Q2'25のOLED出荷速報~モニターとノートPCが好調

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

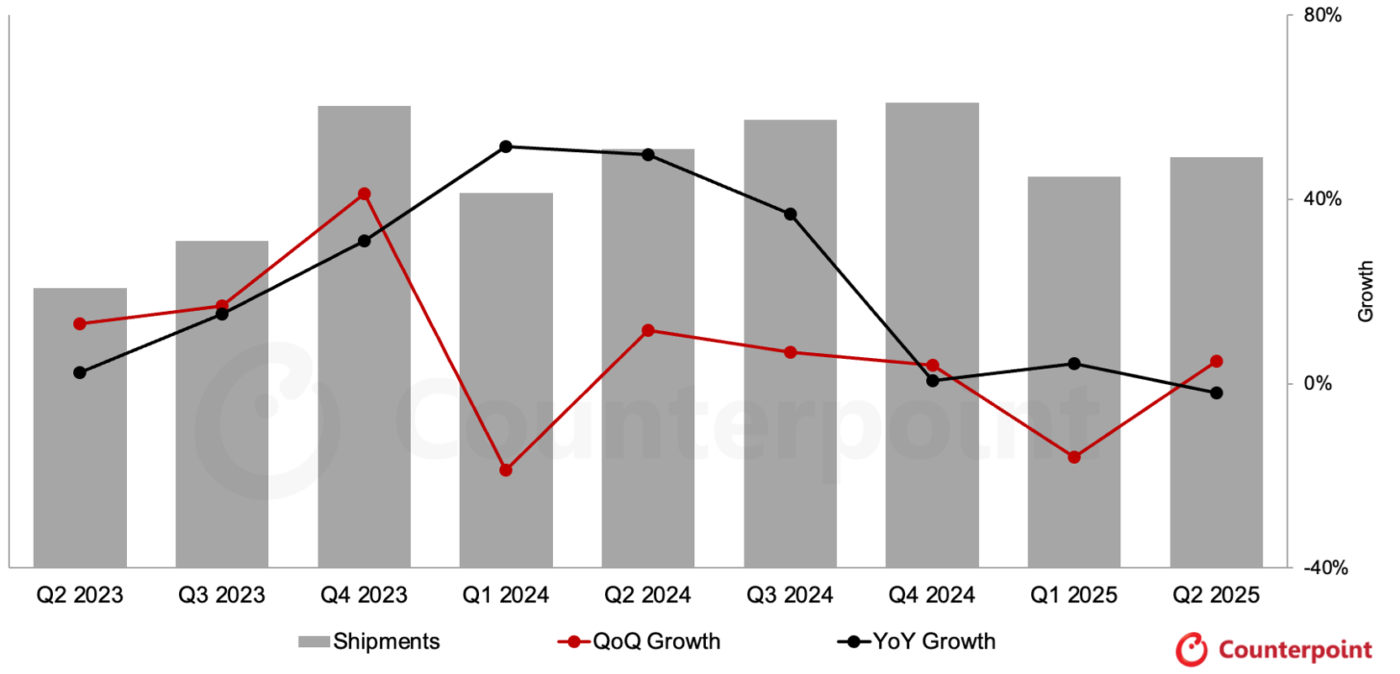

OLED出荷数、Q2'25は前年比2%減~モニターとノートPCが好調

Counterpoint Researchが発刊した最新の Quarterly OLED Shipment Report 速報版によると、Q2’25のOLED出荷数は前期比5%増となった一方、前年比では2%減となった。Q1'25は前期比16%減、前年比4%増だった。

用途別動向

- スマートフォン:前期比2%増、前年比2%減

- TV:前期比31%増、前年比1%減 (季節要因で持ち直したが前年比では依然低迷)

- モニター:前期比44%増、前年比66%増 (ゲーミングや生産性モデルの採用拡大)

- ノートPC:前期比110%増、前年比95%増 (最も成長率が高いセグメント)

モニターとノートPCが好調だったことは明らかで、プレミアムIT需要とOEM採用の拡大に支えられ、いずれも前年比二桁成長を記録した。米国による中国からのノートPC、モニター、部材に対する輸入関税 (2025年の大規模な関税措置の一環) が、エントリーレベルのLCDデバイスのコスト上昇を招いた。これに対しOEM各社は、OLED搭載のノートPCやモニターなど、プレミアム価格帯モデルを強化することで対応した。これらの製品は平均販売価格が高く、関税によるコスト上昇を吸収しやすいためである。この動きが、関税の影響を受ける市場で、PCおよびモニターのOLEDシフトを加速させる結果となった。

