iPhone 14シリーズ用パネル出荷数、6月は前月比22%減~iPhone 15シリーズ用パネル出荷の出だしは好調

出典調査レポート Monthly Flagship Smartphone Tracker の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

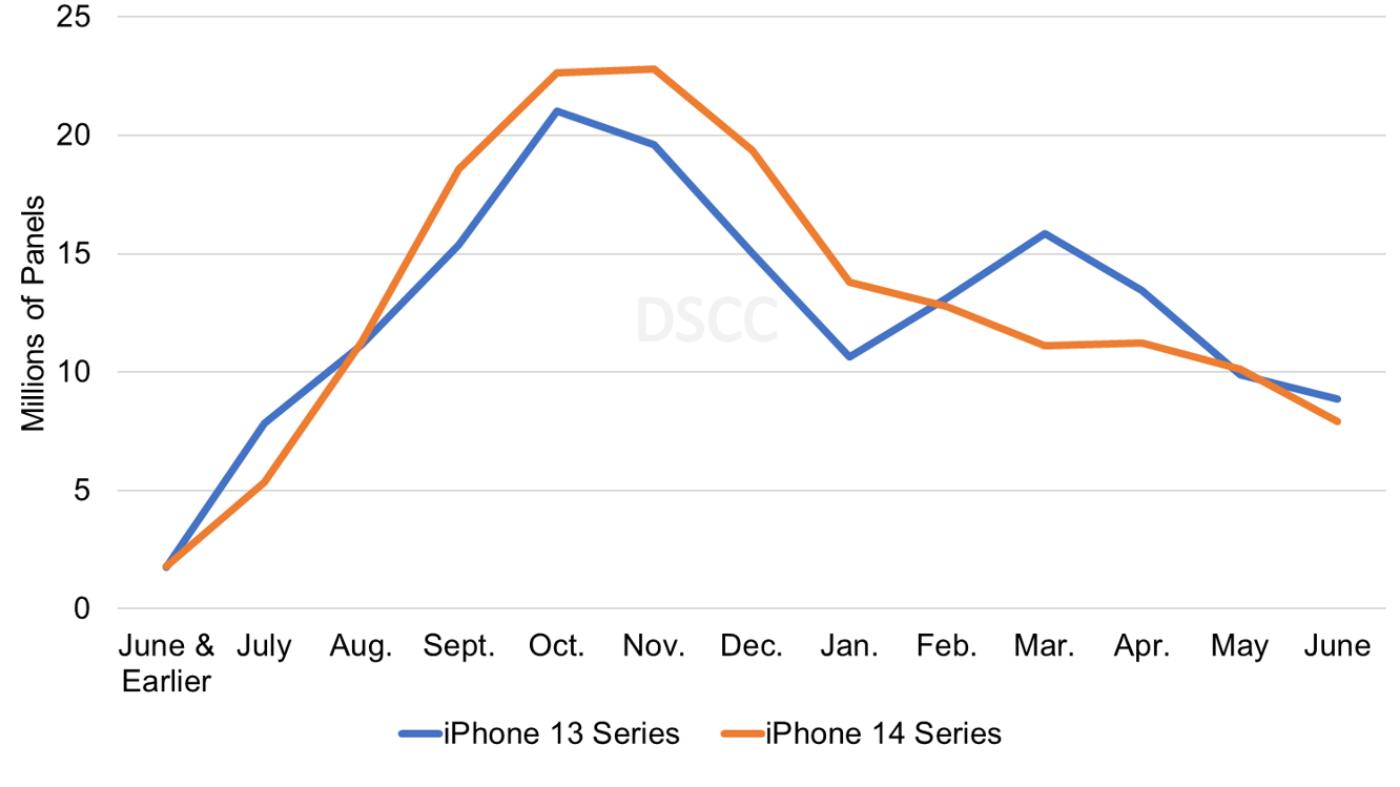

6月も終わろうとしているが、Monthly Flagship Smartphone Tracker 最新版によると、昨年6月から今年6月のiPhone 14シリーズ用パネル出荷数は、1年前の同期間のiPhone 13シリーズ用パネル出荷数に比べて3%増となっているという。この出荷の伸びは、iPhone 14 Proモデルが2022年同時期のiPhone 13 Proモデルに比べて17%増となっていることが要因である。

DSCC Reports June Panel Shipments for the iPhone 14 Series to Fall 22% M/M - iPhone 15 Series Panel Shipments Start Strong

※ご参考※ 無料翻訳ツール (DeepL)

As we approach the end of June, our latest release of the Monthly Flagship Smartphone Tracker shows that panel shipments for the iPhone 14 Series are tracking 3% higher than the iPhone 13 Series during the same time period of June- June. This growth is fueled by a 17% increase for the iPhone 14 Pro models when compared to the iPhone 13 Pro models during the same period in 2022.

