FPD製造装置メーカーの四半期実績、半導体市場を追い風に記録的水準に到達

冒頭部和訳

DSCCでは、主要FPD製造装置メーカー19社の各四半期の財務実績について、収益を事業部門別にセグメント化し、受注やバックログの情報を得るなどして深く掘り下げている。Q4’21は半導体製造装置の好実績が追い風となり、総収益、粗利益、純利益の点で19社にとって記録的な四半期となった。半導体製造装置事業では好実績を記録したが、19社のFPD製造装置の出荷金額は、前期比では4四半期連続の減少、前年比では2四半期連続の減少となっている。

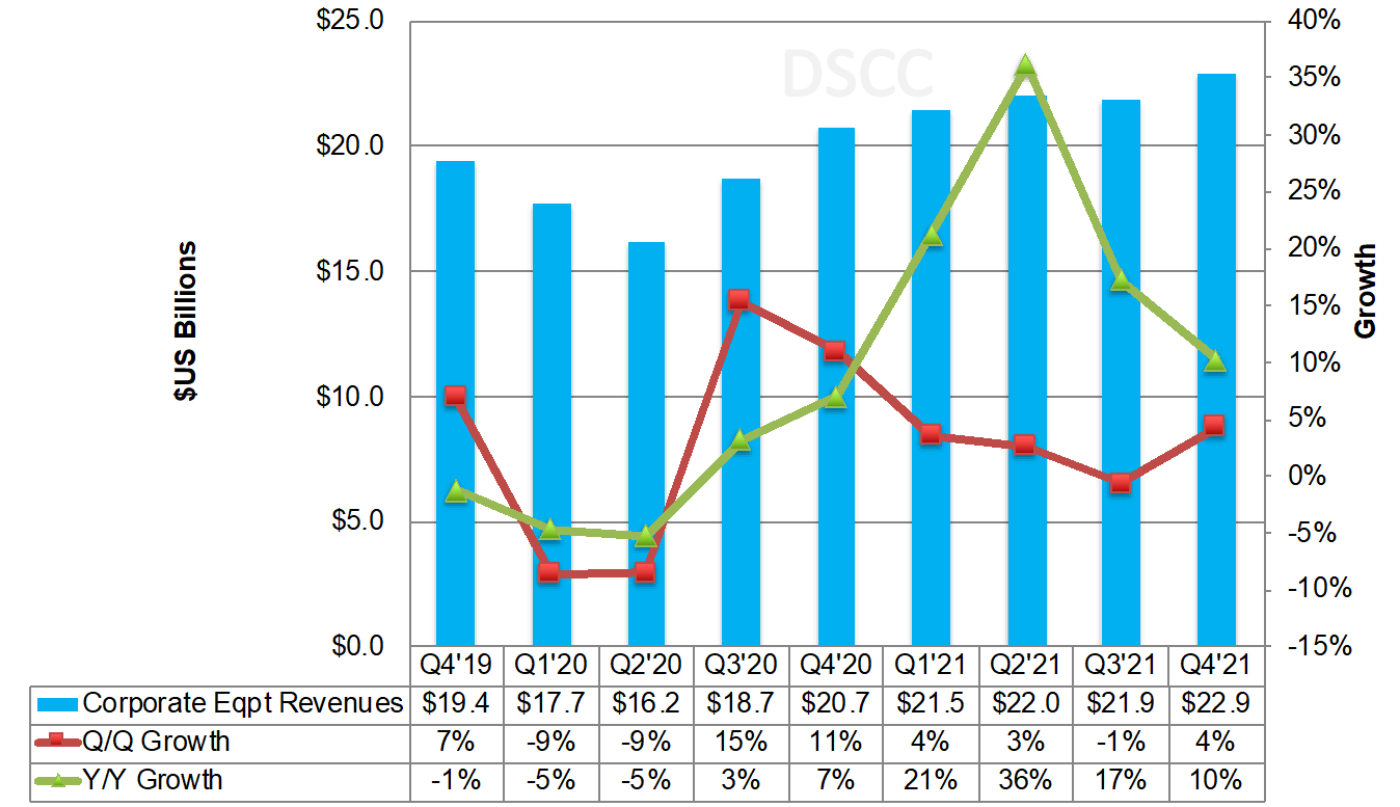

主要FPD製造装置メーカー19社の顔ぶれは、Applied Materials、AP Systems、AVACO、Canon、Charm Engineering、DMS Co.、HB Solution、HB Technology、ICD、INVENIA、Jusung、KC Co.、Nikon、Nissin Electric、SCREEN Holdings、Tokyo Electron、ULVAC、V Technology、Wonik IPSだが、その総収益は前期比4%増で過去最高の229億ドルに達し、半導体製造装置の記録的実績によって前年比では4四半期連続の2桁増となった。半導体市場は少なくとも今年末までは連続的に拡大すると予測されており、今後数四半期でさらに多くの記録的実績が見られるはずだ。主要メーカーのなかでも上位5社が市場を支配しており、その合計シェアは過去9四半期を通して91%〜93%で推移、そのうち8四半期で同じランキング構成、すなわち上から順にCanon、AMAT、TEL、Nikon、SCREENとなっている。

