フォルダブル型スマートフォン市場動向~その他APAC地域における成長:中国OEMが攻勢を強める [スマートフォン調査部門]

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

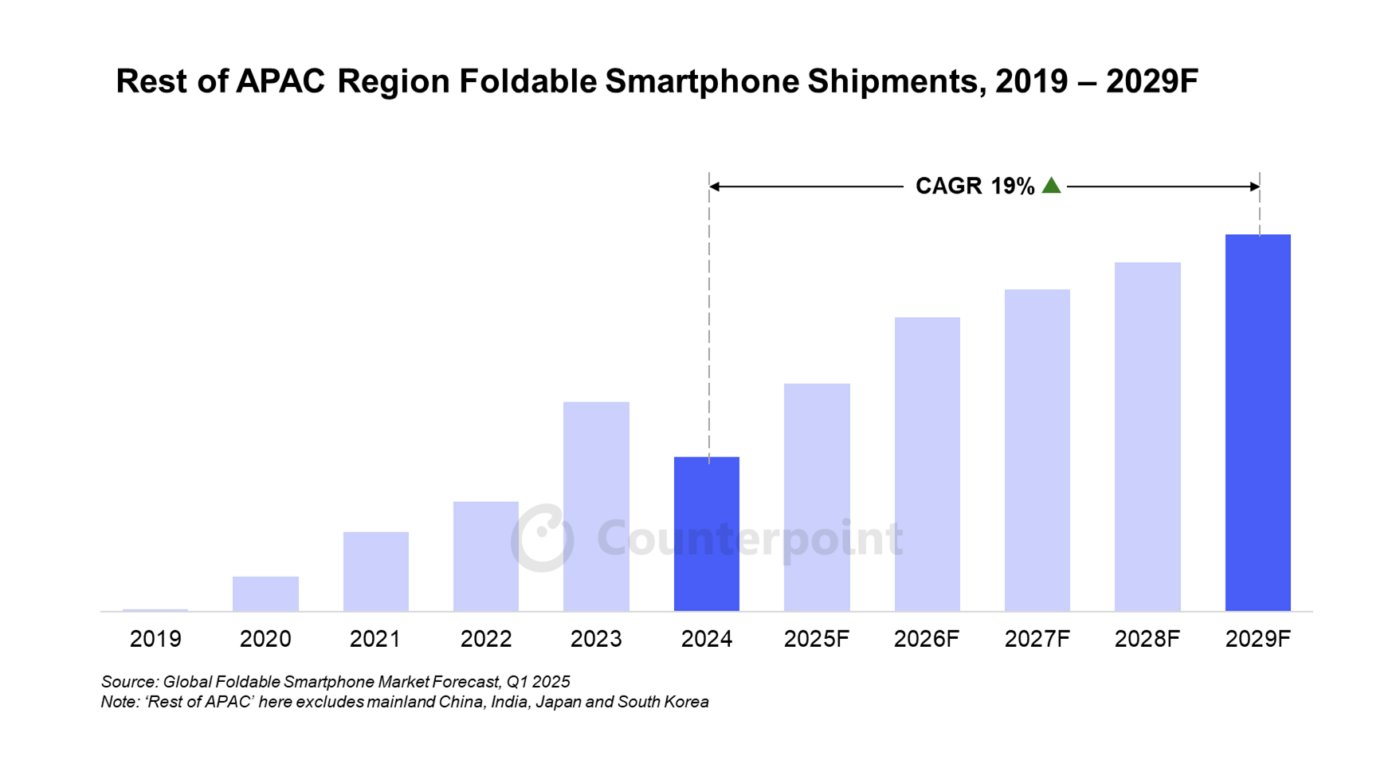

- アジア太平洋地域のうち、中国本土、インド、日本、韓国を除いたその他の国および地域 (以下、その他APAC地域)におけるフォルダブル型スマートフォン出荷数は、2019年から2024年にかけて年平均成長率 (CAGR) 95%で成長し、2029年までCAGR 19%を維持すると予測されている。

- 中国OEMは東南アジアおよびその他APAC地域全体のハイエンドセグメントに積極的に進出しており、アクセスしやすさと最先端デザインを両立させたフォルダブル型プレミアムモデルを提供している。