In Q2’23, iPhone 14 panel shipments are expected to reach 29M units versus the iPhone 13 series with 32M units in Q2’22. Over a 12-month period through June, we expect the iPhone 14 Pro Max to continue to lead the lineup with a 34% share, followed by the iPhone 14 with 30%, the iPhone 14 Pro with 27% and the iPhone 14 Plus with 10%. We are seeing panel shipments beginning for the iPhone 15 series in June. For the period of June – July, iPhone 15 panel shipments are expected to be 100% higher than iPhone 14 series during the same time period in 2022. With the current mix of panel shipments for the iPhone 15 series, the Pro models account for a 58% share versus a 43% share for the iPhone 14 Pro models during the June – July period. The iPhone 15 series is expected to have a series of improvements that include a larger screen size for the iPhone 15 and iPhone 15 Plus of 6.12” and 6.69” respectively, Dynamic Island, the A16 Bionic chipset and a USB-C port. The iPhone 15 Pro models are expected to use the 3nm A17 Bionic chipset, utilize ultra-thin bezels, Wi-Fi 6E, and have an increase to RAM.

As a result of the broader issue of overall industry inventory corrections, continued macroeconomic headwinds, inflationary pressures and softened consumer demand, we now see iPhone 14 Series panel shipments falling 22% in June when compared to the iPhone 13 Series in the preceding year and 10% lower in May. The demand outlook remains weak based on Apple’s guidance that the June quarter will be similar to the March quarter.

Apple’s iPhone 14 Series vs. iPhone 13 Series Procurement Over 12 Months

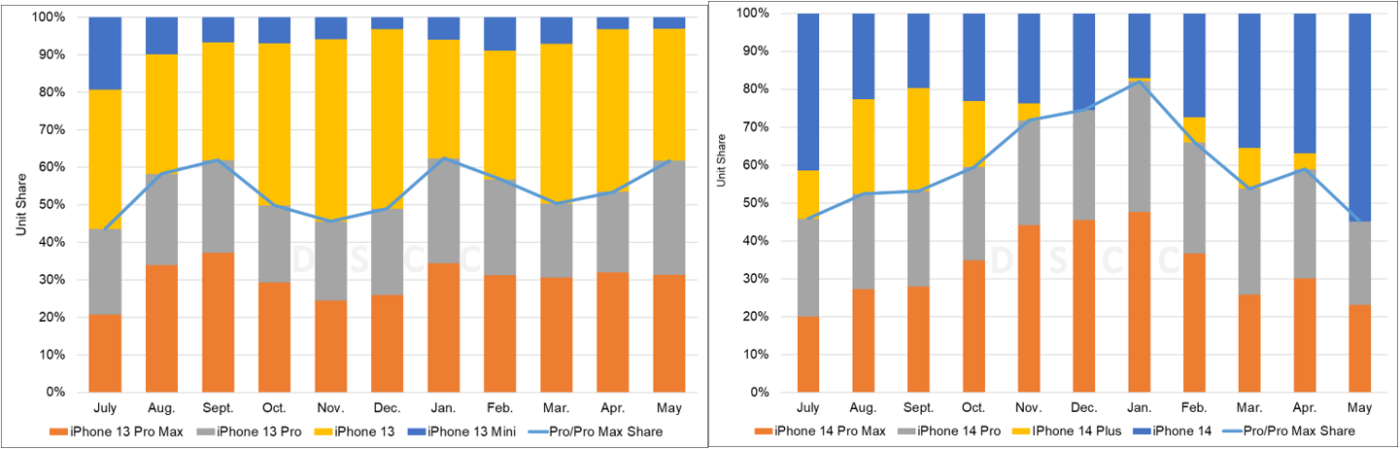

The iPhone 14 Pro and iPhone 14 Pro Max continue to perform well versus the iPhone 13 Pro and iPhone 13 Pro Max. The cumulative share for iPhone 14 Pro models through May was 62% versus a 53% share for the iPhone 13 Pro models. As a result, total panel revenues for the iPhone 14 series are 8% higher and blended ASPs are 4% higher for the iPhone 14 series.

