FPD用ガラス出荷額が10年以上ぶりに過去最高を記録~価格上昇と高稼働率が貢献

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

FPD用ガラス出荷額が10年以上ぶりに過去最高を記録~価格上昇と高稼働率が貢献

Counterpoint Researchが先週発刊した Quarterly Display Glass Report によると、2024年下半期の価格上昇とQ1'25のFPDメーカー各社の高稼働率により、FPD用ガラス出荷額が10年以上ぶりに過去最高を記録した。Q2'25の出荷額は前期比でほぼ横ばいとなり、Q3'25は減少が予測されている。

本レポートでは、すべてのLCDおよびOLED生産ラインを対象に、主要ガラスメーカー全社のガラス投入能力と出荷を追跡している。Counterpoint Researchが誇る、FPD業界の生産能力と稼働率に関する包括的インサイトと、FPD用ガラスとそのサプライチェーンに関する深い理解を組み合わせたレポートである。FPD用ガラス生産の4大地域である日本、中国、台湾、韓国の地域別生産能力を概説し、第1世代から第10.5世代までのガラス出荷を対象としている。また、Corning、AGC、NEGの3大ガラスメーカーとその他のガラスメーカーの出荷についても詳述している。FPDメーカー26社を対象とした調達相関図も掲載している。

Q1’25のFPD用ガラス生産能力は前期比2%減、前年比1%減となった。CorningはSharpの第10世代工場閉鎖を受け、日本での生産を終了した。その一方で中国の国内ガラスメーカーは2023年から2025年にかけて第8.5世代生産能力を追加している。生産能力は依然として需要をやや上回っており、一部は遊休状態にある。

Q1’25のガラスメーカーのFPD用ガラス出荷は前期比5%増、前年比11%増となった。Q2’25の出荷は前期比で横ばい、Q3’25は前期比3%減と予測されている。Q1’25のガラス需要はQ1’22の高水準を下回った。

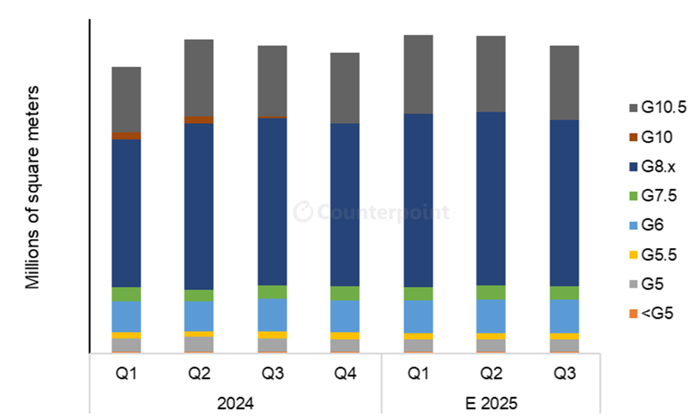

世代別FPD用ガラス出荷の推移 (面積ベース)

Q1’25はFPD用ガラス市場における第8世代以上のシェアが過去最高の79%に達した。これは、米国での関税発動を前にTV製品を出荷するためにLCD生産ラインの稼働率が高まったことや、中国における政府補助金によるTV需要の増加に対応した結果である。現在、Sakai Display Productsが操業を停止したことで、ガラス市場における第10.x世代生産ラインのシェアは約24%で安定しており、第8.x世代が市場の半分以上を占めている。

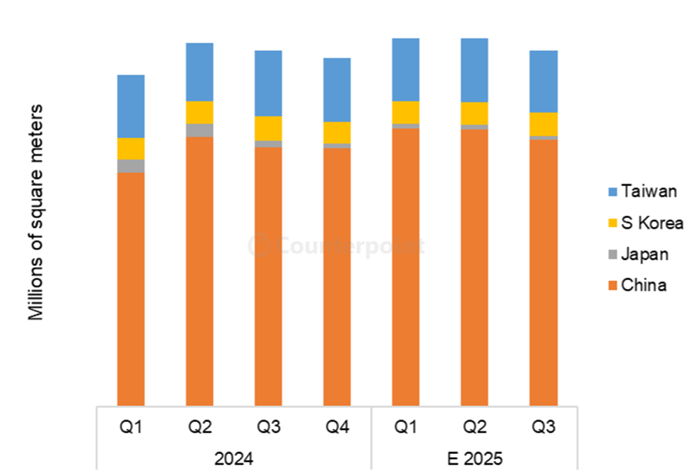

市場を地域別に見ると、FPD業界では中国FPDメーカーが優位を占めており、韓国と日本の影響力が縮小していることがわかる。Samsung DisplayとLG Displayの両社がOLEDにシフトしLCD生産ラインを閉鎖したことで韓国のFPD総生産能力は減少している。2017年以降に増設されたOLED生産能力は、LCDが2枚必要であるのに対し、ガラスが1枚で済むため、ガラス需要はさらに減少している。10年前、韓国はガラス需要の最大地域であり、そのシェアは2018年初めには27%だったが、最近の四半期では約6%で安定している。

