FPD需給予測~FPDの供給過剰が終息へ、LCDは供給不足の兆し

出典調査レポート「田村喜男の『季刊 FPD需給観測 (市場総論) レポート&データベース』&解説動画 (約90分間)+お客様個別の質疑応答WEB会議※オプション」の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

FPD需給予測~FPDの供給過剰が終息へ、LCDは供給不足の兆し

パンデミックによる需要急増時に増強された生産能力はFPD業界に構造的な供給過剰をもたらし、その状況は2025年も続いている。しかし、長期的な需要の推進要因が引き続き作用することで、こうした供給過剰はやがて供給不足へと転じる見通しだ。その転換点は、Counterpoint Researchが先週発刊した 田村喜男の「季刊 FPD需給観測 (市場総論) レポート&データベース」の予測期間である5年以内に起こると見られている。FPD製品需要は緩やかな成長にとどまると予測されるが、その持続的な成長によって既存の生産能力が満たされ、いずれは新たなLCD生産ラインの建設や拡張の需要をもたらすだろう。

田村喜男の「季刊 FPD需給観測 (市場総論) レポート&データベース」は需要と供給の両面を対象にFPD業界の包括的見解を提供している。同レポートの需要予測はCounterpoint Researchの Quarterly FPD Forecast Report と同様に、8用途のFPD出荷をLCDとOLEDの各技術別に予測している。レポートでは、2018年から2029年までの全用途向けの出荷数、出荷面積、出荷額の実績と予測を提供している。

