2023年のスマートフォン用OLED出荷額は前年比11%減も、2024年は回復へ

出典調査レポート Quarterly Advanced Smartphone Display Shipment and Technology Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

DSCCが Quarterly Advanced Smartphone Display Shipment and Technology Report 最新版を発刊、スマートフォン用ディスプレイ市場に関する詳細データとインサイトを明らかにした。最新版に追加された新たな章では、カメラ技術と命名法、さらには2024年に向けたGoogleのスマートフォンロードマップも提供しており、同社スマートフォン全モデルで画面サイズが拡大するという。

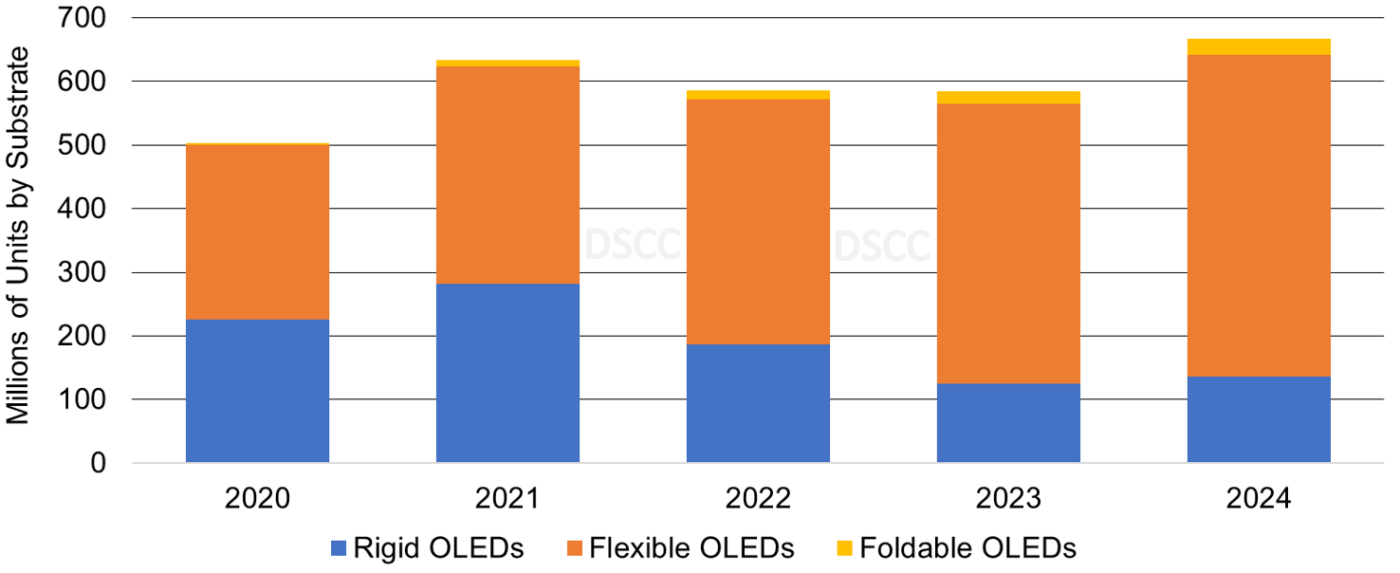

DSCCでは2023年のスマートフォン用OLED出荷数を前年比0.3%減の5億8500万枚、出荷額を前年比11%減の290億ドルと予測している。予測の背景には、パンデミック後の中国の経済再開が予想よりも遅れたこと、2023年上半期の在庫増加、マクロ経済環境といった要因がある。

2023年のフレキシブルOLED出荷数は前年比14%増、パネルのブレンドASP (平均価格) の20%下落によって、出荷額は前年比9%減と予測されている。DSCCのシニアディレクターであるDavid Naranjoは次のように述べている。「DSCC Weekly Review 9月25日号の巻頭記事では、SDCのリジッドOLED事業のシェアを奪うべく、中国系OLEDメーカー各社が2022年に始めたフレキシブルOLEDの思い切った値下げを取り巻く環境について取り上げた。中国系メーカーは確かにシェアを獲得し、SDCのリジッドOLED事業に大きな影響を与えたものの、かなりの財務実績低迷に悩まされることとなった。フレキシブルOLED価格は大幅に低下、SDCのリジッドOLED価格を下回ることさえあり、かなりのボリュームがリジッドOLEDからフレキシブルOLEDに移行することとなった。この記事でも指摘している通り、パネルメーカー各社はQ4’23に約5-10%の上昇を期待している。既存のプロジェクトやブランドの交渉力を考えれば、2023年にはこの上昇の実現は難しいかもしれない。ただし、需要が高まる2024年には現実化の可能性がある」