本レポートではバックプレーンタイプ別でガラス市場を区分しており、そのデータからFPD業界における先進技術バックプレーンの重要性が浮き彫りになっている。OLEDが成長しているにもかかわらず、業界の主力製品であるアモルファスシリコン (a-Si) ガラス基板がFPD用ガラス需要の90%近くを占める状況が続いている。OLEDに比べてLCDの生産ライン稼働率が高いことから、このシェアは徐々にではあるが低下している。2025年上半期のa-Siのシェアは88%程度になると予測される。

本レポートでは、a-SiガラスとLTPSガラスの基板サイズ別ガラス価格表を掲載している。FPD用ガラス価格は日本円で設定されており、FPD業界のガラス価格は数量や顧客によって異なるが、本レポートでは平均価格を掲載している。戦略的関係を持つ大口顧客 (NEG:LGD、AGC:CSOT、Corning:Samsung、BOE) には平均よりやや低い最低価格が、大口顧客より数量の低い顧客は高い価格が提示されている。

Corningは2023年と2024年の両年に値上げを発表した。CorningはQ1’25までに、両年とも価格 (日本円ベース) を2桁%引き上げることに成功したと発表した。Q1’25のガラス価格は、前期比では横ばいだが前年比では10%上昇し、Q4’16以来の最高値を記録したと推定される。

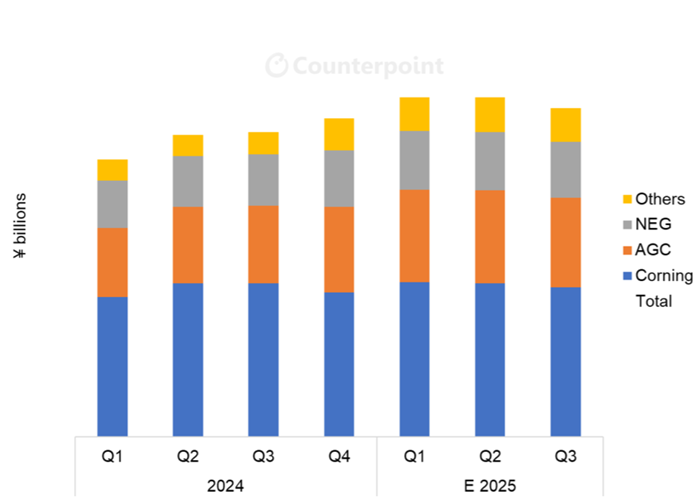

以下の最後のグラフは業界の出荷額見通しをガラスメーカー別に示したものである。なお、ガラス関連の合弁事業については、溶融および成形を行っている企業に出荷額を帰属させている点に留意されたい。NEGはTunghsuとの、CorningはIricoとの合弁事業を有しており、これらの合弁事業による出荷額は、それぞれNEGおよびCorningに帰属させている。

Corningは数量、金額ともにガラスメーカー首位の座を維持している。ただし、Q3’24からQ4’24にかけて、中国の国内ガラスメーカーの生産能力増強とSDP第10世代の閉鎖により、Corningのシェアは低下した。Q2’25の出荷額は日本円ベースで横ばいになると予測されるが、これまでのところ第2四半期の平均為替レートは144円/ドルで、第1四半期から5.5%上昇している。

FPD用ガラスメーカー別出荷額の推移

Source: Counterpoint Research's Quarterly Display Glass Report

------------------------------------

Counterpoint Researchの Quarterly Display Glass Report はすべてのLCDおよびOLED生産ラインを対象に主要ガラスメーカー全社のガラス能力と出荷を追跡しており、地域/FPDメーカー/バックプレーンタイプ/基板サイズなどの項目別にデータを表示できるピボットテーブルを提供しています。第1世代から第10.5世代までのa-SiガラスとLTPSガラスの価格データのほか、Q1’19からの四半期実績とQ3’25までの予測を掲載しています。

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

Price Increases, Strong Utilization Lift Display Glass Market to Highest Revenues in More than 10 Years

An increase in prices in the second half of 2024, combined with strong utilization by panel makers in Q1 2025, drove the display glass market to its highest value in at least 10 years, according to Counterpoint Research’s Quarterly Display Glass Report, released last week. We expect that revenues will be close to flat QoQ in the second quarter of 2025 and decline in the third quarter.

