半導体ファウンドリー2.0世界市場のQ2'25の収益~先進プロセスとパッケージングの牽引により前年比19%増 [半導体調査部門]

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

Counterpoint Research

半導体調査レポート

ラインナップはこちらから

Global Semiconductor Foundry 2.0 Market’s Q2 2025 Revenue Up 19% YoY Driven by Advanced Process and Packaging

- The semiconductor foundry 2.0 market’s revenue surged 19% YoY in Q2 2025, driven by robust and sustained demand on both advanced process and advanced packaging. We expect this momentum will continue, resulting in a mid-single digit revenue growth into Q3 2025.

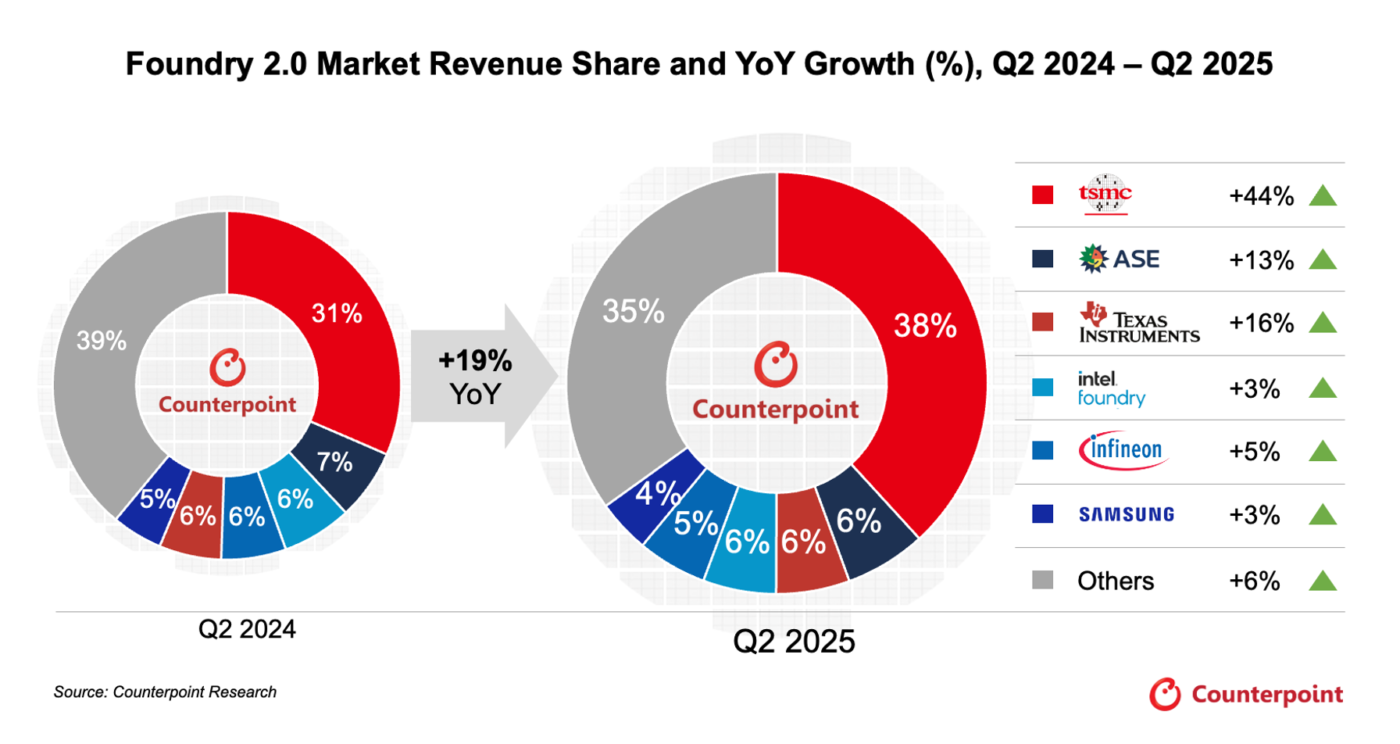

- TSMC market share rose from 31% in Q2 2024 to 38% in Q2 2025 on 3nm ramp and CoWoS expansion .

- OSAT sector growth accelerates to 11% YoY from only 5% during Q2 2024; ASE contributes most and KYEC enjoys steepest rise benefiting from AI GPU demand.

- Looking ahead, we see advanced packaging driving new growth momentum for OSAT companies.

- Non-memory IDM returned to positive growth, but automotive sector yet to show a significant order recovery in H1 2025; we expect rebound to arrive later in H2.

