2021年のAdvanced (OLEDまたはMiniLED LCD搭載) モニター用FPD出荷は397%増。2022年は241%成長見通し~42インチWOLED/34インチQD-OLED/27インチMiniLEDがけん引

冒頭部和訳

DSCCの Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) では、OLEDまたはMiniLED LCDを搭載したタブレット、ノートPC、モニターの出荷データを、四半期/ブランド/サイズ/解像度/リフレッシュレートの項目別に、またその他多くの機能別に提示している。

最近リリースされた最新号に掲載のAdvancedモニター市場の重要ポイントは以下の通り。

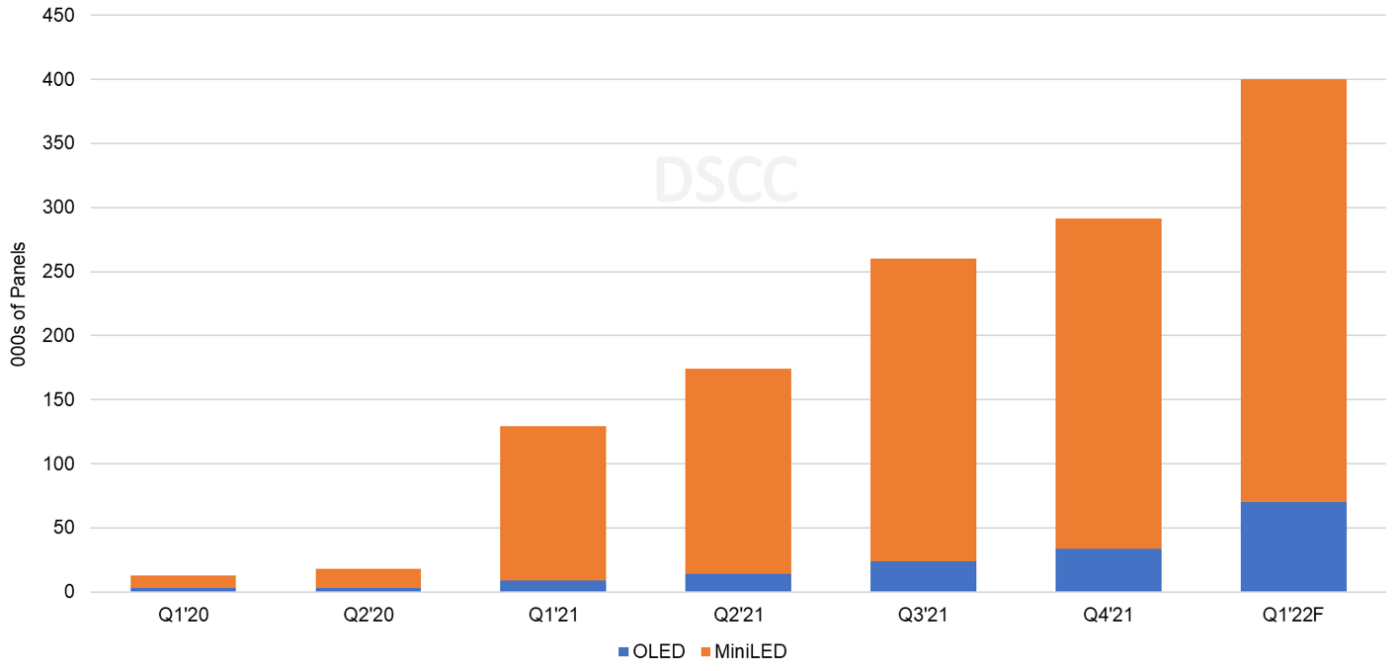

- 2021年はAsusの32インチMiniLEDモデル用、Appleの32インチMiniLEDモデル用、LGの27インチ/32インチIJP RGB OLEDモデル用のパネル調達が増加した結果、Advancedモニター用ディスプレイ出荷枚数は前年比397%増となった。

- 2021年のモニター用パネル調達はMiniLEDとOLEDの比率がほぼ10 : 1で、MiniLEDがシェア91%を獲得した。2022年には42インチと48インチのWOLEDモデル、さらに27インチと32インチのIJP RGB OLEDモデルが発売され、MiniLEDのシェアが80%に下がると予測される。

- 2022年には、CES 2022で発表された新たなQD-OLEDモデル、42インチと48インチのWOLEDモデルが強く、モニター用OLEDパネル調達は前年比612%増となる見通しだ。DellとSamsungの34インチQD-OLEDモデル用、LGの27インチと32インチのIJP RGBモデル用、LGとAsusの42インチと48インチのWOLEDモデル用などがここに含まれる。

- Q2’22にはAppleが27インチのMiniLEDモニターを発表する予定で、これが2022年のパネル調達を大きく後押しすると見られる。このモデル用パネルの生産は今月始まったようだ。この27インチのMiniLEDモニターは、価格が4999ドルの32インチのPro Display XDRと比較すると、調光ゾーン数が2倍、MiniLED数が7倍になるようだ。この新たな27インチMiniLEDモニターは2022年に、MiniLEDモニターカテゴリーで出荷台数シェア30%、Advancedモニターカテゴリーで同24% (いずれもパネル調達ベース) の見通しである。

- 2022年には、OLEDモニターカテゴリーで、27インチから48インチのディスプレイサイズを含むWOLEDモデルが出荷台数シェア51%を占め、QD-OLEDモデルが同25%、IJP RGB OLEDモデルが同23%で続くと予測される。SamsungとDellから34インチQD-OLEDモニターが発表されるのに加えて、その他の3ブランドもSDCの34インチQD-OLEDベースのモニターを導入すると見られるのは本レポートで明らかにしている通りだが、DellとSamsungの配分が最も高くなりそうだ。

DSCC Report Reveals Advanced Monitor Market Rose 397% in 2021 - 241% Growth is Expected in 2022 Fueled by 42” WOLED, 34” QD-OLED and 27” MiniLEDs

DSCC’s Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) reveals OLED vs. MiniLED LCD monitors, notebook PCs and tablets shipments by quarter, brand, size, resolution, refresh rate and many other features.

