Apple iPhone 14シリーズのモデル別パネル出荷シェア~Pro用とPro Max用が64%占める

全文和訳

DSCCは Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) 最新刊の「Q3'22実績 速報版」を発行しました。

--------------

DSCCは先週、Appleが発表した、中国・鄭州市にあるFoxconnの生産工場での新型コロナウイルス感染症発生によるiPhone 14 ProおよびiPhone Pro Maxへの一時的な影響に関する通知についての記事を掲載した。

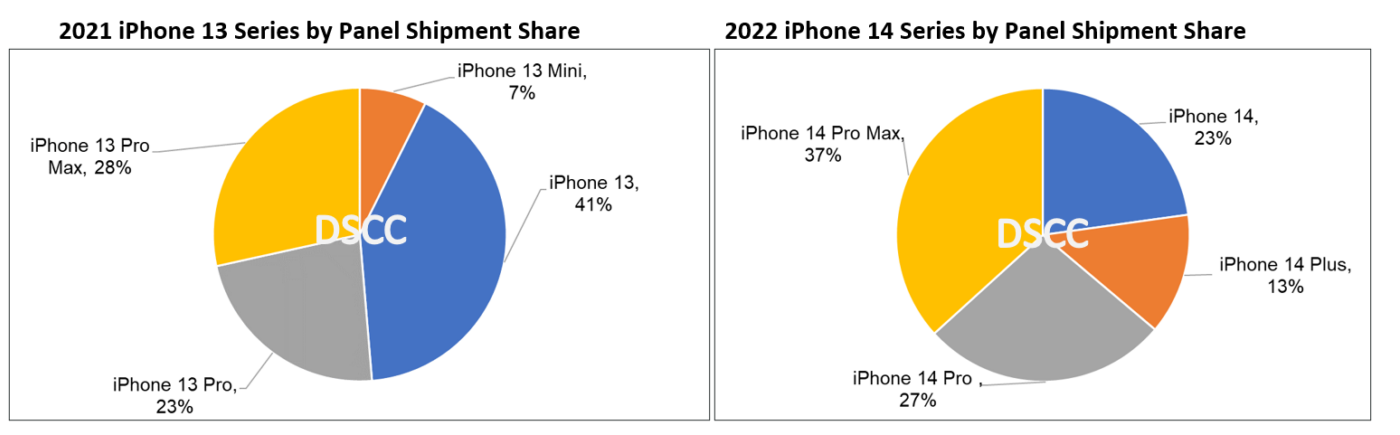

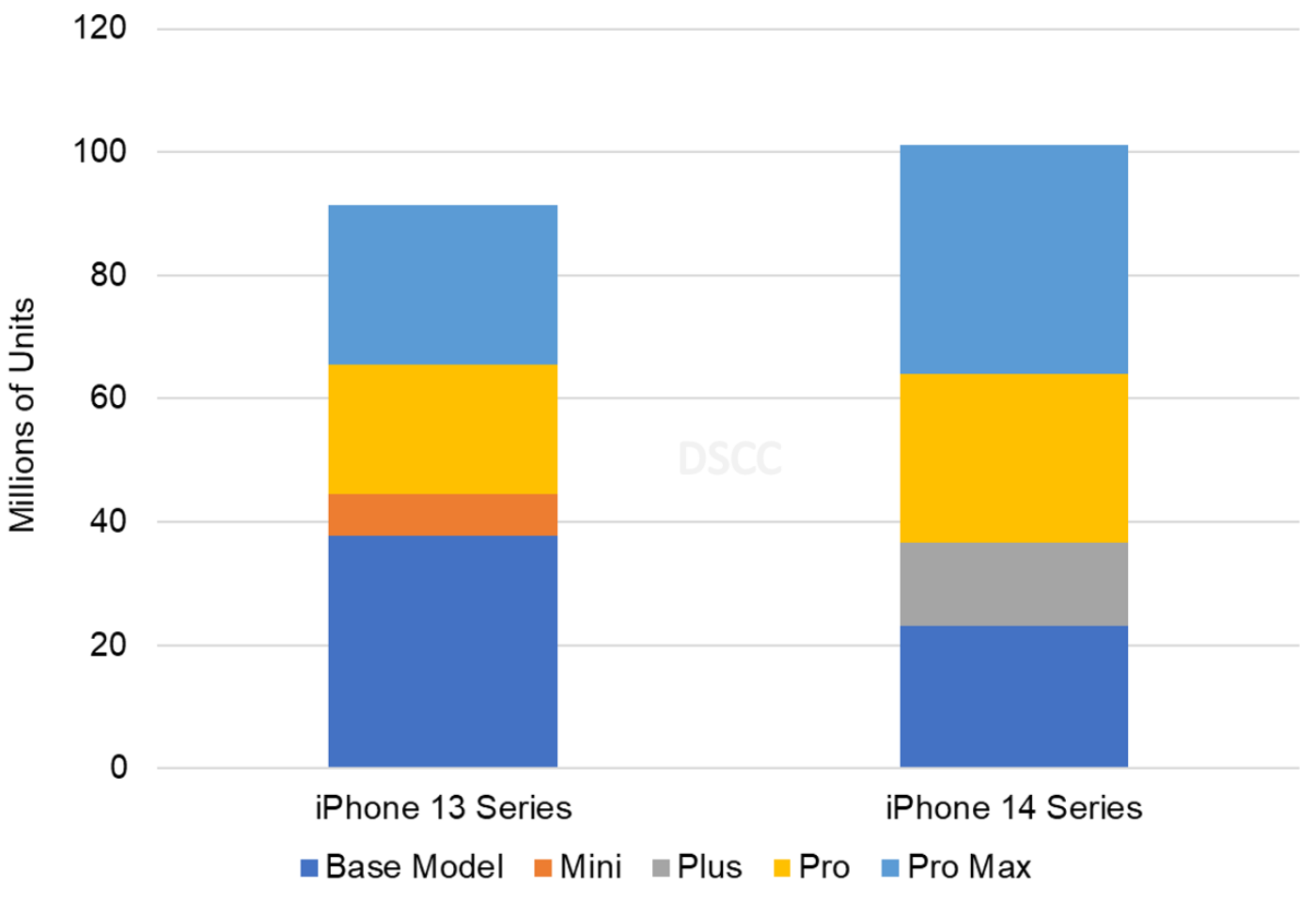

2022年のサプライチェーンソースに関する最新の調査によると、iPhone 14モデル向けパネル出荷枚数は順調に推移し、2021年のiPhone 13モデル向け枚数を超える見通しであることが明らかになった。DSCCが収集した、10月までの実績値と11月および12月の推定値を示す最新データによると、iPhone 14向けパネル出荷枚数は10%増の1億100万枚で、2022年のパネル出荷枚数に対するiPhone 14 ProおよびiPhone 14 Pro Maxのシェアは64%になると予測される。2021年はiPhone 13 ProおよびiPhone 13 Pro Maxのシェアが51%だった。Blended ASP (パネル平均単価) も10%上昇している。2022年のiPhone 14シリーズでもPro Maxが依然としてベストセラーで、同モデル向けパネル出荷枚数は43%増となり、シェアは2021年の28%から37%へと拡大する。

Pro向けのパネル出荷枚数は31%増で、シェアは23%から27%へと拡大する。ベースモデル向けは依然弱く、パネル出荷枚数は39%減で、昨年はiPhone 13のシェアが41%だったのに対し、今年はiPhone 14のシェアが23%へと縮小する。iPhone Plusのシェアは13%、パネル出荷枚数はiPhone 13 Miniに対して100%増となっている。12月のPlus向けパネル出荷枚数は需要停滞のため、ほぼゼロになると見られる。

パネルメーカー別シェアをiPhone 13モデルとiPhone 14モデルで比較すると、SDCのシェアは76%で変わらず、LGDが13シリーズの1モデルに対して14シリーズでは2モデルへの供給を獲得したことを考えればSDCのシェアは予測をかなり上回っているが、これはLGDがPro Max向けパネルサプライヤーの資格獲得に苦戦したことが要因だ。事実、LGDのシェアは13シリーズの21%から14シリーズでは16% に低下している。一方、BOEのシェアは13シリーズの3%から14シリーズでは8%に上昇している。

Apple iPhone 14 Pro and iPhone Pro Max Account for a 64% Share of iPhone 14 Models

Last week, we reported on the warning that Apple issued regarding the temporary impact to the iPhone 14 Pro and iPhone Pro Max as a result of the COVID-19 outbreak at the Foxconn facility in located in Zhengzhou, China.

