SID Business Conference 講演概要 (IT編)

冒頭部和訳

David Naranjo (Counterpoint Research) – IT市場動向および展望

筆者の講演では、IT市場と技術の展望について述べ、OLEDイノベーション、生産能力投資、製造コスト削減など、ITディスプレイの成長を促進する分野に焦点を当て、当社の長期予測も紹介した。

IT用FPD市場は2023年の前年比8%減を経て、2024年は前年比12%増となった。これは在庫調整と商業需要改善によるものだ。ノートPC用FPD市場は、2023年の前年比13%減の後、2024年には前年比13%増となった。2025年のIT用FPD市場については、関税と需要が先行き不透明であることから、以前の予測である前年比3%成長から、横ばいへと予測を更新している。ノートPC用FPD市場は、以前の予測である前年比5%成長から、前年比1%成長へと予測を更新した。1桁成長となったのは、関税の影響がある一方で、商業セクターからの需要の改善、3-5年の買い替えサイクル、Microsoft Windows 10のサポート終了、さらにAI搭載PCといった要因がその影響をある程度相殺するためである。

SID Business Conference: IT Session Highlights

David Naranjo, Counterpoint Research – IT Market Trends and Outlook

In my talk, I covered the IT market and technology outlook and highlighted areas that will fuel the growth of IT displays, which include OLED innovations, capacity investments and manufacturing cost reductions, as well as shared our long-term outlook.

