SID Business Conference 講演概要 (TV編)

冒頭部和訳

SID Business Conferenceの「TV市場を形作るディスプレイ技術」セッションでは、ディスプレイにとっておそらく最も重要な用途であるTVに関する最新動向が紹介され、広色域ソリューションをめぐるさまざまなビジョンの競合についても取り上げられた。セッションでは、筆者自身の発表を皮切りに、テレビOEM企業1社と材料メーカー2社による計4件の講演が行われた。

筆者の講演は、この日の2つの優先事項に分けて行った。1つ目は、FPD技術別に見たTV市場の最新動向について、2つ目は、講演後のパネルディスカッションに向けた準備として、関税がFPD業界に与える影響に関する最新情報である。TV市場の最新動向では、まずプレミアムTV市場における3つの主要先進技術、すなわちMiniLED LCD、White OLED、QD-OLEDの間で繰り広げられている技術競争について説明した。それぞれの技術に強みと弱みがあり、どれも最高の画質性能を主張できるだけの根拠を持っている。

画質要素以外にも、MiniLED LCD TVは市場で優位に立つための明確なサプライチェーン上の利点を持っている。White OLEDとQD-OLEDがいずれも単一企業によって製造されているのに対し、MiniLED LCDはパネルとバックライトの両方をさまざまなメーカーから選択できる。また、MiniLED LCD TVは32インチから115インチまで幅広い製品ラインナップがあり、性能の選択肢も豊富で、さまざまな価格帯に対応できる。