OLED出荷数および前年比成長率の推移

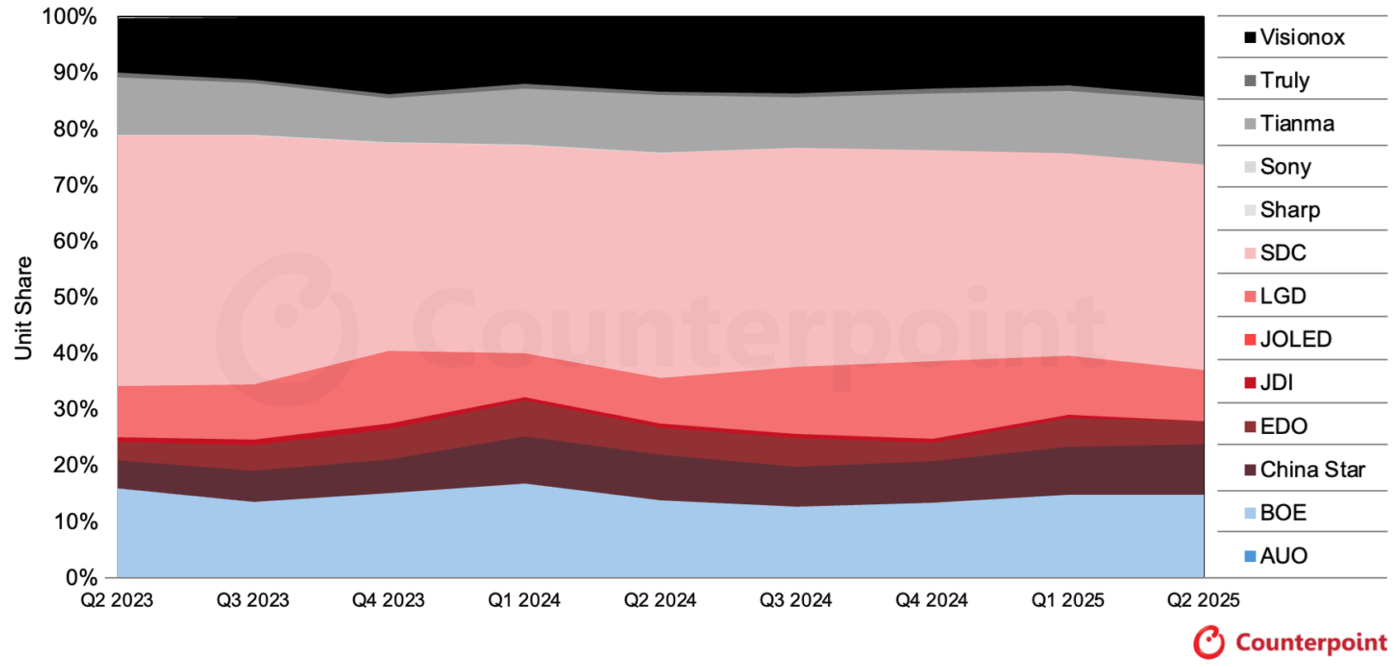

FPDメーカー別動向

Samsung Display (SDC)

- シェアは37%へ上昇 (Q1'25の36%から)

- モニター、ノートPC、スマートウォッチが成長をけん引した。

- ノートPCは前期比131%増、前年比121%増と急成長、ASUS、Dell、Lenovoが主導した

- モニターは前期比47%増、前年比90%増で、27インチQD-OLEDモデルの旺盛な需要が貢献した

LG Display (LGD)

- シェアは9%へ低下 (11%から)

- スマートフォンは前期比20%減、前年比9%増

- スマートウォッチは前期比8%増、前年比41%増

- モニターは前期比35%増、前年比18%増

- TVは前期比30%増、前年比1%減

BOE

- シェアは15%で安定

- ノートPCは前期比12%増、前年比213%増 (最大の成長要因)

- スマートフォンは前期比6%増、前年比18%増

China Star (CSOT)

- シェアは9%へ上昇 (8%から)

- 総出荷数は前期比12%増、前年比9%増

- スマートフォン用は前期比8%増、前年比6%増で、HuaweiとOPPOの需要に支えられた

Visionox

- シェアは14%へ上昇 (12%から)

