FPDメーカー各社の第2四半期決算発表プレビュー

冒頭部和訳

7月27日 (水) のLG Displayを皮切りに、今後数週間でFPDメーカー各社の第2四半期決算発表が相次ぐ。FPD業界が史上最大の利益を上げたQ2’21から1年を迎えたQ2’22、業界展望は全く異なる様相を呈している。1年前に下落し始めたFPD価格は下げ止まらず、価格が下がってもパネル需要は縮小した。FPDメーカー各社からはQ2’22もまた利益率の低下が報告されることになりそうで、営業損失を報告するFPDメーカーも数社あるものと予測される。

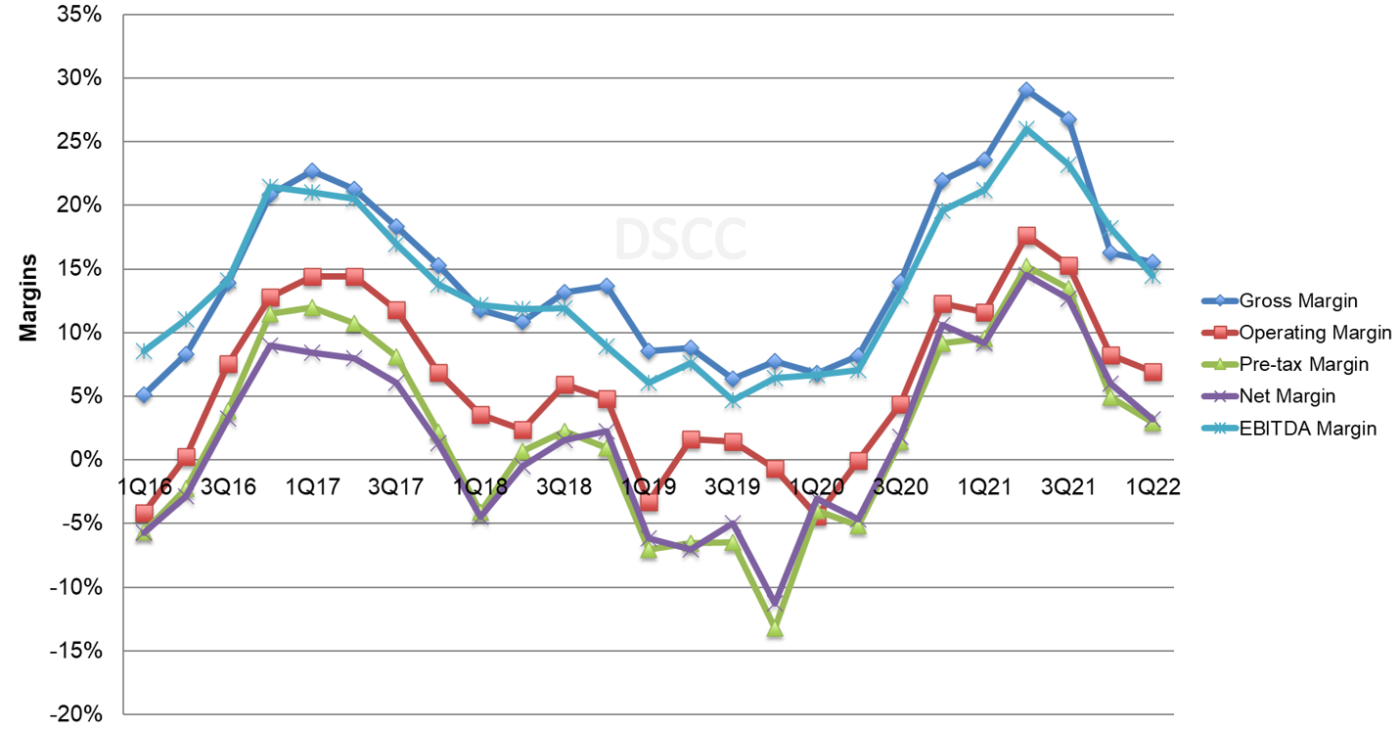

まずは以下の図で業界の利益率の全体像を見ていこう。図に示すように、利益率はQ2’21にピークに達し、クリスタルサイクルの底から頂点までの連続5四半期で最も高い値を記録した。利益率はQ4’21に大幅に低下した後、Q1’22に再び低下したもののそのペースは緩やかで、FPD価格のパターンと一致していた。TV用LCD価格はQ4’21に平均で前期比32%下落を記録、これは過去最大の前期比価格下落率だったが、Q1’22には下落率が13%に減速した。価格はQ2’22になってさらに13%下落したことから、第2四半期の利益率の低下は第1四半期と同様と予測される。

Panel Maker Q2 Earnings Preview

In the next few weeks, we will see the Q2 earnings announcements for flat panel display makers, starting with LG Display on Wednesday, July 27th. The most recent quarter marks a full year after the biggest profits in the history of the flat panel display industry in Q2’21, and the prospects for the industry could not be more different. Panel prices started to decline a year ago and have not stopped their decline, and even with lower prices the demand for panels has decreased. We expect that panel makers will report another quarter of declining margins for Q2’22 and expect several panel makers to report operating losses.

