OLED出荷金額、2022年は前年比4%減の見通し~IT用途の成長は鈍化

冒頭部和訳

DSCCは先日発刊の Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) で2022年のOLED出荷金額が前年比4%減の403億ドルになるという予測を明らかにし、その根拠としてモニター、ノートPC、ゲームプラットフォームの成長鈍化と、スマートフォンの前年比マイナス成長の加速を挙げている。

インフレとの闘いに対するマクロ経済の懸念は根強く、インフレ対策の金融政策が実行に移されている。景気後退の可能性、消費者需要の伸び悩み、継続するサプライチェーン問題、商業需要の弱体化、在庫の積み上げといった諸要素のバランスが求められる非常に困難な状況のなか、2022年はスマートフォン、スマートウォッチ、TVの出荷台数と出荷金額が前年比で減少となる見通しだ。2022年の用途別の出荷台数と出荷金額の前年比減少見通しは、以下の通りである。

- OLEDスマートフォン:出荷台数は13%減、出荷金額は5%減

- OLEDスマートウォッチ:出荷台数は12%減、出荷金額は3%減

- OLED TV:出荷台数は4%減、出荷金額は10%減

OLED Panel Revenues Expected to Decline 4% Y/Y in 2022 - Slower Growth for IT Applications

In the recently released Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします), we reveal that 2022 OLED panel revenues are expected to decrease 4% Y/Y to $40.3B as a result of slower growth for monitors, notebook PCs and game platforms combined with faster Y/Y declines for smartphones.

As macroeconomic concerns persist for battling inflation, monetary policies are enacted to combat it. While balancing a possible recession, weakened consumer demand, persistent supply chain issues, softening commercial demand and inventory buildup have created the perfect storm for Y/Y unit and revenue declines for smartphones, smartwatches and TVs in 2022. In 2022, by application, we expect Y/Y unit and panel revenue declines for the following:

- OLED smartphones: 13% Y/Y unit and 5% panel revenue decreases;

- OLED smartwatches: 12% Y/Y unit and 3% Y/Y panel revenue decreases;

- OLED TVs: 4% Y/Y unit and 10% Y/Y panel revenue decreases.

Although emerging applications have slower growth as a result of the aforementioned macroeconomic issues, we still expect positive Y/Y unit increases and Y/Y revenue growth with the exception of notebook PCs.

- OLED notebook PCs: 10% Y/Y unit growth and 5% Y/Y panel revenue decline;

- OLED monitors: 582% Y/Y unit growth and 251% panel revenue growth;

- OLED tablets: 32% Y/Y unit growth and 31% Y/Y panel revenue growth;

- OLED game platforms: 70% Y/Y unit growth and 65% Y/Y panel revenue growth;

- OLED automotive: 105% Y/Y unit growth and 96% Y/Y panel revenue growth;

- OLED AR/VR: although this application has <1% revenue share, this application is expected to have over 2500% Y/Y panel revenue growth as result of development and product efforts by Sony, Meta and others.

For OLED monitors, we expect 2022 revenue of $200M from $57M in 2021. The 42”, 45” and 48” WOLED monitors are expected to account for a 38% revenue share, while QD-OLED monitors are expected to account for a 32% revenue share.

For OLED notebook PCs, we expect 2022 panel revenue of $613M in 2022, down from $646M in 2021 on gains of 6.1M units from 5.5M units in 2021. Our long term forecast for OLED notebook PCs remains robust as a result of new G8.7 OLED fabs capacity coming online in 2024 that will target IT applications.

