Q3'22のAdvanced (先端技術FPD搭載) TV出荷実績

冒頭部和訳

DSCCが発刊した Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) 最新版によると、Q2’22に低迷したAdvanced TV市場では、マクロ経済的事象と地政学的事象が重なって、成長の阻害要因となる状況が継続している。Samsungは出荷数、出荷額ともにシェアが低下し困難な四半期となった一方、同社の3大競合企業であるLG、Sony、TCLはいずれもシェアを拡大した。

本レポートはWOLED、QD-OLED (SamsungではQD Displayと呼称) 、QDEF (SamsungとTCLではQLEDと呼称) 、MicroLED、4Kおよび8K解像度のMiniLEDなどの最先端TV技術を含む、世界のプレミアムTV市場を対象としている。技術、地域、ブランド、解像度、サイズなどの項目ごとに、現在と将来のTV出荷台数と出荷額を調査、これらすべての技術の成長を予測している。Q4’22発行のレポート最新版には、Q3’22の出荷実績と2026年までの最新予測を収録している。本稿ではQ3’22出荷実績を確認する。最新予測の内容については数週間後に別の記事で取り上げて確認する予定だ。

Samsung Lost Ground in Advanced TV Market in Q3’22

After a weak Q2’22, the combination of macroeconomic and geopolitical events continued to hinder growth for the Advanced TV market, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします), now available to subscribers. Samsung struggled through a difficult quarter, losing both unit and revenue share while its three biggest competitors – LG, Sony and TCL – all gained share.

This report covers the worldwide premium TV market, including the most advanced TV technologies: WOLED, QD-OLED (which Samsung calls QD Display), QDEF (which Samsung and TCL call QLED) and MiniLED with 4K and 8K resolution. The report looks at current and future TV shipments and revenues by technology, region, brand, resolution and size, and forecasts the growth of all these technologies. The Q4’22 update includes the shipment results for Q3’22 and an updated forecast out to 2026. In this article, we will review the historical results of Q3’22; in another article in a few weeks, we will review the updated forecast.

We define an “Advanced TV” (capitalized) as any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology. The historical data in the report allows analysis by feature for Advanced LCD TVs. The historical data through 2021 for OLED TV includes only one product configuration, LGD’s White-OLED (WOLED) technology, but in Q1’22 we saw the first volumes for QD-OLED TVs sold by Samsung and Sony and the first sales of MicroLED TVs in very small volumes.

