SID Business Conference 基調講演ハイライト

冒頭部和訳

2025 SID Business Conferenceが5月13-14日に開催された。カンファレンスには16ヵ国、100社以上から約200名が参加した。 (中略) 筆者の講演では、2024年FPD市場の実績、TV/スマートフォン/車載/IT用FPD市場動向および技術動向に焦点を当て、予測を提示した。

2024年はFPD市場が2021年以来初めて成長を遂げた年で、前年比11%増の1290億ドルに達した。LCDは7%増、OLEDは17%増となった。出荷額ベースではFPD業界史上3番目の好実績だった。2021年はコロナ禍で在宅勤務や在宅学習によって需要が急増、FPD業界史上最高の年となったが、2024年と2021年を比較するは興味深い点が浮かび上がってくる。FPD市場出荷額を2021年と比較すると、ほとんどのセグメントで大幅な価格下落と数量ベースの需要減少により、22%減となる。LCD出荷額は32%減少しシェアは74%から64%に低下した。一方、OLEDは2021年から2024年で9%増加しシェアは26%から36%に上昇した。LCDでは車載のみ出荷額が増加しているが、その要因として、出荷数増加、平均サイズ拡大、MiniLEDやQLEDといった先進技術の成長が挙げられる。2021年と比較したOLED出荷額の成長をけん引したのはモニター、タブレット、AR/VR、車載の各分野における300%超の成長で、スマートフォンは5%増だった。

設備投資と生産能力を見ると、OLEDが2016年から2025年のFPD設備投資の50%を占めているが、資本集約度が高く、ディスプレイサイズが小さいことから、業界全体の生産能力に占める割合は10%程度に留まっている。全体として、2025年のFPD生産能力は工場閉鎖により対2022年比でわずか1%増に留まると見られる。2023年から2027年の期間の設備投資は2016年から2022年の期間と比較して大幅に減少すると予測されており、これが財務健全化と稼働率向上に寄与し、いずれ生産能力が逼迫するにしたがい設備投資増加につながると考えられる。OLEDにとっての好材料は、設備投資が2023年から2026年にかけて年々増加しており、AppliedのMAX OLEDソリューションが普及すれば、さらに増加の可能性があることだ。

営業利益率を見ると…

SID Business Conference Keynote Highlights

The 2025 SID Business Conference was held on May 13-14. Around 200 people registered from more than 100 different companies and 16 countries. We had a record number of sponsors with Applied Materials serving as a Gold sponsor and nine other companies – Coherent, Edison Innovations, InZiv, OTI Lumionics, Pixel-Flo, Smartkem, Tianma, Universal Display and VueReal – sponsoring at the Bronze level.

The event was keynoted by:

- Ross Young, VP, Counterpoint Research

- Richard Kim, SVP Overseas Sales, BOE Technology Group

- Dr Eric Cheng, CEO, Tianma America

- Dr Indrajit Lahiri, Corporate VP and GM, OLED Patterning Business, Display and Flexible Technology Group, Applied Materials

In my talk, I focused on 2024 display market results, market and technology trends in TV, smartphone, automotive and IT displays, and provided a forecast.

In 2024, the display market enjoyed its first year of growth since 2021, rising 11% YoY to $129 billion, with LCDs up 7% and OLEDs up 17%. It was the display industry’s third-best year on a revenue basis. With 2021 the best year in the history of the display industry due to strong COVID work-from-home and learn-from-home display demand, it is interesting to compare 2024 with 2021. Relative to 2021, display industry revenues were 22% lower due to much lower prices and lower unit demand in most segments. LCD revenues were down 32%, with its share falling from 74% to 64%. On the other hand, OLEDs were up 9% from 2021 to 2024, with their share rising from 26% to 36%. Only automotive revenues grew in LCDs, with gains in units, average size and in terms of more advanced technologies such as MiniLEDs and QLEDs. What drove OLED revenue growth from 2021 was the >300% growth in monitors, tablets, AR/VR and automotive, with smartphones up 5%.

Looking at equipment spending and capacity, OLEDs accounted for 50% of 2016-2025 display equipment spending, but their share of industry capacity is only around 10% due to their higher capital intensity and smaller displays. Overall, the 2025 display capacity is only 1% higher than the 2022 capacity due to fab shutdowns. Equipment spending during 2023-2027 is projected to be significantly lower compared to 2016-2022, which is contributing to healthier financials and improved utilization and should eventually lead to higher capex as capacity tightens. The good news for OLEDs is that equipment spending is increasing annually from 2023 to 2026, with potential for larger numbers if Applied’s MAX OLED solution takes off.

