Q1'25の先端技術FPD搭載TV市場~TCLとHisenseがSamsungの覇権に揺さぶり (1)

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

Q1'25の先端技術FPD搭載TV市場~TCLとHisenseがSamsungの覇権に揺さぶり (1)

先端技術FPD搭載TV市場ではQ1'25もTCLとHisenseが引き続きシェアを拡大しており、過去20年間にわたって市場をリードしてきたSamsungを王座から引きずり下ろす勢いを見せている。Counterpoint Researchが先週発刊した Quarterly Advanced TV Shipment and Forecast Report 最新版で明らかにしている。両社は中国という自国市場で出荷数を大きく伸ばしただけでなく、国外市場でも存在感を高めている。

Counterpoint Researchの Quarterly Advanced TV Shipment and Forecast Report は、ブランド/ディスプレイ技術/サイズ/解像度の各項目別に先端技術FPD搭載TV出荷データを提供しており、市場動向の把握に役立つレポートである。22 ブランド、8 地域、すべてのFPD技術 (WOLED、QD-OLED、MicroLED、MiniLED LCD、QD-LCD、Nano Cell LCD、8K TV) を網羅している。Counterpoint Researchの数十年にわたる業界経験に基づいて開発された独自モデルを活用し、トップダウンの企業レベル調査とボトムアップのモデルレベルデータ収集を組み合わせたものとなっている。先週はQ1'25業績を発表、今月末には最新版の予測を発表予定である。本稿ではQ1'25と2024年通年の動向をレビューする。

Q1’25の先端技術FPD搭載TV世界出荷数は前年比44%増の850万台、出荷額は前年比35%増の85億ドルだった。3四半期連続で出荷数が前年比40%増以上、出荷額が前年比30%増以上となっている。