In comparing the iPhone 14 Series vs. the iPhone 13 Series through May, we see the following changes in panel shipments by model:

- iPhone 14: Down 28%;

- iPhone 14 Plus vs. iPhone 13 Mini: Up 55%;

- iPhone 14 Pro: Up 22%;

- iPhone 14 Pro Max: Up 21%.

iPhone 13 Series vs. iPhone 14 Series Mix through May 2022 vs. 2023

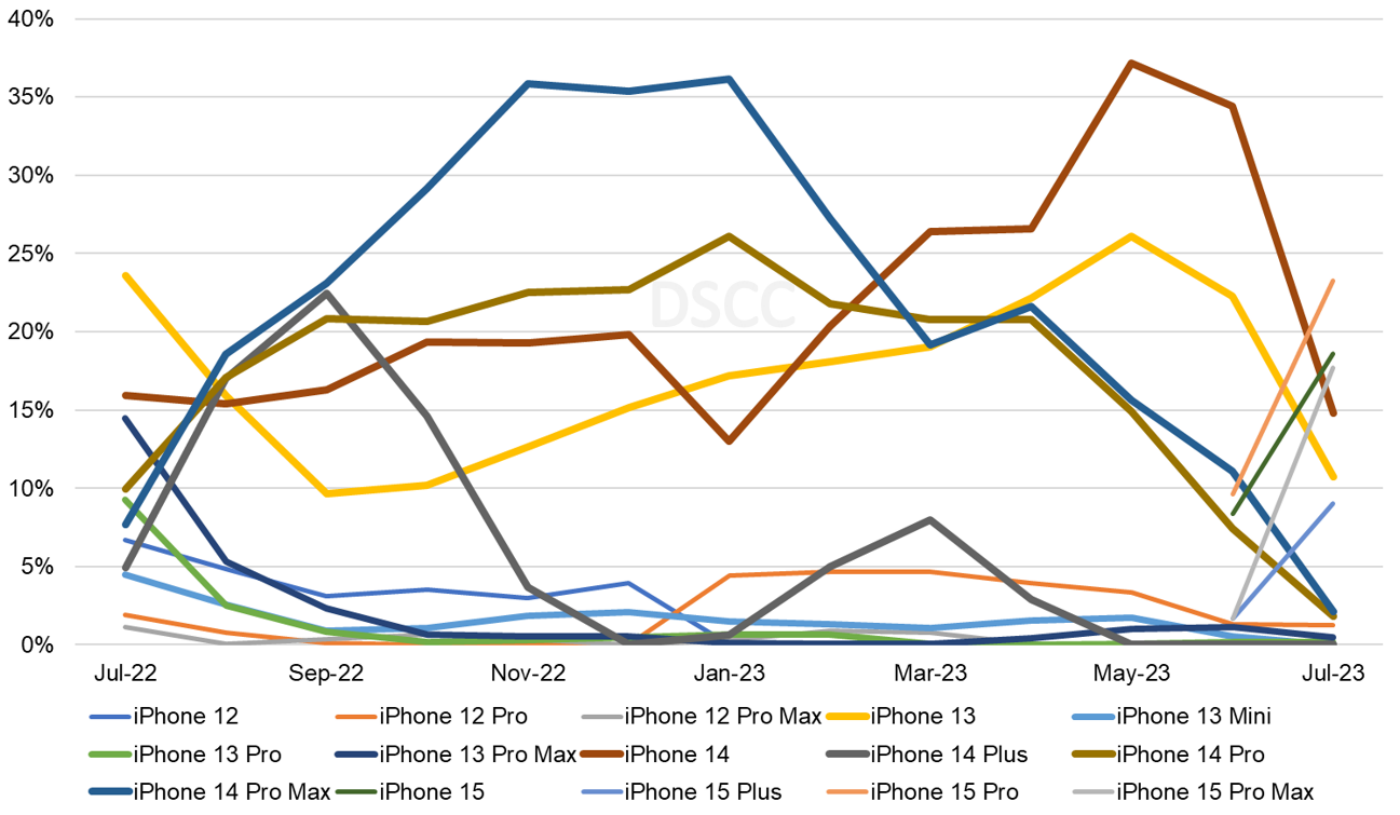

As noted earlier, in our June – July estimates, we are starting to see panel shipments for the iPhone 15 series by SDC and LGD. SDC is expected to supply panels for all four iPhone 15 models similar to what they have provided for the iPhone 14 and iPhone 13 and iPhone 12 series. We expect LGD to only supply panels for the LTPO OLED iPhone 15 Pro and iPhone 15 Pro Max. The below chart represents our historical iPhone share by series as well as our estimate for June – July. The iPhone 15 panel shipments are off to a very strong start.

