世界FPD市場の長期予測~2025年のインド向け出荷額シェアが9%へ

出典調査レポート Quarterly FPD Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

世界FPD市場の長期予測~2025年のインド向け出荷額シェアが9%へ

FPD技術は世界的に急速な進化を遂げているが、その背景には、薄型化、軽量化、高輝度化、省エネ化に対する需要の高まりがある。LCDやQLEDからOLED、MicroLEDに至るまで、ディスプレイの種類は多岐にわたり、コンシューマ・エレクトロニクス、IT、自動車、医療、小売、教育、エンターテインメントなど、多様な業界に対応しており、各業界で需要が拡大している。

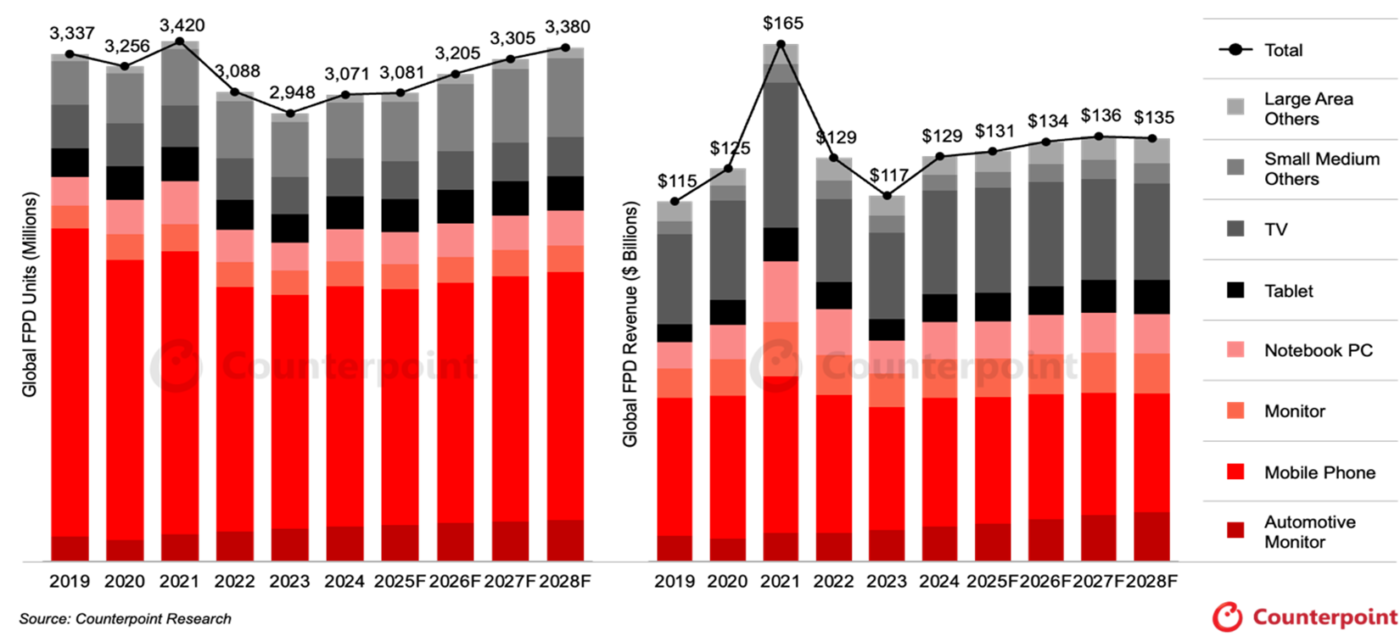

Counterpoint Researchの Quarterly FPD Forecast Report では、各技術別 (LCDおよびOLED) に8つの用途向けの出荷数、出荷面積、平均販売価格 (ASP) 、出荷額、平均画面サイズ、平均解像度などのデータを四半期ベースで提供している。同レポートQ1'25版によると、2025年の世界FPD出荷額は約1310億ドルに達し、2023年から2028年にかけて年平均成長率3%で増加すると予測されている。

世界FPD市場 用途別出荷推移 (左:数量、右:金額)