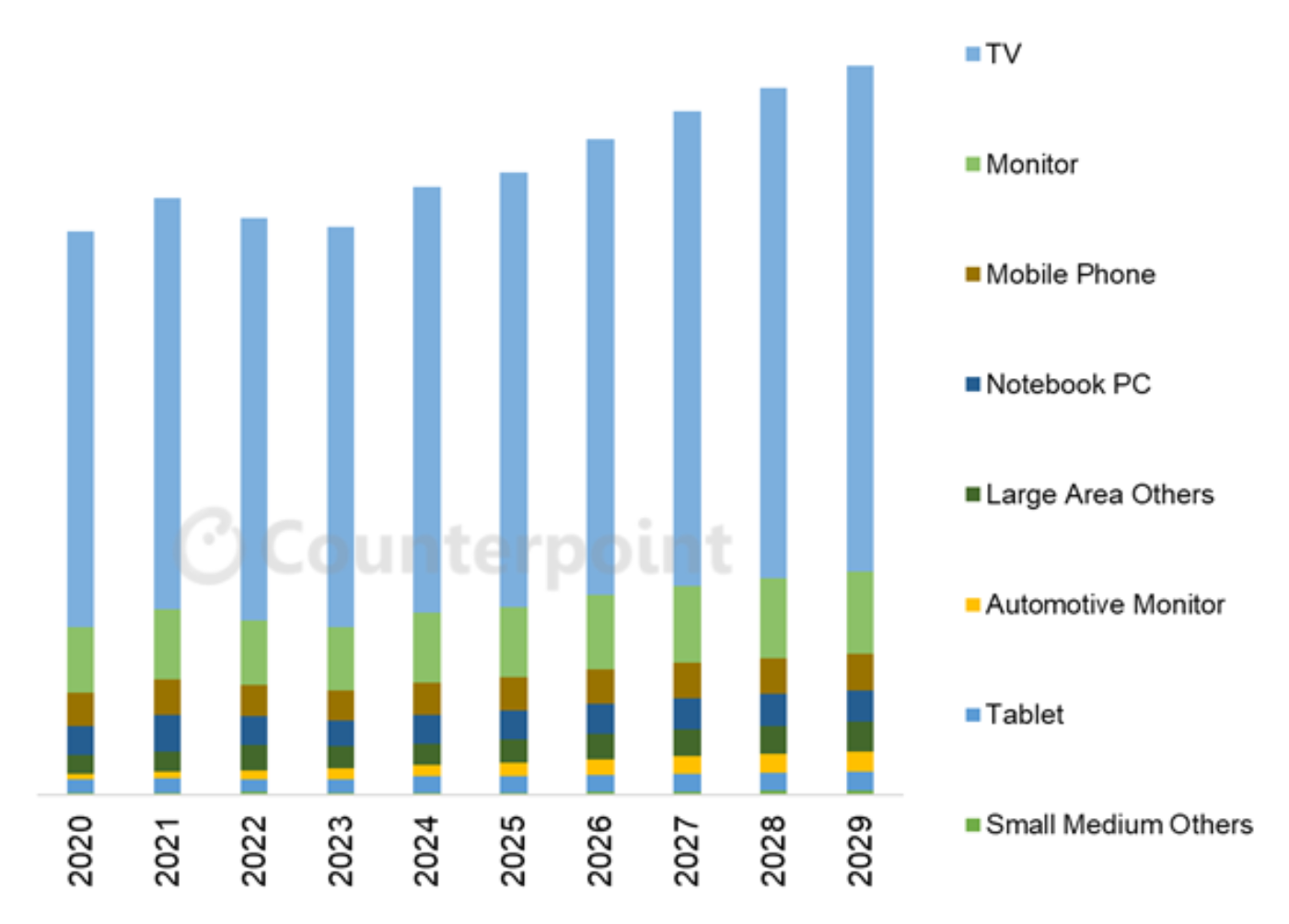

FPD業界を理解する上で出荷数と出荷額は重要だが、需給を把握する上で最も重要な意味を持つのが面積だ。一つ目のグラフは用途別FPD面積需要の長期予測を示している。2022年と2023年はパンデミックの余波でFPDの面積需要が2年連続で減少したが、その後2024年になって7%増で成長が再開しており、これが2029年まで継続すると予測される。2023年-2029年の年平均成長率は4%になる見通しだ。

4%という面積需要の年平均成長率は楽観的すぎると思うかもしれないが、その出発点はパンデミック後の低迷期である2023年であることを考慮していただきたい。レポートに掲載の期間全体、すなわちパンデミック前の2018年から2029年までの期間の年平均成長率はわずか3%である。

TVがFPD需要の大部分を占める状況は今後も変わらず、TVの面積需要は平均画面サイズの拡大と数量の増加にともなって成長していくと見られる。TV用パネルの出荷数成長率は年1%と見込まれ、平均画面サイズは2023年から2029年の間に4.4インチ拡大すると予測される。また、IT市場がパンデミック後の低迷から回復するにしたがい、IT用途 (モニター、ノートPC、タブレット) の面積成長も期待される。

用途別 FPD需要予測 (面積ベース)

OLEDは全用途でシェアを拡大し、OLEDの面積需要はFPD市場全体よりも高い成長率を示すと予測されるが、LCDの成長についても十分な需要の伸びが見込まれる。LCDの面積需要は2023年から2029年にかけて年平均成長率4%で伸び、OLEDの面積需要は年平均成長率12%で伸びると予測される。

LCD需要は引き続きTVが主流である一方、OLED需要はTV、スマートフォン、IT製品など多岐にわたり、成長に貢献するだろう。2027年のOLED面積需要シェアは、TVが36%、スマートフォンが42%、IT製品が15%となる見通しだ。

