2023年も引き続くLCD供給過剰

[田村喜男] 解説動画を進呈します [8月特別企画]

DSCC Japanのメルマガ読者様 (ご登録はこちらから) 向け企画として、アジア代表・田村喜男が「2022年のFPD工場稼働率」及び「2023年のFPD工場稼働率」を詳細解説した動画 (各20分間※再生速度変更可) を無料提供します。ご希望者様はご所属情報をご明記の上、info@displaysupplychain.co.jp 宛に「稼働率動画希望」とメールしてください。翌日中に動画URLをメール返信します。ご応募をお待ちしています。

冒頭部和訳

DSCCが先週発行した Quarterly FPD Supply/Demand Report (一部実データ付きサンプルをお送りします) 最新版によると、FPD業界における現在の供給過剰状態は2023年を通して継続し、その後ゆっくりと修正されていく見通しだ。このレポートの需要パートについては先週の記事で取り上げたが、今週は供給予測とその結果である需給バランスについて解説する。

LCDとOLEDの両技術とも供給過剰が予測されるが、本稿ではLCDの需給状況に焦点を当てる。Quarterly FPD Supply/Demand Report はLCDとOLEDの両技術を対象としているが、OLEDの需給については、DSCCの Quarterly OLED Supply/Demand and Capital Spending Report (一部実データ付きサンプルをお送りします) を取り上げた別の記事で解説している。

