FPD製造装置メーカー各社の業績分析~厳しいQ1’23を耐え抜く

Published June 26, 2023

Logout

出典調査レポート Quarterly Display Supply Chain Financial Health Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

Q1’23はFPD製造装置メーカーにとって厳しい四半期となった。DSCCの Quarterly Display Supply Chain Financial Health Report にて以下のような状況が明らかになった。

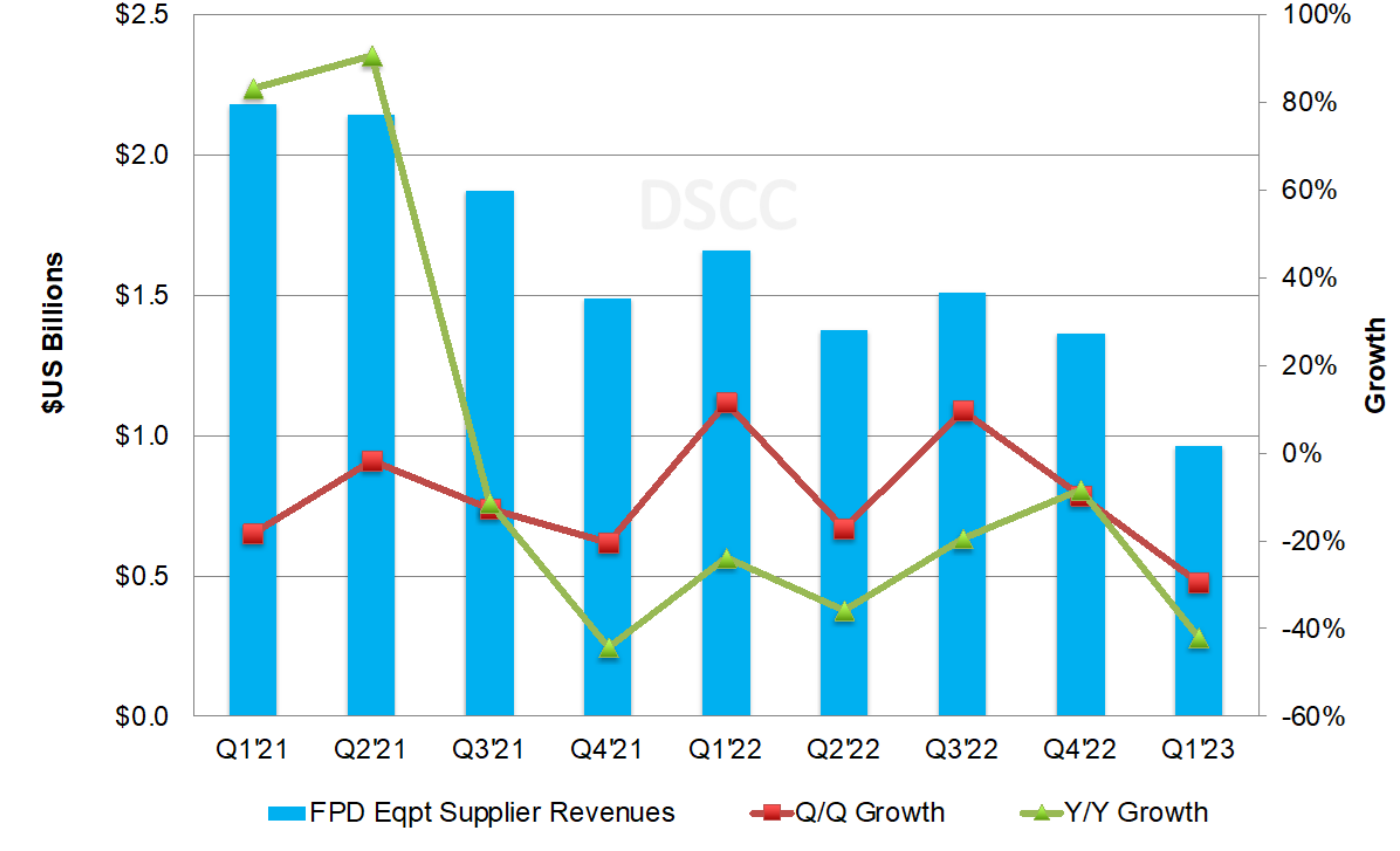

- 大手メーカー16社 (Applied Materials, AP Systems, Avaco, Canon, DMS, HB Solution, HB Technology, ICD, Jusung Engineering, KC, Nikon, SCREEN, Tokyo Electron, ULVAC, V Technology and Wonik IPS) のFPD製造装置売上は前期比29%減、前年比42%減の9億6400万ドルで、少なくとも2015年以来の低水準となった。設置ベースの製造装置売上はQ2’23にさらに減少すると予測されるが、SDCのIT用OLED A5ラインでの受注による売上が、その低迷の一部を埋め合わせる可能性がある。