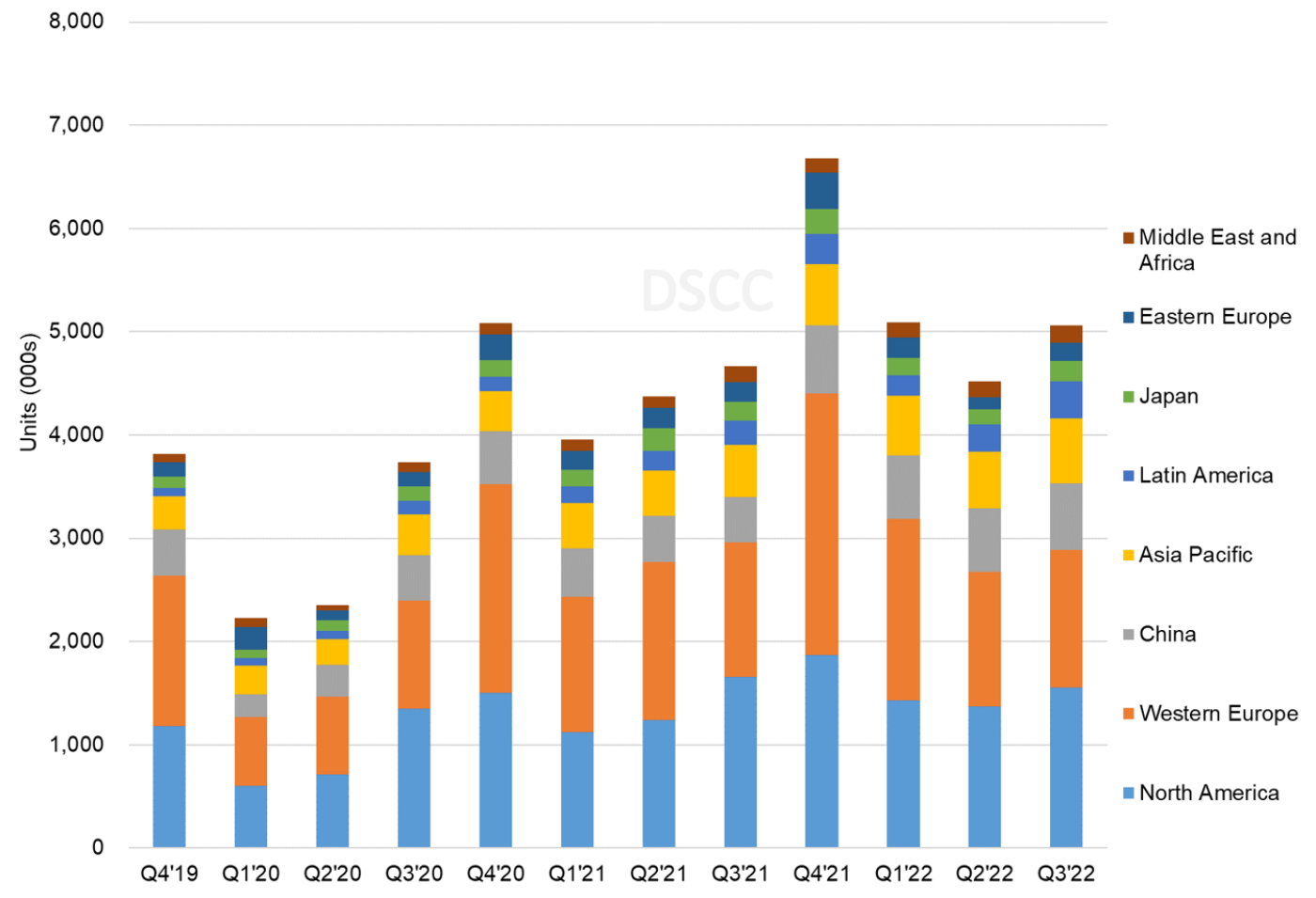

For the second consecutive quarter, the Y/Y growth in Advanced TV shipments in Q3’22 was less than a double-digit %. Advanced TV shipments increased by 8% Y/Y to 5.1M units, as shown in the first chart here of shipments by region. The Russian war in Ukraine continues to affect shipments in Europe. Shipments to Western Europe increased only 2% Y/Y and revenues increased 2% Y/Y. Shipments to Eastern Europe declined by 8% and revenues declined by 13% Y/Y. North America was also a weak spot, with shipments declining 6% Y/Y and revenues declining 11%.

Outside of Europe and NA, Advanced TV shipments continued to increase, with worldwide ex-Europe ex-NA shipments increasing 32% Y/Y and revenues increasing 18% Y/Y. Shipments to China increased by 47% Y/Y and revenues increased 25%. Shipments to Asia Pacific increased 24% Y/Y and revenues increased 11%.

