2025年のFPD用ガラス市場は11%成長見込み~出荷数増加と価格上昇が要因

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

2025年FPD用ガラス市場は11%成長見込み、出荷数増加と価格上昇が要因

FPD用ガラス市場出荷額が、2024年下半期の価格上昇と2025年上半期のFPDメーカー各社の稼働率上昇によって、10年以上ぶりに過去最高を記録する見通しだ。Counterpoint Researchが先週発刊した Quarterly Display Glass Report 最新版で明らかにしている。第3四半期と第4四半期は出荷額が減少すると見られるものの、2025年のFPD用ガラス出荷額は前年比11%増になると予測される。

Q2'25のFPD用ガラス生産能力は前期比1%増、前年比2%減だった。CorningはSharpの第10世代工場閉鎖を受け、日本での生産を終了した。その一方で中国の国内ガラスメーカーは2023年から2025年にかけて第8.5世代生産能力を追加している。生産能力は依然として需要をやや上回っており、一部は遊休状態にある。

Q2’25のガラスメーカーのFPD用ガラス出荷は前期比横ばい、前年比1%増となった。Q3’25の出荷は前期比3%減、Q4’25は前期比1%減と予測されている。

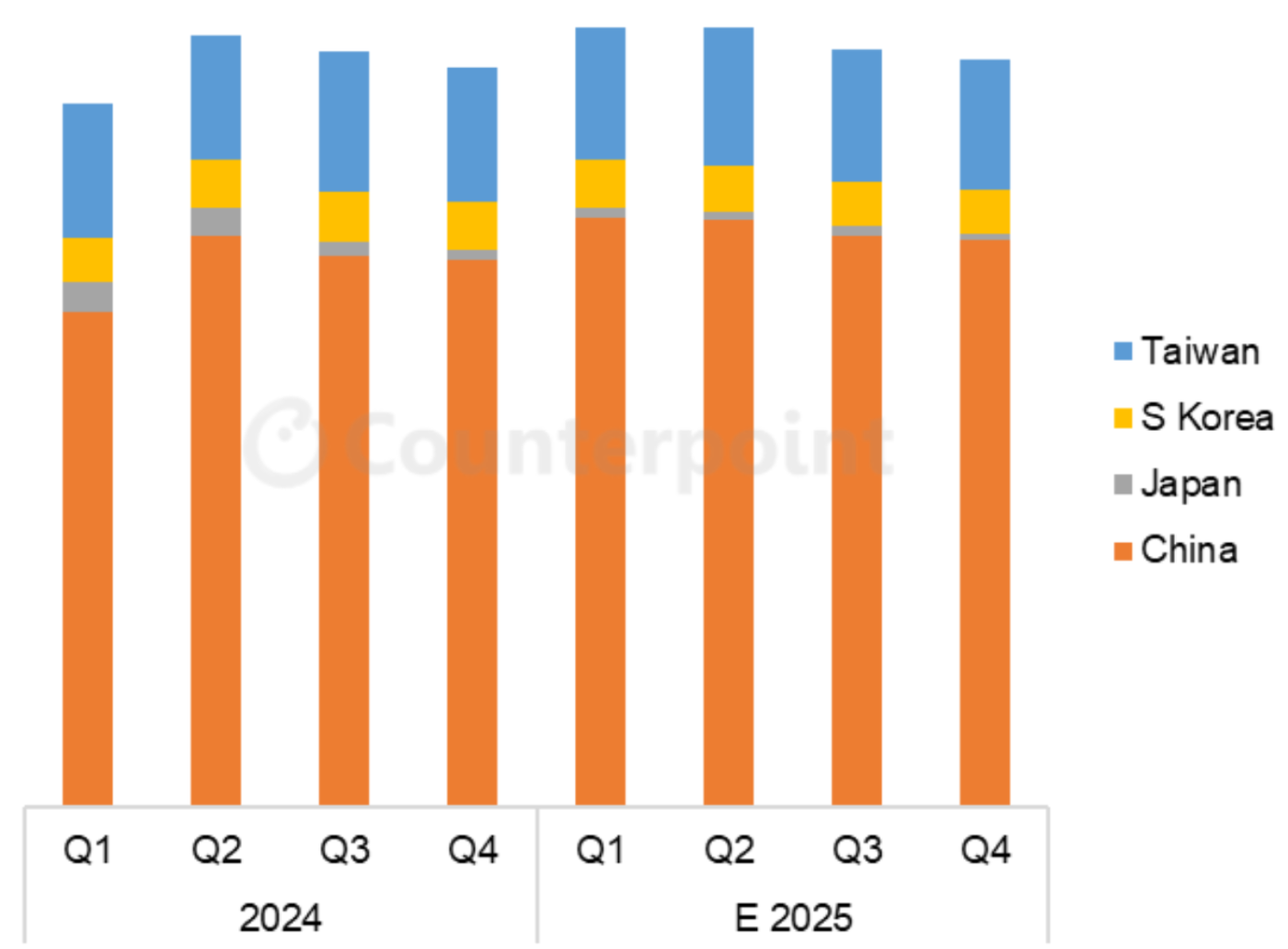

地域別の市場動向を見ると、FPD業界における中国パネルメーカーの支配的地位が浮き彫りになり、韓国と日本の市場での存在感が縮小していることがわかる。Samsung DisplayとLG DisplayがOLEDへの移行を進めLCD生産ラインを閉鎖したため、韓国のFPD総生産能力は減少している。また、ガラス需要もより顕著に減少しているが、これは2017年以降に追加されたOLED生産能力はガラスが1枚で済むのに対し、LCDは2枚必要であるためだ。10年前、韓国はガラス需要において最大の地域であり、2018年初頭のシェアは27%でだったが、Q4'25には6%未満に低下すると予測されている。

地域別 FPD用ガラス出荷の推移 (面積ベース)

本レポートではバックプレーンタイプ別でガラス市場を区分しており、そのデータからFPD業界における先進技術バックプレーンの重要性が浮き彫りになっている。OLEDが成長しているにもかかわらず、業界の主力製品であるアモルファスシリコン (a-Si) ガラス基板がFPD用ガラス需要の90%近くを占める状況が続いている。OLEDに比べてLCDの生産ライン稼働率が高いことから、このシェアは徐々にではあるが低下している。2025年のa-Siのシェアは88%程度で推移すると予測される。

Corningは2023年と2024年の両年に値上げを発表した。CorningはQ1’25までに、両年とも価格 (日本円ベース) を2桁%引き上げることに成功したと発表した。Q1’25とQ2'25のガラス価格は、前期比では横ばいだが前年比では10%上昇し、Q4’16以来の最高値を維持したものと推定される。