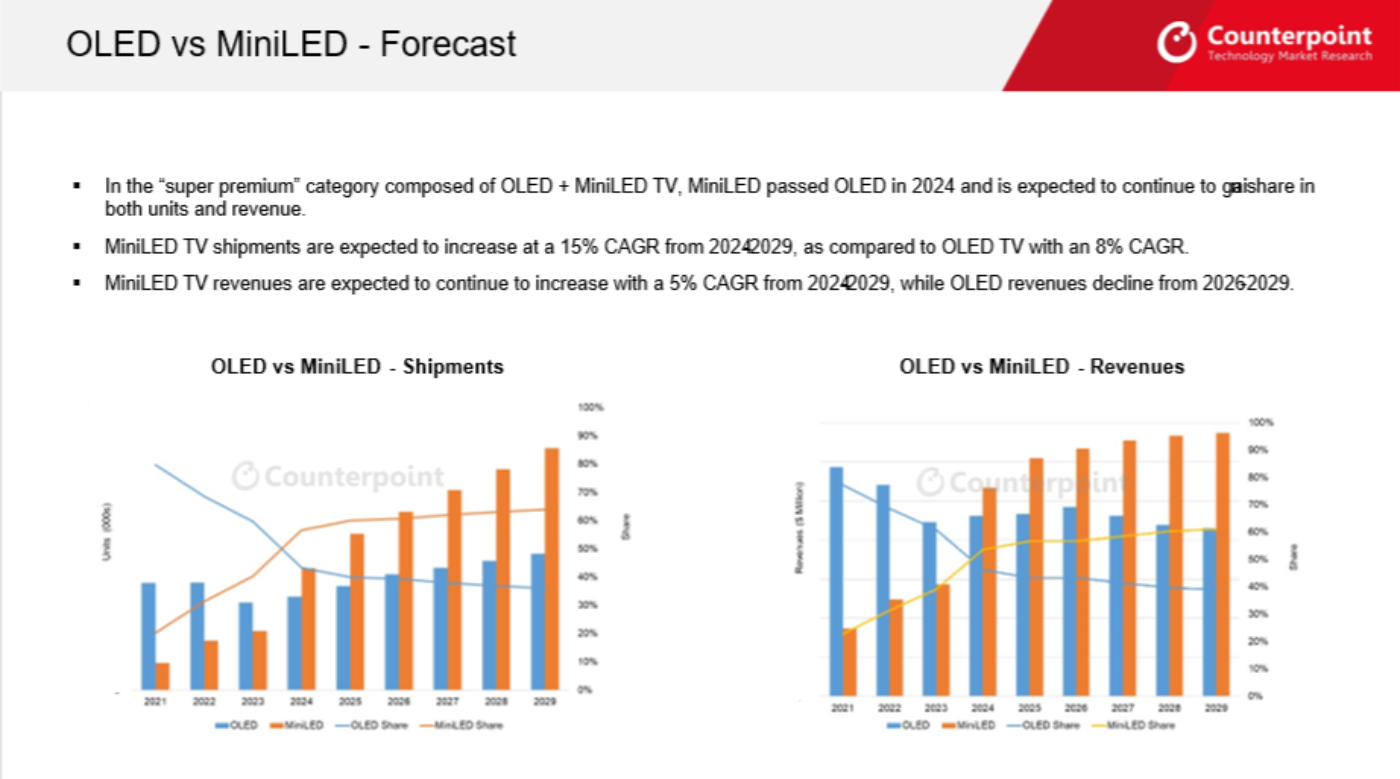

講演では、Counterpoint Researchの Global TV Shipments Quarterly Tracker のデータを用いて、Q2'24にMiniLEDの販売数が2種類のOLED技術を合算した数を上回り、Q4'24にはその差がさらに拡大したことを示した。Counterpoint Researchの Semi-Annual Advanced TV Display Cost Report のデータでは、MiniLEDを含むLCD TV仕様製品のパネル総コストが、すべてのOLED仕様製品よりも大幅に低いことを示した。消費者は、同価格帯であれば小型のOLED TVではなく大型のMiniLED TVを選択する傾向を示している。

筆者はTV用OLED事業を「技術的には成功だが、ビジネスとしては失敗」と位置づけている。Counterpoint Researchの Quarterly Display Supply Chain Financial Health Report のデータを用いて、TV用OLEDを製造する2社、すなわちLG DisplayとSamsung Displayの営業利益を示し、両社ともにこの分野で多額の損失を継続的に出していることを明らかにした。

最後に、TV市場におけるMiniLEDとOLEDの競争に関する当社の長期予測を紹介した。下図がその内容である。両技術ともに出荷数の増加が見込まれるものの、MiniLEDは「スーパープレミアム」市場におけるシェアを台数・金額ともに今後も拡大させるものと予測している。一方、TV用OLED出荷額は2021年のピークを超えることなく、2026年以降は減少に転じると見込んでいる。

SID Business Conference: TV Session Highlights Wide Color Gamut Battle

The SID Business Conference session on ‘Display Technologies Shaping the TV Market’ highlighted developments in arguably the most important application for displays, including competing visions for wide color gamut solutions. The session included four presentations, starting with my own and including one TV OEM and two materials companies.

I split my presentation between two priorities for the day. First, an update on the TV market by display technology, and second, an update on the impact of tariffs on the display industry, as preparation for the panel session later in the day. In my TV update, I first described the technology battleground between three alternatives for premium TV – MiniLED LCD, White OLED and QD-OLED. Each technology has strengths and weaknesses, and each can make a credible claim for the best picture performance.

Aside from the picture quality elements, MiniLED LCD TVs have distinct supply chain advantages that allow them to win in the marketplace. While White OLED and QD-OLED are each manufactured by a single company, MiniLED LCDs have a wide choice of both panel and backlight suppliers. Furthermore, MiniLED LCD TVs are offered in a wider product range, from 32” to 115”, and have a range of performance options to allow multiple price points.

Using data from Counterpoint’s Global TV Shipment Tracker, I showed that MiniLED sales outpaced the combination of the two OLED technologies starting in Q2 2024, and the gap widened in Q4 2024. With data from Counterpoint’s Advanced TV Display Cost Report, I showed that the total panel cost for LCD TV configurations, including MiniLED, was much lower than all OLED configurations. Consumers are choosing to shift up and take a larger MiniLED TV instead of a smaller OLED.

I have characterized the OLED TV panel business as a technological success but a business failure. Using data from Counterpoint’s Display Supply Chain Financial Health Report, I showed the operating incomes of the two OLED TV panel makers – LG Display and Samsung Display, demonstrating that both companies have sustained substantial losses in their OLED TV panel businesses.

I finished up with our long-term forecast for the MiniLED-OLED competition in the TV space, shown here. Although we expect the unit volumes to increase for both technologies, we also expect that the MiniLED share of the “super-premium” space will continue to increase in both units and revenue and that the revenue for OLED TV panels will remain short of its 2021 peak and decline after 2026.

My presentation was followed by a talk from Paul Nangeroni, Senior Director of Product Management for Roku. Nangeroni offered the perspective of a “mainstream TV streamer”, and he started by relating the results of recent consumer surveys among TV buyers. The surveys showed that “picture quality” was the top concern for TV buyers, and surprisingly this was equally true for consumers with a TV budget under $500 as for consumers willing to spend more than $1,500.

A key problem for consumers, brands and retailers is that picture quality is poorly understood by shoppers and is highly subjective. One consequence of this is that while other consumer electronics devices have a high percentage of online sales, TVs are overwhelmingly purchased in brick-and-mortar stores where the consumer can see the product. Nangeroni shared a word cloud on consumers’ thoughts on picture quality, and while a few terms stood out, the myriad terms that consumers use to describe picture quality make it nearly impossible to quantify.