DSCCでは、フレキシブルOLEDスマートフォンが引き続きシェアを拡大し、数量ベースで2022年の66%から2023年には75%に上昇すると予測している。

DSCC Expects OLED Smartphone Panel Revenues to Decline 11% Y/Y in 2023 with an Expected Recovery in 2024

※ご参考※ 無料翻訳ツール (DeepL)

In the recently released Quarterly Advanced Smartphone Display Shipment and Technology Report, DSCC revealed additional granularity and insights for the smartphone display market. In this issue, a new chapter was added on camera technology and nomenclature as well as Google’s smartphone roadmap through 2024, which shows display sizes increasing for all models.

For 2023, DSCC expects OLED smartphones to decline 0.3% Y/Y to 585M units and decline 11% Y/Y to $29B in panel revenues. This is the result of the slower than expected reopening of China, post-pandemic, elevated inventories during the 1H’23 and the macroeconomic environment.

For 2023, for flexible OLEDs, DSCC expects 14% Y/Y growth with a 9% Y/Y panel revenue decline as a result of blended panel ASPs declining 20%. According to DSCC’s Senior Director David Naranjo, “In the September 25th edition of the DSCC Weekly Review, the lead article highlighted the aggressive flexible OLED panel price cutting environment that started in 2022 by Chinese OLED panel suppliers in order to gain share from SDC’s rigid OLED business. While they did gain share and significantly impacted SDC’s rigid OLED business, they also suffered from very poor financial performance. Flexible OLED prices got so low that they even declined below SDC’s rigid OLED prices which shifted significant volume from rigid to flexible OLEDs. As that article also pointed out, in Q4’23, panel suppliers are looking for around a 5% - 10% increase. This increase may be difficult to achieve in 2023 as a result of existing projects and brands’ bargaining power. However, it may be more achievable in 2024 with demand being higher.”

DSCC expects flexible OLED smartphones to continue to gain share and rise from a 66% unit share in 2022 to a 75% unit share in 2023. The flexible OLED revenue share of the OLED smartphone panel market is expected to rise from 80% in 2022 to an 83% share in 2023. In addition, foldable OLEDs are expected to rise from a 2.6% unit share in 2022 to a 3.4% share in 2023 on 20M panels with the foldable panel revenue share rising from 7% to 10%. DSCC expects rigid OLEDs to experience a 33% Y/Y unit decline and 49% Y/Y panel revenue decline in 2023 causing its share to fall from 32% in 2022 to 21% in 2023, with its revenue share falling from 13% in 2022 to 7% in 2023 with ASPs down 24%.

For 2024, DSCC expects flexible OLED smartphone panels to reach a 76% unit share, and an 81% revenue share as a result of double-digit ASP declines and foldable OLED smartphone panels to reach a 4% unit share and an 11% revenue share. Although rigid OLED excess capacity is being used for IT applications, and rigid OLEDs declined in 2023 by 33% Y/Y, DSCC expects rigid OLEDs to have a 9% Y/Y increase in 2024 on 6% Y/Y ASPs (after falling 24% in 2023) as brands look to recover volume lost in 2023 for entry level price points.