Advanced TV Shipments by Region

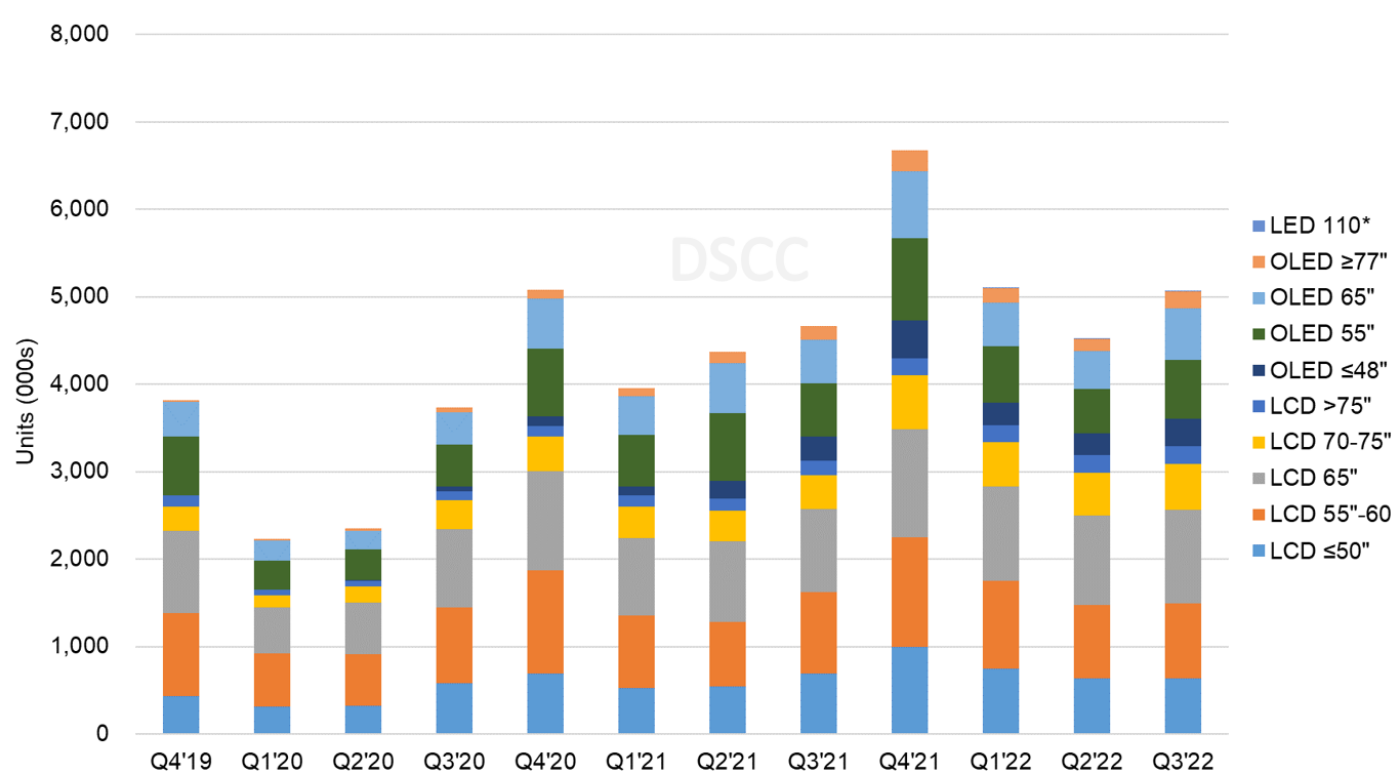

After OLED TV shipments decreased Y/Y for the first time ever in Q2’22, OLED rebounded in Q3 with an increase in shipments of 15% Y/Y as shipments for all screen sizes increased. Advanced LCD TV shipments increased only 5% Y/Y with sizes 55” and smaller decreasing Y/Y while 70” and larger sizes increased. OLED unit share held steady on a Y/Y basis at 33%. Advanced TV revenues increased by only 2% Y/Y. OLED TV revenues increased 14% Y/Y while Advanced LCD TV revenues decreased by 6% Y/Y as growth in units and a richer mix were insufficient to offset price declines.

