インドネシア乗用車市場で中国ブランドが急成長~日本ブランドは減少 [オートモーティブ調査部門]

Counterpoint Research

オートモーティブ調査レポート

ラインナップはこちらから

本記事のポイント

•中国ブランドは、競争力のある価格設定、積極的な現地生産投資、そしてインドネシア消費者向けの手頃な価格帯の電気自動車 (EV) ラインナップの拡充により、2025年第2四半期に市場シェアを3倍の22%に拡大しました。

•この躍進の大部分は、中国ブランドにシェアを奪われた日本ブランドの犠牲の上に成り立っています。ハイブリッド車への注力とEV普及の遅れにより、インドネシアでEVが急速に成長する中で、日本ブランドは市場の変化に対応しきれていません。

インドネシア乗用車市場で中国ブランドが急成長~日本ブランドは減少

インドネシアの乗用車市場は劇的な変貌を遂げています。長年にわたり市場を支配してきた日本メーカーが地位を失う中、中国ブランドが急速に台頭し、競争環境を再構築しています。

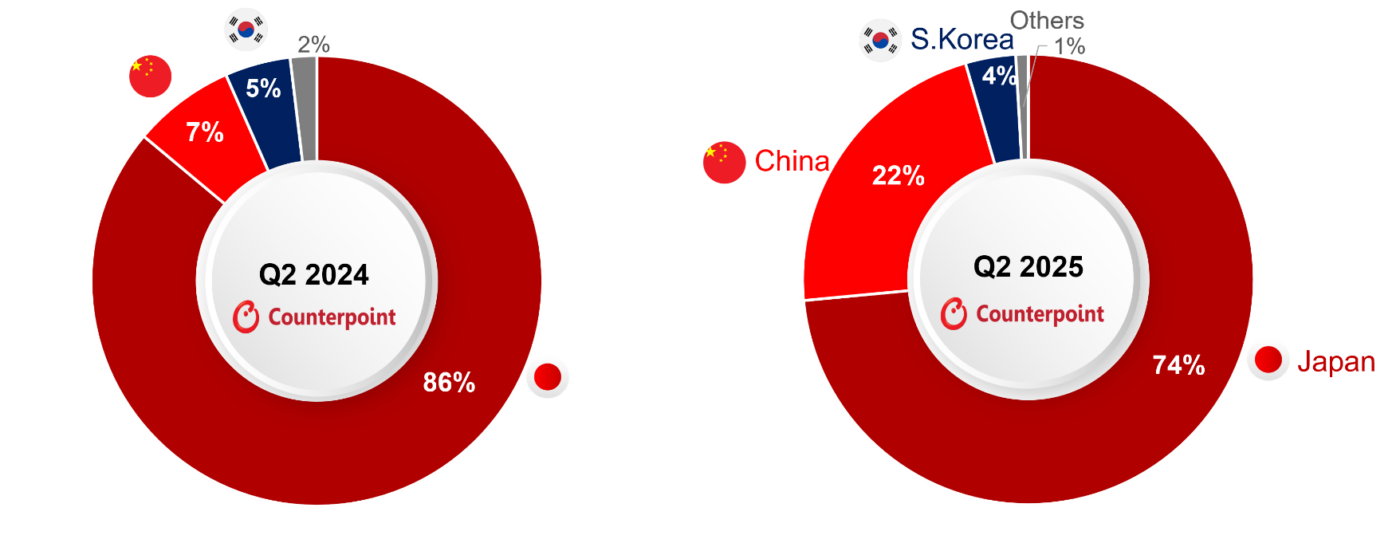

カウンターポイントリサーチ (オートモーティブ調査部門) が発刊した Q2 2025 Passenger Vehicle Sales Tracker によると、インドネシアにおける日本自動車メーカーのシェアは、2024年第2四半期の86%から2025年第2四半期には74%へと急落しました。対照的に、中国自動車メーカーは電気自動車 (EV) 普及の波に乗り、同時期に7%から22%へと急伸しました。

Indonesia Passenger Vehicle Market Share by Brand Origin Country (Q2 2024 vs. 2025)