- 携帯端末のユーザー体験、バッテリー技術、ハードウェアの信頼性における継続的な革新が、フォルダブル型スマートフォンに対する消費者の不安を軽減してきた。フォルダブル型スマートフォンは、特に東南アジアでは日常使用の主要デバイスとして徐々に定着しつつあり、APAC地域の消費者にとって、もはや代替品や高級オプションではなくなっている。

- Origin Workbenchのようなカスタマイズされたソフトウェア・エコシステムやAI駆動型機能が、フォルダブル型スマートフォンを多機能な生産性ツールへと変貌させつつあり、地域ごとの嗜好や利用習慣に適応することで、ユーザーロイヤリティを高めている。

アジア太平洋地域のうち、中国本土、インド、日本、韓国を除いたその他の国および地域 (Rest of APAC) におけるフォルダブル型スマートフォンの出荷数は急速に増加しており、2019年から2024年にかけのて年平均成長率 (CAGR) は95%に達した。Counterpoint Researchが発刊した Global Foldable Smartphone Market Forecast 最新版によると、この勢いは今後も続く見通しで、2024年から2029年にかけてのCAGRは19%と予測されている。消費者は、ブランドや市場による継続的な啓発の影響を受け、価格は必ずしも高いわけではないが品質は高いプレミアム体験を求める傾向が強まり、フォルダブル型を徐々に受け入れつつある。同時に、中国OEM各社は製品の多様化を図るべく、積極的にAPAC市場への展開を進めている。

その他APAC地域のフォルダブル型スマートフォン出荷数推移

フォルダブル型は従来のバータイプ端末とは操作性が異なるため、使いこなすまでにある程度の慣れを要する。また、ハイエンドカテゴリーを代表する製品であることから、ブランドイメージ、最上級のハードウェア、信頼できる品質、そして日常生活が確実にアップグレードする実感など、消費者から期待されるものが数多くある。こうした意識こそが、OEM各社に対し製品開発の限界に挑ませる原動力となっている。世界最大のフォルダブル型スマートフォン市場である中国では、こうした背景から、各ブランドが目の肥えたハイエンドユーザーへの配慮を一層強めるようになった。Huawei、OPPO、vivo、Xiaomiといったブランドは、新機種発表のたびにターゲットユーザーのおもな不満点に対応するよう綿密に設計を行っている。さらに、vivoのようなOEMはブック型フォルダブル機種を、プレミアムな品質や製品トーンを損なうことなく、より多くのユーザーに行き渡らせようと積極的な取り組みを見せている。このように、フォルダブル型のフラッグシップ製品は、もはや「目新しいガジェット」ではなく、同地域のより幅広い層にとっての「定番デバイス」へと進化しつつある。

