世界OLED蒸着材料市場に変化の兆し、中国企業が躍進

出典調査レポート Semi-Annual AMOLED Materials Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

- 世界OLED蒸着材料市場の2025年出荷額は前年比約7%増の成長が見込まれている。

- 中国のOLED蒸着材料メーカーの2025年出荷額は前年比21%増になると予測されている。中国FPDメーカー向け材料出荷額における中国OLED蒸着材料メーカーのシェアは2029年に43%到達が見込まれている。

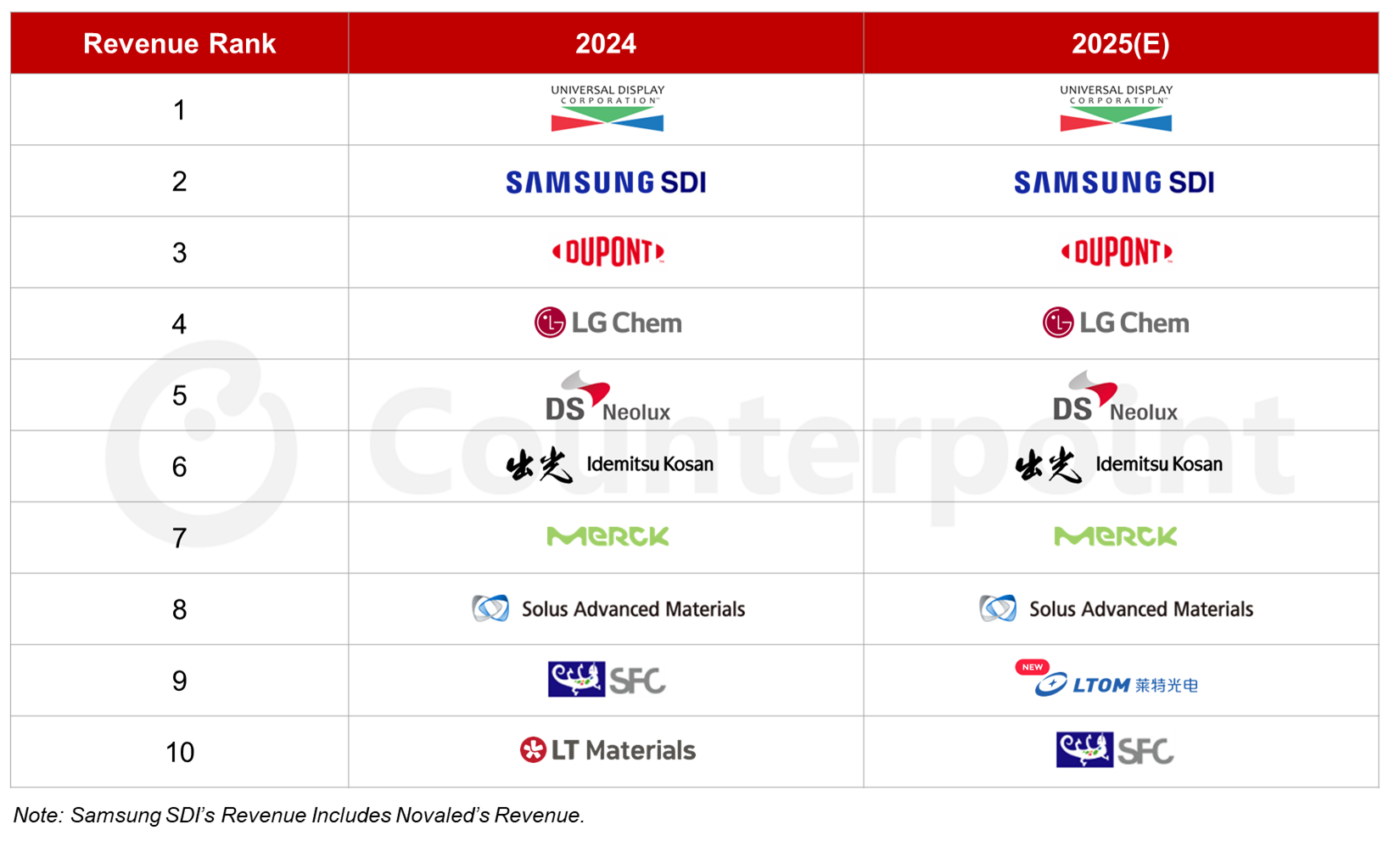

- 2025年にはLTOMが中国OLED蒸着材料メーカーで初めてトップ10入りすると予測されている。

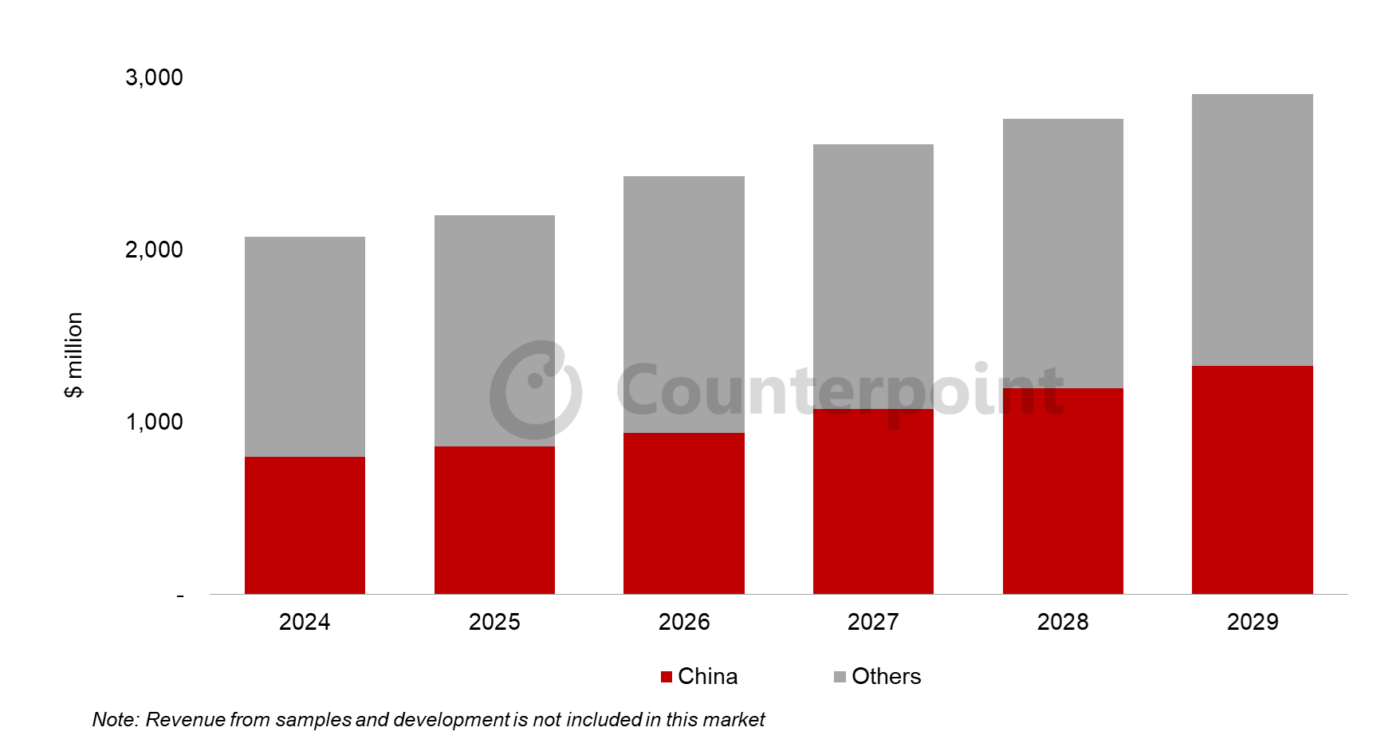

世界OLED蒸着材料市場の出荷額は2025年に前年比約7%の成長が見込まれ、2029年までに年平均成長率7%で増加し約280億ドルに到達すると予測されている。Counterpoint Researchが Semi-Annual AMOLED Materials Report 最新版で明らかにしている。

