TV用LCD価格はQ3でピークアウトの見通し

冒頭部和訳

2月に始まったTV用LCD価格の上昇は第3四半期も続いているが、それと同時に、LCDメーカーの稼働率上昇により供給も広範囲にわたって増加している。価格はこれまでに、多くのLCDメーカーで利益率がプラスに転じるのに十分なほど上昇しており、TVサプライチェーンは第4四半期の大商戦に向けて在庫を積み上げている。DSCCは現在、LCD価格は9月にピークに達し、供給が豊富なため、第4四半期には価格が下落すると予測している。

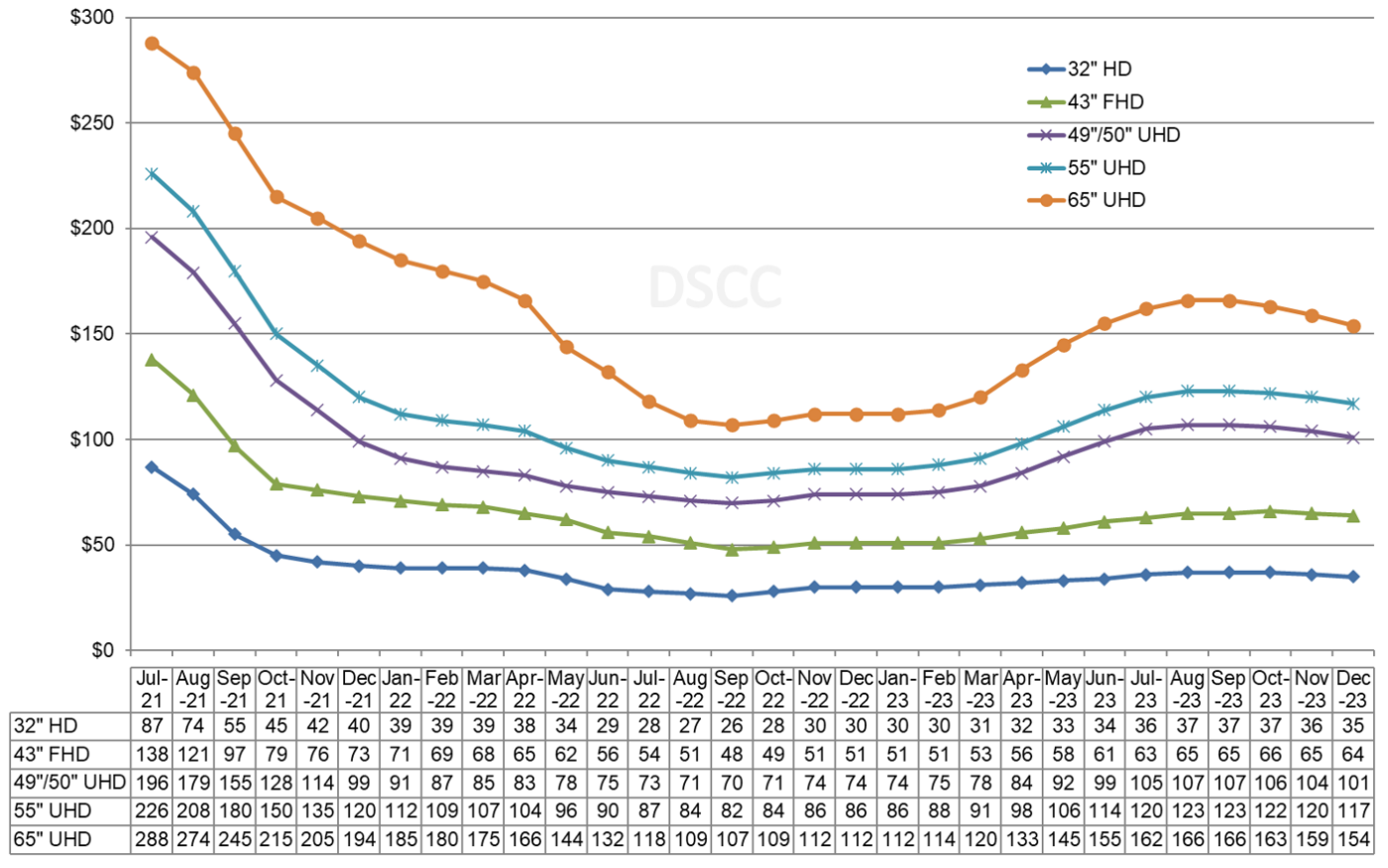

一つ目のグラフは2023年12月までのTV用LCD価格動向の最新予測である。パンデミック後の2021年中盤から2022年夏にかけて価格が急落したことがグラフに表れている。価格は2022年9月に過去最低値を記録し、Q4’22からQ1’23にかけて緩やかに上昇した後、2023年4月に大幅な上昇を示し始めた。7月には実勢価格が当社の予測を上回ったため、7月と8月の価格は先月の予測から上方修正となっている。

※ご参考※ 無料翻訳ツール (DeepL)

The rally in LCD TV panel prices, which started in February has continued in the third quarter and has been accompanied by a widespread increase in supply as LCD makers increase utilization. Prices have increased enough to bring many panel makers into positive margins and the TV supply chain is building inventory toward the big selling season in the fourth quarter. We now expect that panel prices will peak in September and that an abundance of supply will lead to prices declining in the fourth quarter.