Nangeroni showed examples from the consumer research that consumer preferences varied even when they agreed on the picture elements. One TV which was consistently perceived as the brightest was preferred by one consumer, saying that it made the TV “stand out”, but another consumer thought it was too bright and caused “distraction”. In another example, consumers differed on their preferences when viewing a dark movie scene, with one preferring more background detail and another preferring to see the focus point of the scene.

Nangeroni finished his analysis of picture quality by saying that brightness, color, contrast, motion and detail are the most important attributes of picture quality based on the frequency of comments and self-assessed ranking. He then pivoted to a discussion about streaming.

He showed that Roku has been one of the major drivers behind the shift to streaming, with more than 90 million active accounts in over 50% of US broadband households. He then demonstrated that streamed content is far from perfect, with major shortcomings including banding, mosquito noise, blocking noise, staircase noise and basis patterns. Compression artifacts, bit-rate ladders and lack of HDR degrade picture quality in ways consumers cannot see from a retail floor.

The dilemma in TV streaming is that no one is willing to pay for improving streaming content, which would take more bandwidth. As a result, the mainstream customer, which Nangeroni defined as spending less than $500, loses out. He said that most TVs, even lower-priced TVs, have multiple picture modes which can substantially reduce the most common streaming artifacts for any given picture, but 91% of consumers never use the different modes and watch TV using the factory settings. Roku has been working with content providers to generate metadata which, combined with analysis of individual user preferences, can build a “smart content pipeline" that allows true personalization.

Following Nangeroni, Dr ZhongSheng Luo, GM of Product Development and VP of Sales at Nanosys, described the Quantum Dot (QD) experience for TV. He first introduced his company, now a subsidiary after being acquired by Shoei Chemical. Shoei has built a high-volume manufacturing plant in Japan which started operations in March 2024 and has enough capacity for more than 40 million TVs per year, with further expansions possible up to eight times this amount.

Luo, in a pre-emptive strike at the presenter who followed him, spent the bulk of his presentation showing how quantum dot TVs outperform KSF phosphors. He showed data from RTINGS.COM on TV 2.0 scores from viewers that indicated viewers perceived TVs with QD technology as having better performance on multiple picture quality elements than KSF or what he called “pseudo-QD”.

Luo noted that QD technology provides the best ambient saturation due to better color volume and higher HDR luminance, and described QD’s advantage in response time over KSF, which has a characteristic delay time of 8.5 milliseconds compared to QD’s time measured in nanoseconds.

Luo then turned to an analysis of ambient color saturation, comparing QD to KSF and claiming that “at a typical home/office lighting of 300 lux, QD TV can still maintain 93%-94% DCI P3 coverage while KSF TV will drop below 89%”.

