2023年のFPD用ガラス需要、中国のシェアが70%超に~専門調査レポートより

出典調査レポート Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

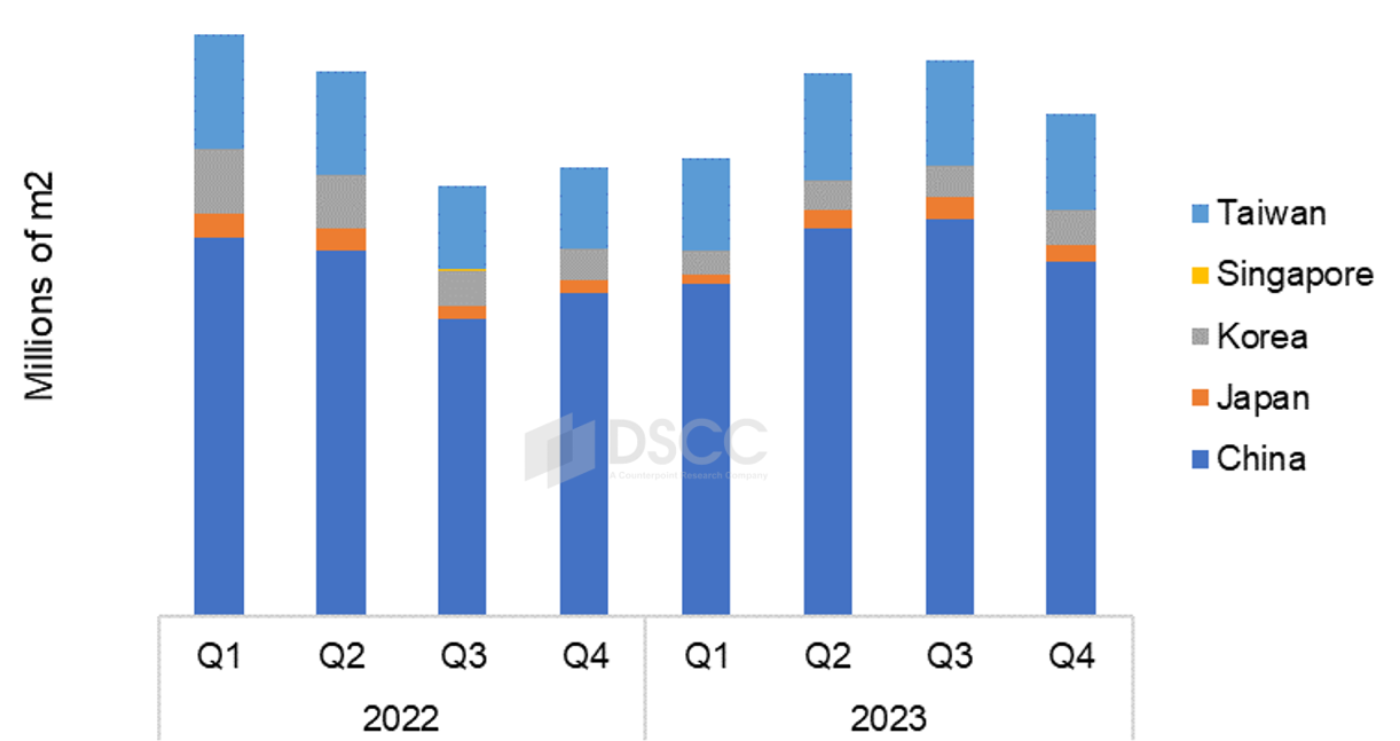

FPD業界では中国が次第に優位性を高めているが、その最たる例がFPD用ガラス市場である。DSCCが先週発表した Display Glass Report 最新版によると、FPD用ガラス需要における中国のシェアは過去最高を記録し、2023年には70%を超えた。

