先端技術FPD搭載TVコストレポートを発刊~QD-OLEDから116インチLCD までのディスプレイを追跡

出典調査レポート Semi-Annual Advanced TV Display Cost Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

- 中国は2025年も政府による補助金制度が継続し、人件費、間接費、販売費および一般管理費など、主要分野におけるコスト優位性を維持するだろう。一方、中国と韓国のWOLED生産ラインはすでに減価償却が完了、中国の総生産コストはさらに低下しており、コスト優位性がさらに拡大している。

- 中国におけるTV用55インチUHDWOLEDパネルの総生産コストは韓国に比べて約20%低くなる見込みで、65インチUHDパネルでも同様のコスト優位性が予測される。

- QD-OLEDパネルの歩留まりは予想以上の速度で改善しており、2025年の歩留まり予測はTV用の55インチおよび65インチパネルで85%未満とWOLEDに近づいている。しかし、減価償却費と販売費および一般管理費が高いため、QD-OLEDパネルのコストは同サイズのWOLEDパネルに比べて60-80%高くなっている、とシニアアナリストのNikhil Kishorは述べている。

- インクジェット印刷 (IJP) は材料の利用効率向上と廃棄の削減により、材料コストの削減につながるはずだ。ただし、新規IJPラインの減価償却費は、すでに減価償却が完了しているWOLEDラインに比べてかなり高い。

Counterpoint Researchが、OLEDおよびLCDのコストプロファイルを更新した Semi-Annual Advanced TV Display Cost Report 最新版を発刊した。2025年上半期版には、WOLEDパネル全サイズおよび55インチ以上のLCD (MiniLEDバックライト搭載LCDを含む) の最新情報、ならびにSDCの55インチ、65インチ、77インチQD-OLEDパネルのコスプロファイルが掲載されている。また、中国の第8.5世代、第8.6世代、第10.5世代基板で製造された98インチ、100インチ、115インチ、116インチUHD-LCDパネルのコストプロファイルも新たに追加された。SDCの新たなゲーミングモニターである49インチおよび34インチQD-OLEDパネルも含まれている。

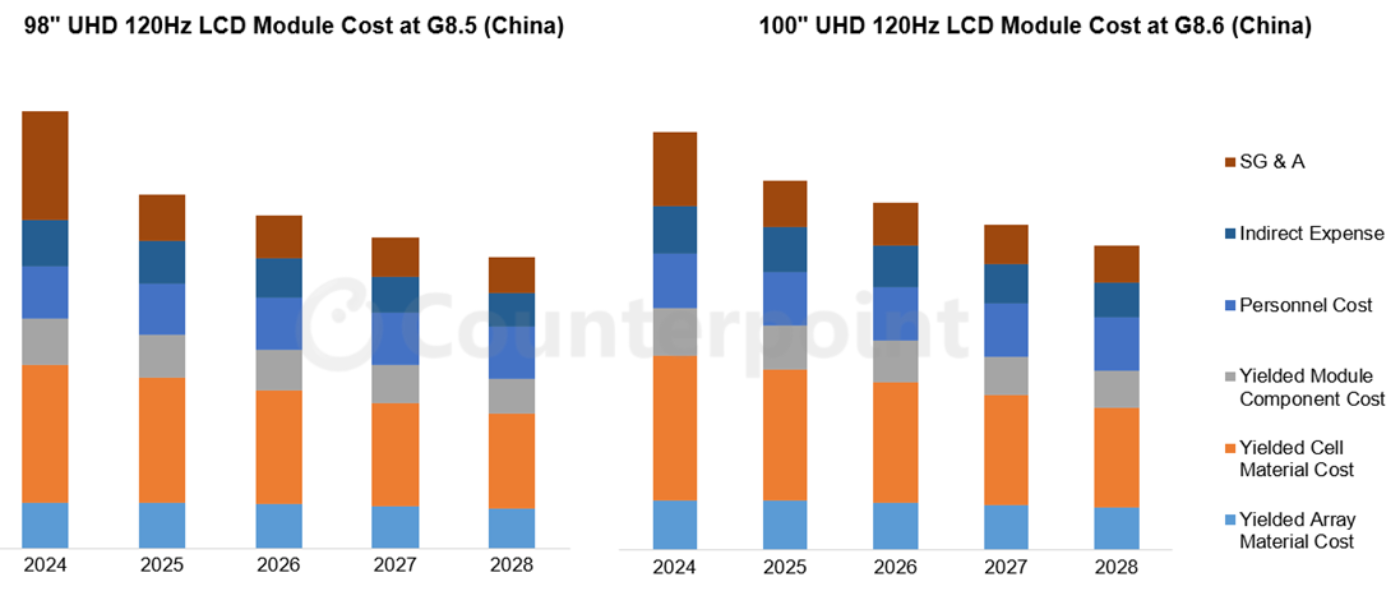

以下のグラフはリサーチディレクターであるBob O’Brienによるもので、2024年から2028年までの98インチ/100インチLCDパネルのコスト構造を示しており、コスト要素ごとの内訳と対応する歩留まりの推定値が記載されている。これらの大型LCD製品は、中国で第8.5世代および第8.6世代ラインにおいて2面取りで効率良く製造されている。これら製品の高い歩留まりがコスト効率向上をもたらしている。そのため、中国のパネルメーカーは価格を積極的に引き下げ、中国のTVブランドはこのような超大型サイズを積極的に販売促進し、売上成長をけん引している。