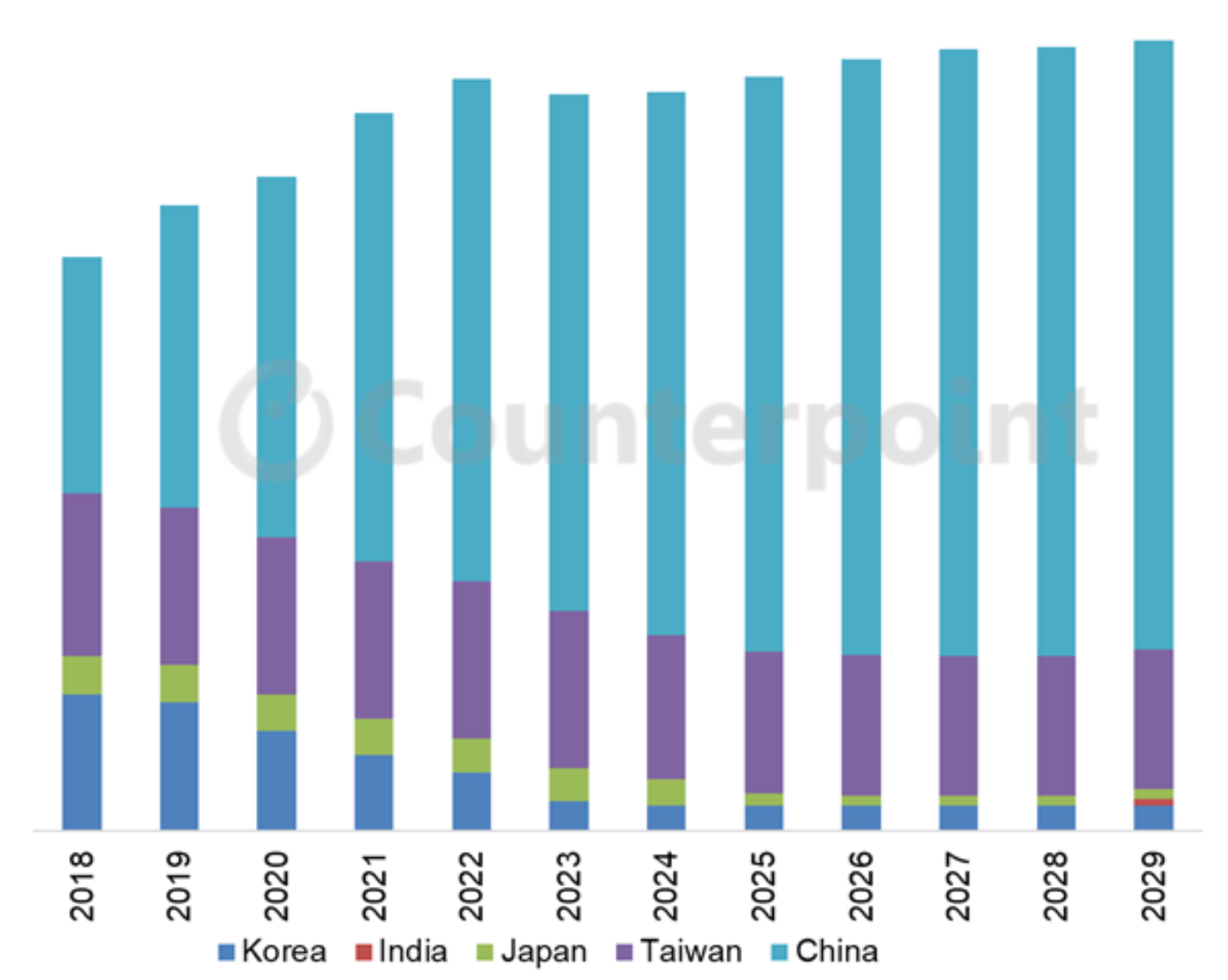

業界の供給側については、 田村喜男の「季刊 FPD需給観測 (市場総論) レポート&データベース」にCounterpoint Researchの詳細な生産能力予測を掲載しており、LCDとOLEDの生産能力見通しを世代別、メーカー別、生産地域別に提示している。この予測はCounterpoint Researchの Quarterly Display Capex and Equipment Market Share Report で提示している内容と同じである。次の図はLCD生産能力予測を生産地域別に示すものである。LCD生産能力は2023年に2%減少した。これは、一部の小規模生産ラインの閉鎖による。2024年には、堺市のSharp第10世代ラインが閉鎖されたにもかかわらず、1%未満の増加を記録したと見られる。

LCD生産能力は全般的にほぼ横ばいで推移する見通しだ。台湾、韓国、日本のLCD生産能力は2022年-2028年の期間に20%減少すると予測している (全体で 20%であり、年平均成長率の数値ではない) 。一方、生産能力の規模がはるかに大きい中国では同期間に18%増が見込まれていることから、業界全体のLCD生産能力は年平均成長率1%で拡大すると予測している。なお、インド初のLCD生産ラインは2029年に稼働を開始すると見られる。

地域別 LCD生産能力予測 (面積ベース)

LCD生産能力が今後4年間ほぼ横ばいで推移すると予測される一方、OLED生産能力は引き続き大幅な増加が見込まれている。近年、JOLEDの日本ラインやAUOのシンガポールラインなど、小規模なOLED生産ラインの閉鎖がいくつかあったが、大規模なOLED生産ラインの閉鎖は発生しておらず、多くの新たなラインが稼働を開始している。OLED生産能力は、2023年-2029年の予測期間において、韓国で年平均成長率3%、中国で同8%となり、総生産能力は同5%での増加が見込まれている。その増加分の大半は、モバイル/IT用途向けのフレキシブルOLEDラインまたはモバイル/IT用途向けの薄膜封止技術を採用したリジッドOLEDラインになると予測される。

