FPD製造装置市場予測とメーカーランキングを更新

冒頭部和訳

FPD市況環境の低迷により、大部分のFPDメーカーが新規生産能力の決定を延期している。特に状況が厳しいのがLCDで、TV用LCD価格は限界費用レベルに近づいており、BOE会長が「今後はTV用LCD生産ラインの建設は行わない」と示唆したことから、B17+ラインはキャンセルとなり、DSCC予測からも除外された。LCDの低迷はOLED設備投資にも波及し、OLEDも供給過剰状態にあり大半のOLEDメーカーはLCDも生産しているため、現在損失を出している。例外はSamsung Displayで、iPhone 14 Pro/Pro Max需要が強力であること、またLG Displayが14 Pro Max向け供給資格獲得で課題に直面していることから、Q4’22には (Samsung Displayの) OLED事業の営業利益と営業利益率が記録的水準に達している。

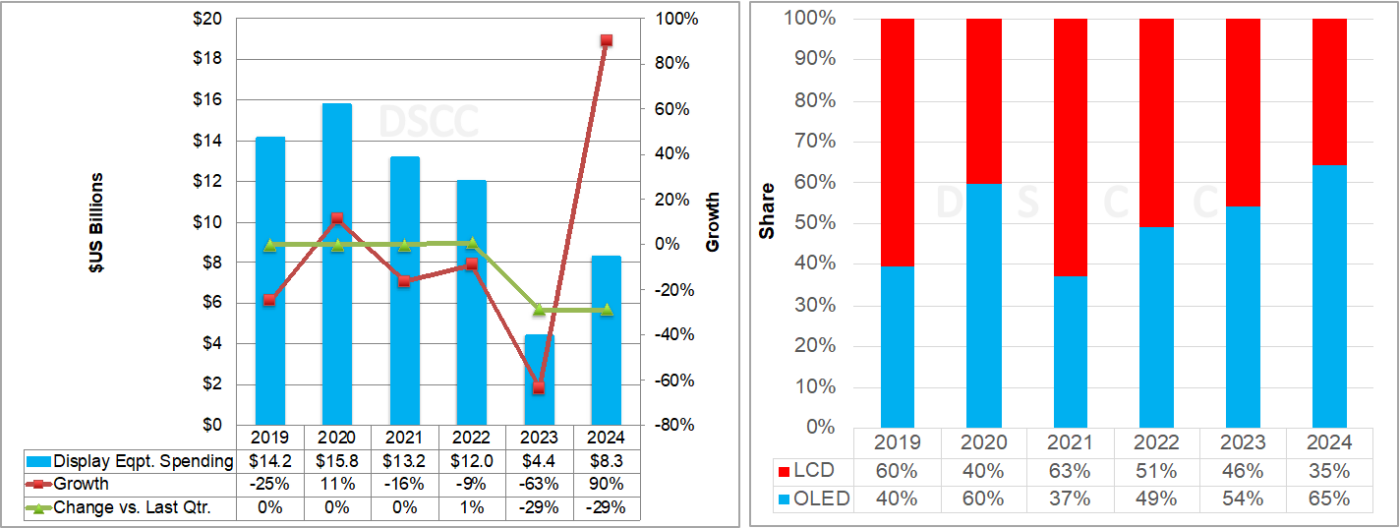

前回予測と比較すると、2020-2025年のFPD設備投資額 (総額) は18%引き下げられた585億ドルとなった。LCD設備投資額は11%引き下げ、これはBOEのB20ライン追加を考慮した結果である。OLED設備投資額は23%引き下げ、その主な要因は延期である。

Display Equipment Spending Cut Significantly as Panel Demand Outlook Remains Weak

Panel suppliers are mostly delaying new capacity decisions given the weak market conditions in the display market. The situation is particularly dire in LCDs where LCD TV panel prices approached marginal cost levels and BOE’s Chairman indicated they won’t build any more LCD TV fabs, resulting in the cancellation of B17+ and its removal from our forecast. The weakness in LCDs also spread to OLED spending since there is an oversupply there also and most OLED manufacturers also produce LCDs and are currently losing money. Samsung Display is the exception as it earned record OLED operating profits and operating margins in Q4’22 helped by strong iPhone 14 Pro/Pro Max demand and LG Display’s challenges getting qualified for the 14 Pro Max.

Relative to our last forecast, we have cut 2020-2025 display equipment spending by 18% to $58.5B. LCD spending was cut by 11% helped by the addition of BOE’s B20 fab. OLED spending was cut by 23% mostly due to delays.

For 2022, DSCC reports display equipment spending will fall 9% to $12.0B with OLEDs up 21% to $5.9B and LCDs down 26% to $6.1B and a 51% to 49% LCD advantage. In 2023, however, we see just $4.4B in spending, down 63%, with SDC delaying one new fab and downsizing another and display revenues expected to continue to shrink. This is the lowest total for display equipment spending since 2012. OLED spending is expected to fall 60% in 2023 with LCD spending down 67% with OLEDs leading by a 54% to 46% advantage. OLED spending is expected to significantly outpace LCD spending from 2023 on, especially as OLED manufacturers target the IT market, which will begin to bear fruit in 2024. DSCC predicts the 2024 market for equipment spending will rise by 90% to $8.3B with OLED spending up 127% and LCD spending up 47% with OLEDs enjoying a 65% to 35% advantage.