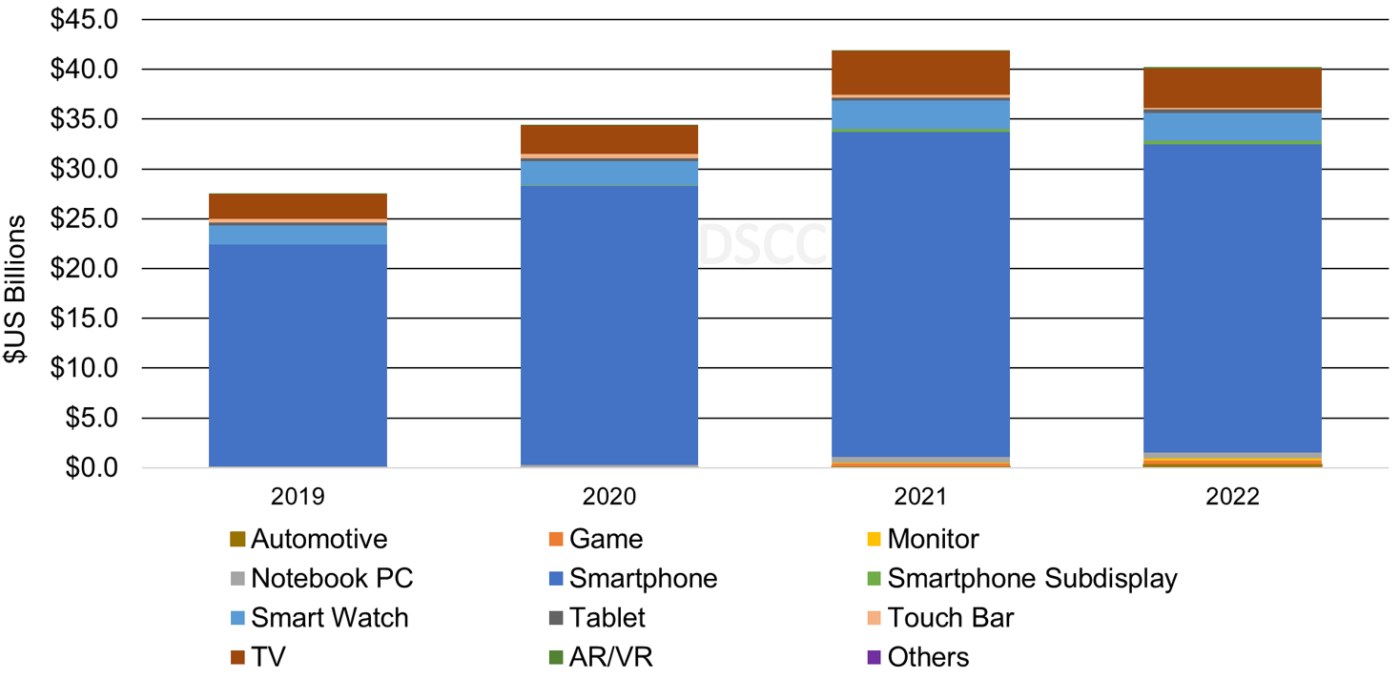

In 2022, smartphones are expected to remain the dominant application with a 75% unit and 77% revenue share, down from 77% unit share and 78% revenue share in 2021 as a result of gains from other applications. In 2023, we expect smartphone unit share to decline to a 74% unit share and 73% revenue share as a result of gains from monitors, notebook PCs, tablets, automotive and AR/VR. In 2025, Smartwatches are the #2 application in 2022 with a 17% unit share and 7% revenue share. On a panel revenue basis, OLED TVs are the #1 application with a 10% revenue share. On a panel revenue basis, we expect notebook PCs to overtake smartwatches for the #2 application with a 6% revenue share and $3B in panel revenue.