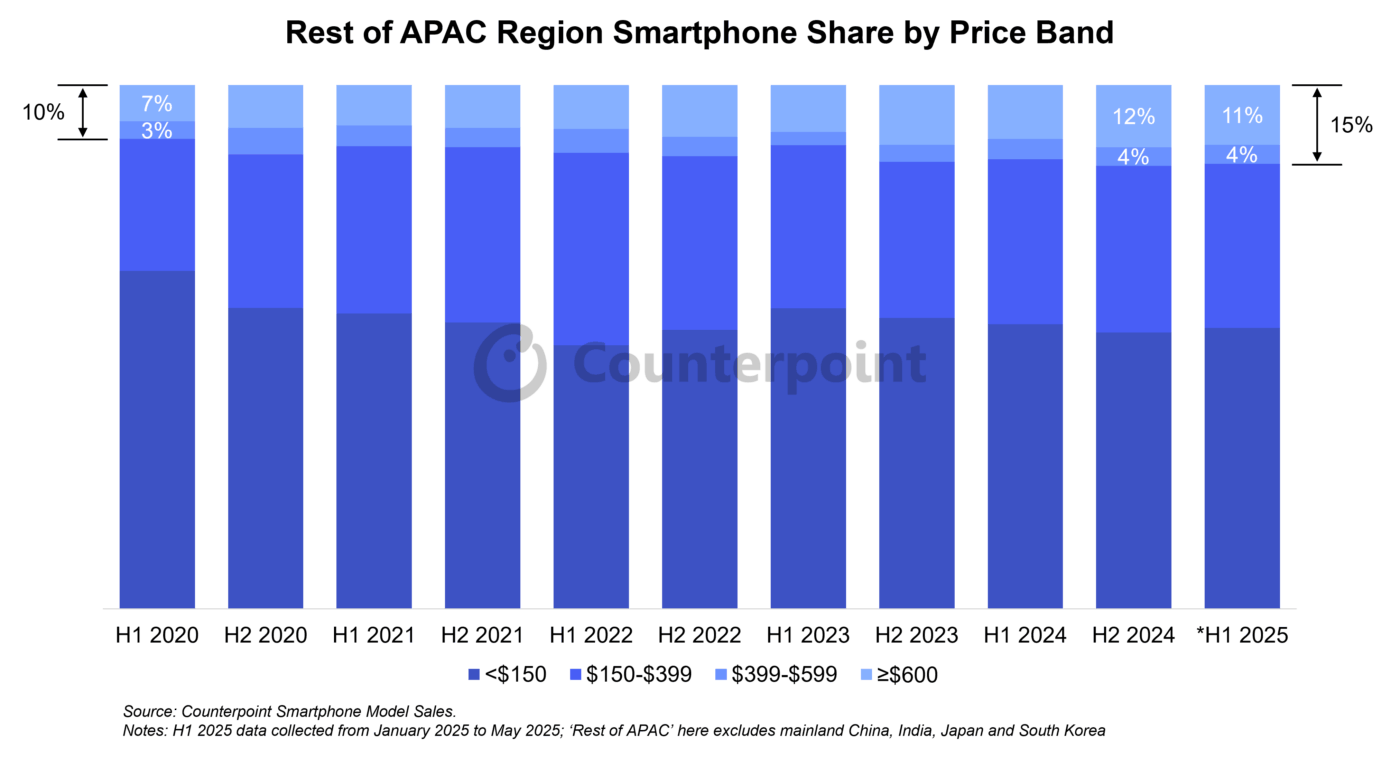

さらに注目すべき点として、2025年上半期時点で、その他APAC地域市場で600ドル超の端末が占めるシェアは11%で安定しており、399-599ドルの中価格帯上位層は4%となっている。言い換えれば、その他APAC地域の経済が安定し徐々にプレミアムセグメントへと移行しつつあるなかで、現時点および潜在的な600ドル超製品購買層を合わせた市場シェアは、今後数年で15%を超える見通しとなる。ハイエンド市場においては、Appleが60%以上のシェアで他を圧倒しており、Samsungは約20%と大きく引き離されている。その一方、フォルダブル型は将来的に有望な成長領域の一つと位置づけられており、Appleも2026年に初のフォルダブル端末を投入する計画があると報じられている。プレミアム市場の競争活性化と新規参入増加が健全な競争環境をもたらすことは明らかで、消費者にとっても選択肢の幅が広がることになる。

その他APAC地域の価格帯別フォルダブル型スマートフォン市場シェア

初期世代のフォルダブル型端末はかさばって重く、長時間持ち続けるには不快さをともなうことも多かった。しかし2025年現在、フォルダブル型は新たな段階に進化している。端末重量は220g未満 (iPhone 16 Pro Maxの標準重量は227g) になり、折りたたみ時の厚さも9mm台、さらには8mm台にまで薄型化が進んでいる。これにより、片手での操作も現実的な使用体験となった。つまり、フォルダブル型端末はすでに従来のハイエンドなバータイプ端末と同等のサイズ感・重量帯に到達しているわけだ。こうした進化は、特に東南アジア市場にとって重要な意味を持つ。より薄型で軽量なフォームファクターは、同地域のユーザーの好みや利用習慣と強く一致しているからである。

現在の消費者はフォルダブル型端末に対しても、SoC、RAM、バッテリーといった内部コンポーネントからディスプレイやカメラなどの外部部品に至るまで、バータイプのフラッグシップ機と同等のハードウェア性能を求めている。これに対し、中国OEM各社は果敢かつ積極的な取り組み姿勢を見せている。たとえば、新たに発表されたvivo X Fold5は、フラッグシップ機並みの仕様を備えている。さらに特筆すべきは、6000mAh相当のBlueVoltバッテリーを搭載している点である。この進歩は、バッテリーのエネルギー密度向上という技術的ブレイクスルーによって実現したものであり、OEMとサプライヤーの緊密な研究開発連携の成果といえる。これらのモデルは、本体を展開した状態でわずか4mm台という超薄型設計を実現しながらも、フォルダブル型端末としてワイヤレス充電にも対応している。これは、いまだ一部のグローバルブランドが追いついていない領域でもある。こうした進化は、バッテリー切れへの不安を解消するうえで大きな意義を持つ。特に、安定した電力インフラの整備が地域によっては依然として課題である東南アジアにおいては、切実なニーズと重なる部分が多い。今では多くのヘビーユーザーが、一回の充電でまる1日以上使用できることを当然のように期待している。

