第4四半期のFPD生産工場の稼働率は低下傾向

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

カウンターポイントリサーチが今月発刊した Quarterly All Display Fab Utilization Report 最新号によると、予想を上回る第3四半期の後、フラットパネルディスプレイ生産工場の稼働率は2025年第4四半期に低下傾向にあります。2025年第3四半期の生産量増加は在庫の増加につながり、年末商戦期の需要予想を上回るリスクがあります。

本レポートは、業界内のあらゆるフラットパネルディスプレイ生産工場(合計100以上の工場)の月間生産能力、TFT入力、稼働率を詳細に示しています。また、サプライヤー、国、TFT工場の世代、バックプレーン、フロントプレーン、または基板の種類ごとにセグメント化できるピボットテーブルも含まれています。本レポートは、2019年第1四半期まで遡った稼働率の履歴と、2026年第1四半期までの月別予測を提供しています。

Flat Panel Display Fab Utilization Trending Down in Q4

After a stronger-than-expected third quarter, flat panel display fab utilization is trending down in Q4 2025, according to the latest release of Counterpoint Research’s Quarterly All Display Fab Utilization Report, issued last week. Higher production in Q3 2025 has led to a build-up in inventory which risks overshooting the expected demand in the holiday sales season.

The report details monthly capacity, TFT input and utilization for every flat panel display fab in the industry, which means more than 100 fabs in all, and includes pivot tables to allow segmentation by supplier, country, TFT fab generation, backplane, frontplane or substrate type. The report provides historical utilization back to Q1 2019 and a forecast by month through the first quarter of 2026.

We saw a modest surge in utilization in Q1 2025 based on strong demand in the China TV market associated with a government subsidy program. According to Counterpoint’s Quarterly Advanced TV Shipment and Forecast Report, advanced LCD TV shipments in China increased by 140% in Q1 2025 and by 85% in Q2 2025, with especially strong growth in very large-sized TVs. Adding to the demand pull, TV makers rushed to get products into the US in anticipation of a tariff increase by President Trump. With the US tariff for TVs from China now set at 41.4%, TV brands are reshaping their supply chains and shifting production to Southeast Asia or Mexico, which results in longer supply chains and more inventory in the pipeline.

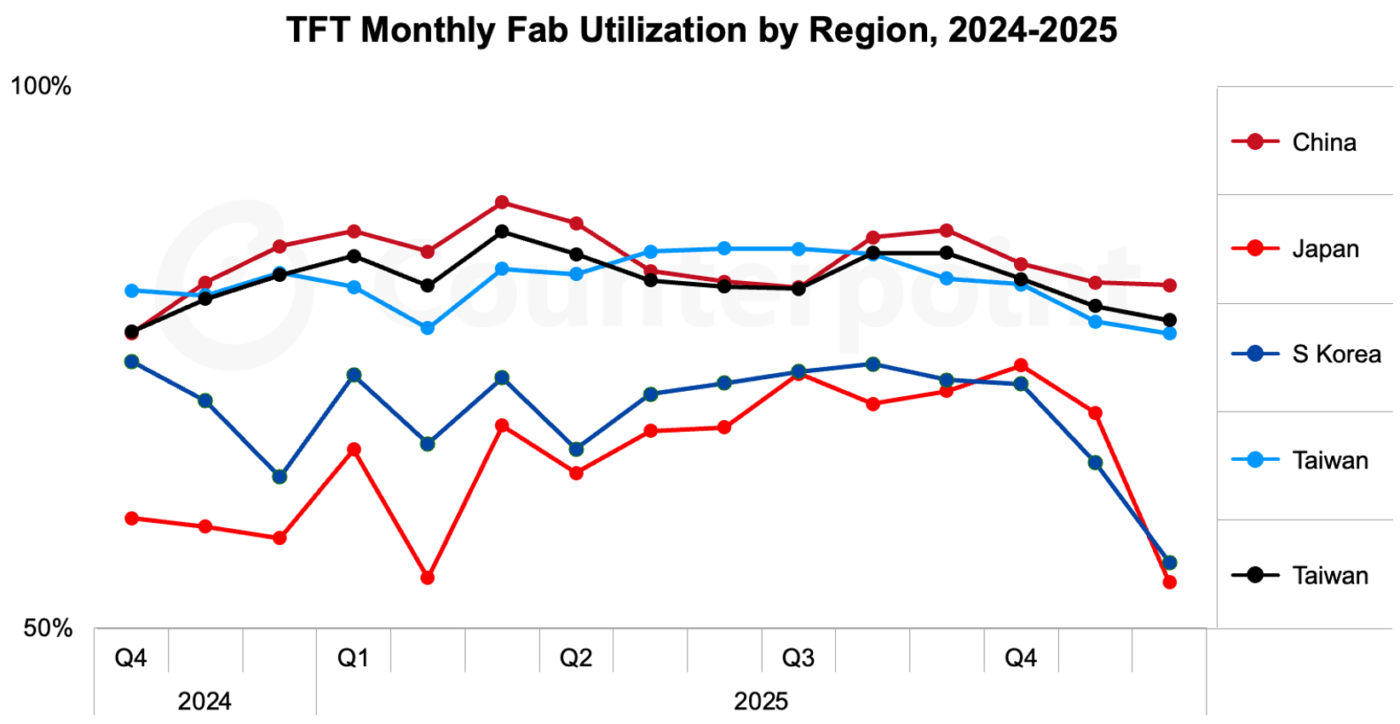

Although utilization in China decreased slightly in June and July 2025, it picked up again in August, as shown in the first chart here. With additional production in Q3 2025, TV makers have stocked adequately and are again putting pressure on LCD TV panel prices, which have resumed their downward trend.