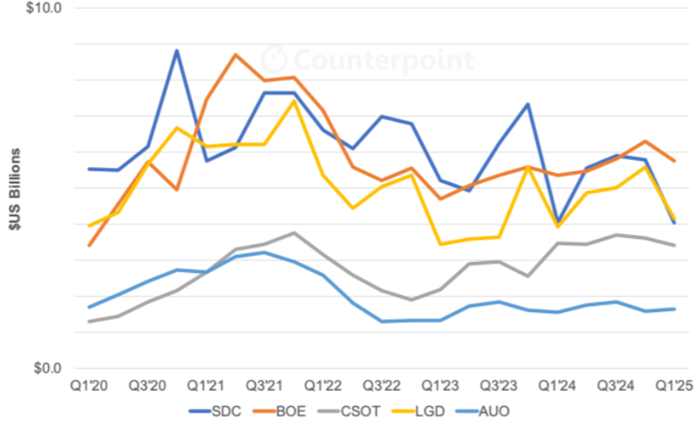

Looking at operating margins, LCD margins have been trending upwards since H2 2022, with China’s CHOT overtaking SDC’s mobile OLED margins in three of the last five quarters. On a revenue basis, BOE overtook SDC in 2024 with a $23 billion to $21.3 billion advantage and has led SDC in three of the last five quarters. LGD was also ahead of SDC in Q1 2025, the first time since Q2 2021. SDC remained #3 in revenues in 2024, followed by China Star.

Quarterly Display Revenues

In the case of TVs, jumbo TVs are a major new trend, with fabs able to produce:

- 98” 2-up at G8.5 with 98% efficiency

- 100” 2-up at G8.6 with 93% efficiency

- 115” 2-up at G10.5 with 74% efficiency

TV prices for 98” and 100” are also affordable at $1,599 and $1,799, respectively, without promotions. 115”, on the other hand, is $14,999 as not all G10.5 fabs are fully depreciated yet, while G8.5 and G8.6 fabs are. The >80” market has quickly risen to the #2 TV category on a dollar basis. China is the largest region for >80” TVs with a >40% revenue share while only having 21% of the overall market. China’s subsidy program, which started in September 2024 and reduced TV prices by 15%-20%, has been a catalyst. The program has been extended through the rest of 2025. Importantly, the surge in 98”-115” LCD TVs will make it more difficult for both OLEDs and MicroLEDs to increase their share in the TV market. In fact, MiniLEDs overtook OLEDs on both unit and revenue basis in 2024, with the average MiniLED TV diagonal, 8”, larger than the average OLED diagonal.

In the case of smartphones, I emphasized the latest shipment results as well as the status of high-efficiency blue OLED materials. LCDs fell 25% in 2024 and now have just a 35% share, losing significant share to rigid OLEDs as Samsung shifted much of its A-Series LCD volume to rigid OLEDs. Rigid OLEDs had the fastest growth by substrate in 2024. Flexible should see the best results in 2025 as Apple shifts E/SE volume from LCD to OLED and all flagships continue to use flexible. Foldables stalled in 2024 and should decline in 2025, although Apple’s entry in 2026 will be a major catalyst for this segment. I showed that flexible OLED smartphone panels have been one of the hottest segments in the display market, rising at least 25% YoY in four of the past five years. By brand, Apple continues to lead, although its share has fallen from around 55% in 2022 to under 40% as flexible OLEDs gain share. By panel supplier, SDC’s share has fallen from 100% in 2016 to less than 31% in 2024, with all four Chinese suppliers earning a double-digit share.

Looking at OLED efficiency, I discussed LGD’s phosphorescent/fluorescent blue tandem OLED, which offers a 15% improvement in efficiency compared to a conventional tandem. Tandem OLEDs have had little penetration to date due to their high cost. This solution should be even more expensive, so it is not expected to take much share. Buyers are waiting on a single-stack high-efficiency blue. Visionox launched the industry’s first high-efficiency blue OLED, which appears in the vivo IQOO Neo 10 using a hyperfluorescence (HF) solution with a fluorescent blue dopant and a TADF sensitizer. It showed a 10% increase in luminous efficiency and a 22% increase in lifetime. 10% is nice, but there is room for further improvement if there is better optimization. One theme is that companies are not just investigating phosphorescent for blue but HF as well. BOE has demonstrated a tandem TADF HF green solution. In addition, on the show floor, Tianma showed HF green using a fluorescent dopant and a phosphorescent sensitizer for cost and performance reasons. Cost can be lower as the volume of material when phosphorescent is used as a sensitizer is much less than when used as a dopant. I showed that at least 12 companies are working on high-efficiency blue consisting of phosphorescent, TADF, HF, HLCT and other solutions. I then explained how HF worked and that there are now a large number of HF combinations with TADF or phosphorescent as a sensitizer and fluorescent, TADF and phosphorescent as a dopant. Why haven’t we seen single-stack phosphorescent blue in production yet? I weighed in on this as well, indicating that it is primarily related to the higher triplet energy levels, higher than red or green and TADF blue, which leads to faster chemical degradation, bond breaking and shorter lifetimes. I concluded that it is too early to say which high-efficiency solution will win in the end, although HF does appear to have a number of advantages today.