iPhone Share by Models

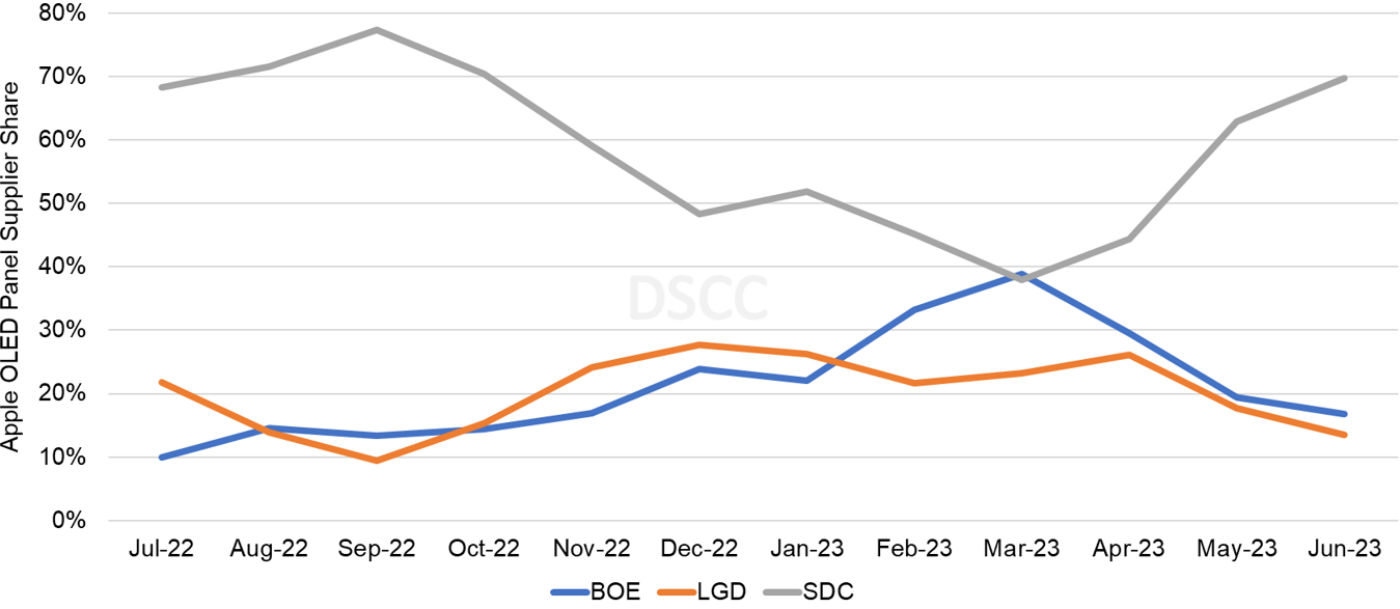

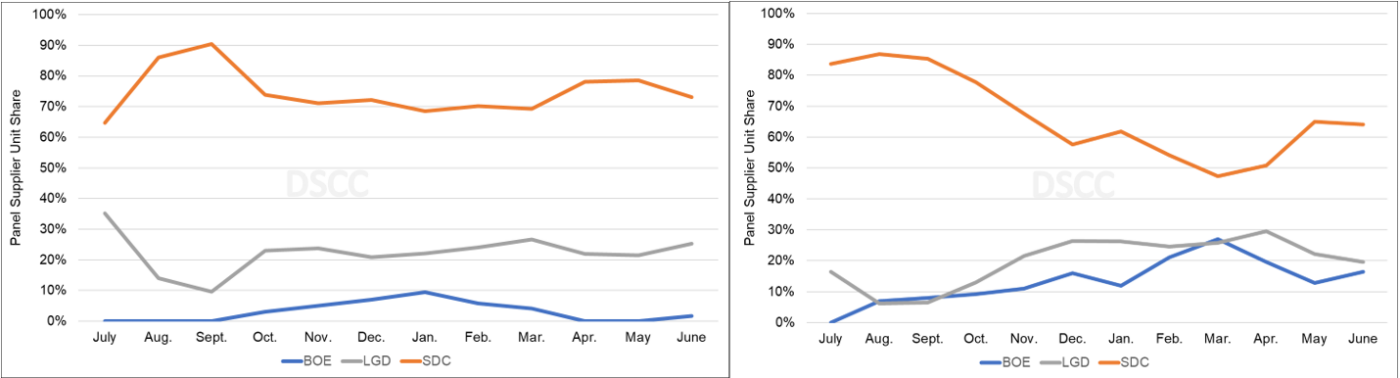

In March 2023, BOE overtook SDC for a 39% share as a result of 11% M/M growth for the iPhone 14 and 42% Q/Q growth for the iPhone 13. For the iPhone product mix within BOE in March, the iPhone 14 represented 52% of the product mix, up from 47% in February, followed by the iPhone 13 at 36% and the iPhone 12 at 12%. BOE has 100% of the total volume for the iPhone 12 and this model represented 15% of the iPhone product mix for BOE and 88% of the total iPhone 12 series volumes in Q1’23. In March, for the iPhone 13, BOE had 74% of the volume, up from 71% in February and for the iPhone 14, BOE had 77% and 76% of the volume in February and March up from 70% in January.

BOE has been trending upwards since December 2022 on increased volumes for the iPhone 13 and iPhone 14 and steady volumes for the iPhone 12 with very competitive panel prices. In Q1’23, BOE’s panel ASP for a 6.06” flexible OLED smartphone was significantly below both Korean panel suppliers. We expect BOE to continue to take share on the iPhone 14 and iPhone 13 models due to its aggressive panel prices.

SDC regained the leadership position in April as a result of cutting prices to win back share that resulted in significant M/M increases for the iPhone 13, iPhone 13 Pro Max, iPhone 14, iPhone 14 Pro and iPhone 14 Pro Max. In May, SDC’s share reached 63% as a result of increased volumes for the iPhone 14, iPhone 13, iPhone 13 Pro and iPhone 13 Pro Max.

