TCLとHisense、MiniLEDでプレミアムTV市場でのシェア拡大を継続

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

TCL, Hisense Continue to Gain Share in Premium TV Market with MiniLED

※ご参考※ 無料翻訳ツール (Google)

TCL and Hisense both continued to gain share in the premium TV market in Q2 2025. The two companies have blown past LG and are battling for the #2 spot behind Samsung, according to Counterpoint Research’s latest Quarterly Advanced TV Shipment and Forecast Report, released last week. During the quarter, TCL and Hisense drove another huge increase in shipments in their home market of China while also showing increasing strength in overseas markets.

The Counterpoint report helps understand market dynamics by providing premium TV shipment data by brand, display technology, size and resolution. The report covers 22 brands, 8 regions and all display technologies, including White-OLED, QD-OLED, MicroLED, MiniLED LCD, QD-LCD, Nano Cell LCD and 8K TV. The report combines top-down corporate-level surveys and bottom-up model-level data collection with Counterpoint’s proprietary models developed through decades of industry experience. Q2 2025 results were released last week, and an updated forecast will be released later this month. In this article, we will review the latest quarter.

In Q2 2025, global Advanced TV shipments increased 40% YoY and revenues increased 21% YoY. It was the fourth consecutive quarter of YoY growth, at least 40% in units and 20% in revenues.

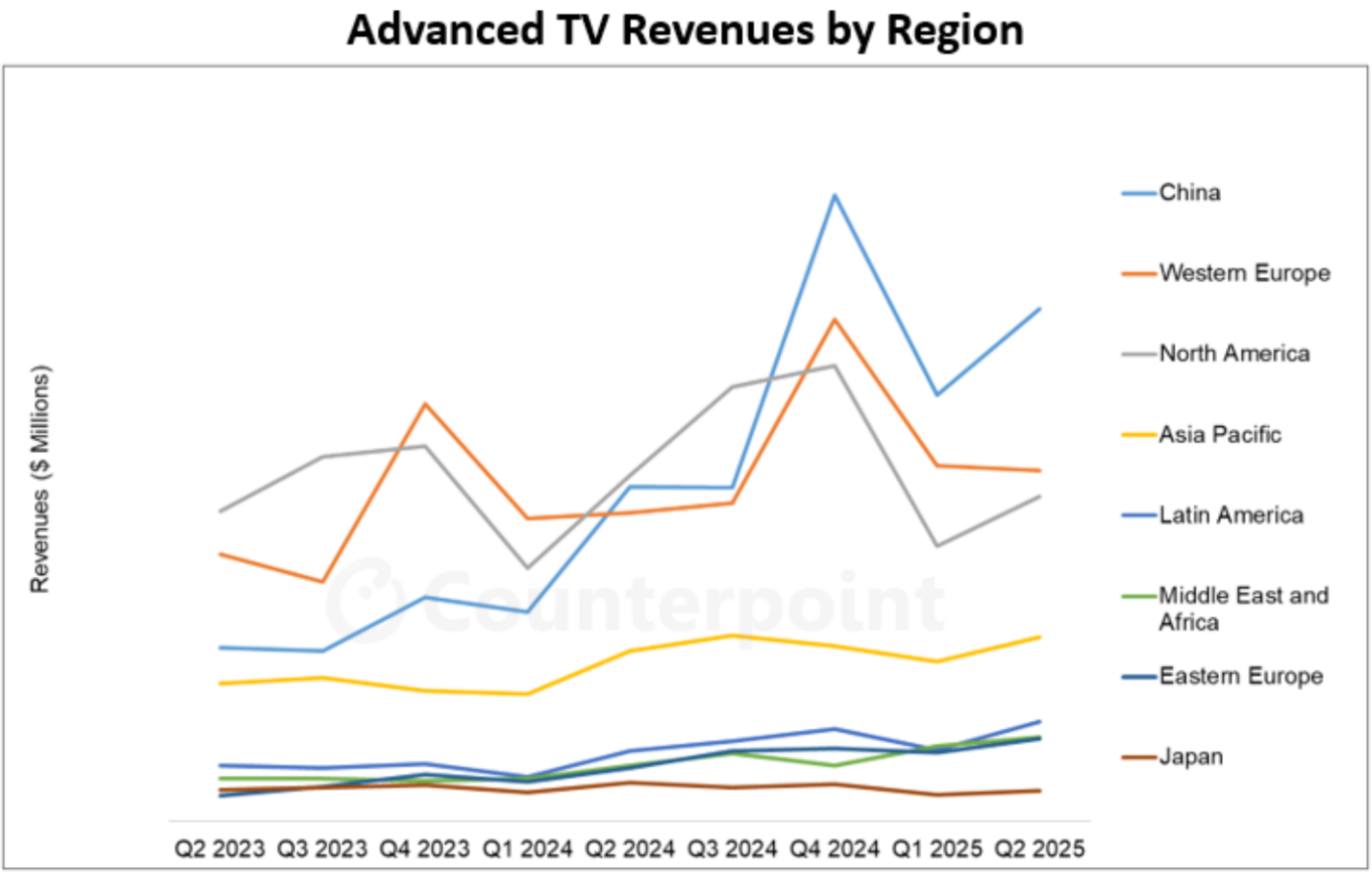

The first chart here shows revenues by region. North America revenues increased QoQ in the usual seasonal pattern but decreased 6% YoY. Revenues in Western Europe followed the seasonal pattern with a slight 1% decline QoQ but increased 14% YoY. China revenues continued to surge with a 53% increase YoY on an 85% increase in shipments. Helped by government incentives that encouraged consumers to trade in older TVs for new models and by aggressive promotions from domestic brands, Chinese consumers continued to purchase bigger, more expensive TV sets with more advanced display technologies.