Automotive displays are increasingly shifting from a single analog cluster to Bigger, Better and More digital displays. We have found, not surprisingly, that the move towards hybrids, EVs and autonomous vehicles is accelerating this shift. I gave examples of cars that featured multiple tiled displays to make a single large display, as well as cars that are adopting a single large display without tiling. I presented data on annual automotive display shipments, area and revenue for 2022 to 2024, with area growing the fastest, followed by revenues and units. In terms of powertrain, hybrids and EVs are also taking unit, area and revenue display share at the expense of internal combustion engine (ICE) vehicles. I also showed average sizes by powertrain and unit/area/revenue share by frontplane and backplane. LTPS displays overtook a-Si displays on a dollar basis for the first time in Q4 2024, with most large displays (>11”) using LTPS backplanes due to their lower power, higher brightness, narrower borders, lower surface temperature, etc. I also showed display revenue share by brand from 2022 to 2024 for the top 20 brands, with Toyota remaining #1 and BYD remaining #2. On a model basis, the Tesla Model Y remained #1 for the second straight year.

The last segment covered was IT displays, where I addressed the market size, status of OLED penetration by segment, OLED iPad Pro results with updated data for Q1 2025, latest IT OLED fab schedules and the numerous backplane and frontplane technical challenges at G8.7.

In terms of our forecast, we see 1% CAGR from 2024 to 2029 to reach $137 billion. From 2023 to 2029, it would be a 3% CAGR, but still modest. Tariffs are slowing down the 2025 market, which is expected to rise just 1% after 11% growth in 2024. LCDs are expected to be flat from 2024 to 2029, with OLEDs growing at a 3% CAGR to raise their share from 36% to 39%. MicroLEDs are expected to see >100% CAGR but are only expected to see a 0.5% share in 2029. We expect MicroLEDs to earn their first major smartwatch business this year. I also forecasted the market by application and showed OLED penetration by year by application.

Richard Kim, BOE

BOE’s Kim discussed the company’s capabilities and how displays empower IoT, as well as sustainability efforts and progress. He made the point that 68% of IoT devices have a display and 75% of the transmitted data are videos and/or pictures. He also presented consumer data on what consumers value most in display technology, with eye protection and high refresh rate earning the top two scores out of 10 parameters. He also shared BOE’s performance roadmap and described its ADS Pro technology, which it believes delivers the best LCD performance. The technology offers up to 180° viewing angles, 500Hz+ refresh rates, no water ripple when pressed, and low blue light, and is eco-friendly. He also discussed BOE's:

- Dual cell (UB cell) technology, which achieves 95% of BT2020 with a 1400:1 contrast ratio and just 0.7% reflectance.

- 12.1” 5Hz – 144Hz oxide LCD for tablets.

BOE expects to achieve operational carbon neutrality by 2050 and already has 18 national green factories, one lighthouse factory and two zero-carbon factories. He mentioned that BOE’s oxide and LTPO+ tandem products are “green” products with 50% reduction in energy for the former and a 50%+ increase in light efficiency for the latter.

Dr Eric Cheng, Tianma

Tianma’s Cheng focused on the automotive market. He started by showing how the AI attach rate is set to surge with numerous Chinese brands already adopting DeepSeek, while other brands have adopted ChatGPT. The growing inclusion of AI will create new scenarios for display adoption, resulting in even more, bigger and better displays per car, to reference my earlier point. Tianma showed data indicating that the number of color displays per car will rise from 0.5 in 2011 to 2.8 in 2030, with LTPS and OLED gaining share along with larger and higher resolution displays. He claimed that Tianma was #1 in automotive-grade displays since 2020, #1 in cluster displays since 2020, #1 in HUD displays in 2024 and a top-three supplier of small and medium display modules since 2018.

Cheng presented that Tianma has three business models in automotive:

- Automotive displays

- Automotive electronics – it is also assembling completed CID and DIC modules and shipping them directly to customers

- New energy vehicle business

He also presented Tianma’s different display technology platforms:

- Super Fine TFT LCD – multifunctional/display and touch integration, HUD and oxide low-power displays

- Super Fine OLED – foldable, low-power, ultra-low blue light

- Super Fine MicroLED – transparent, unlimited size via tiling, front windshield protection

- Super Fine Extra – fingerprint sensor, smart dimming glass, intelligent communication technologies

He also showcased some of Tianma’s unique automotive display technologies:

- Ultra-wide HD projection displays on the windshield that can be 1.2m long, 8000-10000 nits and have a 1M:1 contrast ratio as shown below. It also reduces blind spots, so there is no need to bend your head to get info. It can be connected to the CID for additional info, etc.