Annual OLED Smartphone Panels by Substrate

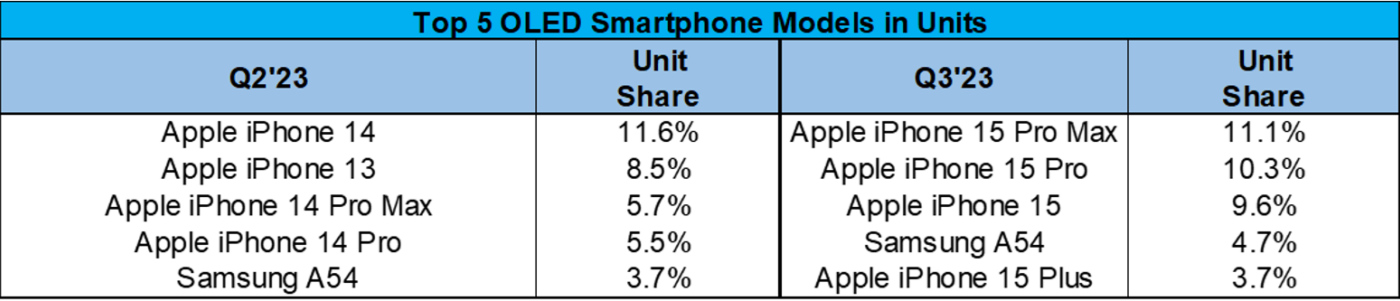

In Q2’23, OLED smartphones were up 6% Q/Q and 4% Y/Y to 138M OLED smartphone panels. The Q/Q and Y/Y increase was the result of the 7% Q/Q increase for flexible OLED panel shipments driven by higher volumes from Honor, Oppo, Vivo and Xiaomi, a 1% Q/Q increase for rigid OLED panels driven by higher volumes from Honor and Vivo and a 60% Q/Q increase for foldable OLED smartphones fueled by Huawei, Samsung, Techno and Xiaomi. In Q2’23, Apple had four of the top five models with the iPhone 14, iPhone 13, iPhone 14 Pro Max and iPhone 14 Pro. The Samsung S23 Ultra was #5. These five models accounted for a 35% unit share and 52% smartphone revenue share.

In Q3’23, DSCC expects a 1% Q/Q and 13% Y/Y increase to 139M panels as a result of significant panel shipments for the iPhone 15 series, triple-digit growth for foldable OLEDs as well as improved inventories and seasonality. In Q3’23, DSCC expects the iPhone 15 Pro Max, iPhone 15 Pro and iPhone 15 to be the top three models accounting for 31% unit share and 47% smartphone revenue share.

Q2’23 and Q3’23 Top 5 Rigid and Flexible OLED Smartphone Panel Procurement by Brand

Readers interested in subscribing to the Quarterly Advanced Smartphone Display Shipment and Technology Report should contact お問い合わせ窓口. This report includes all DSCC’s smartphone data from covering all OLED smartphone and panel shipments by brand, model, all display and major non-display parameters, panel and device revenues and forecasts by quarter and by year through 2027. In addition, it provides insights into technology and innovation trends in OLED display technology, which is applicable to smartphones. There are over 1,300 AMOLED smartphone configurations in our database including variations by substrate, TFT backplane, panel supplier, refresh rate, chipset supplier, 5G networks and much more.

During the Global Display Supply Chain Dynamics & Technology Outlook Conference on November 1, 2023, DSCC will be presenting additional results and the outlook for the smartphone display market.

David Naranjo will be presenting more insights including the smartphone shipments, additional near term forecasts, cost and price outlook, etc., from other reports including the Monthly Flagship Smartphone Tracker and Biannual Smartphone Display Cost Report. He will also highlight which brands and panel suppliers took share in 2023 and are best positioned to gain ground in 2024.

Ross Young will be presenting the latest results and outlook for the foldable and rollable smartphones. He will highlight which brands, models and panel suppliers gained share in 2023 and which are best positioned in 2024. His talk will also examine how the category is likely to evolve, what new products are coming and when Apple is likely to enter the foldable smartphone category.

Rita Li will be presenting and examining the strategy of the Chinese OLED suppliers including technology commercialization plans, capacity, allocation by customer, price trends and cost reduction efforts.

Jeff Fieldhack from Counterpoint Research will examine the latest insights from Counterpoint’s regional smartphone data. Hsi talk will reveal which countries are outperforming and which are underperforming in 2023 and what is expected in 2024. It will also examine other important product and market trends.

For more information, please contact 本セミナー事務局 (Ashton Reagin).

Register here: 本セミナー専用ウェブサイト

※DSCC米国本社の企画であり、日本語の同時通訳・字幕サービスはありません