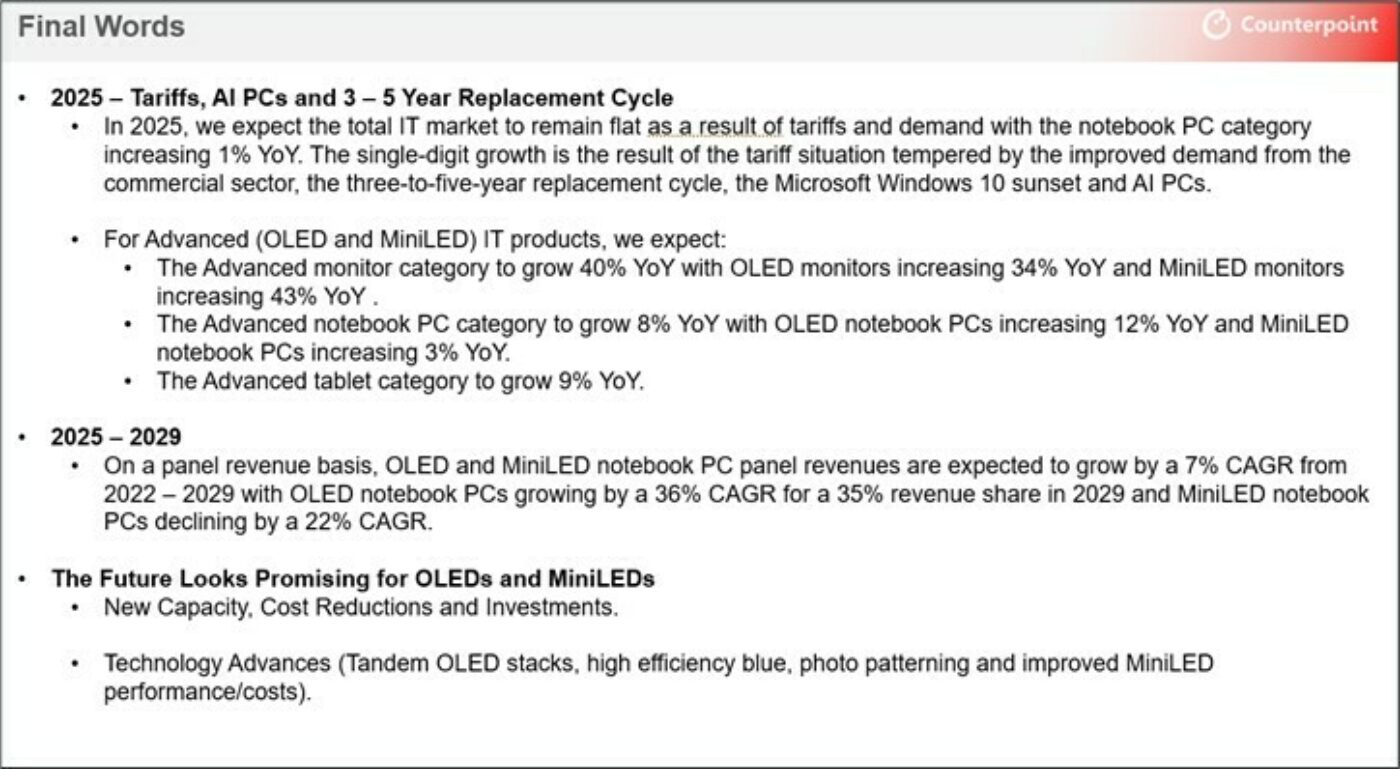

In 2024, according to the presentation, the total IT market increased 12% YoY after declining 8% YoY in 2023. This was due to the rebalancing of inventory and improved commercial demand. The notebook PC display market increased 13% YoY in 2024 after declining 13% in 2023. In 2025, we expect the total IT market to remain flat because of tariffs and demand uncertainty versus our prior forecast of 3% YoY growth, with the notebook PC category increasing 1% YoY versus our prior forecast of 5% YoY growth. The single-digit growth is the result of the tariff situation tempered by the improved demand from the commercial sector, the three-to-five-year replacement cycle, the Microsoft Windows 10 sunset and AI PCs.

For advanced IT displays in 2024, I noted that advanced notebook PCs increased 44% YoY for an 8% share, up from 6% in 2023 due to AI PCs and increased commercial demand because of the three-to-five-year replacement cycle. In 2024, OLED notebook PCs increased 92% YoY and MiniLED notebook PCs increased 14% YoY.

In 2025, we expect advanced notebook PCs to increase 8% YoY, fueled by 12% YoY growth from OLED notebook PCs. For advanced tablets, we expect 9% YoY growth fueled by Google, HONOR, Huawei and others. For advanced monitors, we expect 40% YoY growth, with MiniLED monitors increasing 43% YoY, QD-OLED monitors increasing 40% YoY and W-OLED monitors increasing 19% YoY.

From a brand perspective, I highlighted which brands led in 2024 for advanced notebook PCs and advanced tablets. For OLED notebook PCs, Lenovo overtook Asus for the #1 position due to a wide assortment of new OLED notebook PCs, followed by HP with 18% and Samsung with 14%. For MiniLED notebook PCs, Apple led with a 71% share, down from 79% in 2023 due to gains by Acer, Asus, GigaByte, Lenovo and MSI. In 2025, we expect advanced notebook PCs to increase 8% YoY, with OLED notebook PCs increasing 12% YoY with Lenovo having the #1 share, followed by Asus and HP. For MiniLED notebook PCs, we expect 3% YoY growth with Apple continuing to lead. For advanced tablets, I showed that Apple remained the market leader, with its share rising to 52% in 2024 from 38% in 2023. Apple’s panel shipments jumped 133% YoY in 2024 despite a 50% decline in Q4 2024. Samsung remained in the second position with a 20% share in 2024, down from 29% in 2023. The brand’s panel shipments rose 17% YoY to 2.3 million units in 2024.

I highlighted several new OLED technologies, roadmaps, reduced costs and investments that will help fuel growth for OLED and MiniLED IT displays.

For cost reductions, I showed several examples of manufacturing cost estimates. For example, I showed the manufacturing costs for a 16.2” notebook PC display and a 16.3” notebook PC display using LCDs, MiniLEDs and OLEDs for G6, G8.5 and G8.7 fabs. In 2024, a 16.3” LTPO Rigid + TFE UHD OLED notebook PC cost 307% more than a 16.2” Oxide MiniLED LCD UHD notebook PC display at a G8.5 fab. In 2027, G8.7 Oxide Rigid + TFE Tandem OLED fabs will bring 16.3” Oxide OLED panel costs below G6 LTPO OLED fabs, but 62% above MiniLED costs.

Finally, I shared Counterpoint’s 2022-2029 units and revenue outlook by IT segment and display technology