Annual OLED Panel Revenue by Application

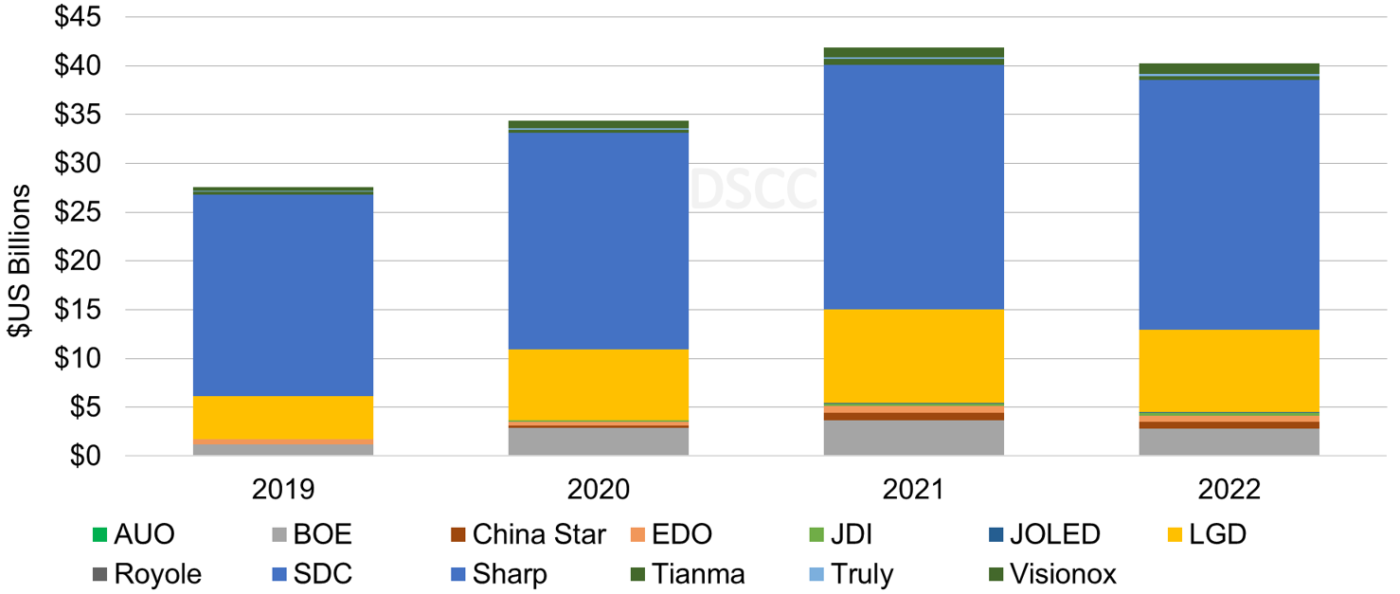

In 2022 by panel supplier:

We expect SDC’s panel revenue share to increase to 63%, up from 60% in 2021, as a result of 10% Y/Y gains from notebook PCs, 25% Y/Y gains from tablets, and 70% Y/Y gains from game platforms, SDC is the only panel supplier providing all four iPhone 14 panels to Apple. We expect SDC to account for a 75% unit share and 80% panel revenue share of the iPhone 14 series volume in 2022. For OLED TVs, SDC is expected to have a 11% revenue share as a result of its 55” and 65” QD-OLED TVs.

We expect LGD’s revenue share to fall slightly from 23% to 21%. LGD is a panel supplier for the iPhone 14 and in Q3’22 became a panel supplier for the iPhone 14 Pro Max. we expect LGD to account for 18% of the iPhone 14 series volume in 2022. LGD is also a key panel supplier for the growth areas of monitor and automotive applications. For monitors, LGD is expected to have a 50% unit share and 42% revenue share. For OLED TVs, LGD is expected to have a 91% unit share and 89% revenue share.

We expect BOE to be the #3 panel supplier with a 7% revenue share in 2022, down from 9% in 2021. The decline in panel revenue share is the result of a 6% Y/Y unit decline for smartphones and 47% Y/Y decline for smartwatches. For smartphones, BOE is also a panel supplier for the iPhone 14 and have 7% of the volume in 2022.