First, let’s set the stage with an industry overview of margins. Margins peaked in Q2’21, capping a five-quarter run from the bottom of the Crystal Cycle to the top, as shown in the chart here. After a sharp decline in margins In Q4’21, margins declined again in Q1’22 but at a slower pace, matching the pattern of panel prices. LCD TV panel prices declined by an average of 32% Q/Q in Q4’21, the largest Q/Q price decline ever, but this slowed down to 13% in Q1’22. Prices declined another 13% in Q2’22, so we may expect that the decline in Q2 margins is like that of Q1.

Display Maker Quarterly Margins

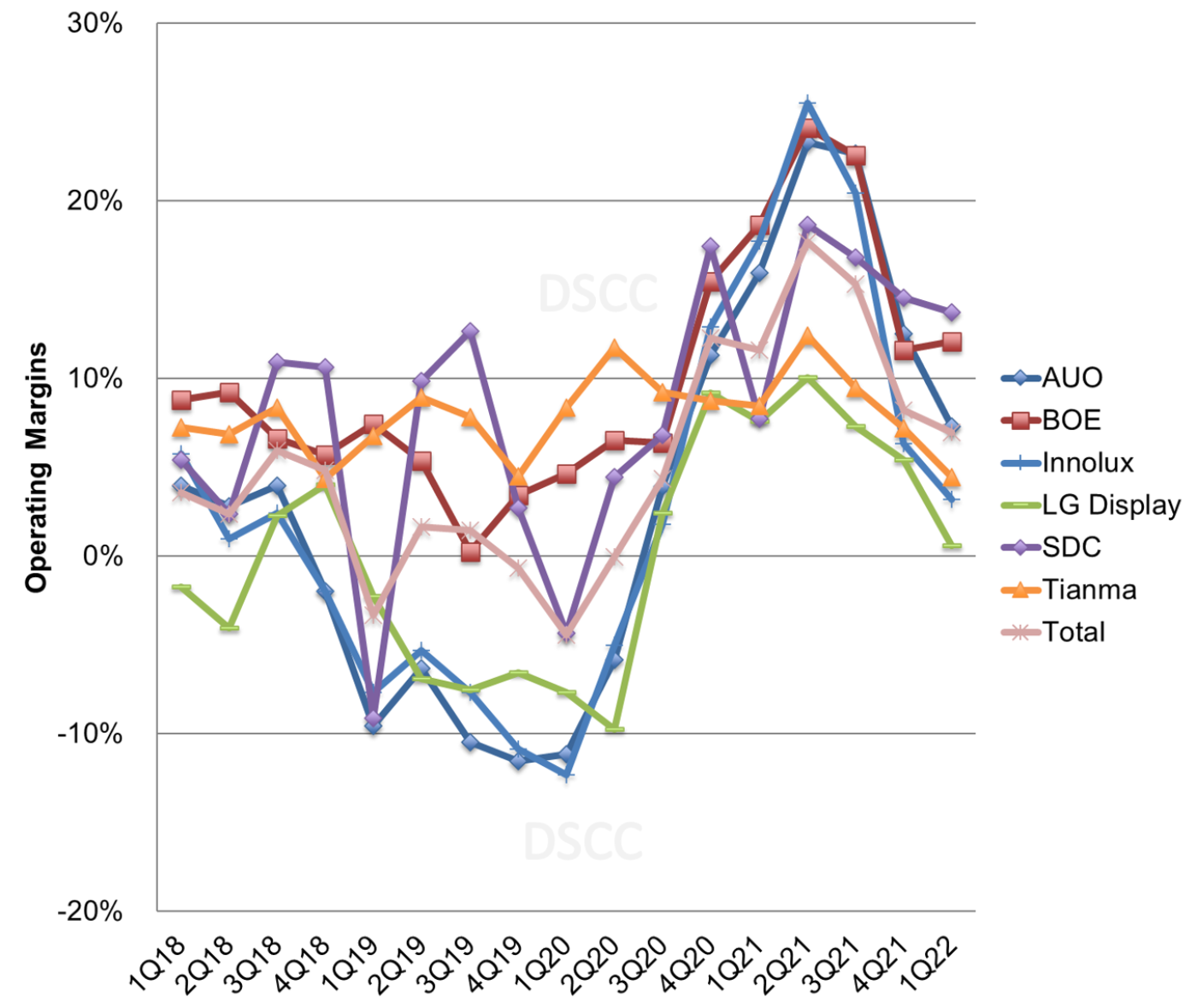

The second chart shows the operating margins of the larger companies in the industry. While the trend of the Crystal Cycle is clear to see, there is a wide divergence of outcomes.