Advanced TV Shipments by Size and Display Technology

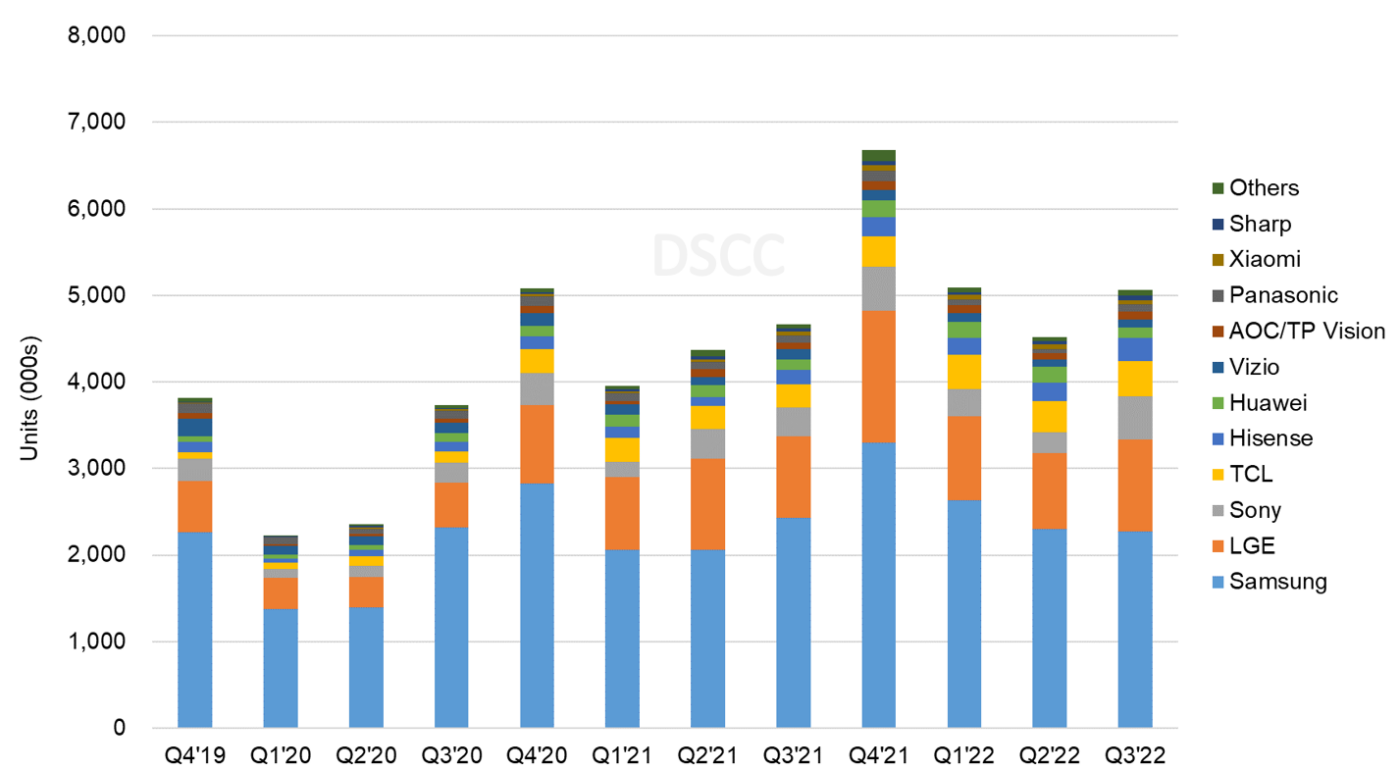

The report’s pivot tables allow an analysis of brand share by screen size, region, technology, resolution and other variables. In the brand battle, while Samsung maintained the top spot in both units and revenue, it lost ground while rivals gained. In Q3’22, among all Advanced TV products:

- Samsung shipments decreased by70% Y/Y and Samsung unit share decreased by 7% Y/Y. Samsung revenues decreased 14% Y/Y and revenue share declined to 37%.

- LG shipments increased by 14% Y/Y and unit share increased from 20% in Q3’21 to 21% in Q3’22. LG revenue increased 10% Y/Y and LG gained share Y/Y to 27%.

- Sony shipments increased 48% Y/Y and Sony increased unit share from 7% to 10%. Sony’s revenue share increased 4 points to 14%.

- TCL shipments increased 56% Y/Y and TCL gained share Y/Y from 6% to 8%. TCL gained one revenue share point to 7%.