The Display Glass Report tracks capacity and shipments for all major glass makers across all LCD and OLED display fabs. The report combines Counterpoint’s comprehensive insights into industry capacity and utilization with an in-depth understanding of display glass and the supply chain. The report outlines capacity by region in each of the four regions of display glass production – Japan, China, Taiwan and South Korea – and covers glass shipments in Gen sizes from 1 to 10.5. The report details glass shipments for the three major suppliers to the display industry – Corning, AGC and NEG – along with other glass suppliers. The report includes a supply matrix covering 26 panel makers.

Industry capacity for display glass decreased by 2% QoQ and 1% YoY in Q1 2025. Corning has shut down capacity in Japan after Sharp’s Gen 10 fab shutdown. On the other hand, domestic Chinese glass makers added Gen 8.5 capacity during 2023-2025. Capacity remains somewhat higher than demand and some capacity sits idle.

Glass makers increased shipments of display glass by 5% QoQ and 11% YoY in Q1 2025. Shipments are expected to be flat QoQ in Q2 2025 million square meters and decrease by 3% QoQ in Q3 2025. Glass demand in Q1 2025 remained below the high-water mark set in Q1 2022.

The Gen 8 and above share of the display glass market reached an all-time high with 79% in Q1 2025, as LCD fabs ran higher utilizations to ship TV products to the US to avoid impending tariffs and as a response to increased TV demand in China stimulated by government subsidies. Now that Sakai Display Products has shut down, the share of the remaining Gen 10.x fabs in the glass market has stabilized at about 24%, with Gen 8.x representing more than half of the market.

A view of the market in terms of regions demonstrates the dominance of Chinese panel makers in the display industry and the shrinking relevance of South Korea and Japan in the market. As both Samsung Display and LG Display have shifted to OLED and closed LCD lines, their total display capacity in South Korea has decreased. Their glass demand has further reduced because all the OLED capacity added since 2017 requires only one piece of glass, whereas LCD requires two. Ten years ago, South Korea was the largest region for glass demand, and its share was 27% at the beginning of 2018, but it has stabilized at about 6% in recent quarters.

The report also gives a split of the glass market by backplane type, showing the importance of more advanced backplanes in the display industry. Despite the growth of OLED, industry workhorse amorphous silicon (a-Si) glass substrates continue to make up close to 90% of display glass demand. This share is declining but slowly because of high fab utilization for LCD compared to OLED. We expect that the a-Si share will be about 88% in the first half of 2025.

The report provides tables of glass prices by Gen size for a-Si and LTPS glass. Glass is priced in Japanese yen across the industry, and while glass prices in the display industry vary by volume and by customer, the report provides average prices. High-volume customers with strategic relationships (NEG: LGD, AGC: CSOT, Corning: Samsung, BOE) get the lowest prices, slightly lower than the average, while lower-volume customers get higher prices.

Corning announced price increases in both 2023 and 2024. By Q1 2025, Corning declared that it had succeeded in implementing a double-digit price increase in both years (in yen terms). We estimate that glass prices in Q1 2025 were flat QoQ but up 10% YoY and are now at their highest point since Q4 2016.

The resulting outlook for industry revenues is shown in the final chart here, with revenues by glass makers. Note that for glass joint ventures, we attribute revenues to the company with melting and forming. NEG has a joint venture with Tunghsu and Corning has a JV with Irico, and we attribute revenues from these JVs to NEG and Corning, respectively.

Corning remains the leading glass maker both in terms of volumes and revenues. But its share decreased from Q3 2024 to Q4 2024 as domestic Chinese glass makers added capacity and SDP Gen 10 shut down. We forecast that revenues will be flat in terms of yen in Q2 2025, but thus far the average exchange rate in Q2 is ¥144/$, up 5.5% from Q1.

Counterpoint Research’s Quarterly Display Glass Report tracks glass capacity and shipments for all major glass makers across all LCD and OLED display fabs, providing pivot tables that allow splits by region, panel maker, backplane type and TFT Gen Size. The report includes prices for a-Si and LTPS glasses for Gen sizes 1 to 10.5 and includes the quarterly history from Q1 2019 and a forecast through Q3 2025. Readers interested in subscribing to Counterpoint’s Quarterly Display Glass Report should contact info@counterpointresearch.com.