この市場成長のおもな要因として以下の3つが挙げられる。(1) 中国FPDメーカーが引き続き高稼働率を維持していることに加え、第6世代OLED生産能力の拡大が継続していること。(2) ノートPCおよびタブレット市場でのOLED採用拡大を背景に、第8世代IT用OLEDラインが間もなく量産を開始する見込みであること。(3) 2スタックタンデム構造のIT用OLED、4スタック白色OLED、5スタックQD-OLEDなど、高性能OLED材料構造が製品に採用されるにしたがい、RGB発光材料の使用増加が予想されること。

特に、第8世代IT用OLED生産ラインの大半は2層スタックタンデム構造を前提に設計されている。顧客獲得が成功した場合、OLED蒸着材料の使用が拡大し、OLED蒸着材料市場の成長率もさらに上昇すると考えられる。

AMOLED蒸着材料市場出荷額の推移

市場動向で最も注目すべきは、中国OLED蒸着材料メーカーの成長である。同レポートでは、有望な中国OLED蒸着材料メーカー9社のの2024年業績分析および2029年までの販売動向予測も提供している。

レポートでは、中国のOLED蒸着材料需要は2029年に世界需要の46%を占めると予測されている。

2024年現在、中国FPDメーカー向け材料出荷額における中国OLED蒸着材料メーカーのシェアは約33%である。2029年にはこれが43%まで拡大すると予測されている。特筆すべきは、中国OLED蒸着材料メーカーが、かつては参入が難しかった高価格帯OLED蒸着材料分野で徐々に技術力を確立している点である。なかでもLTOMは2025年に中国OLED蒸着材料メーカーで初めての世界トップ10入りが見込まれている。

AMOLED蒸着材料メーカー上位10社 (出荷額ベース)

既存の中国OLED蒸着材料メーカーがおもに一般的なレイヤー材料を扱っているのに対し、LTOMは緑色ホストやR-プライムHTLといった高付加価値の発光材料や機能性材料をBOEに供給している。最近では、中国国内の他のFPDメーカーへも供給を拡大しており、次世代OLED向けの新素材であるG-プライムHTLや赤色ホストの開発にも積極的に取り組んでいる。

他に注目すべき企業として挙げられるのがSummer Sproutである。同社は、p-ドーパント、赤色ドーパント、緑色ドーパントなど、高難易度で高コストの材料を中国の主要FPDメーカーに供給することに成功している。これらの材料は技術的障壁が高く、UDCやNovaledといったグローバル企業による寡占状態が続いていた。Summer Sproutが供給量を拡大し顧客をさらに獲得できれば、2027年にはLTOMに次ぐ第2位の販売を達成する急成長が見込まれる。

シニアアナリストのKyle Jangは「中国企業製のOLED蒸着材料はこれまで、おもに国内市場向け製品に使用されてきた。しかし2024年以降、一部がグローバルモデルに採用され始めており、世界市場におけるシェア拡大は今後本格化していくだろう」とコメントしている。

Kyle Jangはさらに「中国AMOLED蒸着材料メーカーが特許ライセンス契約やグローバル材料メーカーとの協業を通じて技術力を向上させることができれば、将来的には市場構造が大幅に変化する可能性もある」と述べている。

------------------------------------

Counterpoint Researchの Semi-Annual AMOLED Materials Report は、OLEDメーカーと材料メーカーが量産に採用している主要OLED蒸着材料構造をレイヤー別に網羅するとともに、燐光青色やTADF、ハイパー蛍光など次世代OLED材料技術の最新動向も取り上げています。また、タンデム構造、インクジェット印刷、OPD (有機光検出器)、CoE (カプセル化カラー) など、OLED材料に関連するその他の重要課題や技術についても考察しています。

付属のExcelデータベースでは、FPDメーカー、主要企業 (中国OLED蒸着材料メーカー9 社を含む) 、材料タイプ、技術タイプ別の市場実績と材料使用の分析、2029年までの予測を含む詳細データを提供しています。

出典調査レポート Semi-Annual AMOLED Materials Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Signs of Change in Global OLED Evaporation Material Market as Chinese Companies Forge Ahead

- The global OLED evaporation material market’s revenue is expected to grow around 7% YoY in 2025.