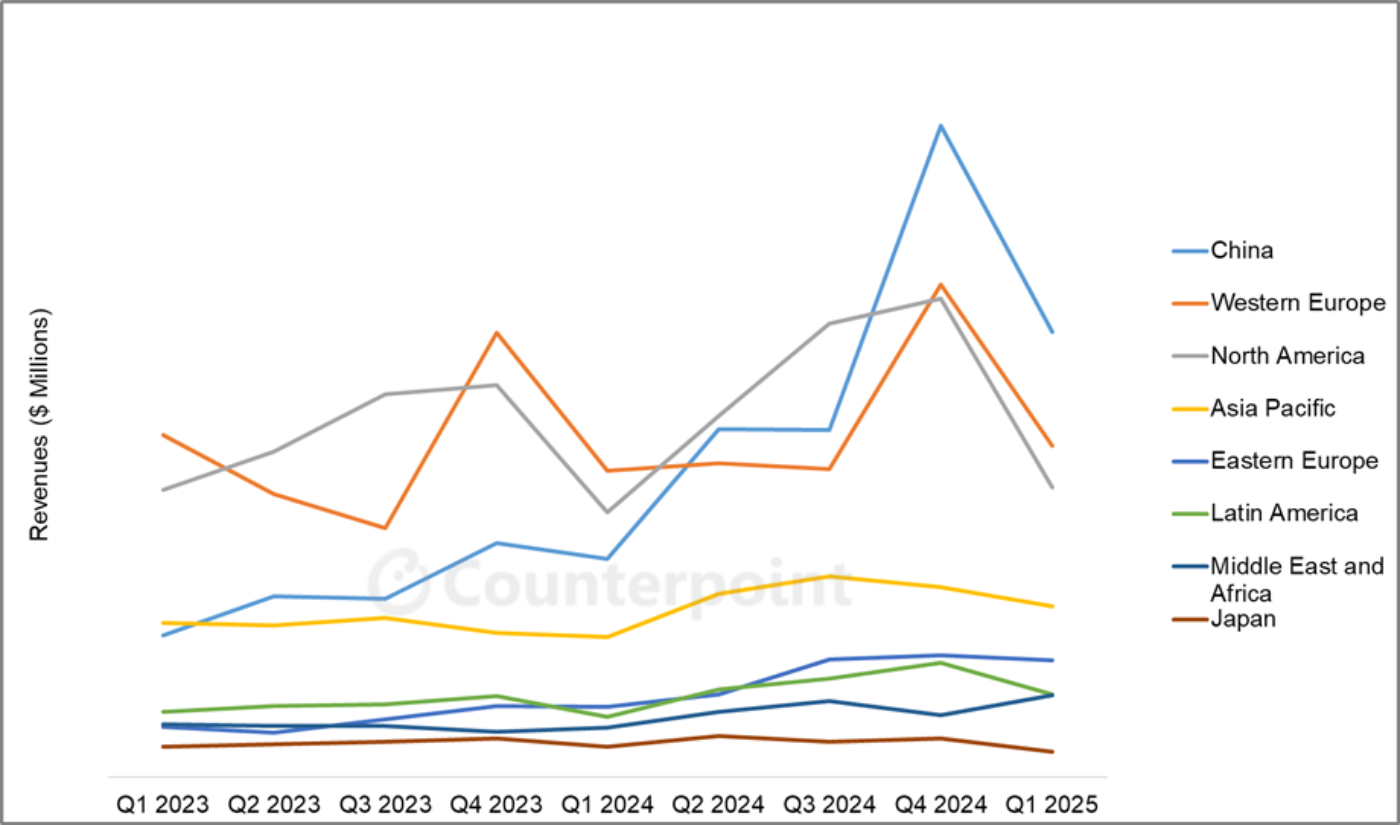

地域別 先端技術FPD搭載TV出荷額推移

一つ目のグラフは、地域別の出荷額推移を示している。中国、北米、西欧の3大地域では第4四半期のピークと比較して季節的な減速が見られたが、Q1’25はいずれの地域も出荷額が前年比増を記録、中国が西欧を上回った。政府の補助金制度によって消費者のTV買い替えが進んだこと、また国内ブランドの積極的な販促展開により、中国の先端技術FPD搭載TV出荷額は前年比104%増、出荷数も前年比139%増となった。中国では消費者が先端技術FPDを搭載した大型で高価なTVを購入したことが読み取れる。

その他の地域の成長は比較的緩やかだったものの、依然として明るい兆しが見られた。西欧のQ1’25先端技術FPD搭載TV出荷数は前年比9%増、出荷額は前年比8%増だった。北米の出荷数は前年比18%増、出荷額は前年比9%増だった。日本を除くすべての地域で、出荷数・出荷額ともに前年比2桁成長を記録した。

中国市場の出荷額成長に加え、他の主要地域市場でのシェア拡大が、HisenseとTCLの世界シェア拡大を後押しした。両社ともに出荷数が前年比で3桁増を記録、出荷額はHisenseが前年比87%増、TCLが74%増となった。先端技術FPD搭載TV市場におけるHisenseの出荷数シェアは、Q1’24の14%からQ1’25には20%に上昇、出荷額シェアも13%から17%に伸びた。TCLの出荷数シェアは13%から19%に急伸、出荷額シェアも13%から16%に上昇した。

両社のシェア拡大はおもに韓国の巨大企業二社のシェアを奪う形で実現された。Samsungの出荷数は前年比わずか1%増、出荷額の伸びも4%にとどまった。先端技術FPD搭載TV市場におけるSamsungの出荷数シェアは、Q1’24の39%からQ1’25には28%に低下、出荷額シェアも38%から30%へと低下した。LGも出荷数が前年比2%増、出荷額が4%増と伸び悩み、出荷数シェアは23%から16%へ、出荷額シェアも23%から18%へと後退した。

SamsungはOLED TVに注力しており、この分野では一定の成果を上げているようだ。次のグラフには、SamsungのOLED TV世界シェアが過去2年間にわたって着実に拡大している様子が示されており、特にQ1’25に大きな伸びが見られる。OLED TV市場におけるSamsungの出荷数シェアはQ1’23の12%からQ1’25には31%に拡大、同期間の出荷額シェアも17%から37%に上昇している。