Advanced TV Shipments by Brand

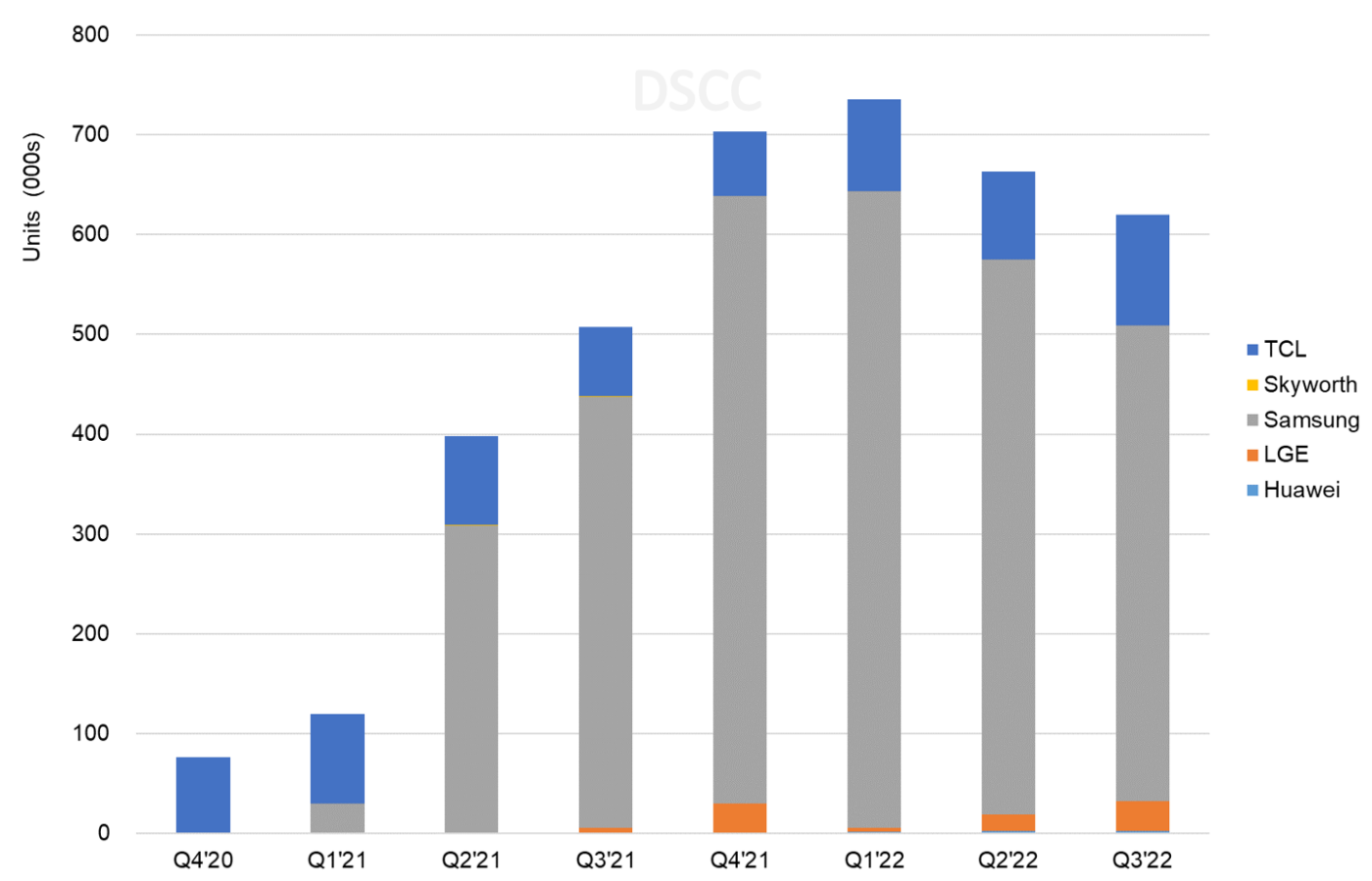

The report tracks the emergence of MiniLED as a competitor to OLED TV in the premium space. The next chart here shows MiniLED TV shipments by brand. While TCL introduced MiniLED in late 2019 and recorded some sales in 2020, the category remained tiny until Samsung and other brands introduced products with MiniLED technology in Q1’21. From less than 100K units in 2020, MiniLED TV shipments grew to more than 1.7M units in 2021, and revenue grew from $73M in 2020 to $3.5B in 2021.

MiniLED TV shipments saw their second consecutive Q/Q decline in Q3’22, and Y/Y growth of shipments slowed to 10%. Samsung continues to dominate this category with 77% unit share and 79% revenue share but slower growth at Samsung meant slower growth for the category overall. MiniLED shipments remained far lower than OLED TV shipments, with 620K units compared to 1.77M units for OLED.

MiniLED TV Shipments by Brand

In North America, Samsung enjoys a dominant position on the strength of its large-screen product portfolio but has seen its share erode as competitors in both Advanced LCD and OLED TV grow share. In Q3’22 Samsung maintained the #1 position but its unit share fell by 11 points Y/Y to 49% and its revenue share fell by nine points to 44%. LG share increased Y/Y by 3 share points in units and by 4 share points in revenue. Sony gained five share points for both unit and revenue share and TCL also gained, but Vizio unit and revenue share continues to erode.

In Western Europe, Samsung maintained the top share but lost share Y/Y in both units and revenue in Q3’22. In units Samsung lost 11 share points Y/Y and in revenues Samsung lost 13 share points Y/Y. LG gained six share points Y/Y in units and seven share points Y/Y in revenue. Sony gained four share points Y/Y in units and five share points Y/Y in revenue.

Panasonic and Philips each maintain a small share with OLED TV models.

