LG Display、広州ライン売却で大幅利益もQ2'25は営業損失を計上

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

LG Display、広州ライン売却で大幅利益もQ2'25は営業損失を計上

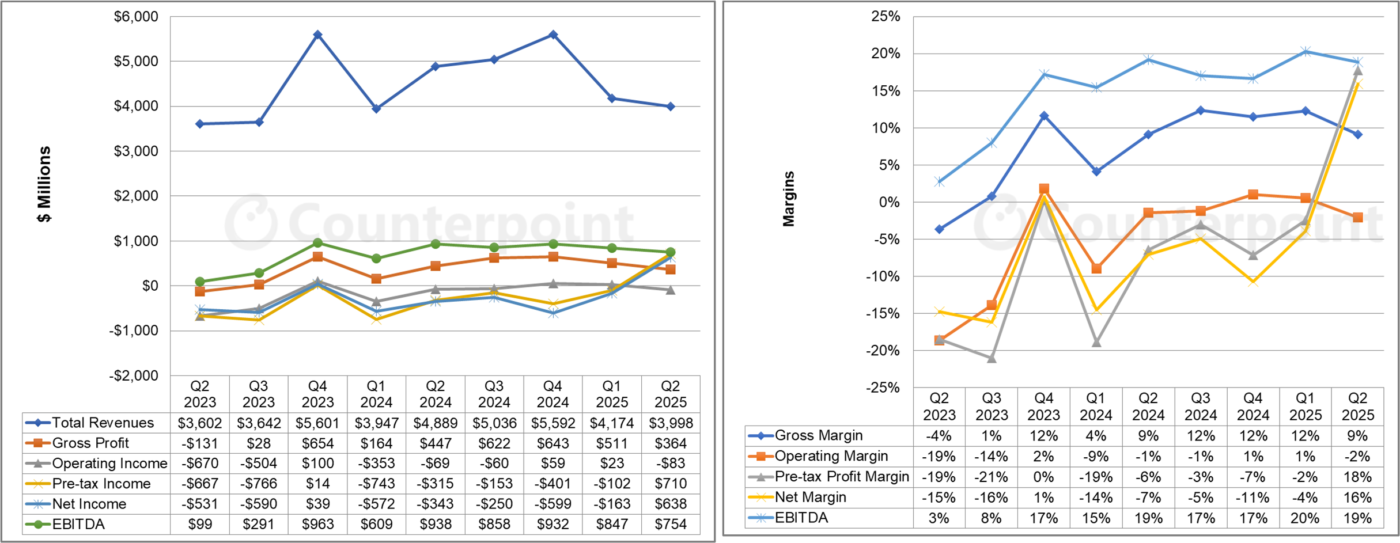

LG Display (LGD) はQ2'25、広州の第8.5世代LCDライン売却で得た特別利益により、過去10年以上で最大の四半期純利益を計上した。この利益によって、全体的には低調だった四半期に一筋の光が差した形となったが、営業利益の連続黒字記録は2四半期で途切れた。LGDは直近13四半期のうち11四半期で純損失を計上している。

LGD(LG Display)は、売上高5兆6000億ウォン(40億ドル)に対し8910億ウォン(6億3800万ドル)の純利益を計上したと報告した。売上高は米ドルベースで前期比4%減、前年比では18%減となった。韓国ウォンは対米ドルで前期比4%上昇、前年比では2%安上昇している。

同社は1160億ウォン (8300万ドル) の営業損失を計上した。Q2’25の営業損失の比較対象となる前期 (Q1’25) は330億ウォンの営業利益、前年同期 (Q2’24) は940億ウォンの営業損失を報告している。LGDの税引前利益は9920億ウォン (7億1000万ドル) で、営業外収益は合計で1兆1000億ウォンに達した。前期の金利費用 (支払利息) が2000億ウォンだったことを踏まえると、為替差益および (主として) China Starへの第8.5世代LCD生産ライン売却により、約1兆3000億ウォンの特別利益を計上したと見られる。

売上高は市場予想とおおむね一致したが、純利益は市場が予想していた1730億ウォンの赤字を大きく上回る好結果となった。一方、営業利益は920億ウォンの営業損失という市場予想を下回った。EBITDA (利払い・税金・償却前利益) は1054億ウォン (7億5400万ドル) で、こちらも市場予想の1121億ウォンを下回った。

営業利益率および売上総利益率は前期比でそれぞれ3ポイント低下し、-2%および9%となった。売上総利益率は前年比では横ばいだったが、営業利益率は1ポイント悪化した。一方、純利益率は前期比で20ポイント改善したものの、EBITDAマージンは1ポイント低下した。