需要と供給の両面を組み合わせることで、FPD業界の予想稼働率を算出することができる。本レポートではFPD全体の稼働率に関する見通しを示しているが、グローバルな状況は実際、複数の異なる需要および供給セグメントの総和にすぎない。たとえば、LCDのように供給側が複数の用途間で代替可能である場合、単一の需要/供給の図式で捉えることができる。しかし、供給側が代替不可能である (例:WOLED TVの製造設備はタブレットやスマートフォンに転換できない) 場合には、需要/供給の図式はより細分化されたものになる。本レポートでは、以下のセグメント別に需要/供給の見通しを掲載している。

• LCD全体 (全世代)

• FPD全体 (LCDとOLEDを含む)

• モバイル/IT用OLED

• TV/モニター用OLED

• モバイル/IT用リジッドOLED

• モバイル/IT用フレキシブルOLED

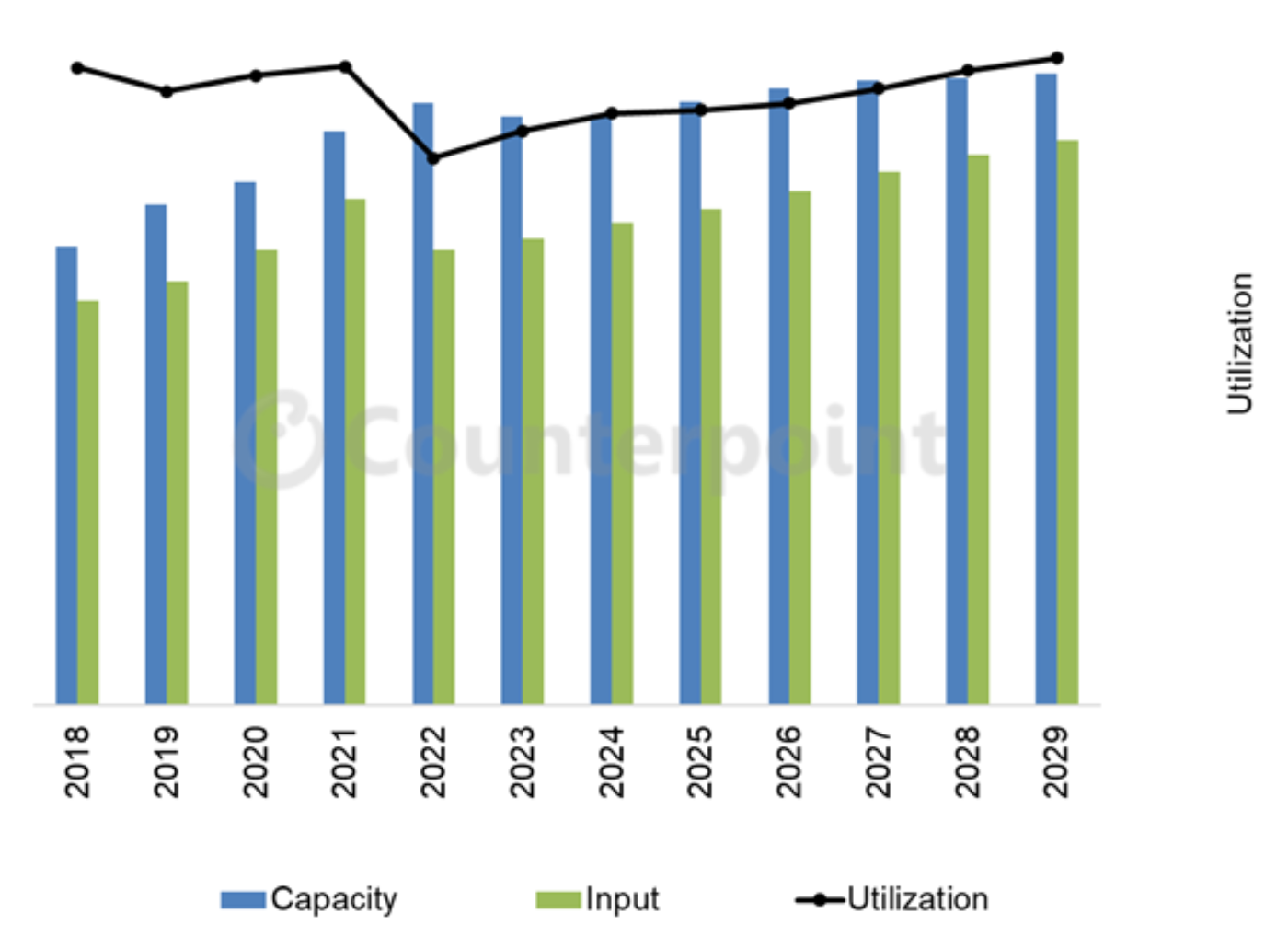

次の図は、全世代を含むLCDの需給状況を示している。LCD業界はパンデミック後のピークを過ぎた2022年に底を打ち、その後は毎年わずかながら改善している。2022年の低稼働率は巨額の営業損失を招いたが、2023年は少し改善し、2024年もさらに改善した。2025年の稼働率は2024年よりやや改善すると予測している。

最小限の生産能力追加と安定した需要の伸びにより、LCDメーカーの収益性は2025年と2026年もさらに改善する見通しだ。現在の需給展望から、2028年の稼働率はパンデミックのピーク年である2021年と同水準になり、2029年にはさらに上昇すると予測している。

LCD需給予測 (面積ベース)

OLED生産能力の追加で需要への対応は可能だろうか?現在の市場では、LCDよりもOLEDへの投資意欲が明らかに高まっている。LCDの供給不足がパネル価格の上昇をもたらす場合 (これは予想される展開だ) 、OLEDは全用途で優位となり、ITおよびTV分野でのOLEDの浸透が加速するだろう。当社の生産能力予測には、LG DisplayまたはSamsung Display、あるいは中国FPDメーカーのいずれも、TV用OLEDの新規ライン建設は織り込まれていない。LCDの供給が逼迫すれば、TV用OLED生産能力への投資が進むことになるかもしれない。

------------------------------------

Counterpoint Researchの 田村喜男の「季刊 FPD需給観測 (市場総論) レポート&データベース」では、8用途を対象としたLCDおよびOLED需要推移を網羅的に提供するとともに、各用途の出荷数、出荷面積、出荷額を予測しています。また、FPD技術別、地域別、世代サイズ別に業界の生産能力を提示し、業界の各セグメントの需要と供給の比較も行っています。

出典調査レポート「田村喜男の『季刊 FPD需給観測 (市場総論) レポート&データベース』&解説動画 (約90分間)+お客様個別の質疑応答WEB会議※オプション」の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] End of FPD Oversupply in Sight, LCD Shortage on Horizon

Capacity additions put in place during the pandemic demand boom resulted in a systematic oversupply in the display industry that continues in 2025. But as long-term demand drivers continue to play out, that oversupply will eventually turn to a shortage. That turn will happen within the five-year timeframe of the forecast from Counterpoint Research’s Quarterly FPD Supply/Demand Report, released last week. Although we expect only modest growth in demand for display products, that persistent growth will fill up capacity and eventually lead to demand for new or expanded LCD fabs.