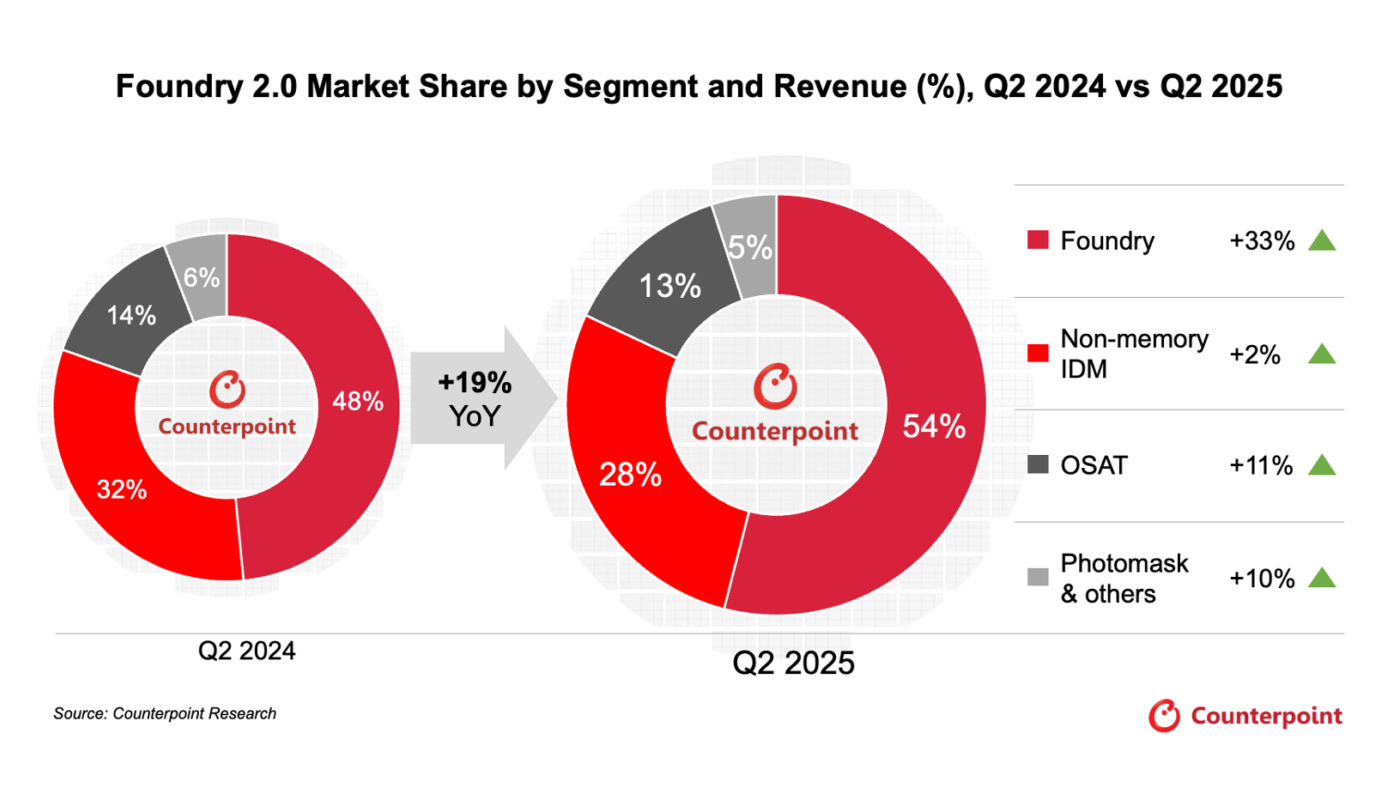

Looking at the evolution of semiconductors industry from smartphone to HPC chips boom, the traditional semiconductor foundry (Foundry 1.0), which focused primarily on chip manufacturing, is no longer sufficient to highlight sector dynamics, which are now driven by AI trends and related system-level optimization. Companies are moving from being part of the manufacturing line to a technology integration platform. This will ensure tighter vertical alignment, faster innovation, and deeper value creation. Thus, we are including pure foundry, non-memory IDM, OSAT, and photomask making vendors in foundry 2.0 vs. only pure foundry players in our foundry 1.0 definition.

According to Counterpoint Research's Foundry Revenue Tracker by Nodes, global semiconductor “foundry 2.0” market’s revenue surged 19% YoY in Q2 2025, largely driven by robust and sustained AI demand on both advanced process and advanced packaging, and also benefited from pull-in demand by China subsidy program. We expect this momentum will continue to accelerate, resulting in a mid-single digit QoQ revenue growth into Q3 2025.

For pure-foundry market, TSMC’s market share rose from 31% in Q2 2024 to 38% in Q2 2025, firmly maintaining its position as the market leader, and accounting for 75% of the YoY revenue growth in foundry 2.0 market in Q2 (vs.10% contribution from other pure-foundry players). The 44% YoY revenue growth was largely due to 3nm ramp up, high utilization rate in 4/5nm from AI GPU, and CoWoS expansion, which we believe will continue to be the major growth driver into H2 2025.

OSAT sector delivers a 11% YoY revenue growth in Q2 2025 (vs. 5% YoY in Q2 2024) as ASE contributed most of revenue growth, while KYEC delivered the strongest YoY growth (30%+ YoY), benefiting from AI GPUs. Advanced packaging is set to provide new growth momentum for OSAT companies. AI GPU and AI ASIC will be the major growth drivers for OSAT vendors in 2025/2026, with potential upside from incremental orders from other sectors. The revenue growth in Q2 echoes our views of advanced packaging set to provide new growth momentum for OSAT companies.

Commenting on the performance of advanced packaging, Senior Analyst William Li said, “As advanced packaging technologies gain importance, we believe chip vendors will increasingly rely on advanced packaging to enhance the performance of their chip solutions. Given TSMC’s current technological capabilities and strong customer relationships, the company is expected to remain not only a leader in advanced process node but also a front-runner in advanced packaging for the foreseeable future.

Non-memory IDMs returned to a 2% revenue growth in Q2 2025 (from -9% YoY in Q2 2024), mainly driven by Texas Instrument’s 16% YoY revenue expansion. Due to clients’ inventories being at a relatively low level, orders’ visibility was relatively solid compared to previous quarter, and we continue to see a warm recovery in industrial sector, which will likely drive the revenue growth. However, automotive sector have yet to show a significant order recovery in H1 2025, and we expect the rebound to arrive later in H2.

Overall, commenting on the revenue performance in H2, Senior Analyst Jake Lai said, “The traditional peak season for consumer electronics, the accelerating AI applications/orders, and the existing subsidy policy in the Chinese market will be major drivers in Q3.” We expect foundry utilization rate in advanced process node in Q3 2025 and wafer shipment across pure-foundry vendor will continue to grow.