カウンターポイントリサーチのアソシエイトディレクター Liz Lee は次のように述べています。「この市場シフトの主因は、電気自動車の爆発的な成長です。わずか1年前の2024年第2四半期には、インドネシアの太陽光発電市場における電気自動車 (EV) の普及率はわずか6%でした。2025年第2四半期までに、この数字は3倍以上の20%に増加しました。トヨタ、ダイハツ、ホンダなどの日本メーカーはハイブリッド車に注力し続けましたが、EVの勢いを捉えることはできませんでした。対照的に、中国メーカーは強力な価格競争力と積極的な現地生産によってこの機会を捉え、EV市場のリーダーとしての地位を確立しました。」

BYDは西ジャワ州スバンに年間15万台の生産能力を持つ工場を建設中で、2025年末の完成を目指している。五菱はすでにインドネシアでブカシ工場を稼働させ、「Air EV」など小型EVの現地組立を拡大している。広州汽車 (GAC) と奇瑞汽車 (Chery) も現地組立・現地化戦略を加速させ、新型EVモデルをインドネシアで生産している。直近では、小鵬汽車 (Xpeng) が電気MPV「X9」のCKD (完全ノックダウン) 生産を開始した。CKDとは、車両を完全分解した状態で輸出し、インドネシアで再組立を行う方式である。

インドネシア政府の政策も中国メーカーを優遇している。2025年までに全車両の20%をEV化するという積極的な目標を掲げ、減税や輸入関税の免除、現地生産連動型インセンティブなどの施策を導入している。日本の自動車メーカーがEVへの移行の停滞と販売減少に苦戦する一方で、中国メーカーはこうした政策支援を活用し、積極的に市場プレゼンスを拡大しています。

注:

EVには、バッテリー電気自動車 (BEV) とプラグインハイブリッド電気自動車 (PHEV) の両方が含まれます。ただし、ハイブリッド電気自動車 (HEV) は含まれません。

記事原文 (英語版)

POINTS

- Chinese brands triple market share to 22% during Q2 2025, driven by their competitive pricing, aggressive local production investments, and a growing line-up of affordable electric vehicles (EV) tailored for Indonesian consumers.

- Most of the gains come at the expense of Japanese brands as they shed share to the Chinese. The focus on hybrids and slower EV adoption limited their ability to keep pace with the market transition as Indonesia experiences rapid growth in EV.

Chinese Brands Surge in Indonesia’s Passenger Vehicle Market - Chinese Brands gain at Japanese loss

Indonesia’s passenger vehicle market is undergoing a dramatic transformation. As Japanese automakers, the long-time dominant players, lose ground. Chinese brands are rapidly surging and reshaping the competitive landscape.

According to Counterpoint Research’s Q2 2025 Passenger Vehicle Sales Tracker, Japanese automakers’ share in Indonesia fell sharply from 86% in Q2 2024 to 74% in Q2 2025. In contrast, Chinese automakers surged from 7% to 22% during the same period, riding the wave of electric vehicle (EV) adoption.

Liz Lee, Associate Director at Counterpoint, commented “The key driver behind this market shift is the explosive growth of electric vehicles. Just a year ago, in Q2 2024, EV penetration in Indonesia’s PV market stood at only 6%. By Q2 2025, that figure has more than tripled to 20%. While Japanese brands such as Toyota, Daihatsu and Honda remained focused on hybrids, they were less able to capture the EV momentum. In contrast, Chinese brands seized the opportunity with strong price competitiveness and aggressive local production, positioning themselves as leaders in the EV market.”

BYD is constructing a plant in Subang, West Java, with an annual capacity of 150,000 units, scheduled for completion by the end of 2025. Wuling already operates its Bekasi plant in Indonesia and has expanded local assembly of small EVs such as the Air EV. GAC and Chery have also accelerated local assembly and localization strategies, with new EV models now being produced in Indonesia. Most recently, Xpeng began local production of its X9 electric MPV through a CKD (Completely Knocked Down) system, exporting vehicles in fully disassembled form for reassembly in Indonesia.

The Indonesian government’s policy stance is also favoring Chinese automakers. With an aggressive target of converting 20% of all vehicles to EVs by 2025, the government has introduced measures including tax cuts, import duty exemptions, and local production-linked incentives. While Japanese automakers struggle with sluggish EV transitions and declining sales, Chinese brands are capitalizing on these policy supports and aggressively expanding their market presence.

Notes:

EVs include both battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). But do not include hybrid electric vehicles (HEVs).

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.