19社のうち11社が前期比プラス成長、7社がマイナス成長、1社が横ばいだった。前期比成長率はAP Systemsが78%と最も高く、AVACO、Jusung、KC Co.、HBTechが続く。前年比では19社のうち9社がプラス成長を記録、Jusungが345%増で最も高く、新たなデザインウィンにより半導体製造装置の出荷金額が617%増となったが、FPD製造装置の出荷金額は前年比6%減となっている。TELも前年比60%増の大幅成長を記録、FPD出荷金額の同41%減を半導体製造装置の同70%増で相殺している。

DSCC Report Shows Display Equipment Suppliers Have Record Quarter Thanks to the Semiconductor Market

DSCC performs a deep dive into the financial performance of 19 leading display equipment suppliers each quarter which includes segmenting their revenues by line of business, capturing bookings and backlog info and more. Q4’21 was a record quarter for these companies in terms of overall revenues, gross profits and net income thanks to strong semiconductor equipment results. While their semiconductor equipment businesses outperformed, display equipment revenues for these companies fell Q/Q for the fourth straight quarter and were down Y/Y for the second straight quarter.

Total revenues for these 19 companies – Applied Materials, AP Systems, AVACO, Canon, Charm Engineering, DMS Co., HB Solution, HB Technology, ICD, INVENIA, Jusung, KC Co., Nikon, Nissin Electric, SCREEN Holdings, Tokyo Electron, ULVAC, V Technology and Wonik IPS - rose 4% Q/Q to a new all-time of $22.9B and were up double-digits Y/Y for the fourth straight quarter on record semiconductor equipment results. With the semiconductor market expected to expand sequentially through at least the rest of the year, we should see more record results in the coming quarters. The top five companies dominate this list with a 91% - 93% share over the last nine quarters and have had the same rankings in eight of the last nine quarters and consist of Canon, AMAT, TEL, Nikon and SCREEN.

11 of the 19 companies had Q/Q growth with seven declining and one flat. AP Systems had the fastest Q/Q growth up 78% followed by AVACO, Jusung, KC Co. and HB Tech. Nine of the 19 companies had Y/Y growth led by Jusung up 345% on a 617% increase in semi revenues on new design wins, as FPD revenues were down 6% Y/Y. TEL also had impressive Y/Y growth up 60% with semi equipment up 70% offsetting a 41% decline in FPD revenues.

