVs to NEG and Corning, respectively.

We estimate that total industry revenues in Q4’21 increased 1% Q/Q and 15% Y/Y to ¥202B. With glass prices stable in the current quarter and volume increasing, we expect industry revenues in Q1 2022 to increase 1% Q/Q and 14% Y/Y to ¥204B.

Display Glass Revenues by Manufacturer, Q4 2021