日本スマートフォン出荷数、Q2'25は前年比11%増~2四半期連続で2桁成長 [スマートフォン調査部門]

Counterpoint Research

スマートフォン (セット) 調査レポート

ラインナップはこちらから

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

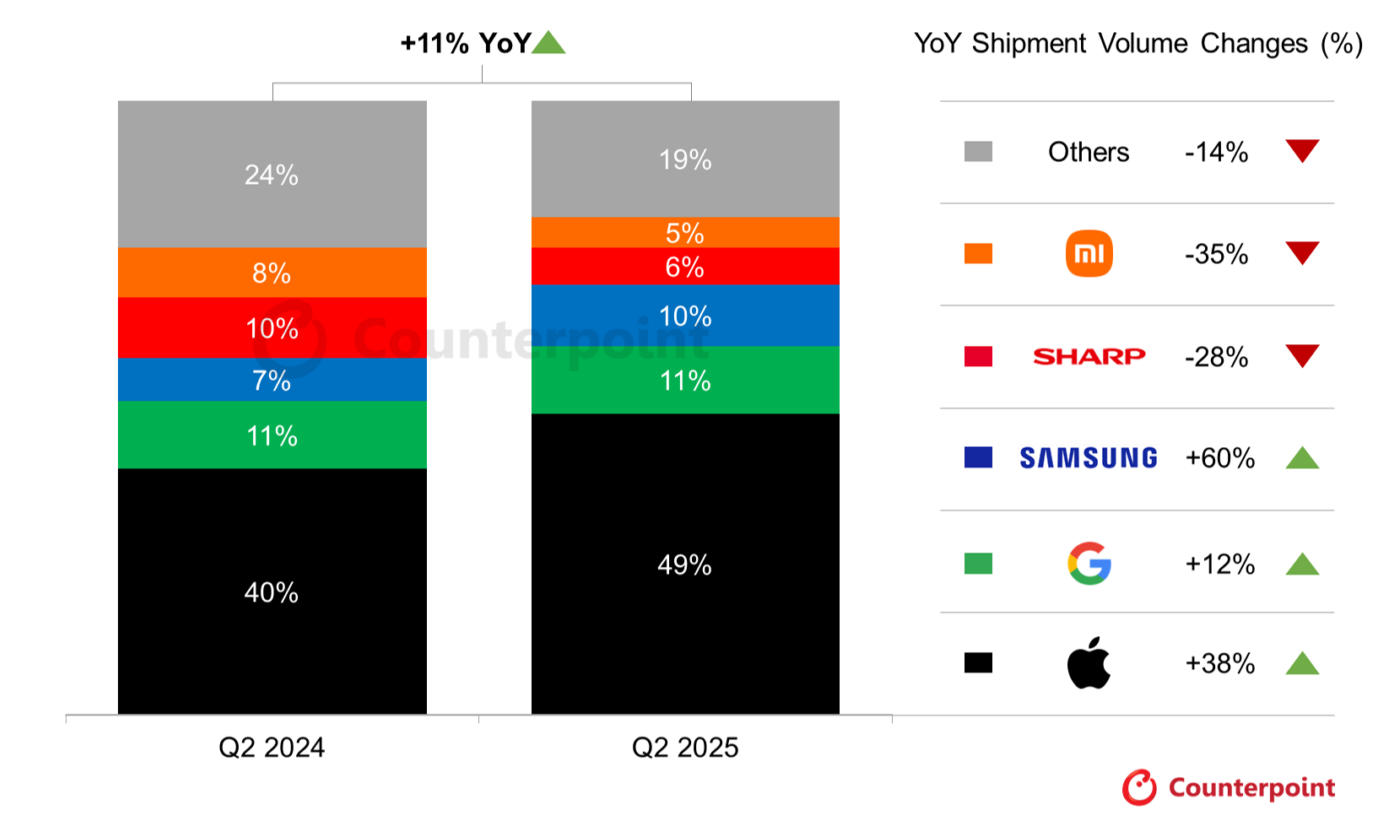

- 日本のスマートフォン出荷数はQ2'25に前年比11%増となり、成熟市場にもかかわらず、2四半期連続で2桁成長を記録した。

- 市場リーダーである Appleの出荷数は前年比38%増となった。iPhone 16eの販売好調がQ1'25から続いたことが要因である。

- Samsungは2025年に販促活動を強化した結果、出荷数が前年比60%増となり、ここ数年で最も高水準の市場実績を達成した。

- 端末下取りプログラムなどの積極的な販促が需要を喚起し、日本市場の成長を支えた。

Q2’25の日本のスマートフォン出荷数は前年比11%増で、市場が成熟しているにもかかわらず2四半期連続で二桁成長を維持した。Counterpoint ResearchのMarket Monitorサービス (Global Smartphone Market Shipment Tracker) が明らかにしている。同四半期の市場の勢いの原動力となったのはAppleで、同社のシェアは大きく拡大した。この結果は日本におけるキャリアの販促活動の激化を反映したもので、いわゆる「1円スマホ」として販売されるケースが多い端末下取りプログラムが買い替え需要を喚起する仕組みの主流となっている状況を示唆している。

