第8.7世代IT用OLED/第6世代新技術投資がFPD設備投資をけん引

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

第8.7世代IT用OLED、第6世代新技術投資がFPD設備投資をけん引

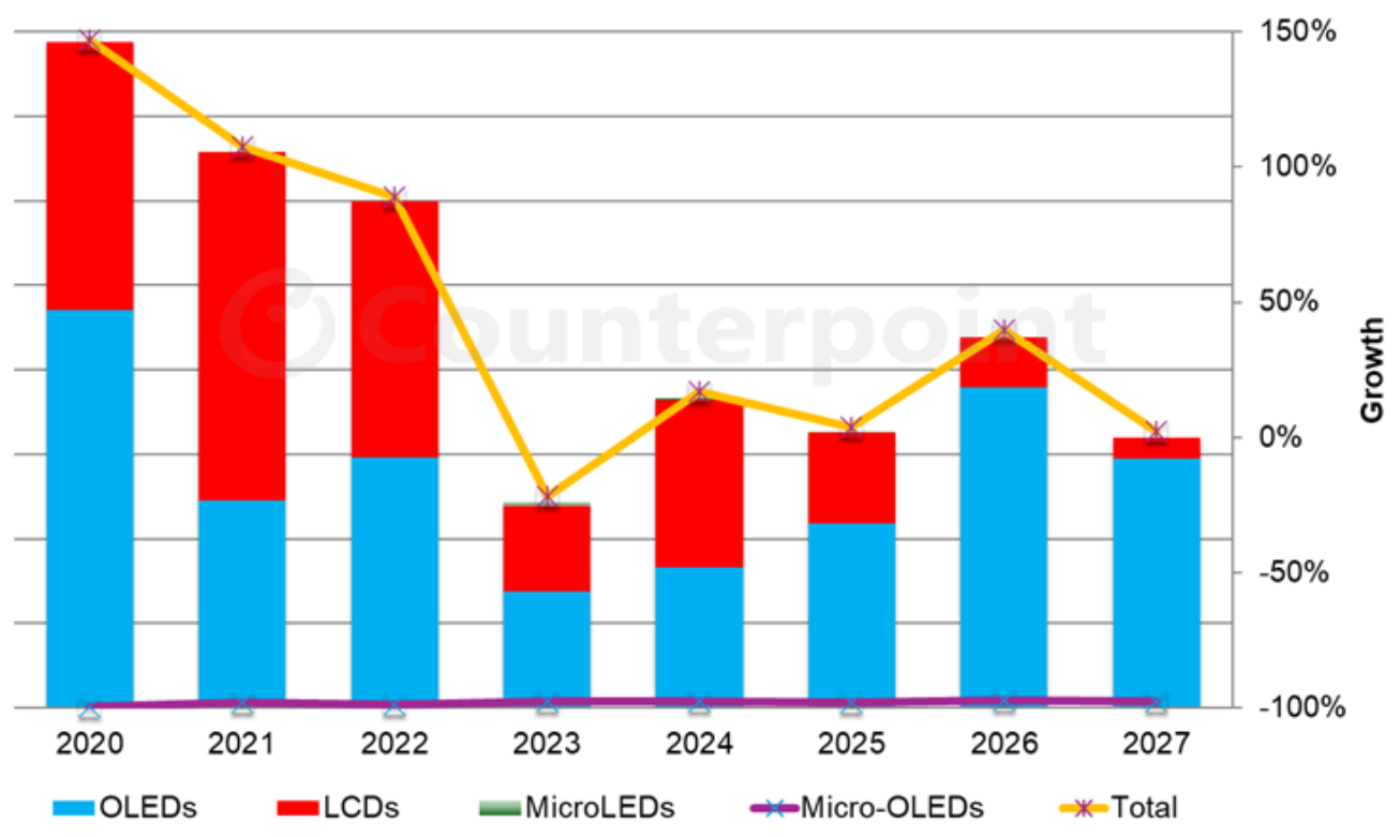

Counterpoint Researchの Quarterly Display Capex and Equipment Market Share Report 最新版の予測によると、2020年-2027年のFPD設備投資は758億ドルになると見込まれており、これは前四半期の予測から1.7%の引き下げとなる。

2025年はOLED設備投資が前年比31%増の43億ドルに増加する見込みの一方、LCD設備投資は前年比45%減の22億ドルに減少すると見られている。

2025年から2027年にかけて、新世代の第8.7世代IT用OLEDと第6世代技術により、OLEDが総投資額の80%を占めると予測されている。一方、LCDは17%を占める見込みである。