Growth in other regions was more sedate but nevertheless encouraging. Revenues in Asia-Pacific increased 8% YoY on a 30% YoY increase in shipments. Latin American revenues increased 40% on a 65% increase in shipments. Revenues and shipments increased in every region YoY except North America and Japan.

The revenue growth in the China market, plus market share gains in other key regional markets, drove global share growth for both Hisense and TCL. Although growth for both companies slowed from the triple-digit % YoY increases in earlier quarters, both companies continued to post strong double-digit % increases. Revenues for Hisense and TCL increased YoY by 39% and 42% respectively. Hisense saw its unit share of the premium TV market increase by 1% YoY and its revenue share increase by 2% YoY. TCL’s unit share jumped by 4% and its revenue share increased by 2%.

Those gains came largely at the expense of the two South Korean giants. Samsung’s shipments increased 18% YoY and revenues increased only 10%. Its unit share of the premium TV market fell by 5% YoY, while its revenue share fell by 3%. LG’s shipments increased only 5% YoY and revenues decreased 13%. Its unit share of the premium TV market fell by 4% % and its revenue share fell by 6%.

Samsung has been focusing on OLED TVs with both White OLED and QD-OLED models, and it has achieved some success there. Samsung’s share in OLED TV units increased from 12% in Q1 2023 to 30% in Q2 2025, while its revenue share increased from 17% to 36% in the same period.

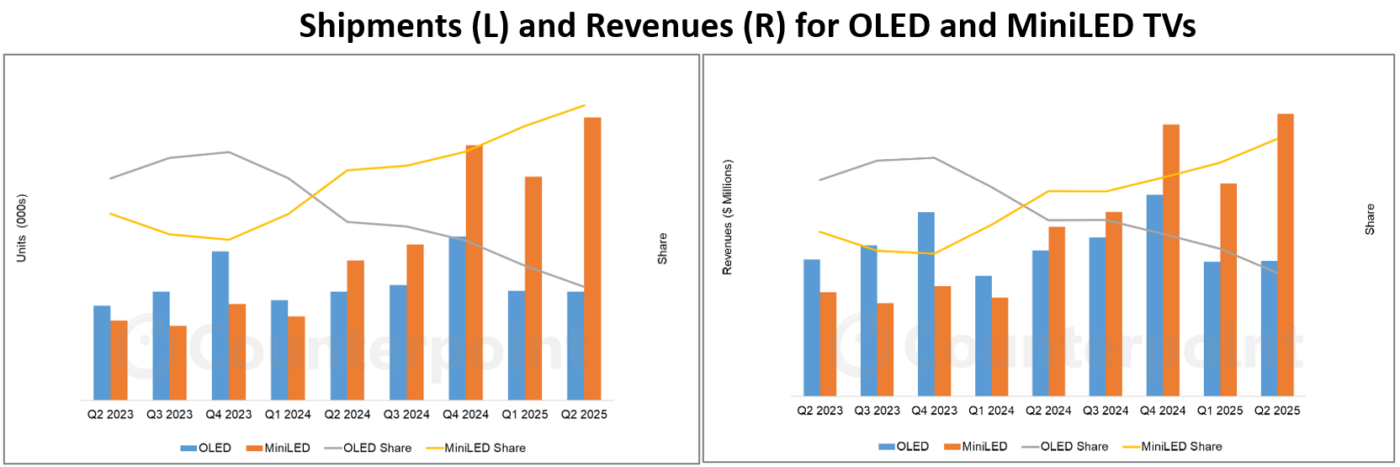

While Samsung was working to improve its OLED share, the Chinese brands were making OLED less important to the overall premium market by aggressively promoting large-screen MiniLED LCD models. MiniLED is taking an increasingly larger share of the “super-premium” market. Back in 2023, OLED captured 60% of units and 61% of revenues in the super-premium market, but MiniLED has grown while OLED has not. MiniLED surpassed OLED in Q2 2024 and has increased its share of the super-premium market in each quarter since then.

MiniLED TVs typically compete at price points similar to OLED TVs, but because of the cost difference between OLED and LCD TV panels, consumers face a choice between a smaller OLED TV or a larger MiniLED TV. An increasing number of consumers are choosing MiniLEDs, as shown in the next two charts. MiniLED LCD TV shipments increased 101% YoY, while OLED TV shipments were flat YoY. Similarly, MiniLED LCD TV revenues increased 66% YoY and OLED TV revenues decreased 7%.

Samsung dominated the MiniLED category in 2021-2022 and still led the category in 2023, but was passed in 2024, first by TCL, then by Hisense, and then by Xiaomi. In Q2 2025, Samsung held the #4 position in units and the #3 position in revenues, looking up at its Chinese competitors.

While the two South Korean brands have been focused on OLED TV, the Chinese TV brands, especially TCL and Hisense but also Xiaomi and Skyworth, have chosen not to try to compete in OLED. Instead, they have chosen to leverage China’s dominance in LCD to achieve a lower cost position, and then leverage that lower cost to aggressively promote very large MiniLED LCD screens, which the South Korean brands cannot match. Consumers are increasingly showing that the Chinese brands have made the right choice.