日本スマートフォン出荷数 ブランド別シェアおよび前年比成長率

日本のスマートフォン市場で最大シェアを持つAppleは、iPhone 16eの販売が好調でQ1’25からの勢いを維持した。しかし、Appleの当初の勢いは6月以降すでに減速し始めているため、下半期の成長は他モデルや新製品の投入に依存せざるを得ない状況となるだろう。

一方、Androidベンダー各社の業績はばらつきが見られ、一部は堅調な伸びを記録した。Samsungは2025年に販促活動を強化し、第2四半期出荷数は前年比60%増の大幅成長となった。Googleも12%成長を達成した。これに対し、Xiaomiの出荷数は35%減、Sharpは28%減、Sonyは50%減となり、OEM各社の明暗が分かれる結果となった。

積極的な販売促進策も市場成長を下支えしている。けん引役の主力となっているのは、端末下取りプログラムに基づいた「1円スマホ」販促で、これが消費者から強い支持を集めており、初期費用を引き下げることで最新モデルへの買い替えを容易にしている。この仕組みによって、新規契約、端末買い替え、さらには2台目需要までも喚起されている。このほか、端末割引、ポイント還元、データ容量拡大、サービスバンドル、MNPインセンティブといったキャリア施策がこの需要を幅広く支えている。

2025年展望

2025年下半期、日本のスマートフォン出荷数は今年上半期の強力な成長の後で減速の可能性がある。Appleの優位は依然変わらない見込みだが、Samsung、Google、OPPO、Xiaomiも強い勢いを示している。新機能やコストパフォーマンスを背景に、市場競争はさらに激化が予想される。ただし、高価格化、買い替えサイクルの長期化、中古端末需要の拡大が全体的な成長を抑制する可能性もある。2026年に向けた一時的な追い風としては、NTT DOCOMOによる3Gネットワーク終了が買い替え需要を生み出すとみられる。キャリアの販促や端末下取りプログラムが買い替え需要を下支えするとはいえ、この成長が持続可能かどうかは不透明だ。今後の市場動向を注視することがきわめて重要である。

[原文] Japan’s Q2 2025 Smartphone Shipments Rise 11% YoY, Marking Second Straight Quarter of Double-digit Growth

- Japan’s smartphone shipments grew 11% YoY in Q2 2025, marking the second consecutive quarter of double-digit percentage growth, despite market maturity.

- Market leader Apple’s shipments climbed 38% YoY due to continued strong iPhone 16e sales momentum from Q1 2025.

- Samsung intensified its promotional efforts in 2025, due to which its shipments jumped 60% YoY, achieving one of its strongest market performances in recent years.

- Active promotions, including device-return programs, have stimulated demand and supported market growth in Japan.

Japan’s smartphone shipments climbed 11% YoY in Q2 2025, sustaining double-digit percentage growth for the second consecutive quarter despite the market’s maturity, according to Counterpoint Research’s Global Smartphone Market Shipment Tracker, Q2 2025. During the quarter, market momentum was mostly driven by Apple, which achieved notable share gains. The performance reflects the intensification of carrier promotions in Japan, with device trade-in programs, often marketed as ‘1-yen handsets,’ becoming a mainstream mechanism to stimulate replacement demand.

Apple, which holds the largest share in Japan’s smartphone market, registered strong sales for the iPhone 16e, continuing its solid performance momentum from Q1 2025. However, in the second half of the year, Apple will have to rely more on other models and new product launches for growth as the brand’s early momentum has already started tapering off since June.

Meanwhile, Android vendors witnessed a mixed performance, with some achieving solid gains. Samsung intensified its promotional efforts in 2025 and posted a substantial 60% YoY increase in shipments during the quarter, while Google achieved 12% growth. In contrast, Xiaomi’s shipments fell 35%, Sharp declined 28%, and Sony tumbled 50%, highlighting the diverging fortunes among OEMs.

Active sales promotions are also supporting market growth. A key driver has been the ‘1-yen device’ promotions built on device return programs, which have been gaining strong consumer traction, lowering upfront costs and making upgrades to the latest models easier. This is stimulating new contracts, device upgrades, and even second-device purchases. Additionally, carrier initiatives such as device discounts, point rebates, expanded data packages, service bundles, and MNP incentives are broadly underpinning this demand.

2025 Outlook

In the second half of 2025, smartphone shipments in Japan may slow down after the strong growth seen earlier in the year. Apple’s dominance will likely continue, but Samsung, Google, OPPO, and Xiaomi are also showing strong momentum. Competition in the market is expected to become more intense, driven by new features and cost performance. However, higher prices, longer replacement cycles, and growing demand for used devices could limit overall growth. As a temporary boost toward 2026, NTT DOCOMO’s planned shutdown of its 3G network is also expected to generate replacement demand. Even with carrier promotions and device return programs supporting replacement demand, whether this growth can be sustained remains uncertain. It will be crucial to closely monitor market trends.