東南アジアは気温や湿度が高く、インフラ整備の遅れにともなう粉塵や大気汚染といった、独自の環境的課題を抱えている。これらの要因により、端末の耐久性や信頼性に対する需要は一層高まっている。フォルダブル型端末は、構造が複雑でヒンジや可動部品が多いことから、消費者の間には「壊れやすい」という印象が依然として存在する。実際、初期モデルではヒンジの摩耗や画面の耐久性、落下時の耐衝撃性などで課題を抱えていた。これに対し、中国ブランド各社はサプライチェーン全体への投資を通じて、こうした懸念への対応を体系的に進めてきた。協調的エンジニアリングによる技術革新によって、防水性、防塵性、落下耐性、画面の耐傷性などの性能が高い水準に到達している。一例を挙げると、vivoは最新モデルのX Fold5向けに、60万回の折りたたみに耐える業界最先端の軽量かつ高耐久なキネマティック・ヒンジを開発している。同モデルはまたフォルダブル型としては初の、IPX8 + IPX9の防水性能とIP5Xの防塵性能を兼ね備えた製品でもある。加えて、先進素材の採用により、−20°Cの低温環境でも使用可能な耐寒性能も実現している。

Counterpoint Researchの市場調査によれば、APAC市場全体で、カメラ性能はハイエンドスマートフォンの購入を左右する最も重要な要素の一つとなっている。ユーザーは日常生活から仕事の場面に至るまで、写真や動画をSNS上で頻繁に共有している。そのため、カメラ性能は信頼を得る最速の手段であると同時に、批判を浴びるリスクにもつながる。こうした背景のもと、中国OEM各社はかめら性能の革新に多大なリソースを投入しており、ハイエンド機 (フォルダブル型を含む) の各世代に最先端の撮影機能を実装してきた。vivoの場合、最新のフォルダブル機種にZEISSと共同開発したイメージングシステムを搭載しており、ZEISS T*コーティングによってフレアやゴーストを低減しつつ色再現性とコントラストを向上させることで、いわゆる「ZEISS Look」を実現している。さらに、vivo独自のAI画像処理アルゴリズムと、ZEISSが長年培ってきた光学技術との融合により、出力品質は飛躍的に向上している。Stage ModeやZEISS Multifocal Portraitといったシグネチャー機能により、仕事の場や日常生活、あるいは友人や家族とのひとときでも、ユーザーは大切な瞬間を簡単かつ確実に捉えることができる。

ハードウェアに加えて、ソフトウェアもユーザーのロイヤリティを確保するうえで非常に重要な役割を担っている。注目すべきは、vivoのような一部の中国ブランドが長期主義思想を掲げつつ、「More Local, More Global (より地域に密着、より世界へ展開)」というローカライゼーション戦略を採用している点である。これらのブランドのなかには、すでに東南アジア域内に研究開発チームを設置し、現地ユーザーに最適化された体験の提供に向け、消費者調査に重点的に取り組んでいる企業もある。こうしたチームはエコシステムパートナーと緊密に連携しながら、現地ユーザーの好みに合わせたソフトウェア体験の最適化を進めている。人気のアプリや使用パターンの進化にともなってオペレーティングシステムも進化を続けており、ユーザーの不満点をさりげなく、直感的な方法で解消するよう工夫されている。たとえばvivoは、X Fold5に生産性を重視した包括的ツールスイートを搭載し、一歩先を行く展開を見せている。このスイートには、Origin Workbench、vivo DocMaster、Smart Call Assistant、AI Transcript Assistといった機能が含まれており、プロフェッショナルやクリエイターを念頭に設計されたこれらの機能群は、マルチタスクやさまざまなシーンにおける使い勝手を大きく向上させている。