In our latest survey of our supply chain sources for 2022, we found that panel shipments for the iPhone 14 models are expected to remain on track and exceed the panel shipments for the 2021 iPhone 13 models. Based on the latest data we collected, which represents actuals through October and estimates for November and December, iPhone 14 panel shipments are up 10% to 101M panels. The iPhone 14 Pro and iPhone 14 Pro Max are expected to account for a 64% share in 2022, versus 51% for the iPhone 13 Pro and iPhone 13 Pro Max in 2021. We are also seeing blended ASPs up by 10%. The iPhone 14 Pro Max continues to be the best seller in 2022 accounting for a 37% share of panels shipped, up from 28% in 2021, on a 43% increase in units.

The iPhone 14 Pro share is up from a 23% share to 27% vs. the iPhone 13 Pro with units up 31%. The iPhone 14 continues to show weakness, with its share at 23% versus a 41% share for the iPhone 13 with units down 39%. The iPhone Plus has a 13% share and units are up 100% versus the iPhone 13 Mini. We see Plus panel shipments at near 0 in December as demand stalls.

Comparing panel supplier share between the iPhone 13 models and iPhone 14 models, SDC share remains the same at 76%, much higher than expected given that LGD was awarded supply on two models vs. one model on the 13 Series but LGD struggled to gain qualification on the Pro Max. LGD’s share is actually declining from 21% on the 13 Series to 16% on the 14 Series. BOE’s share is rising from 3% on the iPhone 13 to 8% on the iPhone 14 Series.

iPhone 14 Series vs. 13 Series Panel Shipments Projected Through December

For more information on this content, please contact info@displaysupplychain.com.

本記事の出典調査レポート

Quarterly OLED Shipment Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。