2022-2029 Revenue Forecast by IT Display by Technology

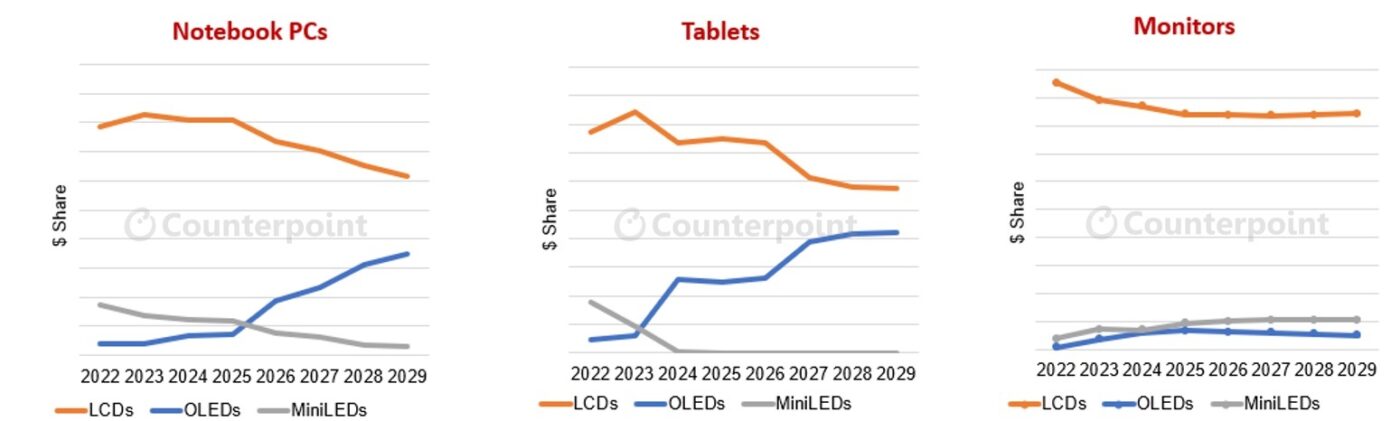

In 2025, we expect a flattish YoY increase after a 12% YoY decrease in 2024 due to tariffs and tempered by demand based on the Microsoft Windows 10 sunset, AI PCs and the three-to-five-year refresh cycle. For notebook PCs, we expect a 1.4% CAGR growth from 2022 to 2029 due to more use cases for AI PCs and brands’ continued focus on the premium segment. In 2026, we expect Apple to launch an OLED iPad Mini from SDC A2, which will account for a big share of the projected 2026 growth of 33% YoY to 16.5 million panels. Overall, we expect the tablet market to increase at a 2% CAGR and OLED tablets to grow at a 19% CAGR from 2022 to 2029.

On a panel revenue basis, OLED and MiniLED notebook PC panel revenues are expected to grow at an 8% CAGR from 2022 to 2029, with OLED notebook PCs growing at a 36% CAGR for a 35% revenue share in 2029 and MiniLED notebook PCs declining at a 22% CAGR. OLED tablet revenues are expected to grow at a 42% CAGR for a 42% share in 2029.

For monitors, the category is expected to decline at a 1% CAGR on a panel revenue basis, with OLED monitors increasing at a 29% CAGR and MiniLED monitors increasing at a 14% CAGR. In 2025, for the OLED category, we expect QD-OLED to have a 73% revenue share, up from 71% in 2024.

My final slide was as follows:

Dr. Georg Bernatz, EMD Electronics - Advancements in OLED Materials for IT displays

Dr Bernatz highlighted the advancements in OLED materials to address market demands related to efficiency, lifetime, color reproduction, and artifact anomalies.

For efficiency, he noted how using low refractive index HTMs as Green Prime layer could significantly enhance the efficiency of a stack, with little effect on voltage and lifetime.

For a higher lifetime, he showed that the addition of a second Green Prime layer could massively boost lifetime with no impact on voltage or efficiency. In addition, the deuteration of hosts improves stack lifetime, with no change in voltage or efficiency. The highest impact on lifetime is achieved with the highest degree of deuteration.

