ロシア対ウクライナ戦争で世界TV需要が減少~DiScien分析

冒頭部和訳

ウクライナでの戦争がTV市場に与える影響を多方面から評価した分析を、DSCCの提携調査会社であるDiScienが発表しました。この分析のオリジナル版 (中国語) には こちらのリンク からアクセスしていただけますが、DSCCではこの分析を翻訳し、DSCCの見解を一部加えた内容を当社の読者様にご提供します。

DSCCのお客様は、TV、業務用ディスプレイ、サイネージ、その他のアプリケーションのサプライチェーンを調査対象とするDiScienの調査レポートをDSCC経由でご購入いただけます。DiScienの Major Global TV Shipments and Supply Chain Report は、グローバルブランド上位15社からのTV出荷を対象に、画面サイズ、解像度、地域などの項目別に出荷データを提供するレポートで、市場の需要、ブランドのダイナミクス、各地域の製品トレンドなどの分析でお客様を支援します。このレポートに関心をお持ちのお客様は info@displaysupplychain.co.jp までお問い合わせください。

----------

DiScienの分析では、ロシアのウクライナ侵攻によって世界のTV需要は460万台減少すると見られ、うち360万台はロシアとウクライナへの直接的影響によるものであり、残りの100万台は中東およびアフリカを含む他地域への間接的影響によるものと推測されている。※この分析の実施時期は2022年3月中旬である。

当初の観測では、ウクライナでの戦争は他の欧州地域に対するTV供給にほとんど影響を与えないだろうと見られていた。ロシアは中国やその他の国からのTV輸入に14%の関税を課しているため、ロシアで販売されるTVの大半はロシア国内の工場で製造されている。原則的にはこれらの工場から他の欧州諸国へも供給は可能だが、実際にはごくわずかである。

2014年のロシアによるクリミア併合後に制裁がいくつか課されたことで、ロシアから欧州への輸出品は関税の対象となり、競争力がなくなった。ロシアから欧州へのTV輸入には14%の関税が課せられるが、欧州連合 (EU) 加盟国であるポーランドで製造されたTVはEU全域で関税対象ではない。2020年時点で、ロシアのTV生産台数はロシアのTV需要の96%とほぼ一致している。

ロシアとウクライナの両国における戦争とそれに伴う経済的影響は、両国のTV需要に負の影響を及ぼす。次のグラフに示すように、DiScienでは2022年のこの影響を360万台と推測している。2021年の両国の需要は合計780万台だった。DiScienでは、2022年にロシアの需要が40%減少しウクライナの需要が80%減少すると予測しており、この予測を楽観的と考えている。DiScienは2023年に回復を見込んでいるが、戦争の犠牲と結果は不明であることから、来年の評価については慎重な検討が求められる。

※メルマガ読者様には本記事の「全文和訳版」をメール配信しました。

Russia - Ukraine War Will Reduce TV Demand, per DiScien Analysis

DSCC’s partners at DiScien have released a multi-dimensional assessment of the impact of the war in Ukraine on the TV market. The original analysis is available in Chinese at this link; for DSCC’s subscribers I have taken a translation and added some of our own thoughts.

DSCC clients can purchase DiScien reports through DSCC covering the supply chains for TV, commercial display, signage and other applications. The DiScien Major Global TV Shipments and Supply Chain Report covers TV shipments from the top 15 global brands and provides shipment information by screen size, resolution, and region, allowing users to analyze market demand, brand dynamics and product trends by region. Readers interested in subscribing to this report should contact info@displaysupplychain.co.jp.

DiScien’s analysis suggests that Russia’s invasion of Ukraine will reduce global demand for TVs by 4.6M units, of which 3.6M comes from the direct impact in Russia and Ukraine, and another 1.0M stems from an indirect impact on other markets including the Middle East and Africa. This analysis was conducted in mid-March 2022.