中国の98インチ/100インチUHD 120Hz LCDモジュールコスト

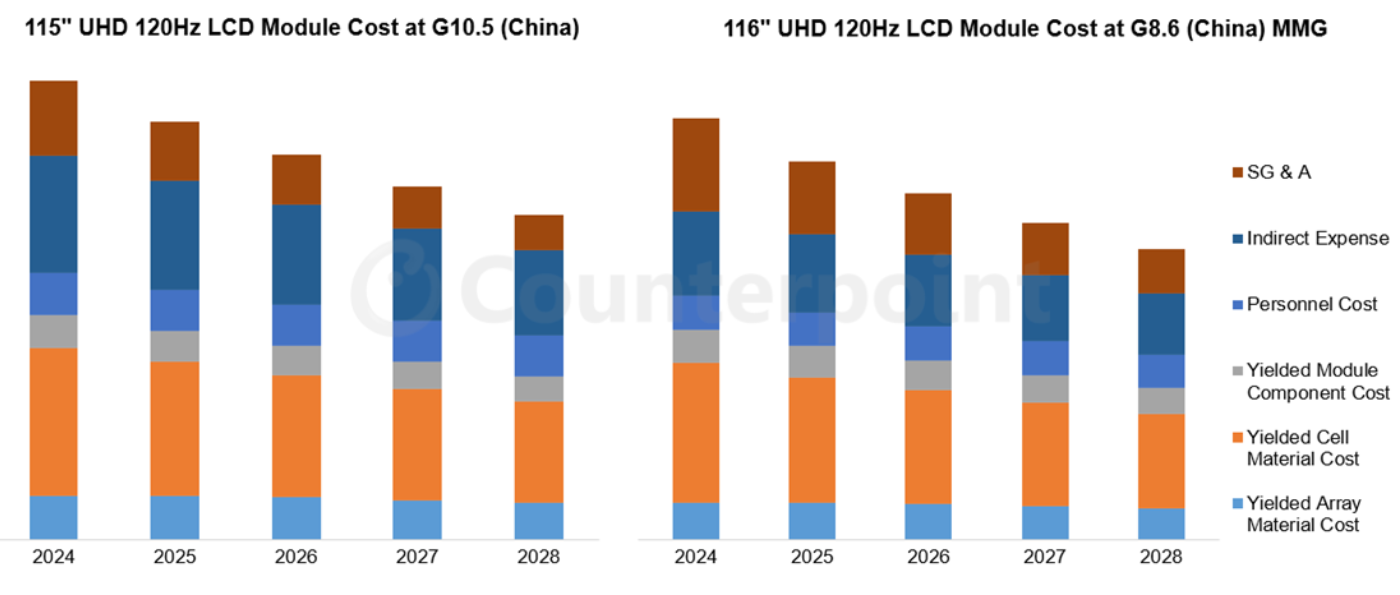

以下のグラフは、2024年から2028年までの115インチ/116インチLCDパネルのコスト構造を示しており、コスト要素ごとの内訳と対応する歩留まりの推定値が記載されている。115インチLCDパネルは中国で第10.5世代ラインで2面取りで効率良く製造されている。一方、116インチLCDパネルは第 8.6世代ラインでMMG採用によって効率を向上させている。これら製品の高い歩留まりがコスト効率向上をもたらしている。これらのサイズは、RGB MiniLEDなどの新技術を採用したフラッグシップモデルに採用されている。

中国の115インチ/116インチUHD 120Hz LCDモジュールコスト

出典調査レポート Semi-Annual Advanced TV Display Cost Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Counterpoint’s Advanced TV Cost Report Tracks Displays From QD-OLEDs to 116” LCDs

- In 2025, the ongoing government subsidies continue to give China a cost advantage across key areas, including personnel cost, indirect expenses and SG&A. Meanwhile, with WOLED production lines in both China and South Korea now fully depreciated, China's overall production costs have declined further, widening its cost lead.

- Total production cost of a 55” UHD WOLED TV panel in China will be nearly 20% lower than in South Korea, with a similar cost advantage projected for 65” UHD panels.

- Yields for QD-OLED panels have improved faster than expected and our yield estimates for 2025 are under 85% for 55” and 65” TV panels, which is close to WOLED, but higher depreciation cost and SG&A make the QD-OLED panel cost 60%-80% higher than a WOLED of the same size, said Senior Analyst Nikhil Kishor.

- IJP should result in a reduction in material costs through better utilization and less waste. But depreciation costs for a new IJP line are substantially higher than for a fully depreciated WOLED line.

Counterpoint Research has released its latest Semi-Annual Advanced TV Display Cost Report, with updates to OLED and LCD cost profiles. The H1 2025 edition includes updates to all sizes of WOLED panels and 55”+ LCD, including LCD with MiniLED backlights, and cost profiles for 55”, 65” and 77” QD-OLED panels from SDC. We have also added new cost profiles of 98”, 100”, 115” and 116” UHD-LCD panels, manufactured on Gen 8.5, Gen 8.6 and Gen 10.5 substrates in China. It covers the new gaming monitors from SDC, which are 49” and 34” QD-OLED panels.

The chart by Research Director Bob O’Brien shows the cost profiles for 98”/100” LCD panels from 2024 through 2028, with breakdown by cost components and the corresponding estimates of yield. These large-size LCD products are made with efficient two cuts on Gen 8.5 and Gen 8.6 lines in China. Better yields on these products make them cost-efficient. Hence, panel makers in China have aggressively reduced prices, and Chinese TV brands have aggressively promoted these ultra-large sizes, generating sales growth.

The chart below shows the cost profiles for 115”/116” LCD panels from 2024 through 2028, with breakdown by cost components and the corresponding estimates of yield. The 115” LCD panel is made with efficient two cuts on Gen 10.5 in China, whereas the 116” LCD panel combines MMG on Gen 8.6 lines to improve the efficiency. Better yields on these products make them cost-efficient. These sizes are used for “flagship” models with new technology such as RGB MiniLED.