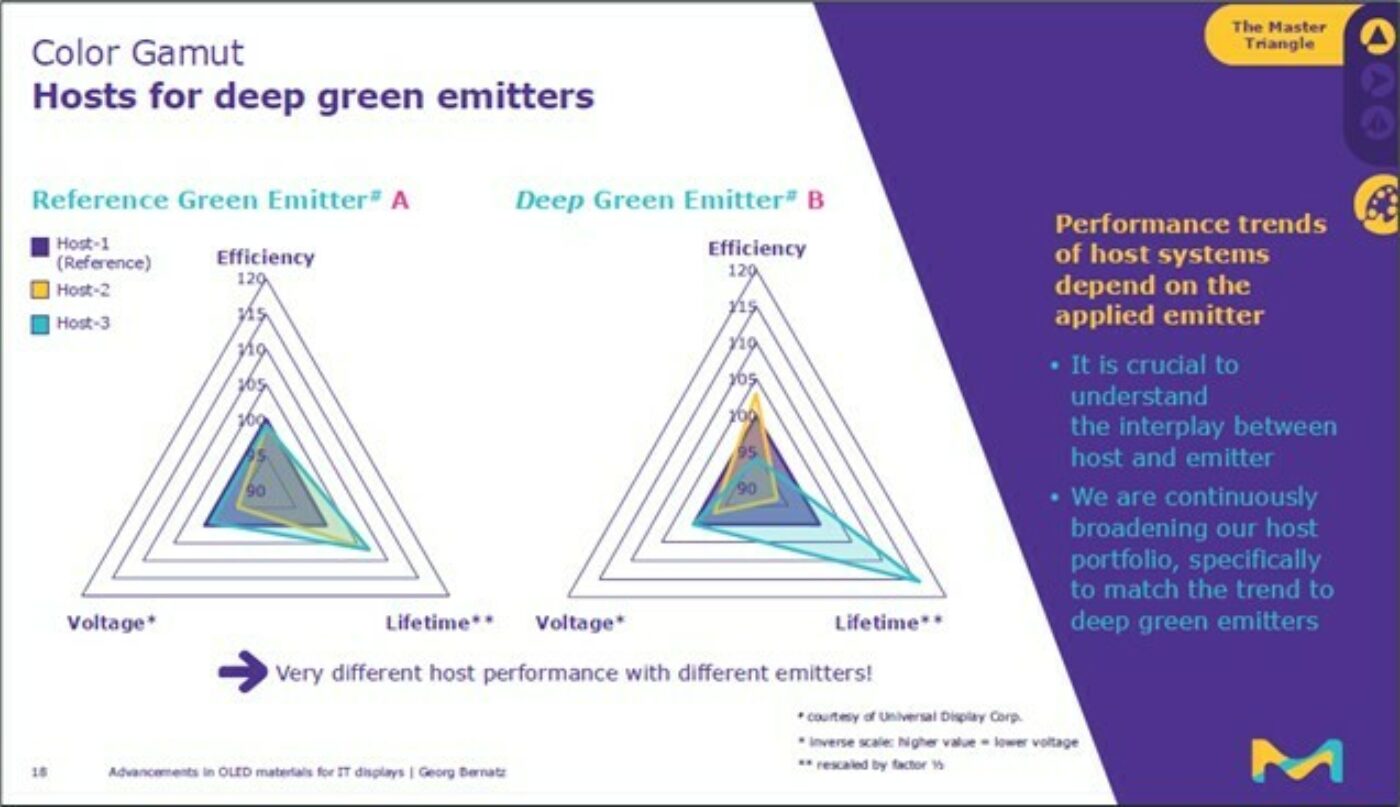

For color gamut, he showed how performance trends of host systems depend on the applied emitter, with color gamut charts showing lower voltage and higher lifetimes by using a deep green emitter and host combination.

For crosstalk, he noted that lateral current is a major issue worsening the color purity in OLED devices. New development L3-HIL (low lateral leakage) allows strongly reduced lateral current at low operating voltage. New HIL materials can strongly reduce lateral leakage current in tandem devices.

Finally for crosstalk, he noted that stack capacitance is an important layer polarity property, which can cause transient Front of Screen (FoS) issues, like trailing in moving pictures or scrolled text. Device simulations clearly show that layer polarity or Material Polarity Factor (MPF) is the most important parameter governing capacitance. As such, the key is the MPF, an intrinsic material property that can be measured in the company’s labs. Merck has a broad portfolio of adapted HTMs and hosts for tuning the capacitance of stacks.

Jan Blochwitz-Nimoth, beeOLED - Lanthanide OLEDs: A Novel Advanced Blue Materials Concept and its Potential Impact on OLED Business

Jan noted that lanthanides have the potential to boost lifetime and maintain the highest efficiency. The lanthanide or lanthanoid series of chemical elements comprises at least 14 metallic chemical elements with atomic numbers 57–70, from lanthanum through ytterbium. In the periodic table, they fill the 4f orbitals. Lutetium (element 71) is also sometimes considered a lanthanide, despite being a d-block element and a transition metal.

Jan noted several key challenges for blue emitters:

Challenge #1 is Vacuum Sublimation. Neutral organic ligand + Lanthanide cation + Counter charges = Organic salts. Sublimation of heavy organic salts poses a major challenge.

Countercharges can be integrated into the molecular design without compromising on photo-physics.

Challenge #2 is OLED efficiency and lifetime. In 2023, it reached the device efficiency target of EQE = 20% = x2 for current emitters in OLED displays. In 2024, it made strong progress in OLED lifetime due to stack/materials/purity enhancements.