The first observation is that the war in Ukraine will have little impact on TV supply to other European regions. Because Russia imposes a 14% tariff on TV imports from China and other countries, most TVs sold in Russia are assembled in local Russian factories. Although in principle, these factories could also supply other European countries, in practice this is negligible.

Since some sanctions were imposed after Russia’s annexation of Crimea in 2014, Russian exports to Europe are subject to tariffs, making them uncompetitive. Whereas European TV imports from Russia are subject to a 14% tariff, TVs made in Poland, which is part of the European Union, are not subject to tariff throughout the EU. As of 2020, the output of TV production in Russia was 96% in line with TV demand in Russia.

The war and the associated economic impact in both Russia and Ukraine will negatively impact TV demand in those countries, and DiScien estimates this impact at 3.6M units for 2022, as shown in the chart here. The combined demand in the two countries in 2021, totaled 7.8M units. DiScien expects demand in Russia to decline by 40% and demand in Ukraine to decline by 80% in 2022, calling these estimates optimistic. DiScien anticipates a recovery in 2023, but any assessment of next year should be viewed cautiously, as the toll and outcome of the war are unknown.

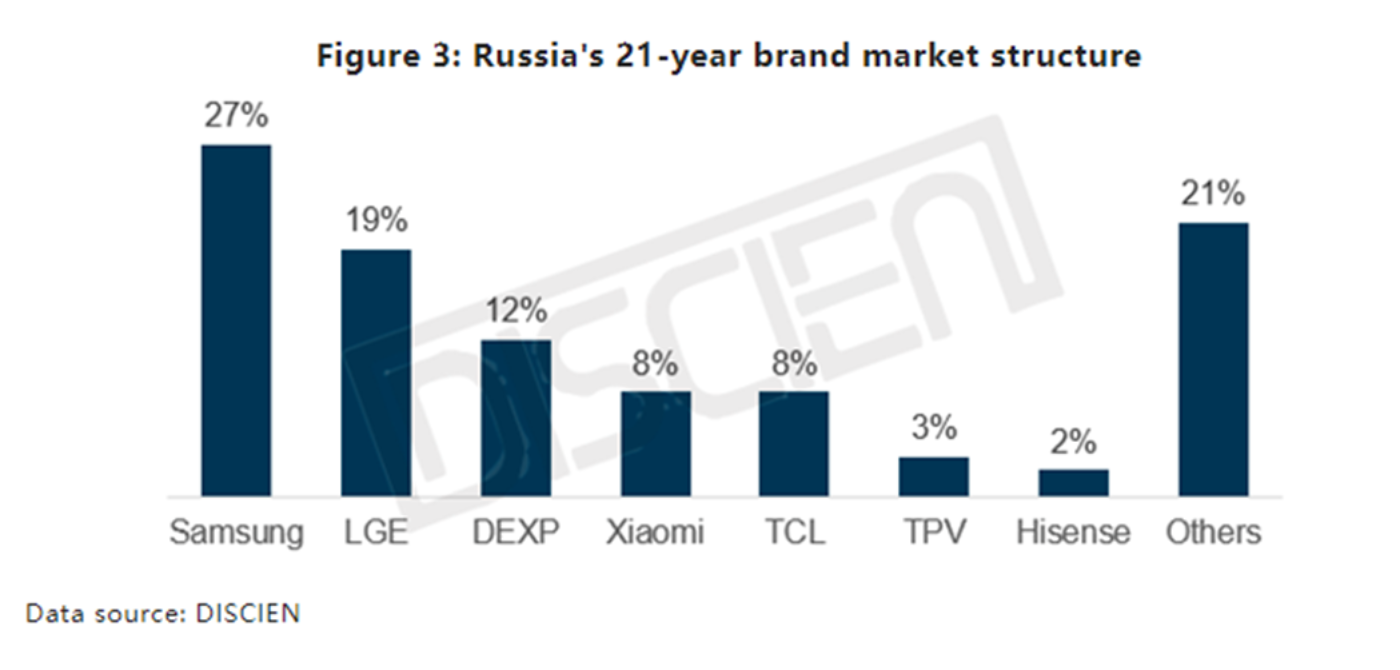

The downturn in the TV market in Russia will have a disproportionate effect on Korean brands, which had the leading position in the Russian market in 2021, as shown in the next chart here. As it is worldwide, Samsung is the leading brand in the Russian market with a 27% share in 2021 and LG is the #2 brand with a 19% share. Samsung TV shipments in Russia in 2021, totaled 1.8M units and LG shipments totaled 1.3M.

