FPDメーカー各社のQ3’23業績プレビュー

出典調査レポート Quarterly Display Supply Chain Financial Health Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

FPDメーカーの四半期決算発表は今回もLG Displayが10月25日(水)に先陣を切るが、今期は業界が昨年末の急激な低迷から回復、大幅な改善が見られる可能性が高い。本稿ではQ3’23業績のプレビューを行う。

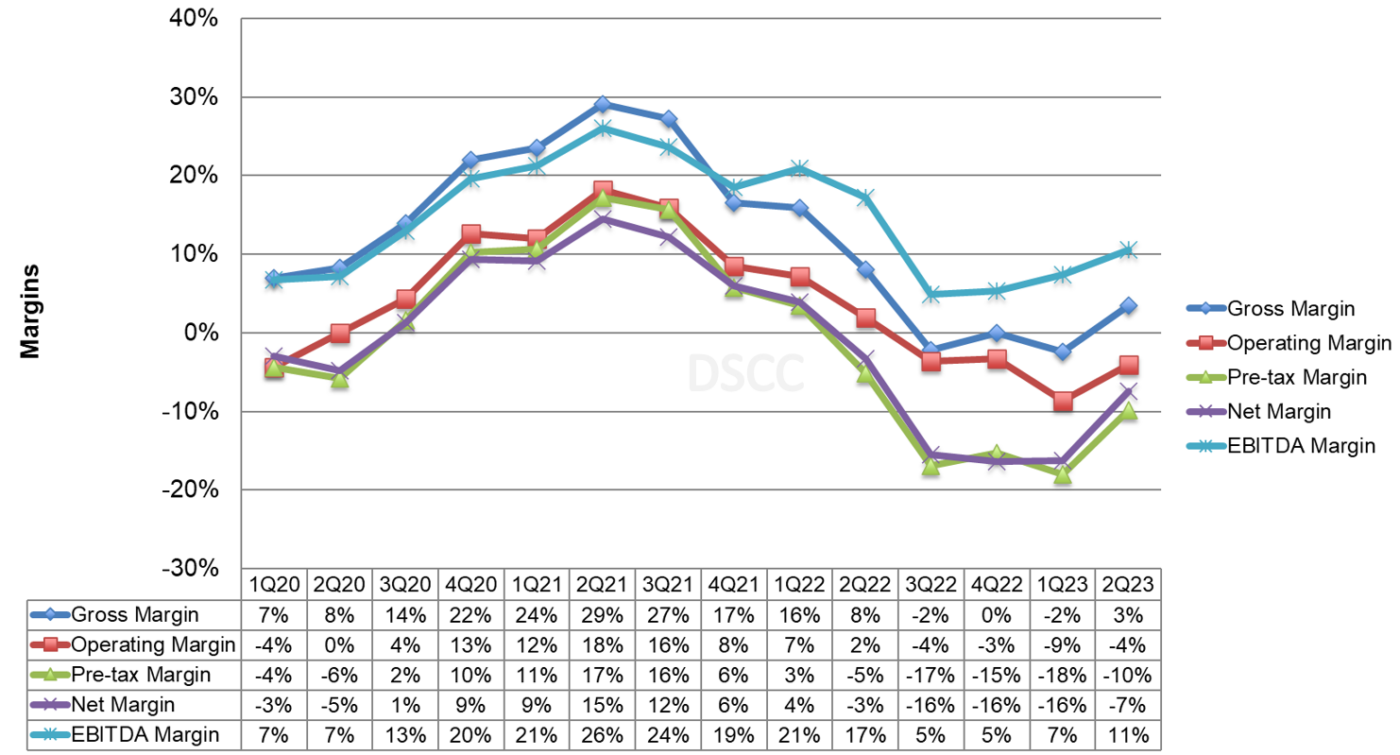

まず、FPD業界の利益率について概要を説明する。以下のグラフに示すように、利益率はQ2’21にピークを迎え、クリスタルサイクルの底から5四半期で頂上に達した。Q3’21以降、業界はQ3’22に底を打つまで5四半期連続で利益率が低下した。利益率はQ1’23まで非常に低い水準で安定しQ2’23に回復し始めた。TV用LCD価格はQ2'23に15%上昇し、利益率の4%-9%の上昇に貢献した。Q3’23にはLCD価格がさらに14%上昇しており、第3四半期も同様の利益率上昇が見込まれる。

Panel Maker Q3’23 Earnings Preview

※ご参考※ 無料翻訳ツール (DeepL)

LG Display will kick off earnings season for panel makers on Wednesday, October 25th, in a quarter that likely saw a big improvement as the industry recovers from its steep downturn at the end of last year. In this article, we will preview the results from Q3’23.