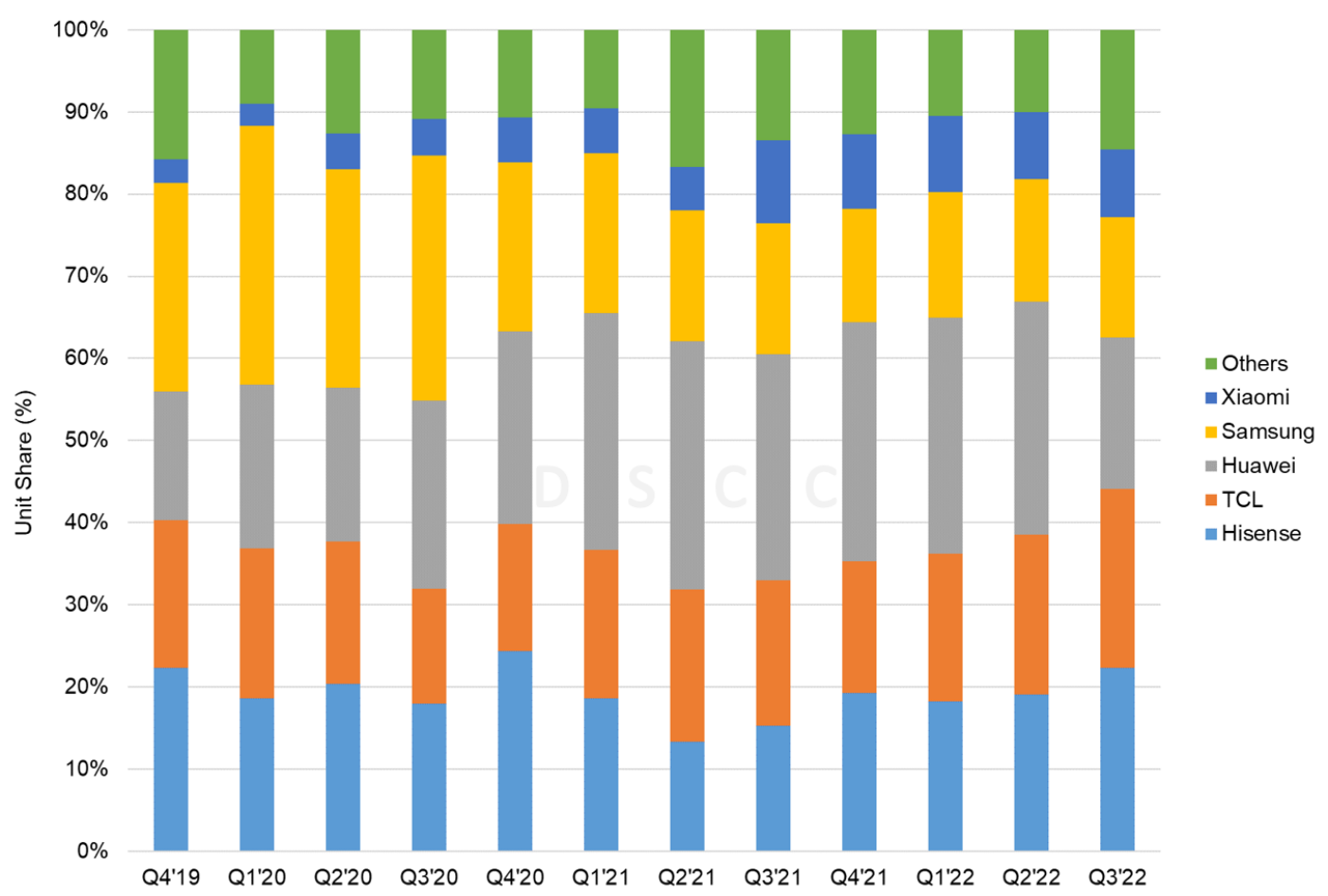

Advanced TV Shipments - China

China remains a true battleground with four companies with double-digit % share in both units and revenues. Hisense jumped past TCL and Huawei to take the top share in units in Q3’22 with 22% share. TCL took the #1 spot in revenue share as revenues increased 23% Y/Y. Huawei share fell as its shipments decreased 2% Y/Y and revenues decreased 4% Y/Y.