Display Glass Report は、すべてのLCDおよびOLED生産ラインを対象に、主要ガラスメーカー全社のガラス能力と出荷を追跡している。DSCCが誇る、FPD業界の能力と稼働率に関する包括的インサイトと、FPD用ガラスとそのサプライチェーンに関する深い理解を組み合わせたレポートである。レポートでは、FPD用ガラス生産4ヵ国 (日本、中国、台湾、韓国) それぞれの能力を概説するとともに、第1世代から第10.5世代までガラス出荷を追跡している。さらに、FPD業界向けの3大サプライヤーであるCorning、AGC、NEGと、その他のガラスメーカーからのガラス出荷について詳しく解説している。レポートには、FPDメーカー26社を対象とした調達相関図も掲載している。

FPD用ガラス出荷量は2022年の前年比10%減を経て2023年には安定し、前年比2%増を記録した。LCD需要の軟化にともなってガラス出荷はQ4'23に10%減少し、Q1'24には前期比5%減になる見通しだが、その後は年末まで緩やかに回復すると予測されている。

地域別では、中国系FPDメーカーが業界で優位性を高めており、FPD用ガラス市場における韓国の影響力が縮小している。10年前は韓国がガラス需要の最大地域だったが、2018年初めにガラス市場の27%を占めた韓国のシェアはQ1’23にわずか5%という低水準を記録している。世界のFPD用ガラス需要に占める中国のシェアはQ1’18には40%だったが、新規生産能力の増加と韓国の生産能力停止によって、2023年には71%に達したと見られる。

地域別 FPD用ガラス出荷面積

DSCCの Display Glass Report では、すべてのLCDおよびOLED生産ラインを対象に主要ガラスメーカー全社のガラス能力と出荷を追跡しており、地域、FPDメーカー、バックプレーンタイプ、TFT世代サイズなどの項目別にデータ表示可能なピボットテーブルを提供しています。レポートには第1世代から第10.5世代までのa-SiおよびLTPSガラスの価格を収録しており、Q1’19以降の四半期実績とQ2’24までの予測を掲載しています。

出典調査レポート Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] China Share of Display Glass Demand Exceeded 70% in 2023

The display industry has been increasingly dominated by China, and the best example of that dominance is the display glass market. China’s share of display glass demand reached an all-time high and exceeded 70% in 2023, according to the latest update to DSCC’s Display Glass Report, released last week.

The Display Glass Report tracks glass capacity and shipments for all major glass makers across all LCD and OLED display fabs. The report combines DSCC’s comprehensive insight into industry capacity and utilization with an in-depth understanding of display glass and the supply chain. The report outlines capacity by region in each of the four regions of display glass production: Japan, China, Taiwan and Korea, and covers glass shipments in Gen sizes from 1 to 10.5. The report details glass shipments for the three major suppliers to the display industry, Corning, AGC and NEG, along with other glass suppliers. The report includes a supply matrix covering 26 panel makers.

After a 10% Y/Y decline in 2022, display glass shipments stabilized in 2023 and recorded a 2% increase Y/Y in volume terms. Glass shipments declined 10% in Q4’23 as LCD demand softened and are expected to decline another 5% Q/Q in Q1’24 before slowly recovering through the rest of the year.

A view of the market by region demonstrates the increasing dominance of the display industry by China panel makers and the shrinking relevance of Korea in the display glass market. Ten years ago, Korea was the largest region for glass demand, and Korea’s share was 27% at the beginning of 2018 but hit a low point of only 5% of the glass market in Q1’23. China’s portion of worldwide display glass demand, which was only 40% in Q1’18, increased to an estimated 71% in 2023 with growth in new capacity and shutdowns of Korea capacity.

Display Glass Market by Region

DSCC’s Display Glass Report tracks glass capacity and shipments for all major glass makers across all LCD and OLED display fabs, providing pivot tables that allow splits by region, panel maker, backplane type and TFT Gen Size. The report includes prices for a-Si and LTPS glass for Gen Sizes from 1 to 10.5 and includes quarterly history from Q1’19 and a forecast through Q2’24.