The first chart here highlights our latest TV panel price update with a forecast to December 2023, showing the post-pandemic price plunge from mid-2021 to summer 2022. Prices hit their all-time lows in September 2022 and increased modestly in Q4’22 and Q1’23 before larger price increases started in April 2023. Actual prices for July came in higher than our expectation, so July and August prices are revised up, compared to last month.

LCD TV Panel Prices

As the industry started its climb out of the deep hole, average prices increased only 2.9% Q/Q in Q1’23 as the industry continued to deplete excess inventory. Once that excess was gone, prices increased an average of 15.3% in the second quarter and are projected to increase another 11.5% in the third quarter.

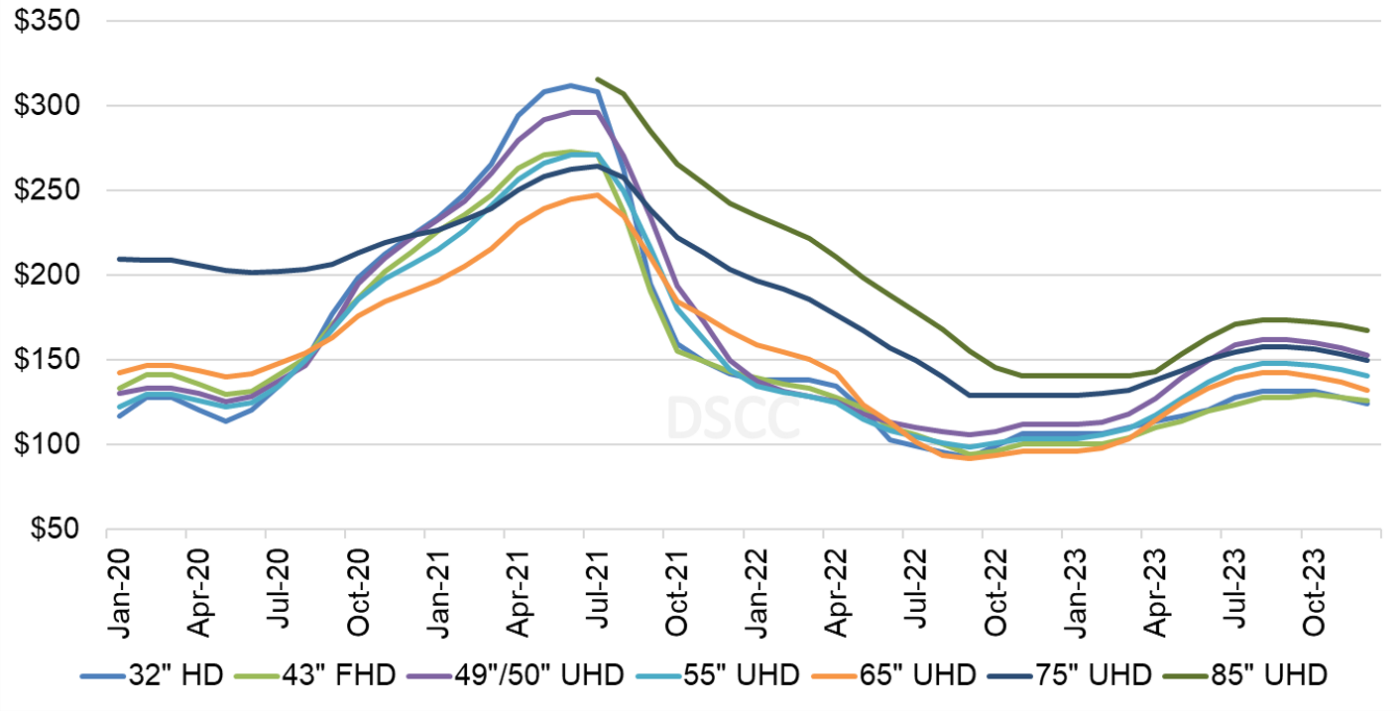

In the second quarter, prices increased for all sizes of TV panels, but 65” panels saw the biggest increases. Prices for those big panels increased 25% in Q2, while smaller size panels like 32” saw only single-digit % increases. In the third quarter price increases are more evenly distributed, with all sizes in the range of 40” to 65” seeing increases between 10% and 16%, while the smallest (32”) and largest (75”) sizes in our survey increasing at single-digit % rates.

As we look at pricing on an area basis, we are seeing some stratification in the range of prices. From August 2022 through March 2023, the price for 65” TV panels was the lowest in area terms, but the increases in recent months have brought the 65” panels into the mainstream. In July 2023, area prices for most panels up to 65” fell in the range from $124 per square meter for 40” panels to $144 per square meter for 55” panels. An exception to that trend is the 49”/50” panel size, which has increased rapidly starting in April. Those panels, which are made efficiently on Gen 8.5 fabs but not on Gen 10.5 fabs, sold for $159 per square meter in July, higher than 75” panels.