First, let’s set the stage with an industry overview of margins. Margins hit their all-time high in Q2’21, capping a five-quarter run from the bottom of the Crystal Cycle to the top, as shown in the chart here. Q3’21 started a five-quarter run of decreasing margins until the industry hit bottom in Q3’22. Margins stabilized at very low levels through Q1’23 before starting to recover in Q2’23. LCD TV panel prices increased by 15% in Q2’23, helping to boost margins by 4%-9%. Panel prices increased by another 14% in Q3’23, so we expect Q3 to show a similar boost in margins.

Display Maker Quarterly Margins

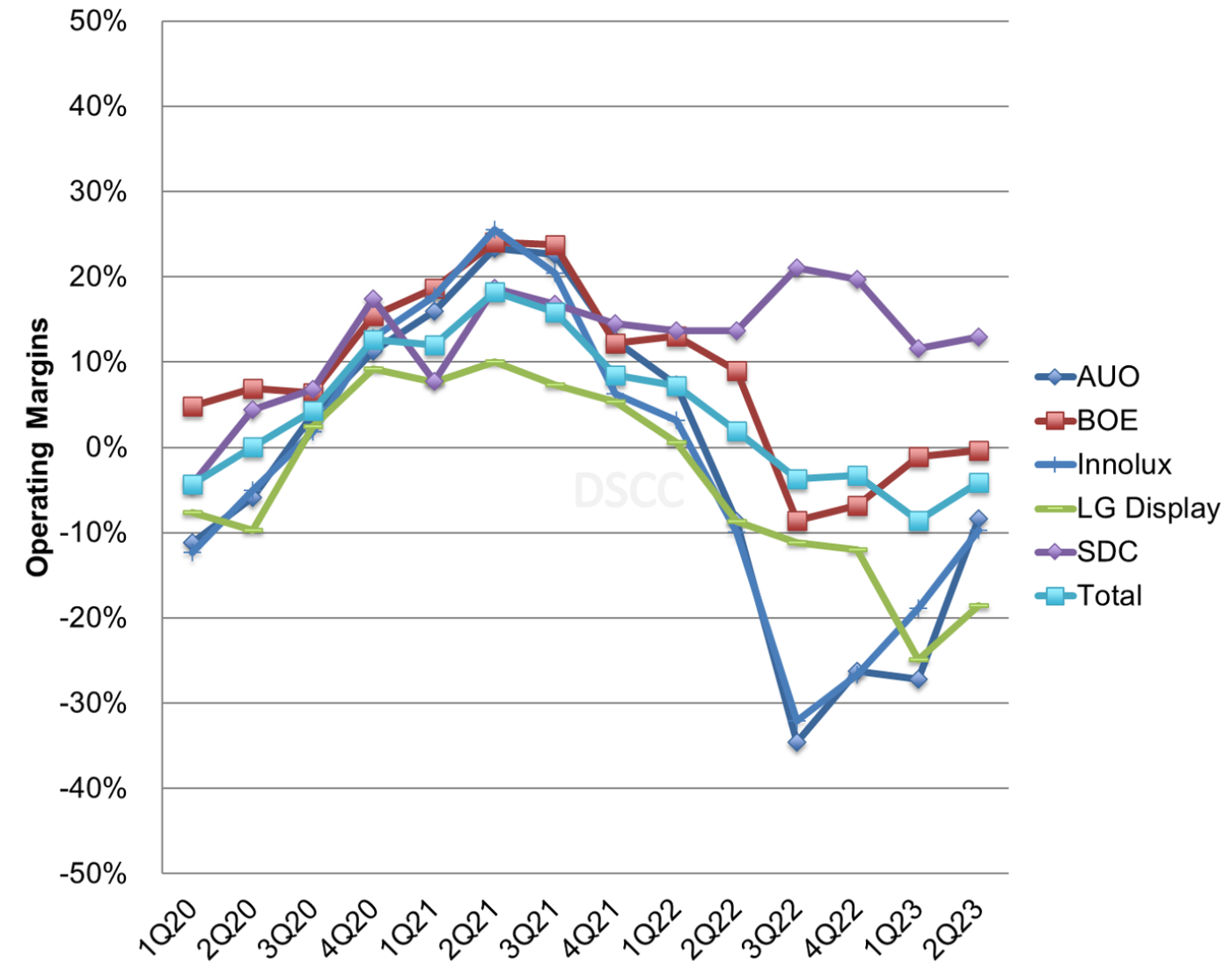

The second chart shows the operating margins of the larger companies in the industry from 2020. While operating margins held in a tight range in 2020-2021 following the Crystal Cycle, and while the Crystal Cycle still characterizes the industry average margins, we see an increasing divergence of performance among panel makers.