DSCC’s Latest Display Equipment Spending Forecast (Delivery Basis)

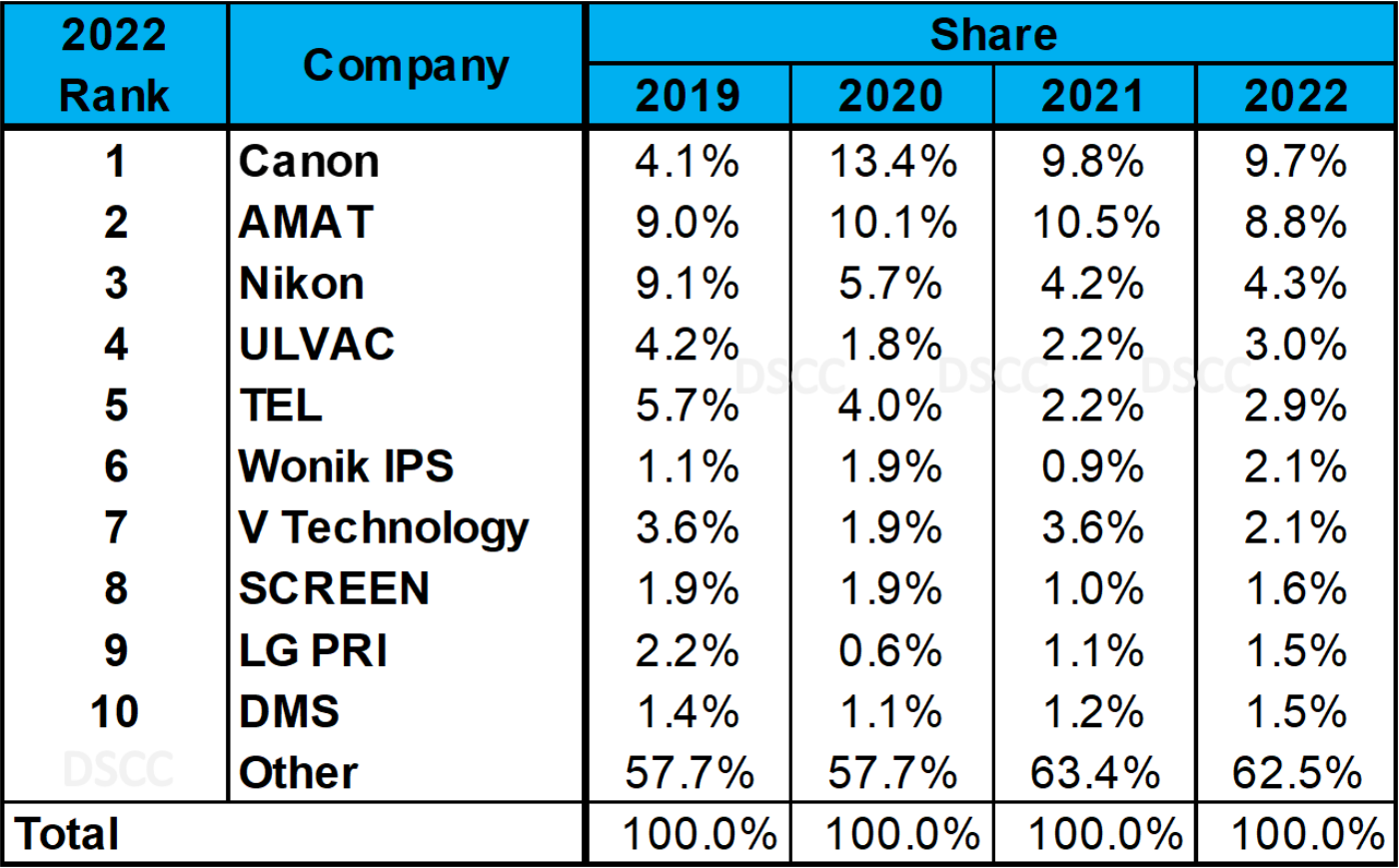

By manufacturer for 2022, we see Canon regaining the top spot in 2022 with AMAT #2. If we separated Canon and Tokki, AMAT would be #1, Canon would be #2 and Tokki would be #4. Nikon remains #3 with a slight share gain on a small litho share gain. ULVAC is expected to rise from #7 to #4 thanks to FMM VTE business at EDO, CVD wins at AUO and LGD and increased ITO/IGZO business offsetting share losses in OLED metal sputtering. TEL is expected to rise from #6 to #5 on LCD & OLED dry etch share gains more than offsetting share losses in coater/developers. Wonik IPS is expected to jump from #14 to #6 on triple digit growth from dry etch wins at t9 and SDC A4. Of the top 25, there were 11 suppliers from Korea, 10 from Japan three from the US and one from China. For market share by segment for 2023 and beyond, please see the latest report.

DSCC’s Display Equipment Spending Share Data (Delivery Basis)

DSCC’s Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします) shows fab schedules, equipment spending by fab and equipment type from 2016-2026. It also reveals key display technology roadmaps. For more information, please contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Display Capex and Equipment Market Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。