Annual OLED Panel Revenue by Panel Supplier

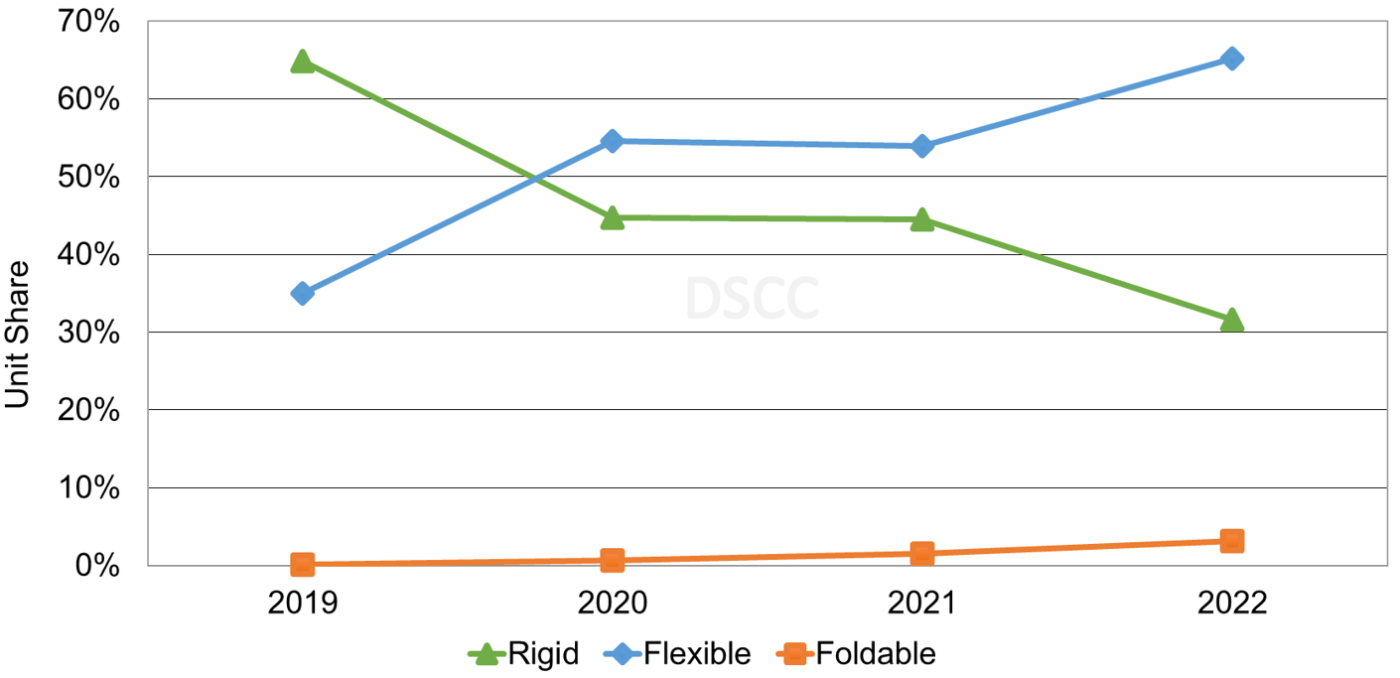

For OLED smartphones by panel shipments, we expect a 13% Y/Y decrease to 554M units. This decrease is the result of a 38% Y/Y decline for rigid OLED and slower growth for flexible OLED panels. Foldable OLED smartphone panels are expected to increase 77% Y/Y, followed by flexible OLED smartphone panels up 6% Y/Y. In 2022, we expect rigid OLED smartphone panels to have a 32% unit share, down from 45% in 2021 and a 13% revenue share, down from 20% in 2021. For flexible OLED smartphone panels, we expect a 65% unit share, up from 54% in 2021 and a 79% revenue share, up from 75% in 2021. For foldable OLED smartphone panels, we expect a 3% unit share, up from 2% in 2021 and an 8% revenue share, up from 5% in 2021.