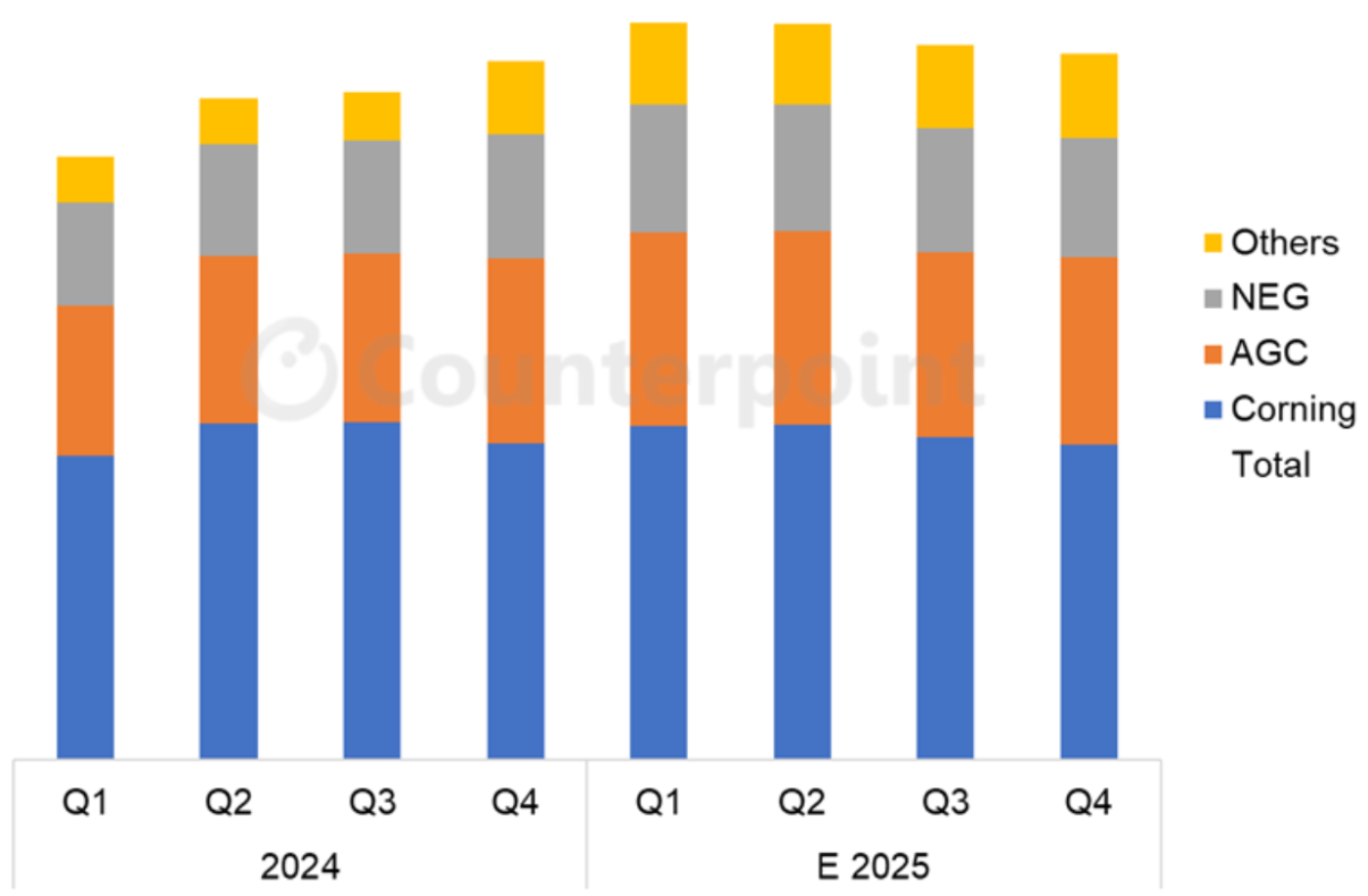

Corningは数量、金額ともにガラスメーカー首位の座を維持している。ただし、Q3’24からQ4’24にかけて、中国の国内ガラスメーカーの生産能力増強とSDP第10世代の閉鎖により、Corningのシェアは低下した。Q2’25は数量と価格が前期比で横ばいだったため、出荷額もまた横ばいとなった。Q3’25の出荷額は日本円ベースで前期比3%減、Q4'25はさらに前期比1%減になる見通しだ。2025年の業界全体の出荷額は前年比11%増と予測される。

メーカー別 FPD用ガラス出荷額の推移 (円ベース)

------------------------------------

Counterpoint Researchの Quarterly Display Glass Report はすべてのLCDおよびOLED生産ラインを対象に主要ガラスメーカー全社のガラス能力と出荷を追跡しており、地域/FPDメーカー/バックプレーンタイプ/基板サイズなどの項目別にデータを表示できるピボットテーブルを提供しています。第1世代から第10.5世代までのa-SiガラスとLTPSガラスの価格データのほか、Q1’19からの四半期実績とQ3’25までの予測を掲載しています。

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Display Glass Market to Grow 11% in 2025 on Strong Volume, Price Increases

An increase in prices in the second half of 2024, combined with strong utilization by panel makers in the first half of 2025, drove the display glass market to its highest value in at least 10 years, according to Counterpoint Research’s Quarterly Display Glass Report, released last week. We expect that revenues will decline in both the third and fourth quarters, but even with those declines, display glass revenues will increase 11% YoY in 2025.

Industry capacity for display glass increased by 1% QoQ but decreased by 2% YoY in Q2 2025. Corning has shut down capacity in Japan after Sharp’s Gen 10 fab shutdown. On the other hand, domestic Chinese glass makers have added Gen 8.5 capacity during 2023-2025. Capacity remains somewhat higher than demand and some capacity sits idle.

Glass maker shipments in Q2 2025 were flat QoQ and up 1% YoY. Shipments are expected to decline 3% QoQ in Q3 2025 and decrease by 1% QoQ in Q4 2025.

A view of the market in terms of regions demonstrates the dominance of Chinese panel makers in the display industry and the shrinking relevance of South Korea and Japan in the market. As both Samsung Display and LG Display have shifted to OLED and closed LCD lines, their total display capacity in South Korea has