- 携帯電話とTVが最大の収益源である状況は変わらない。

- 車載モニターが金額ベースで最も高い成長率を示しているのは、高機能化が進むと同時に、数量と画面サイズがともに成長しているからである。

- 中国と韓国が世界のOLED生産能力のほぼ100%を占めている。

- LCD生産は中国と台湾が優勢で、世界の生産能力の約95%を占めている。

インドのディスプレイ革命

2021年12月の「インド半導体ミッション (ISM 1.0)」立ち上げ以来、複数の企業がインドでの大規模なインフラ投資を発表している。しかし、これらの投資はこれまで半導体産業にのみ焦点が当てられており、成長を続けるエレクトロニクス・エコシステムに不可欠なFPD産業はほとんど見過ごされてきた。FPDは、スマートフォン、TV、コンピュータ、自動車、スマートウォッチ、デジタルサイネージといった製品に不可欠である。

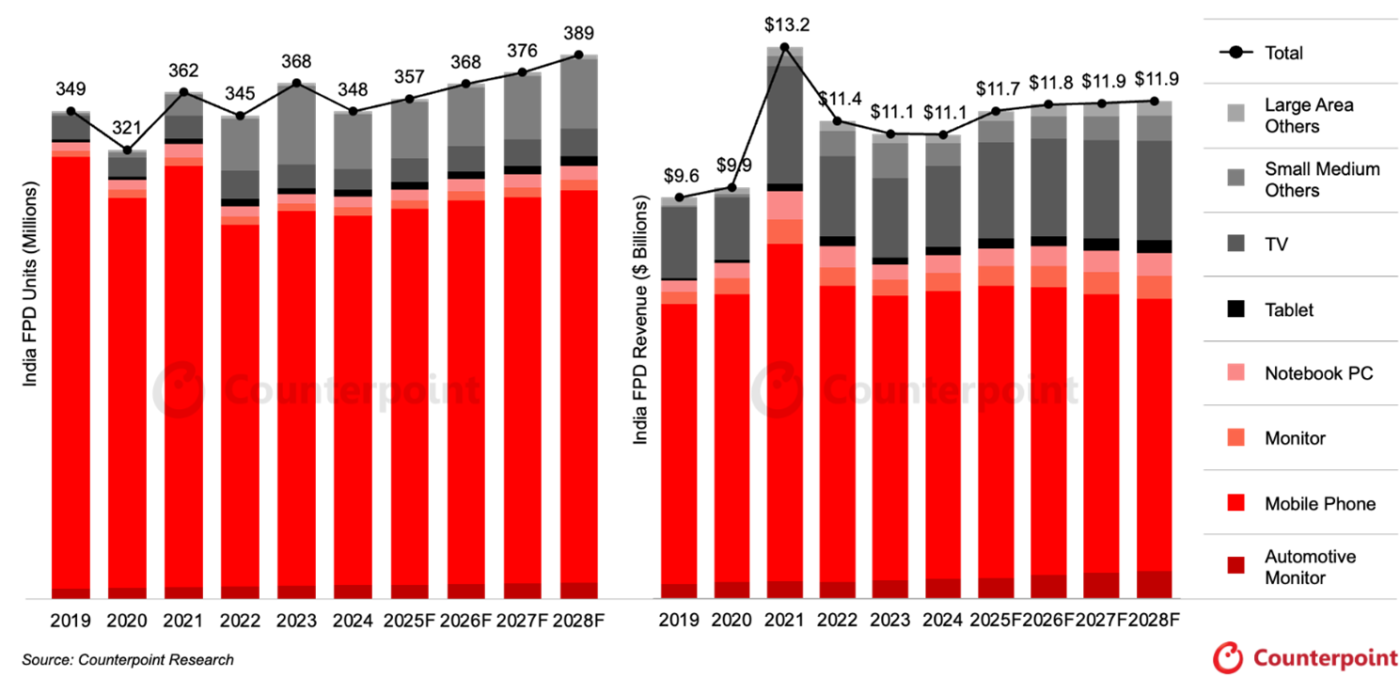

インドFPD市場 用途別出荷推移 (左:数量、右:金額)

