Advanced (先端技術FPD搭載) タブレット市場~Q2’22実績はQ2’21以来最低水準ながら、市場は依然好調

冒頭部和訳

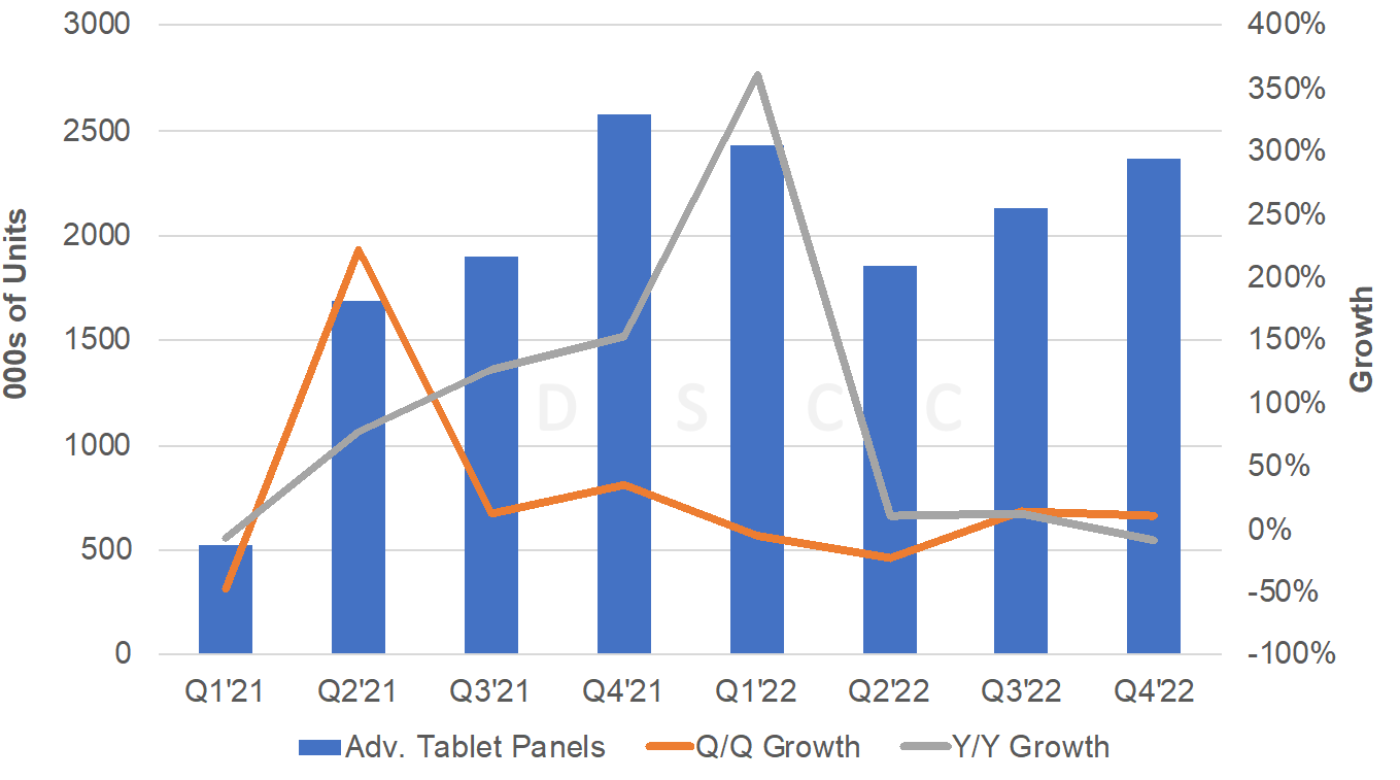

Q2'22のAdvancedタブレット用OLED及びMiniLEDの出荷台数は前期比23%減、前年比10%増の190万台だった。iPad Proの現行モデルの販売期間が長期化し、Q4'22のリフレッシュに向けた準備が進められるなか、Advancedタブレット用FPDの出荷台数はQ1'22以降で最も低い水準となった。Q3'22には、500ドル以下が見込まれるOLED搭載Huawei Mate Pad Pro 11インチの発売と、10月発売が見込まれる新モデルの12.9インチApple iPad Proの伸びにより、前期比14%増、前年比12%増の210万台に回復すると予測される。FPD出荷は年間ベースで31%増の880万台という健全な成長を示し、当社予測を8%上回るものと見られるが、これは主に11インチのHuawei Mate Pad Pro 2022が当初予測を上回る優れた実績を示す見通しによる。こうしたAdvancedタブレット市場の動向は、タブレット用LED LCDの出荷台数が14%減少し、2022年には13%減の1億9500万台が予測されるタブレット市場全体の動向とは対照的だ。タブレット用OLED出荷台数は32%増の370万台、MiniLED LCD出荷台数は31%増の510万台になると予測される。MiniLEDは2021年と同じく2022年もシェア58%を獲得し、シェア42%のOLEDに対する優位性を維持するはずである。タブレット市場全体に対するAdvancedタブレット用FPDのシェアは台数ベースで、2021年の3.0%から2022年には4.5%に上昇すると予測される。金額ベースでは、Advancedタブレットのシェアは2021年の14%から2022年には24%に上昇し、出荷金額は23%増の19億ドルになると見られる。Appleが採用するMiniLEDが高価格なことから、MiniLEDがシェア79%を得て、シェア21%のOLEDに対する大きな優位性を維持するものと見られる。