- SDC has continued to report positive operating margins and SDC is now immune to declines in LCD panel prices since it stopped all production of LCD in June 2022. In terms of operating profit, SDC saw a seasonal slowdown in the first half of 2023 after a record performance in the second half of 2022, but we expect SDC margins to again improve in Q3’23 with seasonal demand kicking in.

- AUO, Innolux and LGD have been more sensitive to the cycle with margins that fell sharply from Q2’21 through Q3’22. LGD fared better than the two Taiwanese companies in 2H’22 based on its emphasis on OLED panels, but the Taiwan players’ strength in LCD has helped them recover faster than LGD.

- BOE fell to an operating loss in Q3’22 for the first time since 2016 and reported operating losses in both Q4’22 and Q1’23, although BOE’s losses were substantially lower than its LCD competitors. BOE continues to benefit from government subsidies which cushion the company against downturns.

Display Maker Quarterly Operating Margins

Most panel makers benefitted from currency tailwinds in the third quarter. The Japanese yen weakened by 5% Q/Q and by 4% Y/Y, the Chinese yuan weakened by 3% Q/Q and 5% Y/Y and the Taiwan New Dollar weakened by 3% Q/Q and 4% Y/Y. The exception to this pattern was the Korean won, which was flat Q/Q and strengthened by 2% Y/Y. Since panel prices are generally expressed in US$, and these companies have costs in local currency, the stronger dollar should boost margins.

In terms of guidance, in July these companies expressed cautious optimism for Q3’23, and the first indications are consistent with guidance:

- LGD expected area shipments to increase by a mid-single digit % Q/Q and for ASPs to increase by a high-single digit %.

- AUO expected area shipments to be up by a low-single digit % Q/Q and ASPs to be up by a low-single digit % Q/Q on a product mix adjusted basis, implying revenue growth of mid-single digit % Q/Q.

- Innolux expected large panel shipments to be flat Q/Q, small/medium panel shipments down by a high-single digit % and blended ASP to be up by a high-single digit % Q/Q.

Innolux revenues were up 3% Q/Q in Taiwan dollar terms, but its large panel shipments were down 17% Q/Q and small panel shipments were down 6%. AUO revenues were up 10% Q/Q, slightly better than guidance.

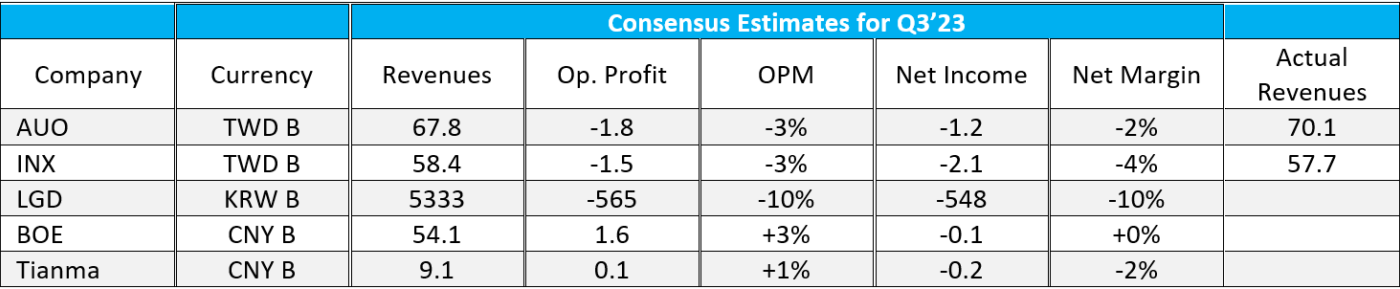

The table below shows analyst expectations for Q3’23 for the panel makers with analyst coverage, according to marketscreener.com. The analyst expectations for margins anticipate that margins in Q3’23 were improved from Q2’23 but still in the red for all except BOE and Tianma. AUO revenues were 3% higher than analysts’ expectations so AUO is likely to do better on operating margin as well. On the other hand, Innolux revenues were 1% below expectations, so Innolux is unlikely to beat expectations.

LGD’s guidance implies an increase in revenues (in KRW) of low-to-mid-teens % and consensus estimates predict a revenue increase of 12% Q/Q, so if LGD meets its guidance it will meet consensus expectations.

Perhaps more important than the results will be the guidance given about Q4’23. With LCD panel prices peaking in September/October and some inventory building in the value chain, we believe that panel makers will be cautious about the fourth quarter.

出典調査レポート Quarterly Display Supply Chain Financial Health Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。