LG Display四半期損益計算書の主要項目

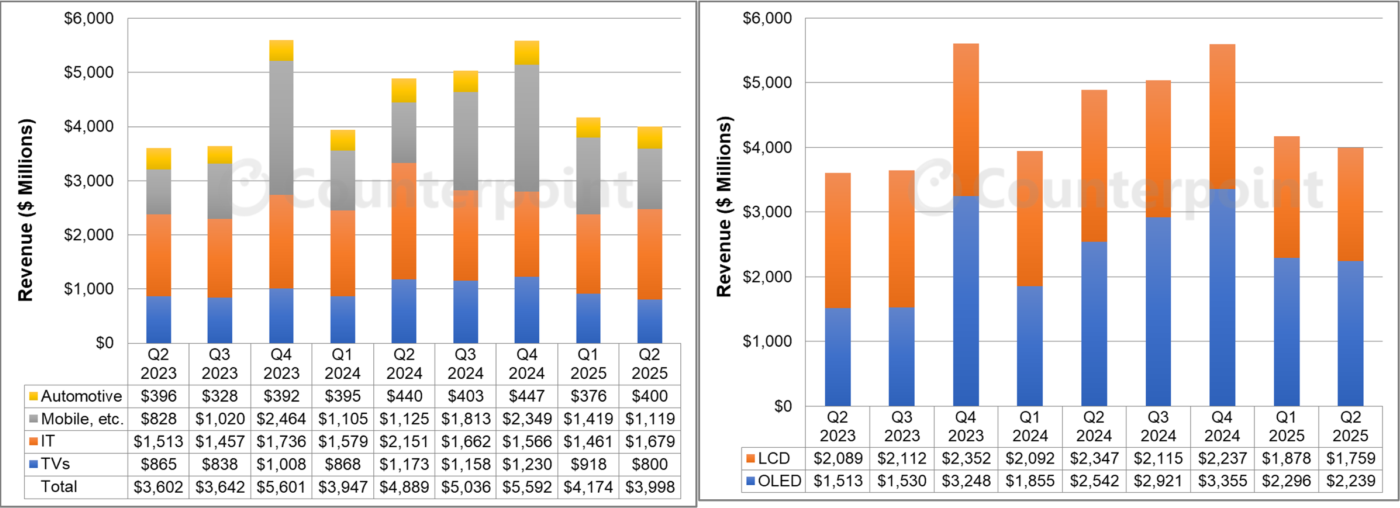

季節的な需要減速の影響により、Q2'25はTVおよびモバイル向けパネル売上が前期比で減少した一方、ITおよび車載向けパネルの売上は増加した。

- 車載用途向けのQ2'25売上は前期比6%増だが前年比ではドルベースで9%減、全体売上に対するシェアは10%だった。

- 「モバイル等」カテゴリーの売上は前期比21%減、前年比では横ばいで、全体売上に対するシェアは28%だった。

- TV向けの売上は前期比13%減、前年比32%減で、全体売上に対するシェアは20%だった。

- IT向けの売上は前期比15%増だが前年比ではドルベースで22%減となった。ただし、全体売上に対するシェアは42%に上昇した。

Q2'25のOLED売上は、前期比で2%、前年比で12%減少 (ドルベース) した。全体売上に対するOLEDのシェア55%から56%へと微増した。一方、LCD売上は前期比で6%、前年比で25%減少した。

また、LGDの面積ベースの出荷は、広州ラインの売却の影響もあり、前期比26%減、前年比38%減の400万㎡となった。一方で、単位面積あたりの販売価格は前期比で31%、前年比で36%上昇し、1㎡あたり1056ドルとなった。

LG Displayの四半期別売上高 (左:用途別、右:ディスプレイ技術別)

バランスシートに目を向けると、Q2'25のLGDの在庫価値はウォンベースで前期比3%減、在庫日数は横ばいの51日となった。現金および現金同等物は前期比で70%増加したが、前年比では29%減少した。

有利子負債は1兆1000億ウォン (4億3000万ドル) 減少し、ドルベースで前期比4%の減少となった。自己資本はウォンベースで3%減少した一方、ドルベースでは1%増加した。負債資本比率は186%から177%へ、ネット負債資本比率も174%から155%へと低下した。2025年7月24日時点におけるLGDの株式時価総額は33億4000万ドルで、株価純資産倍率は0.61と、4月時点の0.55から改善している。一方、負債/時価総額比率は288%、ネット負債/時価総額比率は226%となっている。

LGDの営業キャッシュフローはマイナス4800億ウォン (3億4300万ドル) 、フリーキャッシュフローはマイナス1800億ウォン (1億2900万ドル) となった。一方、投資活動によるキャッシュフローは3000億ウォンのプラスとなり、これは広州ラインの売却益から設備投資を差し引いた額を含むと見られる。

決算説明会では、投資計画に関する質問に対し、LGDは機密性を理由に詳細は伏せたものの、OLED技術の先進化に向けた投資を進める見通しを明らかにした。

Q3'25の見通しについて、LGDは中大型パネルの製品構成の変化および利益率の低い中型パネル製品の比率低下により、出荷面積が1桁台前半から半ばの減少になると予想している。同じ理由から、平均販売単価は20%台半ばの上昇を見込んでいる。2025年の設備投資額は2兆ウォン台前半になる見通しで、TV用OLEDの出荷数は600万台半ばを見込んでいる。