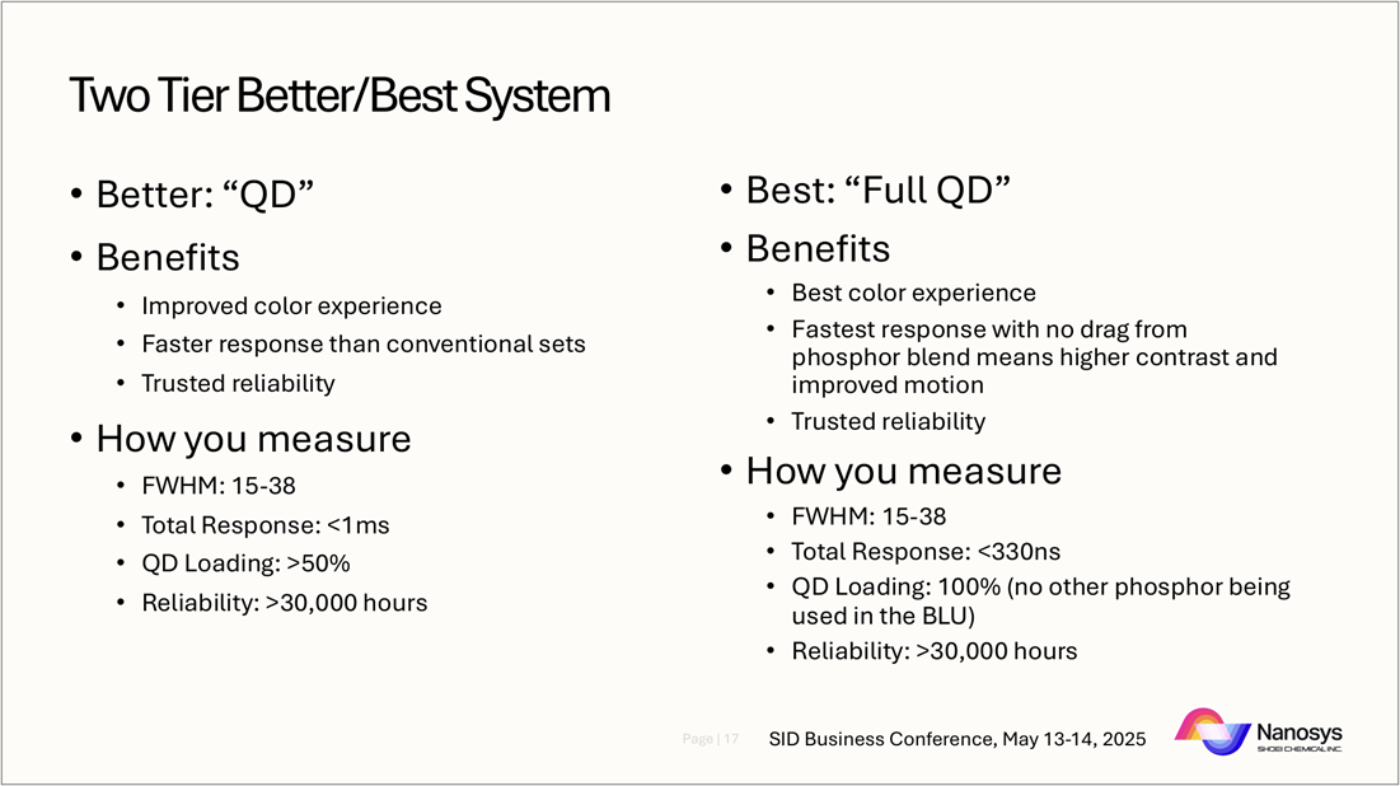

Finally, Luo turned to the issue of “pseudo QDs”, TVs sold as having quantum dots but which exhibit no evidence of the presence of QDs. There have been media reports and at least one lawsuit on this issue. Nanosys proposes that the industry institute some standard for what can be called a “QD TV”, with certain requirements of narrow band emission and that “more than 50% of contribution from QD” is required. He proposed a two-tier system for qualifying QD TVs, as shown in the slide here.

The final presentation came from Dr James Murphy, Chief Scientist and Consultant at Edison Innovations. Edison is a spinoff of the former GE Research group that developed the KSF phosphor. Murphy’s talk countered that of Luo by discussing areas where KSF phosphors clearly have an advantage.

Murphy said that Edison had a portfolio covering six different types of phosphors, including five red phosphors and one green, but he focused most of his talk on only one of these – the KSF for LED package (“on chip”). He noted that more than 85 billion high-brightness, wide-color-gamut LED packages had been sold to date. Of course, this translates to a smaller but unknown number of displays. He showed the chemical composition of KSF (K2SiF6:Mn4+) and listed the 30 patents held by Edison on the technology.

Murphy noted that the first LCDs with LED backlights used broadband phosphors, but that the first quantum dot use in a TV was in 2013, followed by the first KSF use in 2014. He claimed that KSF is used in 2.5X more TVs than QDs, and showed a spectrum profile comparing KSF with a full-width half-maximum (FWHM) of about 15nm with nearly 40nm for QDs.

Murphy noted that while QDs are mostly used in TVs, KSF is much more versatile and is used in a wide range of applications, including the Nintendo Switch gaming system, iPad Air 11 inch, Galaxy A23 smartphone and more.

As a response to Luo’s claim that KSF struggles with response time, Murphy noted that 10 of the top 20 gaming laptops have KSF, including laptops with up to 360Hz refresh rate. He also noted that KSF can be used in multiple different configurations for MiniLEDs, including directly on the LED and in color conversion sheets. Edison has developed smaller grain phosphors for use with MicroLEDs down to 10 microns.