For the iPhone 14 series, SDC continues to dominate Apple’s OLED business with a 67% cumulative share projected through June. For May, LGD had a 20% cumulative share, followed by BOE with 13%.

iPhone Panel Supplier Share

iPhone 13 and 14 Shipment Share by OLED Panel Suppliers

出典調査レポートについて

Monthly Flagship Smartphone Tracker には、主要スマートフォンブランド全社の全モデルを対象としたフレキシブルOLEDおよびフォルダブルOLED出荷の月間実績データと2ヵ月分の予測データを収録しています。すべてのフラッグシップモデルを対象に、月間出荷数を以下の項目別に提示します。

• ブランド

• モデル

• ディスプレイサイズ

• フォームファクター

• フォルダブル型フォームファクター

• パネルメーカー

• TFTバックプレーン

• 解像度

• ホール/ノッチ/UPC

• リフレッシュレート

• CoE (カラー・オン・エンカプスレーション)

• MLA (マイクロレンズアレイ)

• チップセットメーカー

• チップセット

• 標準輝度

• ピーク輝度

• デバイス発売日

Monthly Flagship Smartphone Tracker は、FPD材料メーカー、パネルメーカー、OEM、技術開発企業、ブランド、通信会社、財務アナリストなど、OLEDスマートフォンのサプライチェーンに関わるすべての皆様のお役に立つ優れたツールです。ブランド/モデル/パネルメーカー別のパネル出荷実績と短期予測、近日発売予定の次期モデルをご確認いただけます。

DSCCではこのほか、 Advanced Smartphone Display Shipment and Technology Report も発行しています。このレポートでは、主要スマートフォンブランド全社を対象としたパネル出荷の四半期実績と詳細なモデル仕様およびトレンドのデータを提供しています。ブランド別、モデル別、またすべてのディスプレイおよび非ディスプレイパラメータ別にOLED搭載スマートフォンセットおよびスマートフォン用OLEDの出荷数データ、出荷額データを掲載、過去実績および今年度見通しは四半期ベースで、2027年までの予測は年間ベースで提示します。さらに、スマートフォンに適用可能なOLEDのテクノロジーとイノベーションのトレンドに関するインサイトも提供します。DSCCのデータベースに収録しているAMOLEDスマートフォンの構成は1200以上にのぼり、基板、TFTバックプレーン、パネルメーカー、リフレッシュレート、チップセットメーカー、設計ルール、5Gネットワークなどの項目によるバリエーションを含んでいます。

出典調査レポート Monthly Flagship Smartphone Tracker の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。