Jan noted that Advanced Blue could be utilized by panel makers in two primary ways:

A) Reduce OLED stack complexity by leveraging improved performance → Fewer organic layers are needed, saving costs.

B) Maintain current stack complexity but improve device performance through higher efficiency at comparable lifetimes.

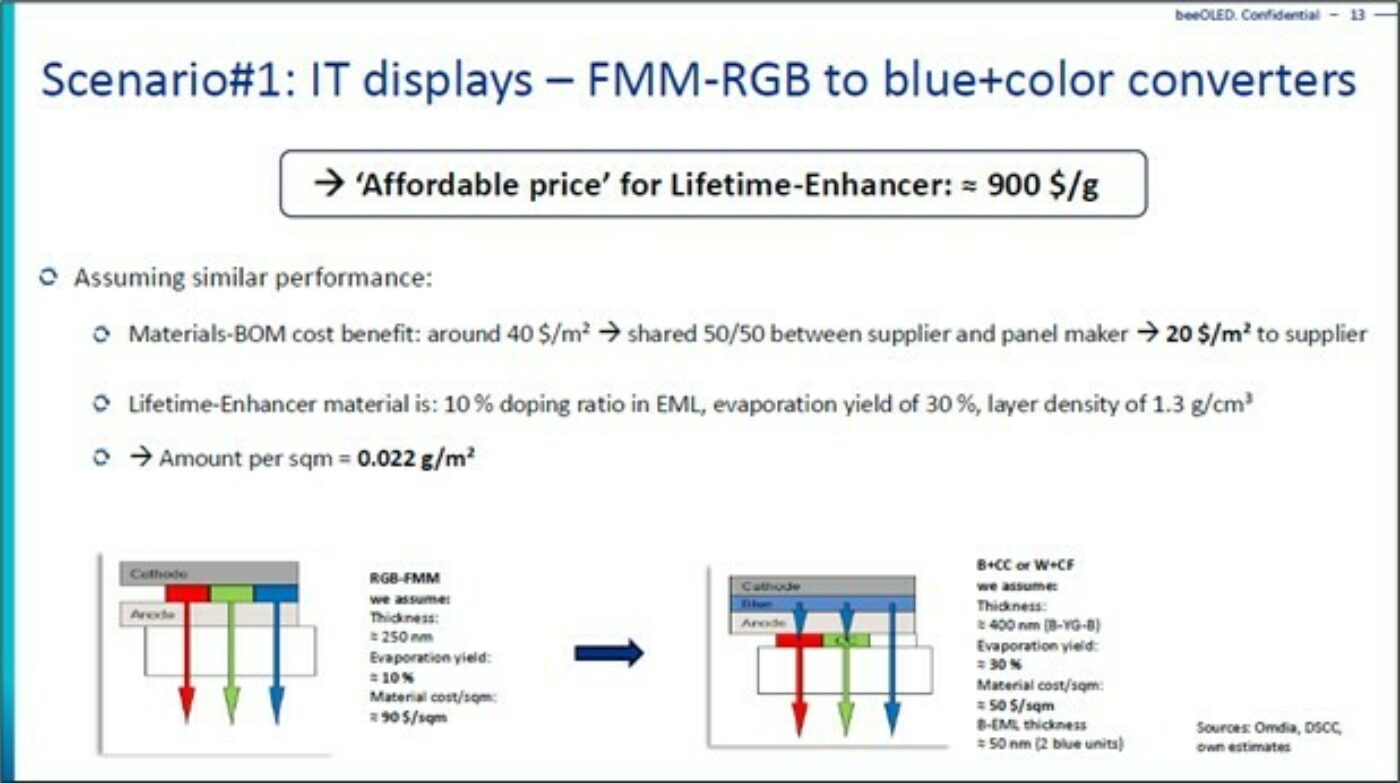

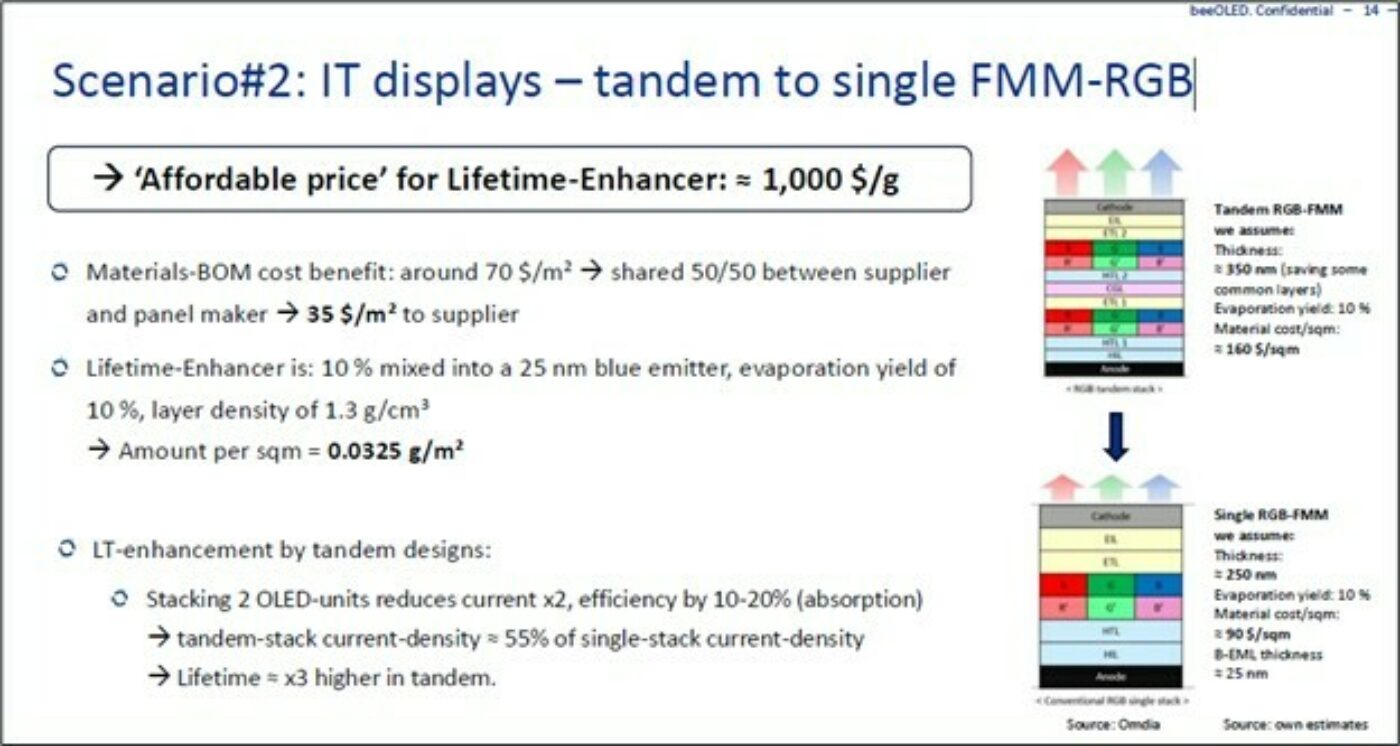

Jan noted that beeOLED uses market and stack data to estimate cost savings on bill-of-material (BOM) for stack materials. The calculated cost benefit is shared equally (50/50) between the panel maker and the material supplier who provides the enabling innovation. Based on the required material volume, beeOLED derives an additional price per gram for the innovative material (emitter or other lifetime-enhancing material).

Two scenarios were highlighted. The first was FMM-RGB-to-blue+color converters where the cost benefit goes from FMM-RGE at around $40/m² to $20/m² for blue+color converters when shared 50/50 between the supplier and panel maker.

The second scenario was tandem-to-single FMM-RGB.

Jan concluded that beeOLED is on its way to enabling lanthanide blue emission, creating a game changer for the OLED display industry. Cost-benefit scenarios explain the strong push by panel makers and material suppliers toward advanced blue OLEDs.