decreased. Their glass demand has further reduced because all the OLED capacity added since 2017 requires only one piece of glass, whereas LCD requires two. Ten years ago, South Korea was the biggest region in terms of glass demand, and its share was 27% at the beginning of 2018, but we forecast that it will fall to less than 6% in Q4 2025.

The report also gives a split of the glass market by backplane type, showing the importance of more advanced backplanes in the display industry. Despite the growth of OLED, industry workhorse amorphous silicon (a-Si) glass substrates continue to make up close to 90% of display glass demand. This share is declining but slowly because of high fab utilization for LCD compared to OLED. We expect that the a-Si share will hold steady at about 88% in 2025.

Corning announced price increases in both 2023 and 2024. By Q1 2025, Corning declared that it had succeeded in implementing a double-digit price increase in both years (in yen terms). We estimate that glass prices were flat QoQ in both Q1 and Q2 2025 but up 10% YoY and remain at their highest point since Q4 2016.

Corning remains the leading glass maker both in terms of volumes and revenues. But its share decreased from Q3 2024 to Q4 2024 as domestic Chinese glass makers added capacity and SDP Gen 10 shut down. With both volume and price flat QoQ in Q2 2025, revenues were flat QoQ. We forecast that revenues (in yen) will be down 3% QoQ in Q3 2025 and down another 1% QoQ in Q4 2025. We forecast that total industry revenues for 2025 will be up 11% from 2024.

Counterpoint Research’s Quarterly Display Glass Report tracks glass capacity and shipments for all major glass makers across all LCD and OLED display fabs, providing pivot tables that allow splits by region, panel maker, backplane type and TFT Gen Size. The report includes prices for a-Si and LTPS glasses for Gen sizes 1 to 10.5, quarterly history from Q1 2019, and a forecast through Q3 2025.