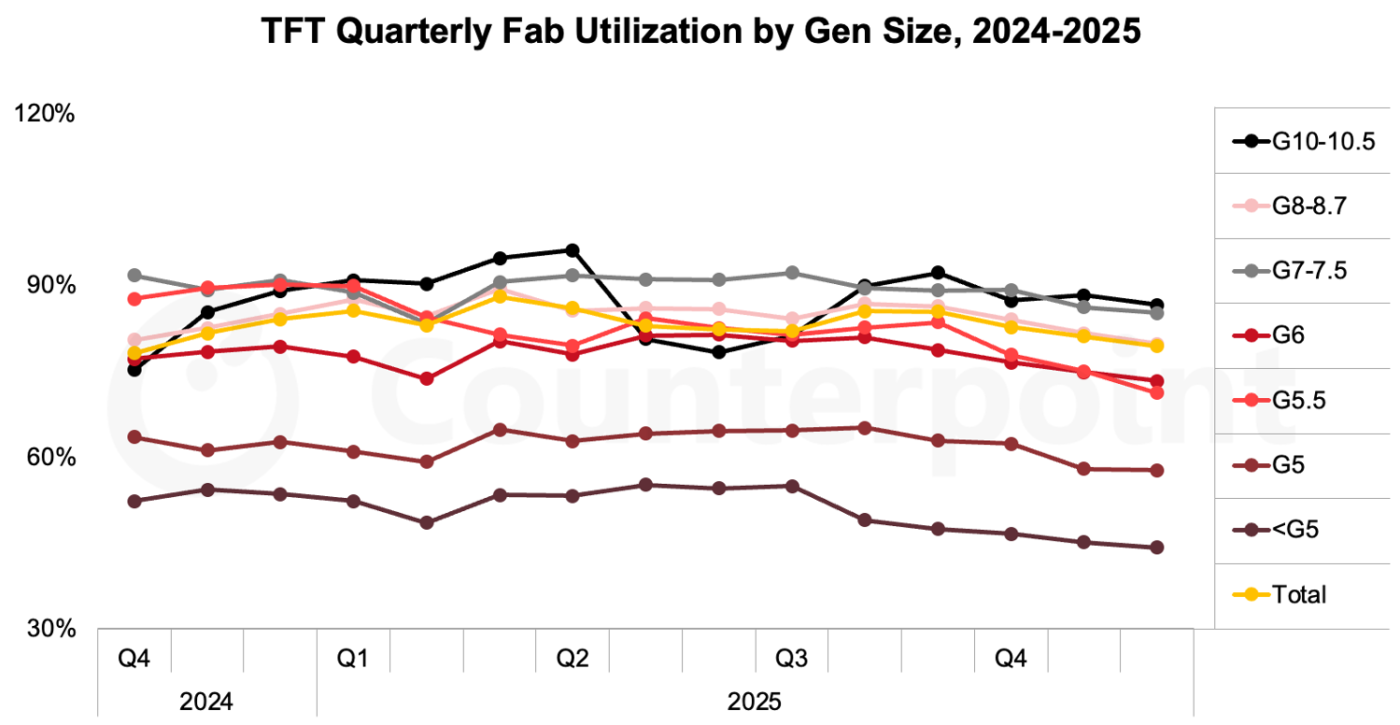

A look at fab utilization by Gen size highlights where the summer slowdown occurred – on Gen 10.5 lines. The four Gen 10.5 lines in China took a pause in May, June and July before returning to high utilization in August. The chart also shows that the smaller Gen fabs, which are typically older lines, have consistently low utilization. These lines are more likely used for niche applications and shorter product runs.

The display industry’s total capacity continues to exceed demand, but that gap is much smaller today than in 2022-2023. With geopolitical strife adding uncertainty to the demand picture, the industry will need to continue to restrain utilization to avoid a hard crash. That restraint looks a lot like a “tap on the brakes” in 2025 as compared to “slam on the brakes” in 2023 and 2024.

Counterpoint Research’s Quarterly All Display Fab Utilization Report covers capacity, TFT input and utilization by month for every flat panel display fab in the industry, with pivot tables to allow segmentation by supplier, country, TFT fab generation, backplane, frontplane or substrate type. The report provides historical utilization back to Q1 2019 and a forecast by month through the first quarter of 2026.

出典調査レポート Quarterly All Display Fab Utilization Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。