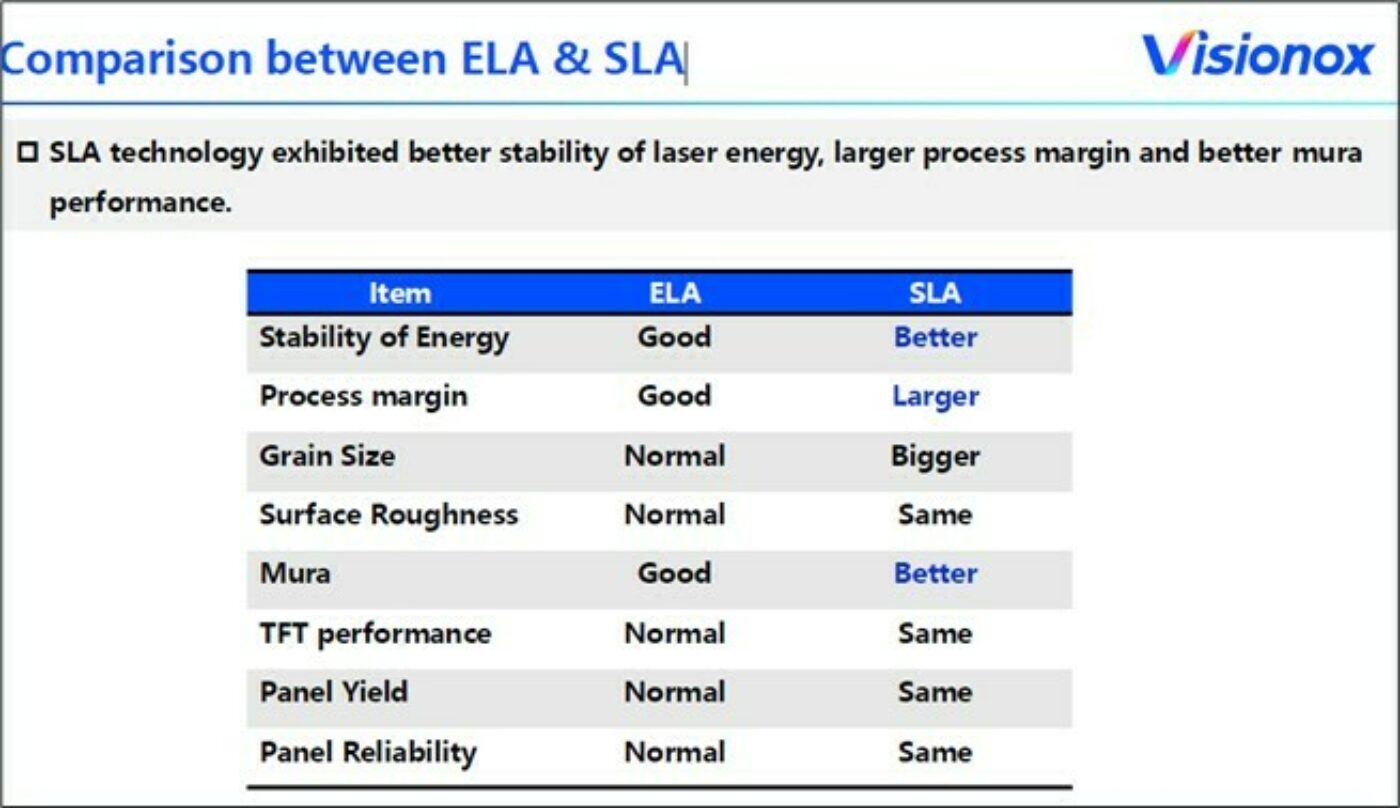

Dr Oliver Haupt, Coherent and Dr Fa-Hsyang Chen, Visionox – Progress on LTPS Backplane Technology for Next-generation OLED Display Panels

Coherent and Visionx teamed up to explain the progress of LTPS backplane technology for the Gen 8 IT fab using SLAs. Oliver started by sharing the benefits of Solid-State Laser Annealing (SLA), which include increased system uptime, better process quality and a larger process window. Excimer Laser Annealing (ELA) and SLA are processes used to enhance the performance of the backplane. ELA uses excimer lasers to anneal the thin-film transistors while SLA, specifically UV-SLA, uses a 343nm UV solid-state laser to achieve similar results with reduced operating costs and maintenance time compared to ELA.

Oliver presented Coherent’s TwinPython diode-pumped solid-state (DPSS) laser annealing system. The development of this system was announced earlier in 2022. Coherent claims that Python offers a 50% lower cost of ownership than traditional excimer laser annealing and even improves on the annealing results. This is achieved by using high-reliability, diode-pumped and solid-state laser technology to precisely duplicate the output of a VYPER excimer laser – including pulse energy, repetition rate, beam size and beam intensity distribution. Python fits existing Coherent LineBeam 750, 1000, 1300 and 1500 systems, and requires virtually no modification to existing ELA processes. This ensures an effortless transition to this higher-reliability, lower-cost laser source.

The other great feature of the LB1300-G8 is that it is compatible with either Coherent VYPER or Python lasers. Python is a diode-pumped, solid-state (DPSS) laser developed to deliver essentially identical output characteristics as the company’s VYPER Excimer laser, but with a significantly lower cost of ownership.