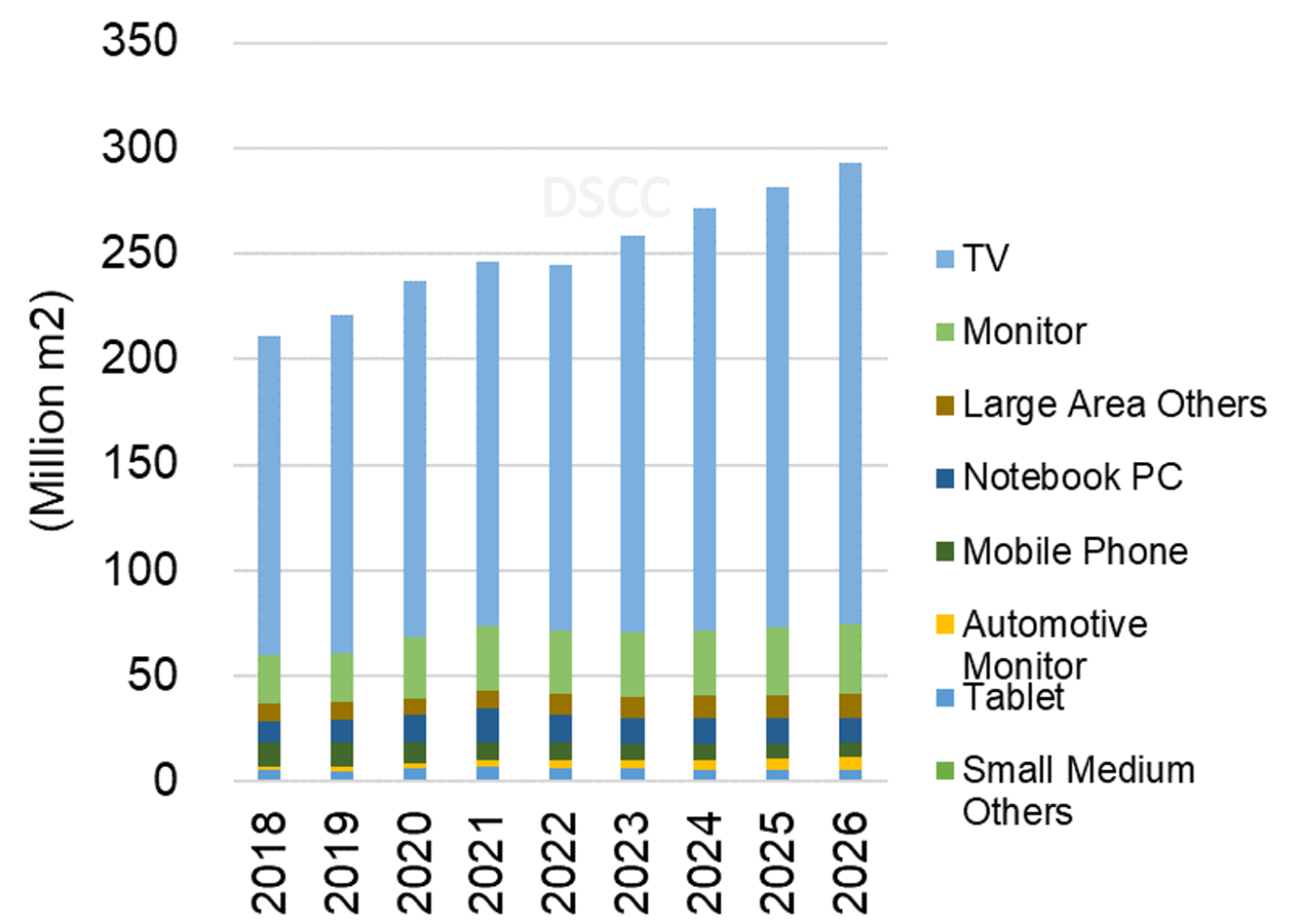

まず需要予測の要約だが、1つ目のグラフはアプリケーション別LCD需要予測 (面積ベース) を示している。面積ベースの需要は2020年に前年比7%増、2021年に4%増となったが、2022年には0.7%減となる見通しだ。TV台数の緩やかな回復とTV画面サイズの大型化の継続により、2023年には6%増の堅調な成長が見込まれている。

LCD Oversupply Will Persist Through 2023

The current oversupply in the flat panel display industry will persist throughout the full year 2023 and will slowly correct thereafter, according to the latest update of DSCC's Quarterly FPD Supply/Demand Report (一部実データ付きサンプルをお送りします), updated last week. We covered the demand portion of this report in an article last week, and this week we will describe our supply forecast and the resulting supply/demand balance.

Although we expect oversupply in both LCD and OLED, for this article we will focus on the LCD Supply/Demand picture. The Quarterly FPD Supply/Demand Report covers both LCD and OLED, but we have described OLED Supply/Demand in a separate article addressing DSCC’s Quarterly OLED Supply/Demand and Capital Spending Report (一部実データ付きサンプルをお送りします).

To quickly recap the demand forecast, the first chart here shows our forecast for LCD demand area by application. Area demand grew by 7% in 2020 and by 4% in 2021 but is expected to be down 0.7% Y/Y in 2022. We expect a solid 6% growth in 2023 based on a modest recovery in TV units and continued growth in TV screen size.