APAC地域は、中国ブランドにとってもその他のブランドにとっても、注力する重点市場である状況に変わりはない。同地域は地理的にも文化的にも中国OEMにとっての本拠地市場に近く、当然ながら競争の主戦場となっている。展開すると大画面になるブック型デザインに代表されるように、フォルダブル型端末が生産性志向を強めるにつれ、デジタル生産性やコンテンツ消費が拡大している地域では、その魅力はより強く響くことになると考えられる。こうした背景から、vivoのX Fold5は、フォルダブルカテゴリーをより薄く、より頑丈で、よりスマートに、そしてより長持ちする「オールラウンド型フラッグシップ体験」へと、その形を再構築しようとしている。プロフェッショナル層は今や日常的なフラッグシップ端末としてフォルダブル型を選択している。その他APAC地域においては、購買力の高い市場ほどフォルダブル型端末の導入がより早く進展する可能性が高いと見られている。

------------------------------------

※本記事はvivoとのコラボレーションにより執筆されました。

[原文] Foldable Smartphone Growth in Rest of APAC: Chinese OEMs Bring Their A Game

- Foldable smartphone shipments in the Rest of APAC region (Asia-Pacific excluding mainland China, India, Japan and South Korea) have grown at a 95% CAGR from 2019 to 2024 and are expected to maintain a 19% CAGR through 2029.

- Chinese OEMs are aggressively advancing into the high-end segment of the Southeast Asian and broader Rest of APAC region, delivering premium foldable devices that balance accessibility and cutting-edge design.

- Continuous breakthroughs in handheld user experience, battery technology and hardware reliability have alleviated consumer anxieties about foldable smartphones. Foldables are no longer an alternative, luxury option for APAC consumers, especially in Southeast Asia, where they are gradually becoming the primary device for daily use.

- Tailored software ecosystems, such as Origin Workbench, and AI-driven features are transforming foldable phones into versatile productivity tools, fostering user loyalty by adapting to local preferences and usage habits.

Foldable smartphone shipments have been growing rapidly in the Rest of APAC region (Asia-Pacific excluding mainland China, India, Japan and South Korea), with a compound annual growth rate (CAGR) of 95% from 2019 to 2024. This momentum is expected to continue with an estimated 19% CAGR from 2024 to 2029, according to Counterpoint Research’s latest Global Foldable Smartphone Market Forecast. Consumers, influenced by continuous brand and market education, are gradually embracing foldables as they increasingly seek premium experiences — high in quality, though not necessarily in price. At the same time, Chinese OEMs are actively expanding into the APAC market to diversify product offerings.

Foldables come with a usage learning curve, as they operate differently from traditional bar-type phones. Further, as a representative of the high-end category, foldables come with a long checklist of consumer expectations – brand image, top-tier hardware, dependable quality, and a noticeable upgrade to daily life. This mindset is precisely what drives OEMs to push the boundaries of product development. As the world’s largest foldable smartphone market, China has pushed its brands to be even more attentive to discerning high-end users. Brands like Huawei, OPPO, vivo and Xiaomi consistently tailor each new release to address the key pain points of their target audience. Moreover, OEMs like vivo are keen to democratize book-type foldables without compromising on premium quality and product tonality. Thus, foldable flagship products are no longer just a “novelty” – they are becoming the “go-to” devices for a broader range of consumers in the region.

Additionally, it is worth noting that as of the first half of 2025, the Rest of APAC market for devices priced above $600 has held steady at 11% share, while the $399–$599 “upper-midrange” segment sits at 4%. In other words, as the Rest of APAC economies stabilize and gradually shift toward the premium tier, the combined share of current and potential $600+ buyers is set to exceed 15% in the following years. Apple commands over 60% of the high-end market, with Samsung a distant second at about 20%. As for foldables, they represent one of the more promising growth opportunities, with even Apple reportedly planning to launch its first foldable in 2026. Clearly, the market will benefit from more participants in the premium segment, fostering healthy competition and offering consumers a wider range of choices.