Monthly Area Prices per Square Meter for LCD TV Panels

Prices for the largest screen sizes, 85”, remain at a premium to the smaller sizes, although that premium has been reduced compared to a year ago. In July 2022, 85” panels sold for $178 per square meter, an 80% premium over 32”. A year later in July 2023 the 85” panels sold for $171 per square meter, a 34% premium.

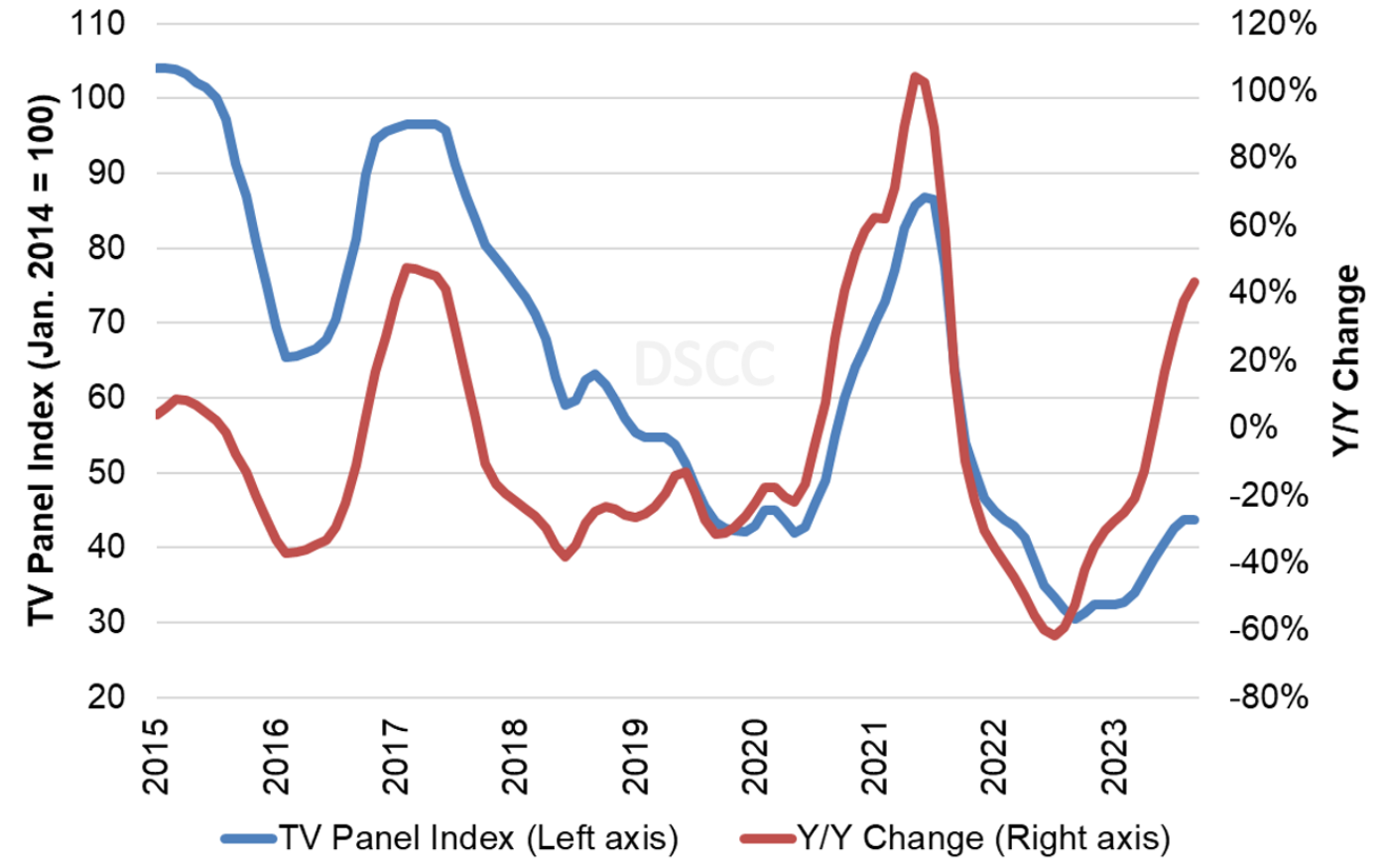

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through December 2023. The price increases in July and August 2023 have brought our index up to 43.7, an increase of 43% compared to the low of 30.5 in September 2022. The price increases in May brought price index into positive territory on a Y/Y basis for the first time since September 2021, and in August 2023 panel prices are 38% higher than a year ago.

LCD TV Panel Price Index

The larger-than-expected price increases in Q2’23 have been welcomed by panel makers, even though they were not enough to bring the industry to profitability, based on the reported results of LGD, AUO and Innolux. The price increases of the third quarter have likely brought the Taiwan panel makers into the black.

However, the industry’s capacity still far outstrips the likely demand for the foreseeable future, and industry utilization in Q3 and as projected in Q4 is creating a supply glut, which we believe will result in prices peaking in September and declining in the fourth quarter.