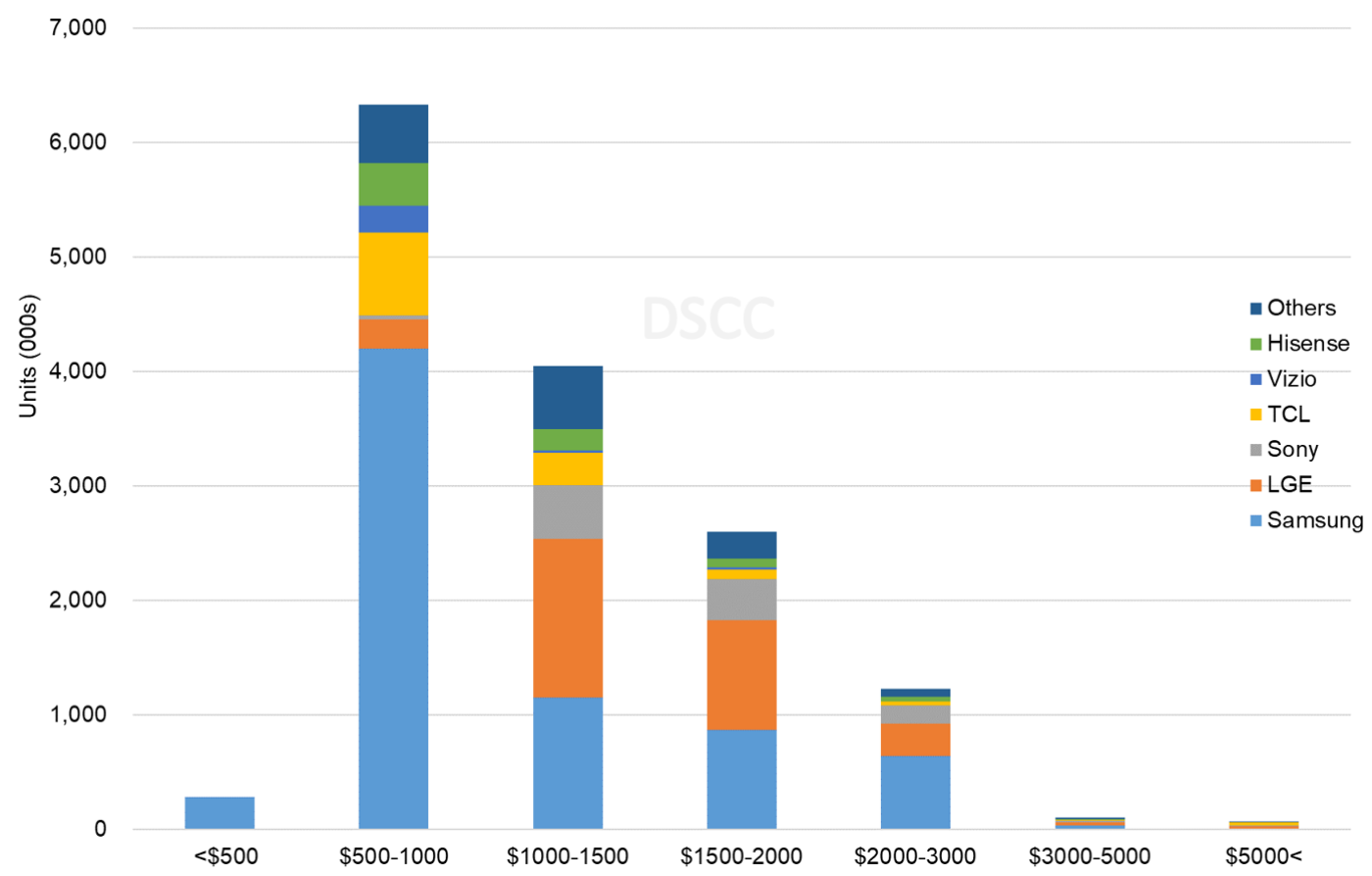

The last chart here shows one last valuable cut of the data, units by brand by price band. The pivot tables allow for this analysis by any time period, and the chart here shows the market by price band for the first three quarters of 2022. The chart shows that Samsung’s leading position in Advanced TV is mostly a function of its dominance in Advanced TVs under $1000. Samsung’s strategy of pushing its QLED product line toward mainstream price points has allowed it to lead, but other brands, especially TCL and Hisense, are increasing their Advanced TV offerings at these lower prices. LG’s OLED TVs give it the leading position in the range of $1000-$2000, and Sony holds a solid #3 position in price points above $1000. Sales volumes at price points over $5000 form only a tiny slice of the market.

Worldwide Advanced TV Units by Price Band for Q1-Q3’22

DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) includes technical descriptions of all major advanced TV display technologies, plus quarterly shipment results from Q1’18 through Q3’22, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast for five years across technology, region, resolution and size. Readers interested in subscribing to the DSCC Advanced TV Shipment Report should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced TV Shipment and Forecast Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。