According to Oliver, the Coherent LineBeam LB1300-G8, particularly when configured with Twin Python lasers, enables display makers to manufacture high-volume LTPS backplanes on Gen 8 substrate panels with the highest yield and greatest efficiency.

In collaboration with AP Systems and Visionox, the LB1300-G8 SLA Performance Qualification was completed in March 2025 and the LB750.2 G5.5 SLA Mass Production Qualification was completed in May 2025 at Visionox.

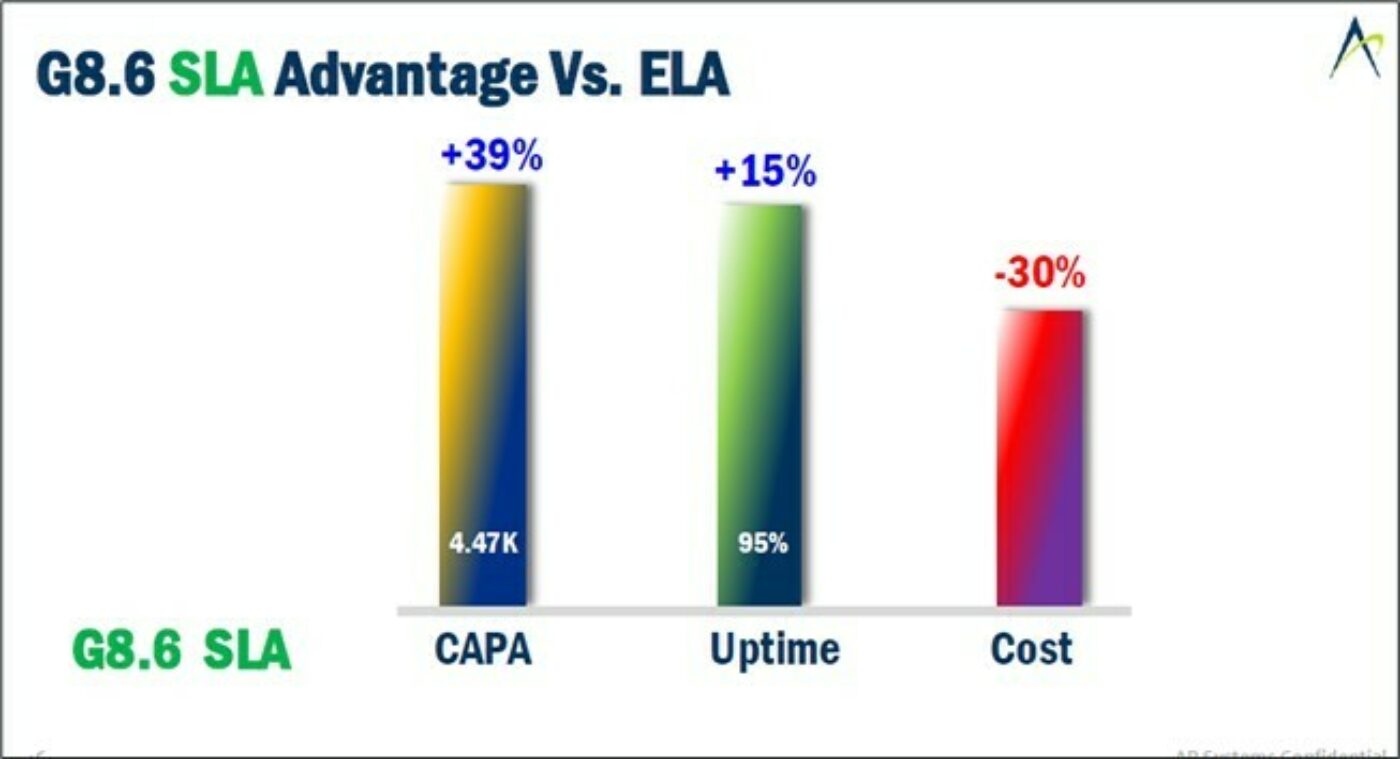

Oliver showed how the G8.6 SLA increases capacity and how increased uptime ad reduces costs when compared to ELA.

Chen then provided Visionox’s detailed schedule for qualifying the SLA system. The project started in July 2023, with the first demo on a G4.5 line in November 2023, followed by the SLA moving to mass production in a G5.5 fab in November 2024 and then final qualification in May 2024. He also noted how the SLA system compared to the ELA system in terms of stability of laser energy, larger process margin and better mura performance.