- SDC sustained positive operating margins during the prior downturn and while it did not benefit much from the upswing in LCD panel prices in 2020-2021, as LCD prices have come down SDC is once again the most profitable panel maker in the industry.

- AUO, Innolux and LGD have been more sensitive to the cycle with margins falling sharply in Q4 and again in Q1.

- BOE saw operating profit margin increase slightly in Q1; BOE continues to benefit from government subsidies which cushion the company against downturns.

- While it benefited somewhat from the upswing in the Crystal Cycle in 2020-2021, LGD’s unprofitable OLED business kept its margins below that of its peers. The company’s reduced dependence on LCD means that it suffers less from LCD TV panel price declines, but trouble in its OLED TV business is likely to drive the company to a loss in Q2.

Display Maker Quarterly Operating Margins

In terms of guidance, companies expressed caution for Q2, but in hindsight, many of the forecasts seem optimistic:

- LGD expected area shipments to increase by low-to-mid teens % Q/Q, and area ASPs to decrease by about 10% based on a seasonal decline in mobile shipments. The combination of higher shipments and lower price implied a revenue increase of mid-single digits % Q/Q.

- AUO expected area shipments down by mid-single digits % and ASPs down by low-to-mid-single digits %, implying a revenue reduction of ~10% Q/Q.

- Innolux expected large panel shipments to be up high-single digits % Q/Q, small/medium panel shipments up high teens % and blended ASP down by low-teens %, implying revenue close to flat.

For the Taiwan players, because they report monthly revenues and shipments, we now know that AUO’s revenues decreased by 23% Q/Q, more than 10% worse than their guidance. Innolux’s revenues declined by 17%, far worse than its guidance. In hindsight, both companies were too optimistic about both prices and shipments.

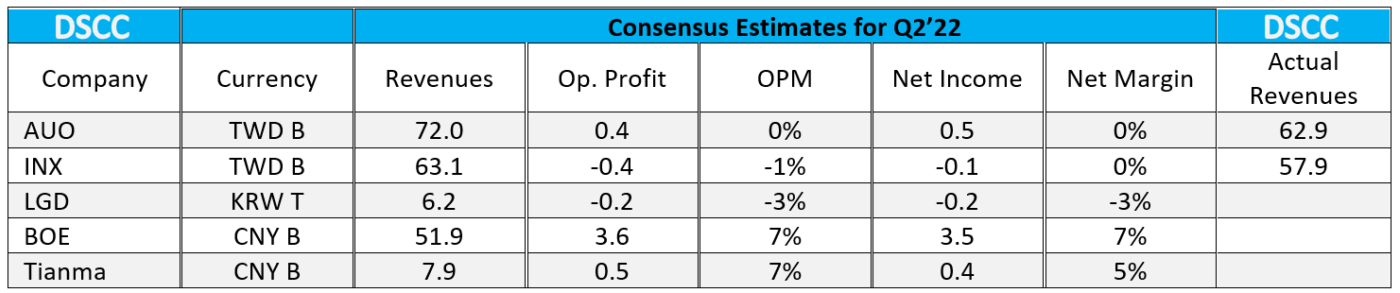

The table below shows analyst expectations for Q2 for the panel makers with analyst coverage, according to marketscreener.com. The analyst expectations for margins anticipate that margins worsened in Q2, but the reality is likely to be worse. The Taiwan panel maker revenues are 13% and 8% lower than expectations for AUO and Innolux, respectively, so operating profit margins are likely to be correspondingly worse.

LGD’s guidance implies an increase in revenues of mid-single digits % but consensus estimates predict a 4% revenue decrease Q/Q, so if LGD performed to their guidance they will be better than consensus, but the reality is more likely to be worse than consensus.

According to DSCC's Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします), LGD’s OLED revenues in $US decreased by 3% Q/Q in Q2, as higher TV revenues TVs failed to overcome the seasonal decrease in revenues for smartphones. Because of declining prices and weak demand in LCD, LGD was unlikely to overcome a decrease in OLED revenue with an increase in LCD revenue. One factor in LGD’s favor was a currency tailwind: LGD was helped in Q2’22 by a weakening of the Korean won against the dollar, as the won weakened by 5% Q/Q and by 13% Y/Y.

Because of declining demand and excess inventory, every major panel maker reduced utilization in the second quarter. According to DSCC's Quarterly All Display Fab Utilization Report (一部実データ付きサンプルをお送りします), in Q2 AUO had the sharpest drop in utilization, falling from 92% in Q1’22 to 75%, but BOE, LGD and Innolux also dropped utilization in the quarter. Even so, inventory may have increased in the quarter because demand fell more precipitously.

Perhaps just as important as the results will be the guidance given about Q3’22 and the rest of the year. With panel prices continuing to decline below cash costs, and continuing concerns about demand, we believe that panel makers will again be cautious about prospects for the rest of 2022.

本記事の出典調査レポート

Quarterly Display Supply Chain Financial Health Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。