Q4’23のAdvanced (先端技術FPD搭載) TV市場~中国ブランドがシェアを拡大

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

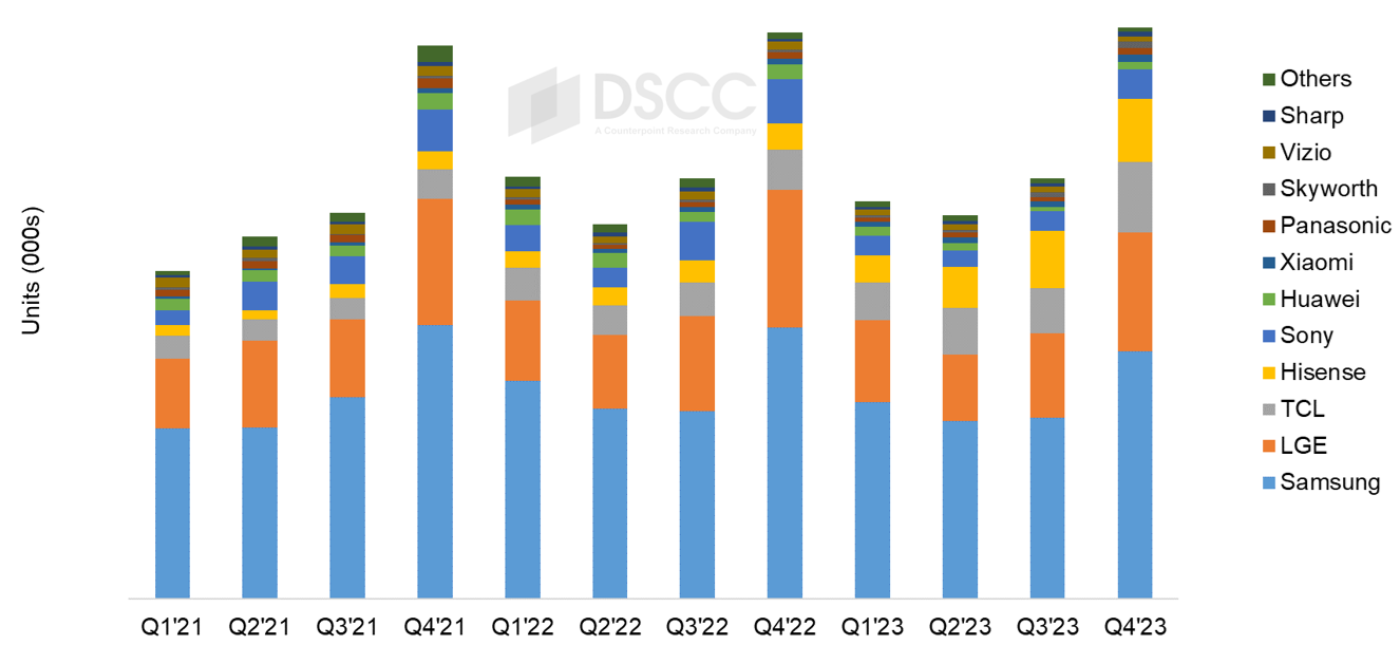

Q4’23のAdvanced (先端技術FPD搭載) TV市場で、TCLとHisenseを筆頭とする中国ブランドがMiniLED LCD TVの積極的な価格設定と販売促進によってシェアを拡大した。DSCCが Quarterly Advanced TV Shipment and Forecast Report 最新版で明らかにしている。中国以外の上位3ブランドであるSamsung、LG、Sonyがいずれも不振だった一方で、TCLとHisenseがプレミアムセグメントでシェアを伸ばした。

Q4’23のAdvanced TV出荷数は前年比1%増の690万台。OLED TVは前年比17%減の190万台、Advanced LCD TVは前年比10%増の500万台だった。Advanced TV出荷額は前年比3%減の76億ドルで8四半期連続の前年比減少となった。OLED TV出荷額は前年比18%減の28億ドルだったが、Advanced LCD TV出荷額は価格下落を上回る台数増加と豊富な製品構成によって前年比9%増の48億ドルとなった。

ブランド間の競争については、Samsungが数量、金額ともに首位を維持したものの、中国のライバルブランドの成長によってシェアは低下した。Q4’23の各ブランドのAdvanced TV出荷実績は以下の通り。

Chinese Brands Gained Share of Advanced TV Market in Q4'23

With aggressive pricing and promotion of MiniLED LCD TVs, Chinese brands led by TCL and Hisense gained share in the Advanced TV market in Q4’23, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report, now available to subscribers. The top three brands outside of China – Samsung, LG and Sony – all fared poorly while TCL and Hisense gained share in the premium segment.

Advanced TV shipments grew 1% Y/Y in Q4’23 to 6.9M units. OLED TV shipments declined 17% Y/Y to 1.9M while Advanced LCD TV shipments increased 10% Y/Y to 5.0M. Advanced TV revenues decreased by 3% Y/Y to $7.6B, the eighth consecutive quarter of Y/Y declines. OLED TV revenues decreased by 18% Y/Y to $2.8B while Advanced LCD TV revenues increased by 9% Y/Y to $4.8B as the increase in units and a richer mix overcame price declines.

In the brand battle, while Samsung maintained the top spot in both units and revenue, it lost ground while its rivals in China gained. In Q4’23, among all Advanced TV products:

- Samsung shipments declined 9% Y/Y to 3.0M units and Samsung unit share decreased by 5% Y/Y. Samsung revenues decreased 5% Y/Y and revenue share declined 1`% to 42%. Samsung continues to lead in MiniLED TV but no longer dominates as Chinese brands are accelerating. Samsung’s MiniLED shipments decreased 34% Y/Y and Samsung’s unit and revenue share declined to 39% and 44%, respectively.

- LG shipments decreased by 14% Y/Y and unit share decreased 3% Y/Y to 21% in Q4’23. LG revenues decreased 22% Y/Y and LG lost 5% share to 24%. LG continues to lead in OLED TV with 52%/50% unit/revenue share, but LG has faltered in MiniLED with only 3% share.

- TCL shipments increased 77% Y/Y and TCL gained share Y/Y from 7% to 12%. TCL revenues increased 71% Y/Y and TCL passed Sony for #3 in revenue share with 11%.

- Hisense also passed Sony to take #4 in both shipments and revenue as shipments increased 135% Y/Y and revenues increased 116% Y/Y.

- Sony shipments declined 33% Y/Y and Sony dropped from #3 to #5 in both unit and revenue share. Sony revenues declined 35% Y/Y.

Advanced TV Shipments by Brand

DSCC’s Quarterly Advanced TV Shipment and Forecast Report includes technical descriptions of all major advanced TV display technologies, plus quarterly shipment results from Q1’18 through Q4’23, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast for five years across technology, region, resolution and size.

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。