Display Equipment Suppliers Survive a Rough Q1’23

※ご参考※ 無料翻訳ツール (DeepL)

Q1’23 was a rough quarter for display equipment suppliers. As revealed in our Quarterly Display Supply Chain Financial Health Report:

- Display equipment revenues for 16 of the largest suppliers fell 29% Q/Q and 42% Y/Y to $964M, the lowest since at least 2015. Equipment revenues on an install basis should fall further in Q2’23, although revenues from bookings at SDC’s IT OLED fab A5 may offset some of that weakness.

- Display capex from 13 publicly traded companies fell 14% Q/Q and 29% Y/Y to $3.9B, also the lowest value since at least 2015. Estimated total capex fell 4% Q/Q and 45% Y/Y to $4.5B, the lowest since Q1’16.

- Capital intensity rose from 17% to 18% despite the low level of capex as display revenues fell faster and remained depressed.

- Revenues for the 16 suppliers amounted to just 22% of the estimated total capex with the average over the last 26 quarters amounting to 27% of capex.

- Nikon was #1 for the first time in display equipment revenues at just $201M on a strong end to its fiscal year with 10 litho tools shipped and a 62% share of the litho market in $US. AMAT remained #2 with Canon dropping from #1 to #3. TEL rose from #7 to #4 on a strong quarter. Six companies had Q/Q growth in display equipment revenues with 10 seeing declines. Japanese companies TEL, SCREEN and Nikon each reported strong Q/Q growth in the last quarter of their fiscal year, which is traditionally a strong quarter. Only two companies had Y/Y growth with 13 seeing declines. Eight companies saw at least 50% Y/Y declines.

- Of the 16 companies we are tracking, six earned at least 50% of their revenues from display equipment. The blended share fell from 6.4% to 4.6% on the sharp decline in display equipment revenues. Of the largest companies, Canon fell from 6% to 2%, AMAT and TEL rose from 2% to 3%, Nikon rose from 12% to 15%, SCREEN grew from 5% to 7%, ULVAC fell from 22% to 19% and Wonik IPS was flat at 15%.

FPD Equipment Revenues for 16 Suppliers

- Margins were mixed.

- Gross margins, operating margins and EBITDA margins rose. Gross margins were the highest since Q2’21 on higher margin semiconductor equipment accounting for a larger share.

- Display equipment operating margins, pre-tax margins and net margins declined. Display equipment operating margins were 11.4% vs. total company operating margins at 18.4%.

- Nikon had the highest display equipment operating income at $74M from its FPD/semi litho business. HB Tech had the highest display equipment operating margins due to an asset sale.

- Bookings for eight companies rose 28% Q/Q and fell 24% Y/Y to $431M. Q4’22 may have been the bottom with bookings expected to jump in Q2’23 on SDC’s A5 IT OLED fab. AP Systems, HB Solution, Jusung and V Tech saw bookings growth with Wonik IPS and V Tech seeing the largest bookings.

- Backlog for eight companies rose 11% while falling 44% Y/Y. V Tech had the highest backlog at $165M followed by Wonik IPS, AP Systems and AVACO each at over $90M.

- Liquidity is not an issue for our list of companies with only two companies with positive net debt/equity including AMAT.

- Operating cash flow rose 6% Q/Q and 476% Y/Y led by AMAT for the second straight quarter. TEL overtook Canon for #2. Eight companies had positive operating cash with eight seeing declines.

- Free cash flow continued to rise up 11% Q/Q and up over $2.8B Y/Y on strong performance from AMAT, TEL and Canon who accounted for 106% of the total. AMAT led the way with over $2B in free cash flow and was one of six companies with positive free cash flow in the quarter.

For more information on display and display equipment supplier financial analysis, please see our Quarterly Display Supply Chain Financial Health Report.

出典調査レポート Quarterly Display Supply Chain Financial Health Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

Written by