- Chinese OLED evaporation material companies’ revenues are expected to grow 21% YoY in 2025. Their share of materials revenue from Chinese panel makers is forecast to reach 43% in 2029.

- In 2025, LTOM is expected to become the first Chinese OLED evaporation material company to enter the top 10.

The international OLED evaporation material market’s revenue is expected to grow around 7% YoY in 2025, according to Counterpoint Research’s latest Semi-Annual AMOLED Materials Report. It is projected to reach around $28 billion by 2029 at a compound annual growth rate (CAGR) of 7%.

There are three main factors behind this market growth: (1) Chinese panel makers continue to operate at high utilization rates, along with the continued expansion of sixth-generation OLED production capacity. (2) Eighth-generation IT OLED lines will soon start mass production against the backdrop of rising OLED adoption in the notebook and tablet markets. (3) With high-performance OLED material structures, such as two-stack tandem IT OLED, four-stack WOLED and five-stack QD-OLED, being applied to products, the use of RGB-emitting materials is expected to rise.

In particular, most eighth-generation IT OLED production lines are designed with two-stack tandem structures in mind. If customer acquisition is successful, the usage of OLED deposition materials is expected to expand, further increasing the OLED evaporation material market’s growth rate.

Among these developments, the most notable is the growth of Chinese OLED evaporation material companies. The abovementioned report includes an analysis of the 2024 performance of nine promising Chinese OLED evaporation material companies and their projected sales trends through 2029.

According to the report, China's OLED evaporation material demand is expected to account for 46% of the global demand by 2029.

As of 2024, Chinese OLED evaporation material companies’ share of materials revenue from Chinese panel makers was about 33%. It is expected to expand to 43% by 2029. In particular, Chinese OLED evaporation material companies are gradually securing technological capabilities in the high-price OLED evaporation material segment, which had been difficult to enter in the past. Among them, LTOM is expected to become the first Chinese OLED evaporation material company to enter the global top 10 in 2025.

Unlike existing Chinese OLED evaporation material companies that mainly deal with common layer materials, LTOM supplies high-value-added emission and functional materials such as Green Host and R-prime HTL to BOE. Recently, it has expanded its supplies to other panel makers in China, and is also actively developing G-prime HTL, Red Host, and new materials for next-generation OLEDs.

Another noteworthy company is Summer Sprout. This company has succeeded in supplying high-difficulty, high-cost materials such as p-dopant, red dopant and green dopant to major Chinese panel makers. These materials had been monopolized by a few global companies such as UDC and Novaled due to high technological barriers. If Summer Sprout expands its supply volume and secures additional customers, it is expected to show rapid growth and achieve the second-highest sales after LTOM by 2027.

Senior Analyst Kyle Jang said, “Until now, OLED evaporation materials from Chinese companies have mostly been used in products for the domestic market. But since 2024, some have begun to be adopted in global models, and global market share expansion will begin in earnest.”

Jang added, “If Chinese OLED evaporation material companies improve their technology through patent licensing pacts or collaboration with global material companies, the market landscape could change significantly in the future.”

Counterpoint Research’s Semi-Annual AMOLED Materials Report covers not only major OLED evaporation material structures currently applied in mass production by OLED panel makers and material suppliers by layer, but also trends in next-generation OLED material technology, including Phosphorescent Blue, TADF and Hyperfluorescence. The report also addresses other important issues and technologies related to OLED materials, like tandem structures, inkjet printing, organic photodetectors (OPD) and Color on Encapsulation (CoE).

In addition, the accompanying Excel report provides a detailed analysis of market performance and material usage by panel maker, major companies (including nine Chinese OLED evaporation material makers), material type and technology type, along with forecasts through 2029.