LGDは広州ラインの売却による大きな収益によって負債をやや削減し、徹底したコスト削減によって事業の安定化を図っており、営業ベースではほぼ損益分岐点に近づくまで回復している。しかし、同社が抱える巨額の負債残高は依然として大きな金利負担をもたらしており、単に損益分岐点を維持するだけでは不十分だ。LGDは今後も事業拡大に向けた資金調達に課題を抱える状況が続くとみられる。

[原文] LGD Books Big Profit on Guangzhou Sale but Posts Operating Loss in a Slow Q2 2025

LG Display booked its largest quarterly net profit in more than 10 years in Q2 2025 based on an extraordinary gain from its sale of the Gen 8.5 LCD fab in Guangzhou. The profit gave a shine to an otherwise bleak quarter, as the company’s streak of quarterly operating profits ended at two. LGD has now reported net losses in 11 of the last 13 quarters.

LGD reported a net profit of KRW 891 billion ($638 million) on revenues of KRW 5.6 trillion ($4.0 billion). Revenues were down 4% QoQ and 18% YoY in US dollar terms. The Korean won appreciated 4% QoQ but depreciated 2% YoY against the US dollar.

The company reported an operating loss of KRW 116 billion ($83 million). The Q2 2025 operating loss compared to an operating profit of KRW 33 billion in Q1 2025 and an operating loss of KRW 94 billion in Q2 2024. LGD's pre-tax profit was KRW 992 billion ($710 million), so net non-operating gains totaled KRW 1.1 trillion. Since LGD’s interest expense was KRW 200 billion in the prior quarter, we estimate LGD had extraordinary gains of KRW 1.3 trillion from gains on currency exchange and (primarily) on the sale of the Gen 8.5 LCD fab to China Star.

Revenues were in line with the consensus estimate and net income was far better than the consensus expectation of a loss of KRW 173 billion. The operating profit was worse than the consensus estimate of an operating loss of KRW 92 billion. The EBITDA profit of KRW 1,054 billion ($754 million) was worse than the consensus EBITDA profit of KRW 1,121 billion.

Operating margin and gross margin declined QoQ by 3% to -2% and 9%, respectively. Gross margin was flat on a YoY basis, while operating margin was 1% worse YoY. Net margin improved by 20% QoQ, but EBITDA margin worsened by 1%.

With a seasonal slowdown, revenues decreased QoQ for TVs and mobile phones but increased for IT panels and automotive:

- Q2 2025 revenues from automotive applications increased 6% QoQ but decreased 9% YoY in dollar terms and represented 10% of all revenues.

- Revenues from the "mobile, etc." category decreased by 21% QoQ but were flat YoY and represented 28% of total revenues.

- Revenues from TV decreased 13% QoQ and 32% YoY and represented 20% of total revenues.

- Revenues from IT increased 15% QoQ but decreased 22% YoY in dollar terms and increased to 42% of total revenues.

OLED panel revenues decreased 2% QoQ and 12% YoY in dollar terms in Q2 2025. OLED represented 56% of LGD revenues in Q2 2025, up from 55% in Q1 2025. LCD panel revenues decreased 6% QoQ and 25% YoY.

LGD area shipments decreased 26% QoQ and 38% YoY to 4.0 million square meters, with the Guangzhou fab sold. Area price increased 31% QoQ and 36% YoY to $1,056.

Turning to the balance sheet, in Q2 2025, LGD inventory value decreased by 3% QoQ in KRW terms, and inventory days were flat at 51. LGD’s cash and cash equivalents were up 70% QoQ but down 29% YoY.

LGD debt decreased by KRW 1.1 trillion ($430 million) and decreased 4% QoQ in dollar terms. LGD equity decreased by 3% QoQ in KRW terms but increased by 1% QoQ in dollar terms. LGD’s debt/equity decreased from 186% to 177% and net debt/equity decreased from 174% to 155%. As of July 24, LGD’s market value of equity is $3.34 billion, for a price-to-book ratio of 0.61 (improved from 0.55 in April). LGD's debt-to-market equity is 288% and its net debt-to-market equity is 226%.

LGD reported negative cash flow from operations of KRW 480 billion ($343 million) and negative free cash flow of KRW 180 billion ($129 million). LGD reported cash flow from investment activities of KRW 300 billion. This includes the proceeds from the Guangzhou sale minus capex.

In the earnings call, LGD cited confidentiality when asked about investment plans, but said that it expected investment to advance OLED technologies.

On the Q3 2025 guidance, LGD expects area shipments to decline by a low-to-mid-single-digit % due to product mix changes in mid-to-large panel products and a reduced share of low-margin medium panel products. The company expects ASPs to increase by mid-20s% for the same reason. LGD expects the 2025 capex to be in the low-KRW-2-trillion range, and OLED TV panel shipments to reach the mid-6-million range.

With the big gain from the Guangzhou sale, LGD has made a modest reduction in its debt load, and with relentless cost-cutting, LGD has managed to stabilize its business and come close to breaking even on an operating basis. But the company’s massive debt load incurs substantial interest expenses, so breaking even is not enough. LGD will continue to be challenged to raise funds for any expansion.