Quarterly Total Revenues for 19 Leading Display Equipment Suppliers

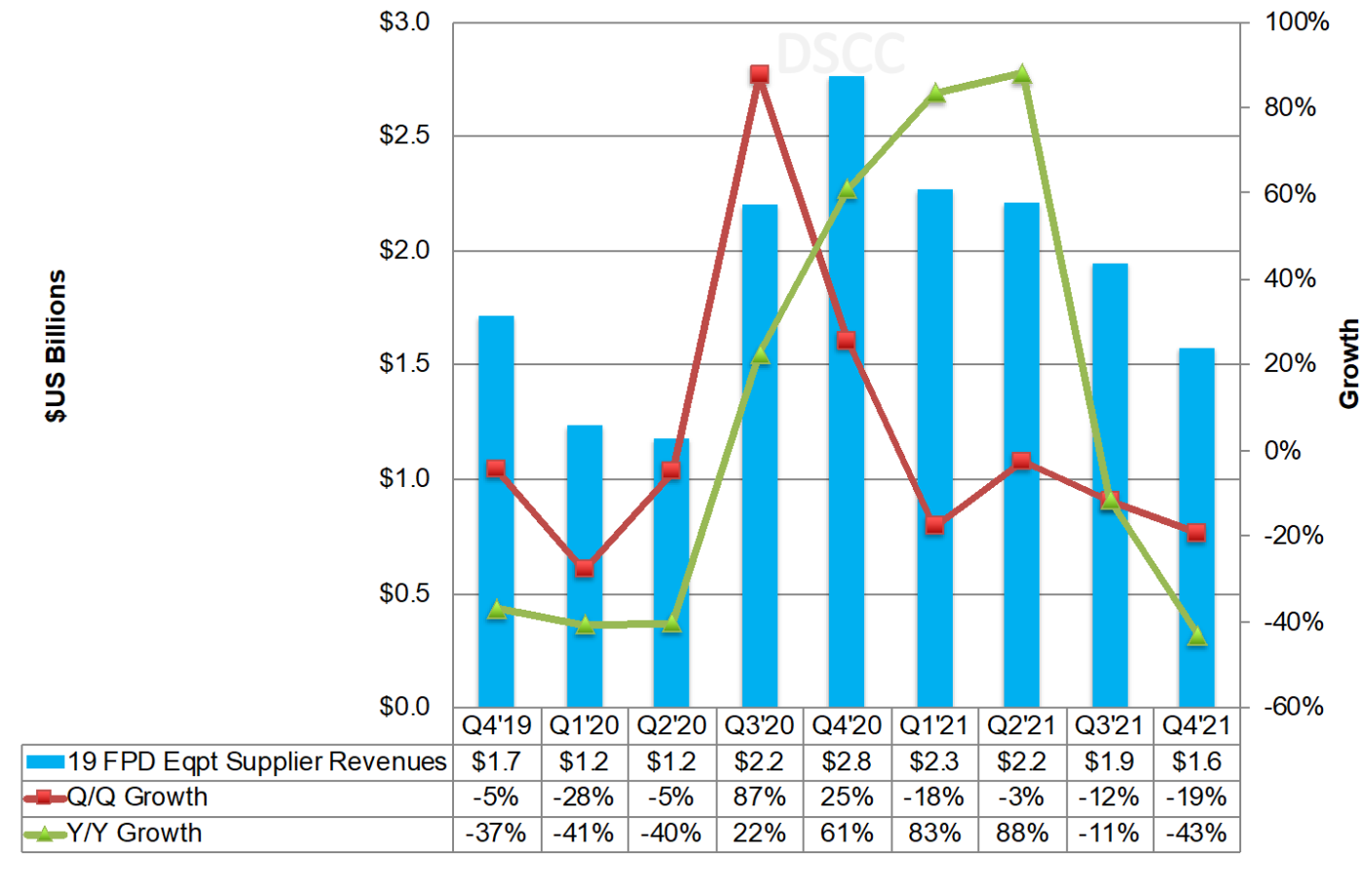

Looking just at display equipment revenues paints a different story, however. Revenues fell 19% Q/Q and 43% Y/Y to $1.6B, the lowest since Q2’20. It was the 4th straight quarter with a Q/Q decline and the lowest value since Q2’20. AMAT was #1 for the 2nd consecutive quarter with Canon overtaking Nikon for #2 which fell to #6. ULVAC rose from #6 to #3 on 49% Q/Q growth which we believe was primarily from Sharp SIO and Tianma TM18 where they won most of the PVD business. TEL jumped from a 6% to a 10% share likely due to dry etch wins at those companies. Companies gaining at least a point of market share included AMAT, ULVAC, TEL, AP Systems and HB Tech. Companies losing more than at least a point of share included Canon, Nikon and V Tech in a difficult quarter for litho suppliers.

Quarterly Display Equipment Revenues for 19 Leading Display Equipment Suppliers

With the blended semiconductor revenue share rising and revenues at an all-time high, margins increased across most parameters as semiconductor equipment is usually more profitable than display equipment:

- Company gross margins rose from 44.3% to 44.8%;

- Operating margins grew from 19.1% to 19.5%;

- Display equipment operating margins rose from 9.4% to 11.8%, significantly lower than in semiconductors;

- EBITDA margins grew from 22.9% to 23.2%;

- Pre-tax profit margins fell from 20.3% to 19.6%;

- Net margins rose from 15.7% to 16.2%.

The report also looks at company cash flow and balance sheets. Operating cash flow rose 52% Q/Q and 55% Y/Y to a record $4.9B, led by AMAT, TEL, Canon, SCREEN and Nikon. It was a strong quarter with only four companies experiencing negative operating cash flow. It was also a strong quarter for free cash flow, up 63% Q/Q and 60% Y/Y to a record $3.8B led by AMAT at $2.5B. Only five companies had negative free cash flow.

Liquidity is not an issue for our list of companies except at Invenia, although their situation improved significantly in Q4’21 with debt/equity and net debt/equity falling below 100%. Only Invenia and HB Tech had positive net debt/equity as equipment suppliers are in strong financial positions due to their high margins and strong performance from the semiconductor industry.

For more insights into display equipment and panel suppliers’ financial results and health, please see our Quarterly Display Supply Chain Financial Health Report (一部実データ付きサンプルをお送りします) or contact info@displaysupplychain.com.

本記事の出典調査レポート

Quarterly Display Supply Chain Financial Health Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。