- 出荷数は前期比21%増、前年比4%増で、タブレットとノートPCの力強い勢いが寄与した

- タブレットとノートPCが三桁成長を記録したことで、Visionoxの出荷数シェアは Q1'25年の12%から14%へ拡大した

メーカー別OLED出荷数シェアの推移

重要ポイント

Q2'25は前年比で小幅な減少となったものの、OLED需要の重心が変化しつつあることが浮き彫りとなった。

- スマートフォンとTVは安定化の兆しを見せているが、昨年と比べると依然軟調である。

- IT用途 (モニターおよびノートPC) がプレミアム製品の採用拡大と供給メーカーの多様化により、顕著な成長を遂げた。

- 供給メーカーの勢力図も変化しており、SDCが首位の座を固める一方、BOEとVisionoxがシェアを伸ばし、LGDは一部カテゴリーでの強みを維持しながらも依然として厳しい状況にある。

- Q2'25はIT用途 (モニターおよびノートPC) がOLEDの新たな成長エンジンとなりつつあることが確かなものとなった。供給体制の整備、OEMによる採用拡大、プレミアムディスプレイへの消費者需要が重なり合い、さらに関税がOLEDシフトを促進する追加要因として作用した。

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] OLED Panel Shipments Declined 2% YoY in Q2 2025; Monitors and Notebooks Bright Spots

Global OLED panel shipments grew 5% QoQ but declined 2% YoY in Q2 2025, following a 16% QoQ decline and 4% YoY growth in Q1 2025, according to Counterpoint Research’s latest Quarterly OLED Shipment Report.

Application trends

- Smartphones: +2% QoQ, –2% YoY

- TVs: +31% QoQ, –1% YoY (seasonal lift, still weak YoY)

- Monitors: +44% QoQ, +66% YoY (strong adoption of gaming and productivity models)

- Notebook PCs: +110% QoQ, +95% YoY (fastest-growing segment)

Monitors and notebooks were the clear bright spots, with both categories posting double-digit YoY growth, driven by premium IT demand and stronger OEM adoption. The US tariffs on imported notebook PCs, monitors and components from China (part of the broader 2025 tariff wave) raised costs for entry-level LCD-based devices. OEMs responded by pushing more premium models, including OLED-equipped notebooks and monitors, where higher ASPs could better absorb tariff-driven cost pressures. This helped accelerate the mix shift toward OLED in PCs and monitors sold into tariff-affected markets.

Panel supplier highlights

Samsung Display (SDC)

- Share rose to 37% (from 36% in Q1 2025)

- Growth fueled by monitors, notebooks and smartwatches

- Notebook PCs surged 131% QoQ and 121% YoY, led by ASUS, Dell and Lenovo.

- Monitors up 47% QoQ and 90% YoY, with strong demand for 27” QD-OLED models.

LG Display (LGD)

- Share slipped to 9% (from 11%)

- Smartphones: –20% QoQ, +9% YoY

- Smartwatches: +8% QoQ, +41% YoY

- Monitors: +35% QoQ, +18% YoY

- TVs: +30% QoQ, –1% YoY

BOE

- Stable at 15% share

- Notebook PCs: +12% QoQ, +213% YoY (biggest upside driver)

- Smartphones: +6% QoQ, +18% YoY

China Star (CSOT)

- Share increased to 9% (from 8%)

- Overall shipments: +12% QoQ, +9% YoY

- Smartphone panels: +8% QoQ, +6% YoY, supported by Huawei and OPPO

Visionox

- Share climbed to 14% (from 12%)

- Shipments grew 21% QoQ and 4% YoY, with strong momentum from tablets and notebooks.

- Visionox’s unit share increased to 14% from 12% in Q1 2025, with 21% QoQ and 4% YoY growth driven by triple-digit growth from tablets and notebook PCs.

Key takeaways

Despite a modest YoY decline, Q2 2025 highlighted the shifting center of gravity in OLED panel demand:

- Smartphones and TVs are stabilizing but still soft compared to last year.

- IT panels (monitors and notebooks) delivered breakout growth, driven by premium adoption and diversified supplier participation.

- Supplier dynamics are evolving, with SDC reinforcing its lead, BOE and Visionox gaining ground, and LGD under pressure despite selective category strength.

- Q2 2025 confirmed that IT applications (monitors and notebooks) are becoming the new growth engine for OLED panels. Supply readiness, broader OEM adoption, and consumer appetite for premium displays have converged, while tariffs have provided an extra catalyst for mix shift toward OLED.