Early-generation foldables were bulky and heavy, often uncomfortable to hold for extended periods. In 2025, foldables have entered a new era – devices weighing under 220 gm (standard iPhone 16 Pro Max weighs 227 gm) and the folded thickness dipping to 9.x mm or even 8.x mm. Single-handed use is now a realistic experience. In other words, foldables have reached the dimensions and weight class of regular high-end bar-type phones. These advancements are especially significant for Southeast Asia, where the slimmer, lighter form factors better align with the preferences and usage habits of local users.

Consumers today also expect parity with bar-type flagships when it comes to core hardware – from internal components like SoCs, RAM and batteries to external components like display and cameras. Chinese OEMs have taken a bold and aggressive approach. For instance, the newly launched vivo X Fold5 features flagship-level specifications. More impressively, it manages to pack an equivalent 6000 mAh BlueVolt battery. This leap was made possible by breakthroughs in battery energy density, a result of close R&D collaboration between OEMs and suppliers. Despite having ultra-thin unfolded bodies (as slim as 4.x mm), these models also bring wireless charging to foldables, an area where some global brands still lag behind. These enhancements address battery anxiety, a particularly pressing concern in Southeast Asia where some regions still struggle with stable electricity infrastructure. Heavy users now expect their devices to last well beyond a full day on a single charge.

Southeast Asia poses unique environmental challenges – high temperatures, humidity, pollution, and dusty conditions due to underdeveloped infrastructure. These factors are driving stronger demand for device durability and reliability. Consumers perceive foldables to be more fragile, given their complex hinges and moving parts — and truthfully, early models did struggle with hinge wear, screen durability, and overall drop resistance. Chinese brands have systematically addressed these concerns by investing across the entire supply chain. Collaborative engineering breakthroughs have enabled devices to achieve high standards in waterproofing, dust resistance, drop protection, and screen scratch resistance. For example, vivo has crafted an industry-leading lightweight and durable kinematic hinge that withstands 600,000 folds in its latest X Fold5 model. It also stands out as the first foldable offering IPX8 + IPX9 water resistance and IP5X dust protection. In addition, with the advanced material application, the phone can be used in low temperatures, with resistance till -20°C.

Counterpoint’s market research indicates photography is one of the top purchase considerations for high-end phones across the APAC market. Users constantly share photos and videos, whether during professional events or everyday moments, on their social media accounts. This makes camera performance one of the quickest ways to earn trust – or attract criticism. Chinese OEMs have poured resources into imaging innovations, ensuring every generation of their high-end (including foldable) devices showcases cutting-edge camera technology. In the case of vivo, its latest foldable features a ZEISS co-engineered imaging system with ZEISS T* coating, designed to reduce flare and ghosting while improving color fidelity and contrast to deliver the signature “ZEISS Look”. Powered by vivo’s self-developed AI-enhanced imaging algorithms and ZEISS’ long-standing imaging capabilities, the output quality has significantly improved. Signature features such as Stage Mode and ZEISS Multifocal Portrait allow users to effortlessly capture precious moments, whether at work, in daily life, or enjoying time with friends or family.

In addition to hardware, software plays a crucial role in securing user loyalty. It is worth noting that some Chinese brands, such as vivo, adhere to a philosophy of long-termism and embrace a “More Local, More Global” localization strategy. Some of these brands have already established Southeast Asia-based R&D teams to focus on consumer research and deliver a localized user experience. These teams work closely with ecosystem partners to adapt software experiences to local user preferences. As usage patterns and popular apps evolve, their operating systems also evolve, often quietly solving user pain points in intuitive ways. For instance, vivo has taken a step forward with the X Fold5’s comprehensive productivity suite, which includes Origin Workbench, vivo DocMaster, Smart Call Assistant and AI Transcript Assist. Designed with professionals and creators in mind, it elevates usability across multitasking and multiple scenarios.

The APAC region remains a core focus for both Chinese brands and other brands. The region’s proximity, both geographically and culturally, to the Chinese OEMs’ home market makes it a natural battleground for them. As foldables become more productivity-focused, especially with book-type designs that unfold into larger screens, we expect them to resonate more with users in regions where digital productivity and content consumption are rising. In this context, vivo’s X Fold5 is reshaping the foldable category into an all-rounder flagship experience – thinner, stronger, smarter and long-lasting. Professionals can now choose foldables as their everyday flagship. Within the Rest of APAC region, markets with higher overall spending power will likely see faster growth in foldable adoption.

* This blog is in collaboration with vivo