In the recently released report, some highlights for Advanced Monitors include:

- In 2021, the Advanced Monitor market rose 397% Y/Y as a result of increased panel procurement for the Asus 32” MiniLED models, the Apple 32” MiniLED model and LG’s 27” and 32” IJP RGB OLED models.

- In 2021, panel procurement for MiniLED models outpaced OLED models by a ~10:1 ratio. MiniLED monitors accounted for a 91% share in 2021. In 2022, with the launch of 42” and 48” WOLED models and more 27” and 32” IJP RGB OLED models, the MiniLED share is expected to decrease to 80%.

- In 2022, we expect panel procurement for OLED monitor models to increase 612% Y/Y on the strength of new QD-OLED models and 42” and 48” WOLED models that were announced at CES 2022. Those models include the 34” QD-OLED models from Dell and Samsung, the 27” and 32” IJP RGB models from LG and the 42” and 48” WOLED models from LG and Asus.

- In Q2’22, Apple is expected to announce a 27” MiniLED monitor that is expected to drive significant panel procurement in 2022. We believe panel production for this model started this month. We expect this 27” MiniLED monitor to have 2X the number of dimming zones and 7X more MiniLEDs versus the 32” Pro Display XDR that is priced at $4999. We expect this new 27” MiniLED monitor to account for a 30% unit share on a panel procurement basis for the MiniLED monitor category and 24% share of the Advanced Monitor category in 2022.

- In 2022, for the OLED monitor category, WOLED models that include display sizes from 27” to 48” are expected to account for a 51% unit share, followed by QD-OLED models with 25% and IJP RGB OLED models with 23%. In addition to Samsung and Dell announcing 34” QD-OLED monitors, we also expect three other brands to introduce monitors based on SDC’s 34” QD-OLED monitor as revealed in the report, however, Dell and Samsung will have the highest allocation.

Advanced Monitor Display Shipments by Technology

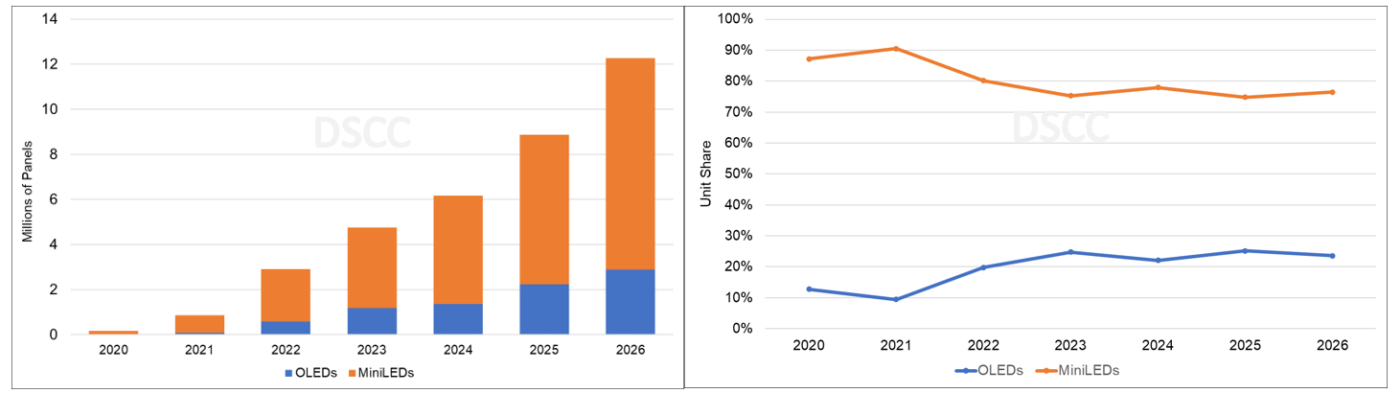

- Beyond 2022, we expect strong double-digit Y/Y growth for MiniLED and OLED monitors as more brands launch new products in the 42” OLED monitor category as well as continued growth in the 27” and 32” MiniLED monitor category driven by Apple with the 27” MiniLED monitor.

- MiniLEDs are expected to continue to lead with the majority share through the forecast period. OLEDs are not yet cost optimized for monitors. WOLED and QD-OLED TV panels being positioned into the monitor market suffer from lower brightness and resolution compared to MiniLEDs. Future cost optimized G8.5 IGZO FMM VTE RGB OLED fabs will help OLEDs sustain a 22% to 25% share from 2023.

- Over the forecast period, we expect Advanced Monitors to grow at a 70% CAGR with OLED monitors growing at a 104% CAGR and MiniLED monitors growing at a 65% CAGR.

For more insights into Advanced Display shipments by brand, size, resolution, refresh rate, backplane, substrate, OLED stack, touch, etc., as well as panel and product roadmaps, cost and technology advancements, please see the Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) or contact info@displaysupplychain.co.jp.