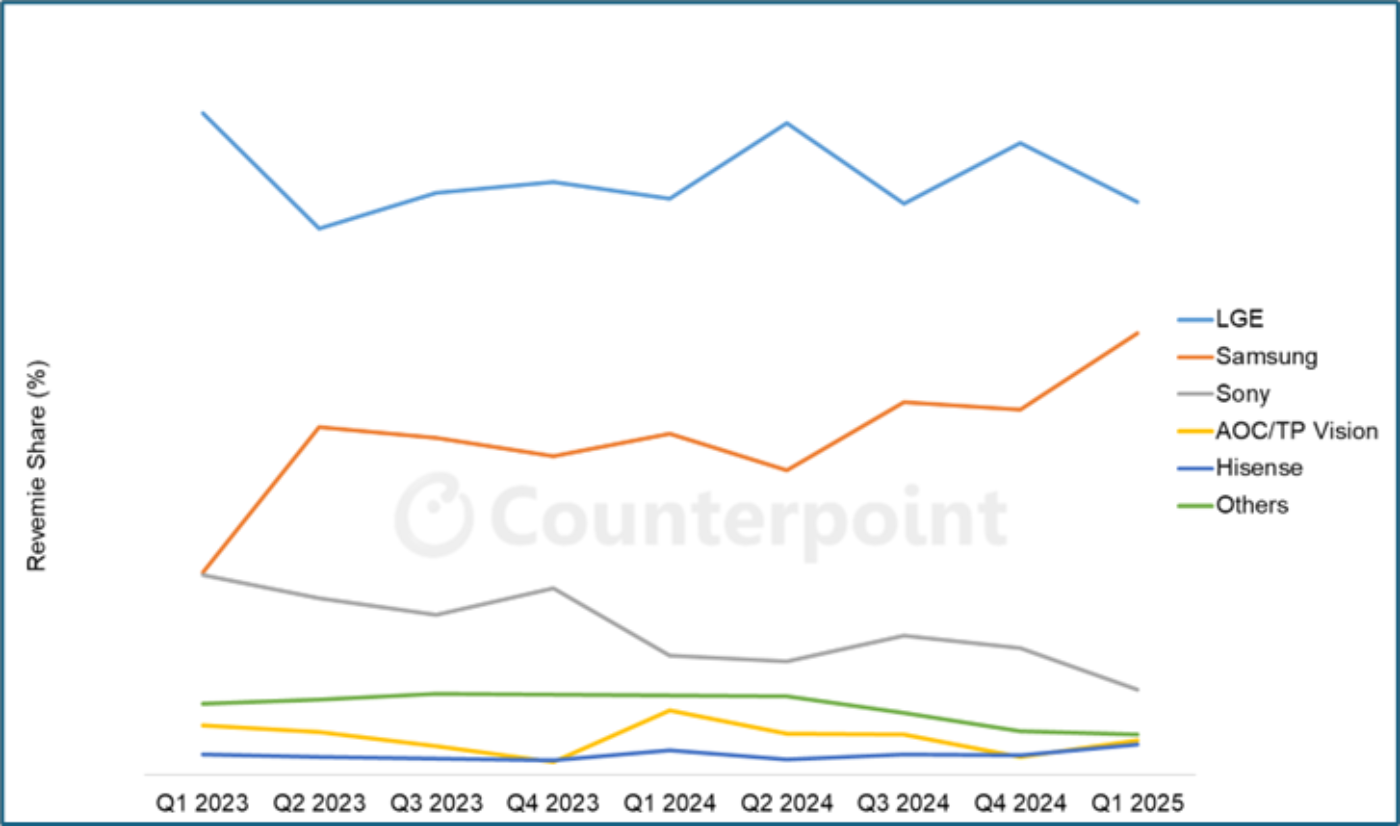

ブランド別 OLED TV出荷額シェア推移

グラフが示すように、Samsungのシェア拡大はLGのシェアを奪った結果ではない。LGは一貫して、出荷数ベースで50%超、出荷額ベースでもほぼ50%のシェアを維持している。実際、Samsungがシェアを奪った相手は、Sony、Panasonic、Philipsなどの他ブランドだった。SonyのOLED TVにおける出荷数シェアは2年前の17%からQ1’25には8%に低下し、出荷額シェアも17%から7%に下がっている。