Advanced Tablets Still Performing Well Although Q2’22 Was Lowest Quarter Since Q2’21

Advanced Tablet (OLED and MiniLED) panel shipments fell 23% Q/Q while rising 10% Y/Y in Q2’22 to 1.9M units. It was the lowest quarter since Q2’21 as the iPad Pro is getting long in the tooth, ready for a refresh in Q4’22. Q3’22 is expected to rebound to 2.1M units, up 14% Q/Q and 12% Y/Y helped by the launch of the ~$500 OLED Huawei Mate Pad Pro 11” and the ramp of a new 12.9” Apple iPad Pro expected to launch in October. On an annual basis, we show a healthy 31% growth to 8.8M panels, 8% higher than our forecast, which is mostly due to the 11” Huawei Mate Pad Pro 2022 expected to perform better than previously expected. This contrasts with the total tablet market which is expected to fall 13% in 2022 to 195M panels with LED LCD tablet panels down 14%. OLED tablet panels are expected to rise 32% to 3.7M with MiniLED LCD panels rising 31% to 5.1M. MiniLEDs should maintain a 58% to 42% unit share advantage in 2022, same share as in 2021. Advanced Tablet panels are expected to account for a 4.5% share of the total tablet market on a unit basis in 2022, up from 3.0% in 2021. On a revenue basis, the Advanced Tablet share is expected to rise from 14% in 2021 to 24% in 2022 on 23% growth to $1.9B. MiniLEDs to maintain a large advantage over OLEDs, 79% to 21% on the high price of Apple’s MiniLED panels.

Advanced Tablet Panel Market

In Q2’22, OLEDs overtook MiniLEDs in the Advanced Tablet market due to the slowdown in MiniLED iPad Pro volumes earning a 60% to 40% advantage, their first lead since Q1’21. However, with a new iPad Pro expected to launch in October, MiniLED panels should resume leadership in Q3’22 and Q4’22 with at least a 66% share each quarter. MiniLEDs maintained an advantage in Q2’22 on a revenue basis despite 40% of volumes on their higher prices.