- Ultra-low latency mirrors that can automatically adjust the angle and brightness for ultra-low latency in all conditions

- InvisiVue – display seamlessly integrated into the interior

- Dynamic Flexible OLED display – conforms to curved interior shapes

- High-definition transparent displays – transform windows into smart interfaces. Can also be used for mood lighting. Targeting side windows and sunroofs

- Ultra-bright exterior displays – can display safety tips and messages to others. Could share driving intentions, status and road conditions with other vehicles, etc. Must be ultra-bright, 8000-10,000 nits

Tianma’s Ultra-Wide HD Projection Display

He then went on to discuss all of Tianma’s capabilities, its different fab sizes and locations, etc. He also emphasized Tianma’s recently started G8.6 LCD fab, TM19, its highly automated new module line, TM20, and its MicroLED line in Xiamen. All of these new lines will focus much of their output on the automotive market. Tianma showcased a large number of automotive displays in its booth, which we will cover in a future issue of the Counterpoint Display Weekly Review.

Dr Indrajit Lahiri, Applied Materials

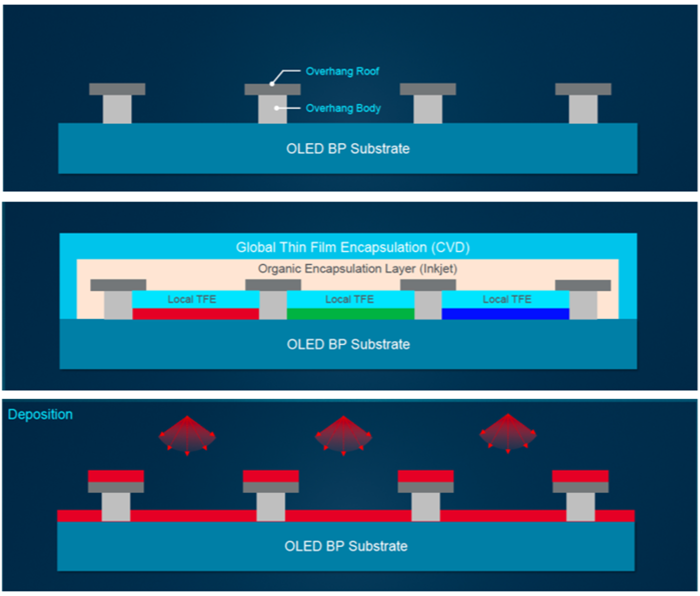

Applied Materials’ Lahiri discussed the status, promise and outlook for the company’s MAX OLED technology. He paid particular attention to the need for an alternative patterning solution in IT OLEDs as fine metal masks (FMMs) have trouble delivering a small enough pixel definition layer (PDL) to enable high-resolution and high-aperture ratio displays. The smaller the PDL, the larger the aperture ratio that enables higher-resolution displays. He commented that PDLs with FMMs are typically ³17um, which leads to low aperture ratios of around 30% compared to LCDs that are around 60%. Applied has developed an alternative structure that produces an overhang PDL structure using lithography, followed by patterning of the RGB OLED layers one color at a time using evaporation, followed by encapsulation. The result is an OLED that delivers the highest brightness at the lowest current density, enhancing resolution, quality and lifespan at a lower cost.

MAX OLED Process

He also discussed the company’s smaller-footprint linear-source vertical evaporation system that also includes encapsulation, which can deposit and encapsulate the entire 15+ layer OLED stack. In terms of OLED performance, it could:

- Double aperture ratio

- Increase brightness by up to 3X

- Increase lifetime by up to 5X

- Can be produced at up to 2000 PPI vs ~800PPI for FMMs

- Reduce crosstalk

- Reduce power by 30%+ helped by a local cathode contact reducing IR drop, etc.

- Require only around half as much OLED material as FMM VTE systems

- Eliminate the need for mask cleaning chemicals

- Enable increased MMG use, which lowers costs

- Could be scaled to G10.5

- Shorten time to market due to FMM lead times

- Enable new pixel structures, such as the ability to easily move back to RGB stripe configurations

- Larger aperture ratios create more room for sensors

- Reduced FMM PDF margins enable a larger transmissive area for transparent displays

- Can be used for Micro-OLEDs

- Improve the ability to offer free-form designs with different shapes

- Is more environmentally friendly and has the potential for greater CO2e savings vs existing display technologies

Note: Visionox showcased 14” ViP displays on the SID exhibition floor that use Applied’s MAX OLED technology. It was great to see the migration to larger and larger MAX OLED displays. They were very bright, although there was some noticeable color shift. We look forward to seeing the performance optimized in the future with little to no color shift.