Annual OLED Smartphone Panel Share by Substrate Forecast

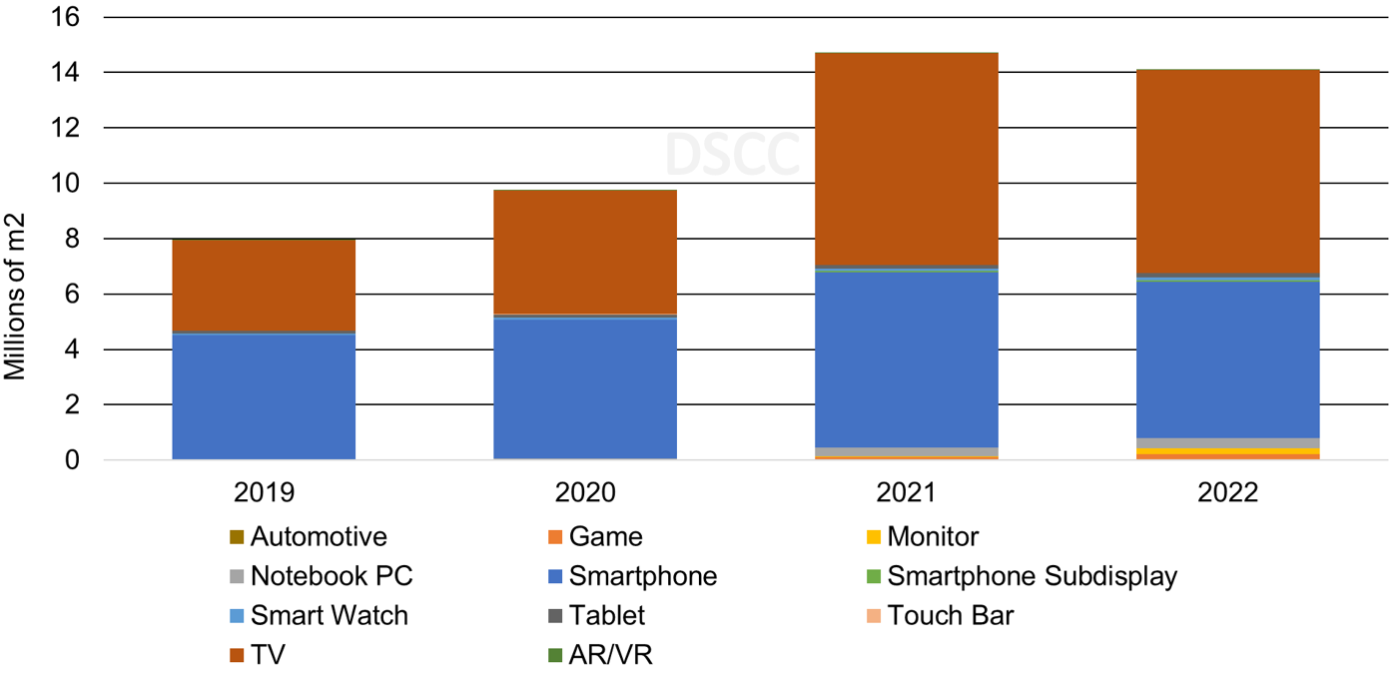

On an area basis, OLED TVs are expected to remain with a 52% area share in 2022 as a result of gains from 55” and 65”

QD-OLED TV and gains from 55”, 65”, 77”, 88” and 97” WOLED TVs. We expect notebook PCs to grow share from a 2% area share in 2021 to 3% in 2022 and increase to a 10% area share in 2026 as new G8.7 IT OLED fabs come online. Excluding OLED TVs, OLED smartphones have an 83% area share, down from 90% in 2021 on gains from notebook PCs, monitors, tablets, game platforms and automotive.

Annual OLED Area by Application

Readers interested in subscribing to the Quarterly OLED Shipment Report (一部実データ付きサンプルをお送りします) should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly OLED Shipment Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。