SamsungがOLED分野でのシェア拡大に取り組んでいる一方、中国ブランド各社は大型MiniLED LCDデルを積極的に推進し先端技術FPD搭載TV市場におけるOLEDの重要度を相対的に低下させつつある。MiniLEDは「スーパープレミアム」市場で着実にシェアを伸ばしている。2023年時点では同市場におけるOLEDのシェアは数量ベースで60%、金額ベースで61%だったが、それ以降はMiniLEDが成長を遂げ、OLEDは伸びていない。MiniLEDはQ2’24にOLEDを上回り、それ以降の各四半期でシェアをさらに拡大している。

MiniLED TVは通常、OLED TVと同等の価格帯で競合しているが、OLEDとLCDではTVパネルコストに差があることから、消費者は「小型のOLED TV」か「大型のMiniLED TV」のどちらにするか、という選択に直面する。現在、MiniLEDを選択する消費者が増えており、それは次の2つのグラフにも示されている。MiniLED LCD TVの出荷数が前年比で159%増加した一方、OLED TVはわずか10%増にとどまった。出荷額ベースでも、MiniLEDが前年比111%増となったのに対し、OLEDは14%増にとどまっている。

OLED TVとMiniLED TVの出荷数 (左) と出荷額 (右) の推移

TCLは2019年に業界初のMiniLED TVを投入したブランドだが、出荷数が本格的に増加したのは2021年以降だった。2021年にはSamsungがMiniLEDを導入し瞬く間にこのカテゴリーの主導権を握った。Samsungは2021年から2022年にかけてこの市場を支配し、2023年も首位を維持していたが、2024年にはTCLに抜かれ、さらにHisense、Xiaomiの順に追い越された。Q1'25にはSamsungは数量ベースで第4位、金額ベースで第3位となり、中国勢を見上げる立場となっている。

Samsungは数十年ぶりにTV市場におけるリーダーの座を失う現実的な脅威に直面している。中国のTVブランド、特にTCLとHisense、さらにXiaomiとSkyworthは、Samsungの得意分野であるOLED TVで真っ向から競うのではなく、中国が優位に立つLCDを活用して低コストのポジションを確立し、そのコスト優位性を武器に、韓国勢が追随できないほどの大型MiniLED LCD TVを積極的に販売促進するという戦略を選んだ。消費者は今、その選択が正しかったことを証明しつつある。

[原文] TCL, Hisense Threaten Samsung’s Leadership in Premium TV Market

TCL and Hisense both continued to gain share in the premium TV market in Q1 2025 and both companies threaten to dethrone Samsung, the market’s leading brand for the last 20 years, according to Counterpoint Research’s latest Advanced TV Shipment and Forecast Report, released last week. The two companies drove a huge increase in shipments in their home market of China but also showed increasing strength in overseas markets.

Counterpoint’s Advanced TV Shipment Report helps understand market dynamics by providing premium TV shipment data by brand, display technology, size and resolution. The report covers 22 brands, 8 regions and all display technologies including White-OLED, QD-OLED, MicroLED, MiniLED LCD, QD-LCD, Nano Cell LCD and 8K TV. The report combines top-down corporate-level surveys and bottom-up model-level data collection with Counterpoint’s proprietary models developed through decades of industry experience. Q1 2025 results were released last week, and an updated forecast will be released later this month. In this article, we will review the latest quarter and 2024.

In Q1 2025, global Advanced TV shipments increased 44% YoY to 8.5 million. Global Advanced TV revenues increased 35% YoY to $8.5 billion. It was the third consecutive quarter of YoY growth over 40% in units and over 30% in revenues.