On March 5th, Samsung announced that it has suspended shipments of all products to Russia “due to the current geopolitical developments.” In a statement emailed to Bloomberg, the company said that exports of all Samsung products ranging from chips to smartphone and consumer electronics have been suspended. Samsung has a TV production plant in Kaluga, Russia, according to Bloomberg, and besides its TV business, Samsung is the leading smartphone seller in Russia with a market share slightly above 30%. LG Electronics made a similar move on March 19th, announcing that it “is suspending all shipments to Russia and will continue to keep a close watch on the situation as it unfolds. We are deeply concerned for the health and safety of all people, and LG remains committed to supporting humanitarian relief efforts.”

DiScien reports that Samsung’s TV plant in Russia is operating normally, but this may change under pressure from either the Korean or Russian governments. Whereas in 2014, South Korea did not participate in sanctions on Russia, this year South Korea has announced several rounds of sanctions, including a ban on exports of strategic items and severing transactions with Russia’s central bank. South Korea’s further sanctions “will be in line with US financial sanctions,” according to a quote by an official in the country’s finance ministry. Samsung (and LG) might be subject to countersanctions imposed by the Russian government and may face a backlash from patriotic Russian consumers reducing purchases of Korean products, according to DiScien.

Finally, DiScien estimates that the war between Russia and Ukraine will indirectly lead to a 1M unit decline in global TV demand, mainly in Eastern Europe, Latin America, the Middle East and Africa. This indirect effect is attributed to inflation resulting from higher oil and gas prices and the spillover to higher shipping costs. Inflation has been a growing problem in many countries, and DiScien says that “among them, some countries in Eastern Europe/Latin America/Middle East Africa are already facing higher inflation rates, and because of the fragile economies, the probability of being affected by inflation in this event may be greater.”

Although I am not ready to make a quantitative estimate, I believe that this indirect impact may be substantially higher than the DiScien estimate of 1M. I think 1M is a sensible number to start, but mainly an indication that “this effect could be large, and we’ll be watching it.” DSCC estimates that the total TV market in the Middle East and Africa is 26M units and the market in Latin America is 30M units, so a decline in those regions of 1M represents only a 2% impact, and even if it were limited to MEA the impact is only 4%.

Higher inflation is seen not only in energy and shipping; perhaps the more important factor will be in food supply. According to the Wall Street Journal, some 50 countries, mostly poorer nations, import 30% or more of their wheat supply from Russia and Ukraine. Most of this wheat is shipped through ports in the Black Sea, which is now closed to commercial shipping. Ukraine is responsible for 10% of global wheat exports, 14% of corn exports and about half of the world’s sunflower oil. On commodity markets, the price of wheat futures has increased 42% so far this year and the price of corn has increased 27%. Per the WSJ citing Trade Data Monitor statistics, Egypt and Indonesia are the largest buyers of Ukrainian wheat, each accounting for more than 3M tons. Other major buyers are Turkey and Pakistan, which imported 1.7M and 1.3M tons of wheat, respectively, from Ukraine in 2021.

The impact of the Russian invasion of Ukraine will reduce global TV demand in 2022, of that there can be no doubt. The direct impact on those two countries will be substantial for the local markets but will represent less than 2% of the global TV market of ~250M. The indirect impact on demand resulting from higher prices on oil, gas and food is much more difficult to quantify, but it may be much larger.