- インド向けFPD出荷額は2025年に117億ドルに達すると予測されており、これは世界のFPD出荷額の約9%に相当する。

- 現在、インドで消費されているFPDは100%輸入品である。

- 携帯電話とTVがFPD全体の出荷額の80%近くを占めている。

- IT (タブレット、ノートPC、モニター) と車載モニターが今後も成長するだろう。

- 関税をめぐる地政学的な緊張が高まることで、インドの成長見通しはさらに強まる可能性がある。これは、インド系メーカーが輸出販売を拡大する可能性があるためである。

インドのFPD産業のサプライチェーンを構築するには、この分野における現在の課題と機会に対応し、かつグローバルなベストプラクティスを採用する、戦略的かつ体系的な枠組みの整備が必要になる。

- ディスプレイの主要構成要素の一つがパネルだが、これは複数の精密に設計された層で構成される薄型軽量の構造体で、光を生成または制御し画像を表示する。パネルの設計仕様は、ディスプレイ全体のコストを左右する重要な役割を果たす。

- ディスプレイの製造は、基板の準備、アクティブ層の成膜、カラーフィルター、封止など、複数の工程からなる複雑なプロセスである。

- ディスプレイの製造施設 (fab) の設立には、特殊な設備、クリーンルーム環境、熟練した人材、厳格な品質管理体制などが求められるため、非常に複雑かつ資本集約的な取り組みとなる。

- したがって、インド政府には、「メイク・イン・インディア (Make in India) 」構想および、近く発表予定の「インド半導体ミッション 2.0 (ISM 2.0)」のもとで、ディスプレイ製造エコシステムの確立に向けた戦略的な政策転換と投資促進が求められる。

出典調査レポート Quarterly FPD Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] India Commands 9% of Global Flat Panel Display Revenue

Globally, display technology is evolving at a rapid pace, driven by the rising demand for thinner, lighter, brighter and more energy-efficient screens. From LCD and QLED to OLED and Micro-LED, display types cater to a wide range of industries, including consumer electronics, IT, automotive, healthcare, retail, education and entertainment, and all of these are seeing rising demand.

According to Counterpoint Research’s Q1 2025 Quarterly FPD Forecast Report, which provides quarterly insights into the display market in terms of units, display area, average selling price (ASP), revenues, average diagonal size and resolution for eight different application categories across LCD and OLED technologies, global Flat Panel Display (FPD) revenue is expected to reach about $131 billion in 2025, growing at a 3% CAGR from 2023 to 2028.

- Mobile phones and TVs remain the largest sources of revenue.

- The automotive monitor segment shows the fastest revenue growth because it is growing both in terms of units and screen size while witnessing increasing functionality.

- China and South Korea together account for nearly 100% of global OLED FPD production capacity.

- China and Taiwan dominate LCD FPD production, holding about 95% of global capacity.

India’s display revolution

Several companies have announced major infrastructure investments in India since the launch of the India Semiconductor Mission (ISM 1.0) in December 2021. However, these investments have been focused only on the chip industry, while the FPD industry, an essential part of the growing electronics ecosystem, has been largely overlooked. FPDs are critical for products like smartphones, TVs, computers, cars, smartwatches and digital signage.

- India’s FPD revenue is expected to reach $11.7 billion in 2025, which is about 9% of the global FPD revenue.

- Currently, 100% of the FPDs consumed in India are imported.

- Mobile phones and TVs account for nearly 80% of the overall FPD revenue.

- The IT (tablets, notebook PCs and monitors) and automotive monitor segments will continue to grow.

- Geopolitical tensions over tariffs could further strengthen India’s growth outlook as Indian manufacturers could develop export sales.

To develop a supply chain for India’s FPD industry, a strategic and systematic framework needs to be set up that addresses the current gaps and opportunities in this sector, as well as adopts global best practices.

- Among the key components of any display is the panel, which is a thin, lightweight structure made of precisely engineered layers that generate or control light to produce images. The panel’s design specifications play a key role in determining the overall cost of the display.

- The production of displays is a complex process comprising multiple steps such as substrate preparation, deposition of active layers, color filters and encapsulation.

- Setting up a Display Fabrication Facility (fab) is a complex and capital-intensive endeavor, requiring significant investments in specialized equipment, cleanroom environments, skilled personnel, and stringent quality control measures.

- Hence, a strategic policy shift and investment push is required from the Indian government toward establishing a display fabrication ecosystem under the “Make in India” vision and India Semiconductor Mission 2.0 (ISM 2.0), to be announced by the government soon.