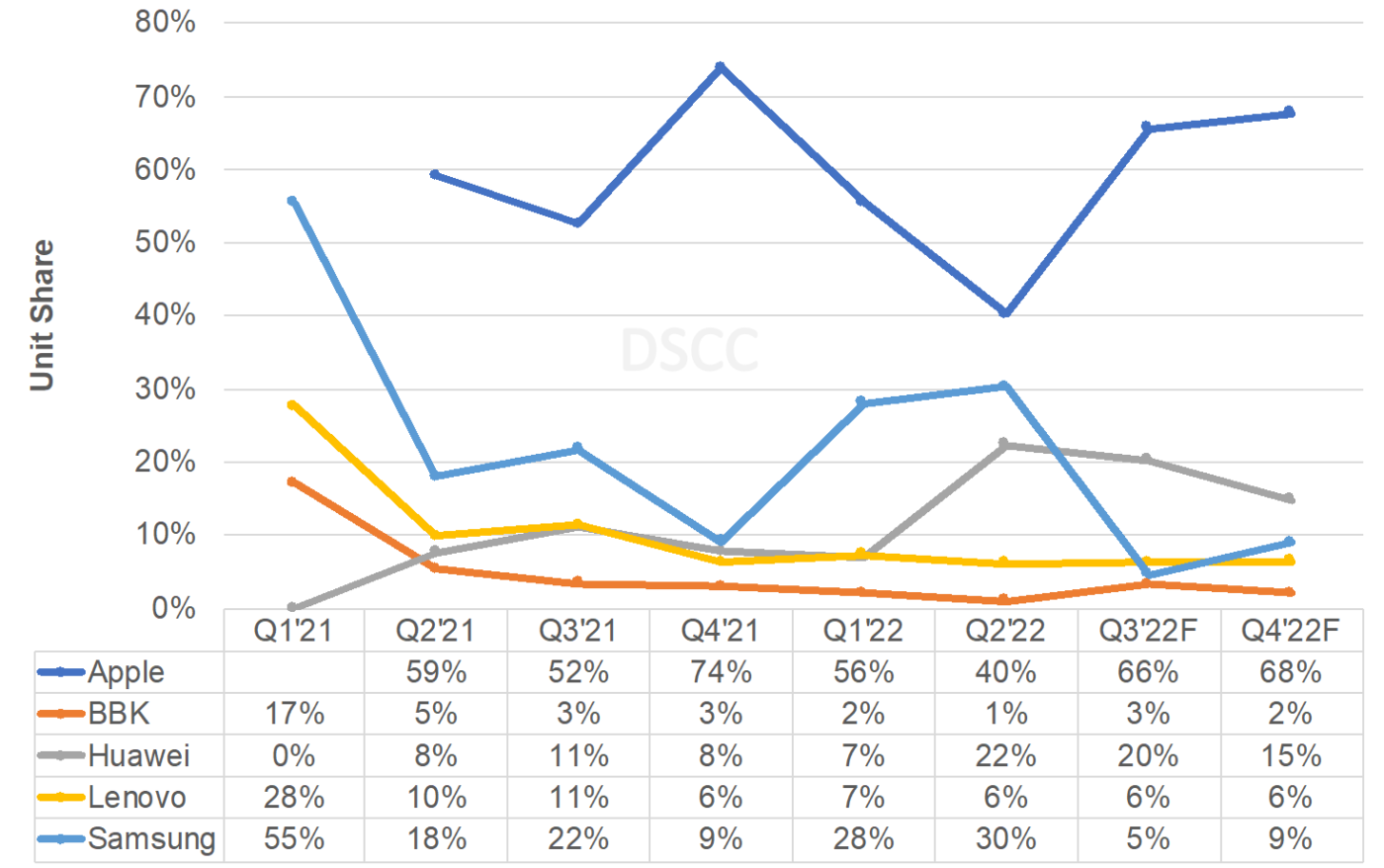

In terms of brand share:

- Apple’s share of Advanced Tablet panel procurement fell from 56% in Q1’22 to 40% in Q2’22 as it is due for a refresh in Q4’22 and volumes are shrinking. Its share should rebound to 66% in Q3’22 as it ramps production ahead of the expected October launch.

- Huawei’s panel procurement share surged from 7% in Q1’22 to 22% in Q2’22 as it ramped production ahead of the launch of the 11” Mate Pad Pro in July. It should maintain a high share of 20% in Q3’22.

- Samsung’s share grew slightly from 28% to 30% despite volume down 17%. Samsung is expected to lose significant share in 2H’22 on no new products launched.

- For all of 2022, Apple is expected to maintain a 58% share with their 2022 volumes upgraded by 3% vs. last quarter.

- Samsung’s volumes were downgraded by 10% to 1.6M for 2022 and their share is expected to fall slightly from 18% in 2021 to 18% in 2022.

- Huawei’s 2022 volumes were significantly upgraded on the strong outlook for the 11” Mate Pad Pro enabling their share to double from 8% to 16% in 2022.

- By model:

- The MiniLED iPad Pro is expected to lead each quarter. In Q2’22 it had a 40% share of panel procurement followed by the Samsung S8+ with a 15% share and the Samsung S8 Ultra and the Huawei Mate Pad Pro 2022 with a 14% share each.

- In Q3’22, the current iPad Pro is expected to lead with a 38% share of panel procurement followed by the new iPad Pro with a 28% share and the Mate Pad Pro 2022 with a 14% share as Samsung’s models sink.

Advanced Tablet Brand Share (Panel Procurement Basis) Including Forecasts for Q3’22 and Q4’22

- By panel supplier:

- In Q2’22, the market was closely divided on a unit basis with SDC earning a 30% share, EDO 29% and LGD 27%.

- In Q3’22, LGD is expected to have a commanding 56% share followed by EDO at 30% with Sharp falling to 9% and SDC’s share falling to 5%. In Q4’22, LGD’s share should surge to 59% on higher iPad Pro volumes with SDC rebounding to 9% and EDO and Sharp losing share.

- For all of 2022, LGD is expected to lead with a 46% share, up from 39%, followed by EDO at 24%, up from 23%, with SDC falling from 19% to 18% and Sharp falling from 19% to 13%.

- On a $US basis, given the higher prices of the MiniLED panels, LGD and Sharp’s shares are even higher with LGD expected to earn a 75% share in Q4’22, up from 43% in Q2’22. For all of 2022, LGD is expected to lead with a 62% share followed by Sharp at 17%, SDC at 11% and EDO at 10%.

- In regard to Advanced Tablet processors:

- Qualcomm led the Advanced Tablet market with a 51% share in Q2’22 followed by Apple at 40%.

- Apple should lead with more than a 2X advantage over Qualcomm in Q3’22 and Q4’22, however.

- In Q2’22, the Apple M1 led with a 40% share followed by the Snapdragon 8 Gen 1 with a 29% share. The Snapdragon 888 was the #3 chipset with a 14% share. In Q3’22. the M1 should lead followed by the M2 and the Snapdragon 888.

For more insights on the tablet market out to 2026 including volumes by refresh rate, backplane, number of cameras, stylus support, etc. as well as the Advanced Notebook and Advanced Monitor markets, please see our Quarterly Advanced IT Display Shipment and Technology Report (一部実データ付きサンプルをお送りします) or contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced IT Display Shipment and Technology Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。