The Quarterly FPD Supply/Demand Report gives a comprehensive view of the display industry because it covers both the demand and supply sides. The demand forecast, which is the same forecast as in Counterpoint Research’s Quarterly FPD Forecast Report, covers flat panel display (FPD) shipments across eight different applications, with technology split between LCD and OLED. The report includes units, area and revenue history and forecasts for all applications from 2018 to 2029.

While units and revenue are important to understand the display industry, the most meaningful metric for supply/demand is area. The first chart here shows our long-term forecast for display demand area by application. After two consecutive years of pandemic hangover where FPD demand area decreased in 2022-2023, growth resumed in 2024 with a 7% increase and we expect it to continue through 2029 with a 2023-2029 CAGR of 4%.

If you think a 4% CAGR for area demand is too aggressive, consider that the starting point is the depressed post-pandemic market of 2023. If we consider the whole timescale of the report from pre-pandemic 2018 to 2029, the CAGR is only 3%.

TVs will continue to represent a dominant share of FPD demand. Area demand for TVs will grow primarily from increasing average screen size along with incremental unit growth. We expect unit growth for TV panels at 1% per year and expect that the average size for TV panels will increase by 4.4” from 2023 to 2029. We also expect area growth from IT applications (monitor, notebook, tablet) as the IT market recovers from its post-pandemic trough.