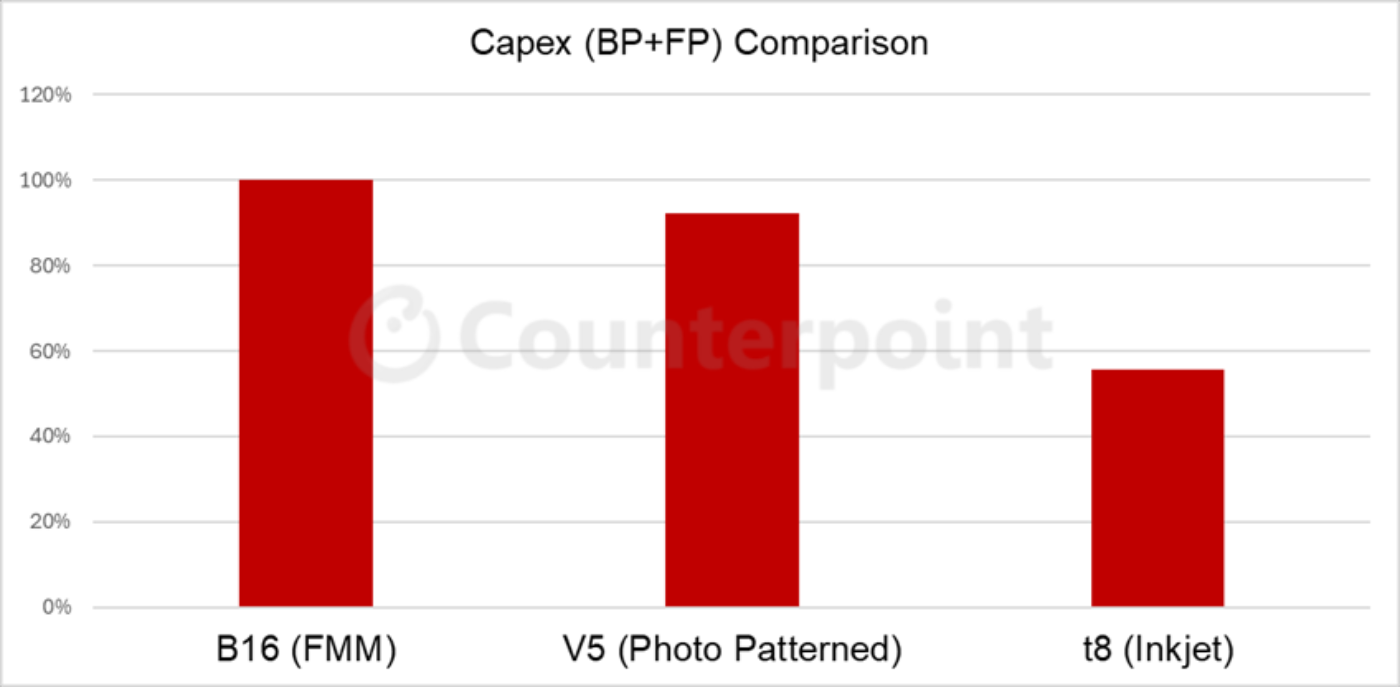

これまで、第6世代 (1500×1850 mm) 生産ラインを保有するOLEDメーカーの大半は、歩留まりの安定とファインメタルマスク (FMM) 技術の進展を背景に、成膜方式を変更することなく第8.7世代 (2290×2620 mm) へと拡張してきた。

FPD技術別 設備投資推移 (装置導入ベース)

しかし、中国の第8.7世代FPDメーカーは、FMM以外の技術を採用する方向に進んでいる。VisionoxのV5ラインはフォトパターニングOLED技術を採用しており、CSOTのt8ラインはRGBインクジェットOLEDを採用する見込みである。従来のFMMとは異なり、この蒸着方法の変更は、次世代OLEDにおける競争優位性とコスト優位性を両立させるための取り組みと見られている。

Counterpoint ResearchではQ4'23にFMMとマスクレスの蒸着法比較を行っている。 Quarterly Display Capex and Equipment Market Share Report Q3'25版には、FMM、マスクレス (フォトパターン) 、RGBインクジェットの各技術の最新情報に基づく設備投資比較を掲載している。

Q3'25版レポートでは、各技術の設備投資、メリットとデメリット、採用の背景についてさらに詳しく解説している。

プロセス別 設備投資比較

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Gen 8.7 IT OLED, Gen 6 New Technology Investments Drive Display Equipment Spending

Display equipment spending for the 2020-2027 period is expected to reach $75.8 billion, a 1.7% decrease compared to the previous quarter’s estimate, according to Counterpoint Research’s latest Quarterly Display Capex and Equipment Market Share Report.

For 2025, OLED spending is expected to increase by 31% YoY to $4.3 billion, while LCD spending is expected to decrease by 45% YoY to $2.2 billion.

From 2025 to 2027, OLED is forecasted to account for 80% of total investments, driven by new Gen 8.7 IT OLED and Gen 6 technologies, while LCD is expected to represent 17%.

Until now, most OLED manufacturers with Gen 6 (1500x1850 mm) fabs have expanded to Gen 8.7 (2290x2620 mm) without changing the method of deposition, backed by stable yields and advancements in Fine Metal Mask (FMM) technology.

However, China’s Gen 8.7 panel suppliers are looking to adopt technologies other than FMM. Visionox’s V5 fab has select ed Photo Patterned OLED technology, while CSOT’s t8 line is likely to adopt RGB Inkjet OLED. Unlike conventional FMM, this shift in evaporation methods is seen as an effort to secure both a competitive edge and cost advantages for next-generation OLED panels.

Counterpoint Research compared FMM and mask-less evaporation methods in Q4 2023. In the Quarterly Display Capex and Equipment Market Share Report for Q3 2025, it provides an updated comparison of capex among FMM, mask-less (Photo Patterned) and RGB inkjet technologies.

The capex, advantages and disadvantages, as well as the background for the adoption of each technology, are discussed in greater detail in the Q3 2025 report.

The report tracks equipment revenues for over 70 different display equipment segments, with market share provided for each one. Over 170 different equipment supplies are identified with design wins by segment.