The first chart here shows revenues by region. While the three largest regions – China, North America and Western Europe – each had a seasonal downturn compared to the Q4 peak, all three regions had revenue growth in Q1 2025, with China outpacing the West. Helped by government incentives that encouraged consumers to trade in older TVs for new models and by aggressive promotions from domestic brands, Advanced TV revenues in China surged 104% YoY on 139% YoY shipment growth. Chinese consumers purchased bigger, more expensive TV sets with more advanced display technologies.

Growth in other regions was more sedate but nevertheless encouraging. In Western Europe, Advanced TV units increased by 9% YoY in Q1 2025 while revenues increased by 8%. In North America, Advanced TV units increased 18% YoY and revenues increased 9% YoY. All other regions except Japan saw double-digit % YoY growth in units and revenues.

The revenue growth in the China market, plus market share gains in other key regional markets, drove global share growth for both Hisense and TCL. Both companies had triple-digit % YoY increases in shipments. Revenues for Hisense and TCL increased YoY by 87% and 74% respectively. Hisense saw its unit share of the premium TV market increase from 14% in Q1 2024 to 20% in Q1 2025 and its revenue share from 13% to 17%. TCL’s unit share jumped from 13% to 19% and its revenue share increased from 13% to 16%.

Those gains came largely at the expense of the two South Korean giants. Samsung’s shipments increased only 1% YoY and revenues increased only 4%. Its unit share of the premium TV market fell from 39% in Q1 2024 to 28% in Q1 2025, while its revenue share fell from 38% to 30%. LG’s shipments increased only 2% YoY and revenues increased only 4%. Its unit share of the premium TV market fell from 23% to 16% and its revenue share fell from 23% to 18%.

It appears that Samsung has been focusing on OLED TVs, and it has achieved some success there. The next chart of the global market share for OLED TVs shows how Samsung has steadily increased its share over the last two years, with a particularly strong jump in Q1 2025. Samsung’s share in OLED TV units increased from 12% in Q1 2023 to 31% in Q1 2025, while its revenue share increased from 17% to 37% in the same period.

As the chart shows, Samsung’s gain was not at the expense of LG, which has steadily maintained more than 50% share of units and close to 50% share of revenues. Instead, Samsung’s gain came at the expense of Sony, Panasonic, Philips and others. Sony’s unit share of OLED TVs dropped from 17% two years ago to 8% in Q1 2025, while its revenue share fell from 17% to 7%.

While Samsung was working to improve its OLED share, the Chinese brands were making OLED less important to the overall premium market by aggressively promoting large-screen MiniLED LCD models. MiniLED is taking an increasingly larger share of the “super-premium” market. Back in 2023, OLED captured 60% of units and 61% of revenues in the super-premium market, but MiniLED has grown while OLED has not. MiniLED surpassed OLED in Q2 2024 and has increased its share of the super-premium market in each quarter since then.

MiniLED TVs typically compete at price points similar to OLED TVs, but because of the cost difference between OLED and LCD TV panels, consumers face a choice between a smaller OLED TV or a larger MiniLED TV. An increasing number of consumers are choosing MiniLEDs, as shown in the next two charts. MiniLED LCD TV shipments increased 159% YoY while OLED TV shipments increased only 10% YoY. Similarly, MiniLED LCD TV revenues increased 111% YoY and OLED TV revenues increased only 14%.

TCL was the first brand to introduce MiniLED in 2019, but its shipments were minimal until 2021. Samsung’s introduction of MiniLED in 2021 allowed it to quickly dominate the category. Samsung dominated the category in 2021-2022 and still led the category in 2023, but was passed in 2024, first by TCL, then by Hisense, and then by Xiaomi. In Q1 2025, Samsung held the #4 position in units and the #3 position in revenues, looking up at its Chinese competitors.

For the first time in decades, Samsung faces a legitimate threat of losing leadership of the TV market. The Chinese TV brands – especially TCL and Hisense but also Xiaomi and Skyworth – have chosen not to try to compete with Samsung’s strength in OLED TV, but instead have chosen to leverage China’s dominance in LCD to achieve a lower-cost position, and then leverage that lower cost to aggressively promote very large MiniLED LCD screens which the South Korean brands cannot match. Consumers are increasingly showing that the Chinese brands have made the right choice.