Although we expect OLED to gain share across all applications and expect the OLED demand area to grow faster than the FPD market as a whole, there is enough demand growth to allow LCD to grow. We expect the LCD demand area to grow by a 4% CAGR from 2023 to 2029, while the OLED demand area will grow by a 12% CAGR.

Whereas demand for LCD panel area will continue to be dominated by TVs, the OLED demand area will be more diverse with TVs, smartphones and IT products all contributing to growth. By 2027, we expect TVs to represent 36% of the OLED area, while smartphones will make up 42% and IT products 15%.

Turning to the industry’s supply side, the Quarterly FPD Supply/Demand Report covers Counterpoint’s detailed capacity forecast, giving views of LCD and OLED capacity by Gen Size, by supplier and by production region. This is the same forecast as given in Counterpoint Research’s Quarterly Display Capex and Equipment Market Share Report. The next chart here shows our forecast for LCD capacity by production region. LCD capacity decreased in 2023 by 2%, as some smaller fabs shut down, and increased by less than 1% in 2024 despite the shutdown of Sharp’s Gen 10 fab in Sakai City.

Overall, we expect minimal growth in LCD capacity. We expect that LCD capacity in Taiwan, South Korea and Japan will decrease by 20% over the 2023-2029 period (20% in total, not a CAGR). The much larger capacity in China will grow by 18% over the same period, so the overall LCD capacity of the industry will grow at a 1% CAGR. Note that we do expect the first LCD fab in India to come online in 2029.

While LCD capacity will be close to flat over the next four years, we expect OLED capacity to continue to increase substantially. While there have been a few small OLED fabs closed in recent years, such as JOLED’s lines in Japan and AUO’s lines in Singapore, there have not been any larger OLED fabs closed and many more fabs have started. OLED capacity will grow at a 3% CAGR in South Korea and at an 8% CAGR in China over the forecast period (2023-2029), with total OLED capacity growing at a 5% CAGR. Almost all of that growth will come from flexible OLED lines for mobile/IT applications or from rigid OLED lines with thin-film encapsulation for mobile/IT applications.

Putting the supply and demand pieces together, we can calculate the expected capacity utilization for the display industry. While the report includes a view of FPD utilization as a whole, the global picture is really just the sum of several different supply/demand segments. Where the supply side can be fungible across applications, such as in LCD, there can be a single supply/demand picture, but when the supply side cannot be fungible (for example, WOLED TV production cannot make tablets or smartphones), the supply/demand picture becomes more fragmented. The report includes separate Supply/Demand views for the following segments:

• LCD in aggregate across all gen sizes

• FPD in aggregate, including LCD and OLED

• Mobile/IT OLED

• TV/Monitor OLED

• Mobile/IT Rigid OLED

• Mobile/IT Flexible OLED

An example is included as the next chart here, showing the supply/demand picture for LCD across all gen sizes. The LCD industry hit a low point in 2022 following the pandemic high but has improved a bit each year since then. The low utilization in 2022 meant huge operating losses, but 2023 was a little better, and 2024 too was a little better. We expect that 2025 utilization will average slightly better than 2024.

With minimal capacity additions planned and steady demand growth, LCD makers’ profitability is likely to continue to improve in 2025 and 2026. Based on the current supply/demand outlook, we expect utilization in 2028 to be equal to the pandemic peak year UT% in 2021, even higher in 2029.

Could additional OLED capacity meet the demand? In today’s market, there is clearly a greater appetite for investments in OLED than for LCD. If an LCD shortage pushes up panel prices (which is to be expected), that will certainly favor OLED across all applications, leading to faster penetration of OLED in IT and TV. Our capacity outlook includes no new fabs for OLED TV, neither from LG Display nor from Samsung Display or one of the Chinese panel makers. Perhaps an LCD shortage will lead to investments in OLED TV capacity.

As noted above, Counterpoint Research’s Quarterly FPD Supply/Demand Report provides a comprehensive listing of historical panel demand in LCD and OLED for eight different applications, plus a forecast of units, area and revenues for each application. The report gives a view of industry capacity by display technology, region and gen size. It also gives a comparison of supply and demand across industry segments. Readers interested in subscribing to this report should contact info@counterpointresearch.com.