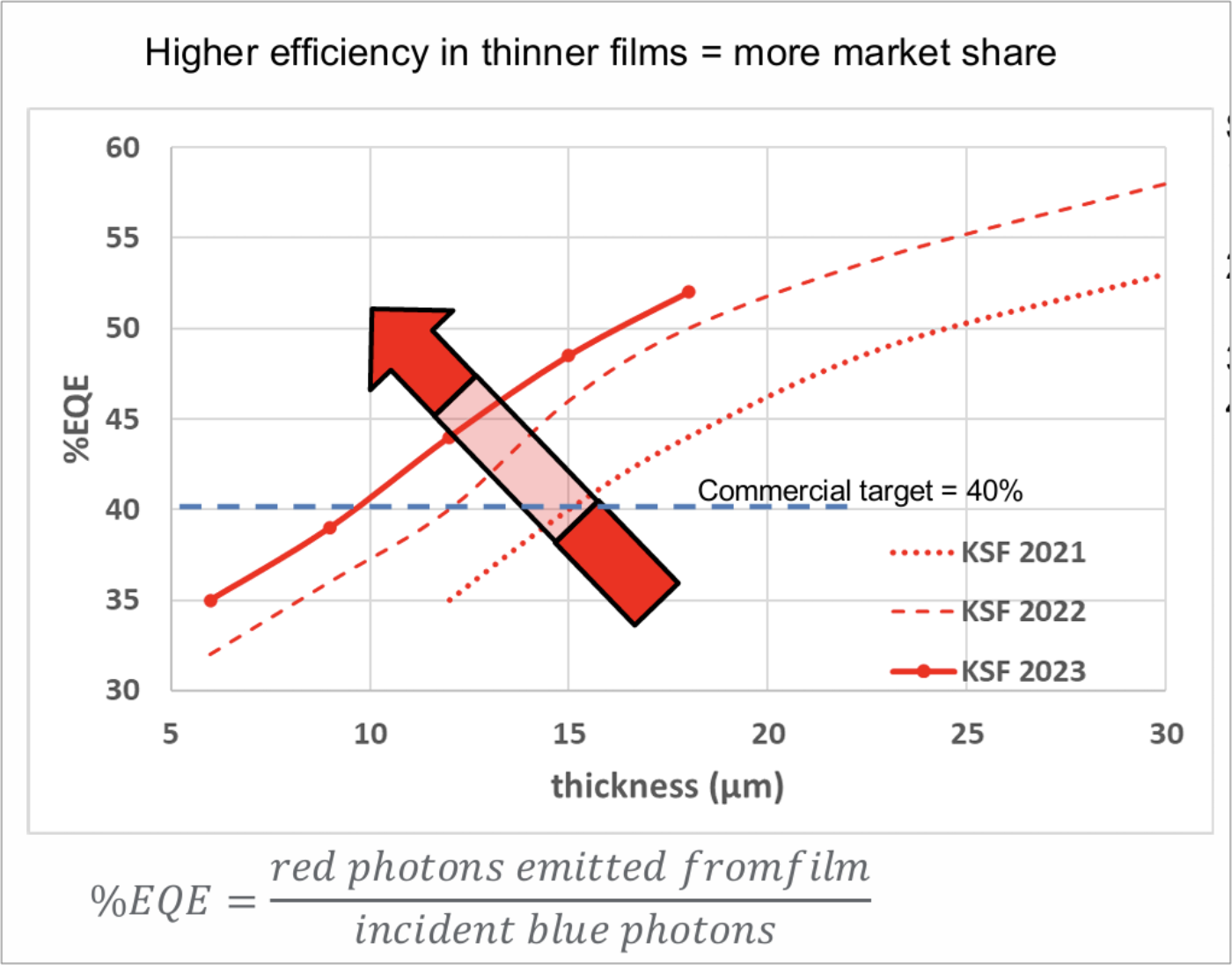

Edison has continued to improve KSF performance, and Murphy showed this chart quantifying the improvement over several years in the absorption of the phosphor to allow its use in thinner films for color conversion. Murphy asserted that when the layer thickness exceeds 10 microns, KSF has superior efficiency performance compared to QD.

Finally, Murphy showed data indicating that KSF is superior to QD in high-flux applications such as color conversion for blue MicroLED. Murphy asserted that many MicroLED applications operate at greater than 1 W/cm2 of blue flux, and in a 5-minute steady-state test at 1.6 W/cm2, KSF phosphors retained their peak emission at 631nm and maintained an intensity greater than 97%, while QDs under the same test exhibited both a peak emission shift from 651nm to 657nm and a loss of intensity of more than 10%.

Counterpoint cannot confirm Murphy’s specific claims of high-flux quenching. On a related issue of thermal quenching, we spoke with Zhongsheng Luo after the Business Conference and he confirmed that QDs change with temperature. He said that peak emission shifted upward by 1nm for each 10°C change in temperature, and described this as a physical effect of the QDs getting larger. This means that an increase of 60°C would be required to observe the emission shift noted by Murphy.

At the end of the TV session, participants could conclude that the battle for wide color gamut supremacy continues, and both quantum dots and phosphors continue to improve performance.