LCD Demand Area by Application

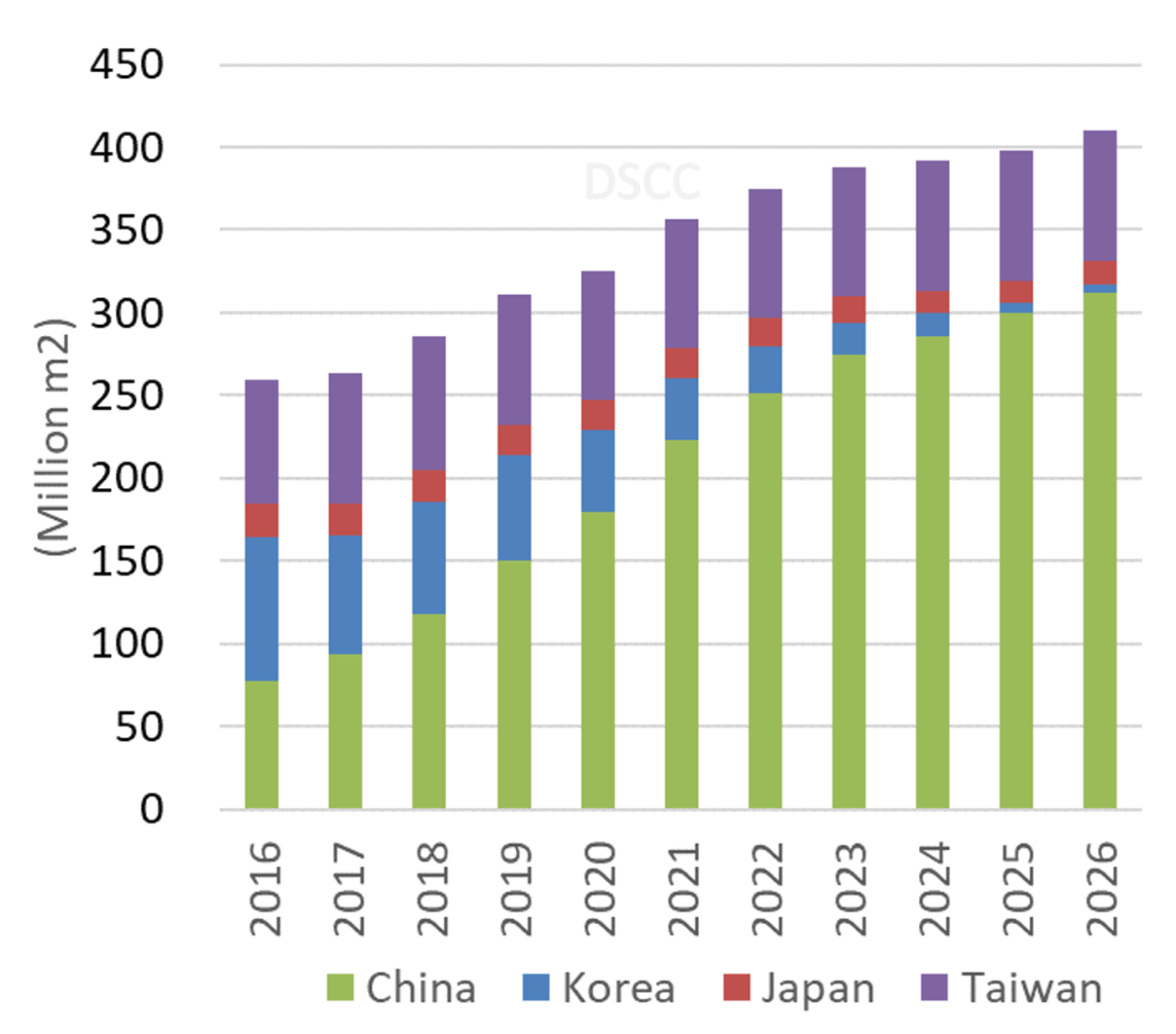

The next chart shows our outlook for LCD capacity, demonstrating the continued strong growth of LCD capacity based on expansions planned during the pandemic-fed surge in 2021. Although new investments in LCD will be greatly diminished after this year, the expansions in Gen 8.x and Gen 10.5 capacity which were planned when LCD panel prices were high are still expected to be put into production. Therefore, even though LCD capacity in Korea will be falling during the forecast period, the expansions in China will continue to push overall industry capacity higher.

LCD capacity increased 10% Y/Y in 2021 and another 5% in 2022 even after the mid-year closure of SDC’s last LCD production line. Capacity is forecast to grow another 3% in 2023 despite the expected closure of LG Display’s P7 line. Although demand growth of 7% in 2023 is higher than supply growth, the recovery does not make up enough ground to justify high utilization.

LCD Area Capacity by Region

As the chart indicates, the LCD industry is increasingly dominated by China. While China represented only 30% of worldwide LCD capacity in 2016, it passed Korea to become the largest region in 2017 and passed 50% of the industry in 2020. In 2022 we estimate that China represents 67% of industry LCD capacity, and the China share is increasing to 76% in 2026.

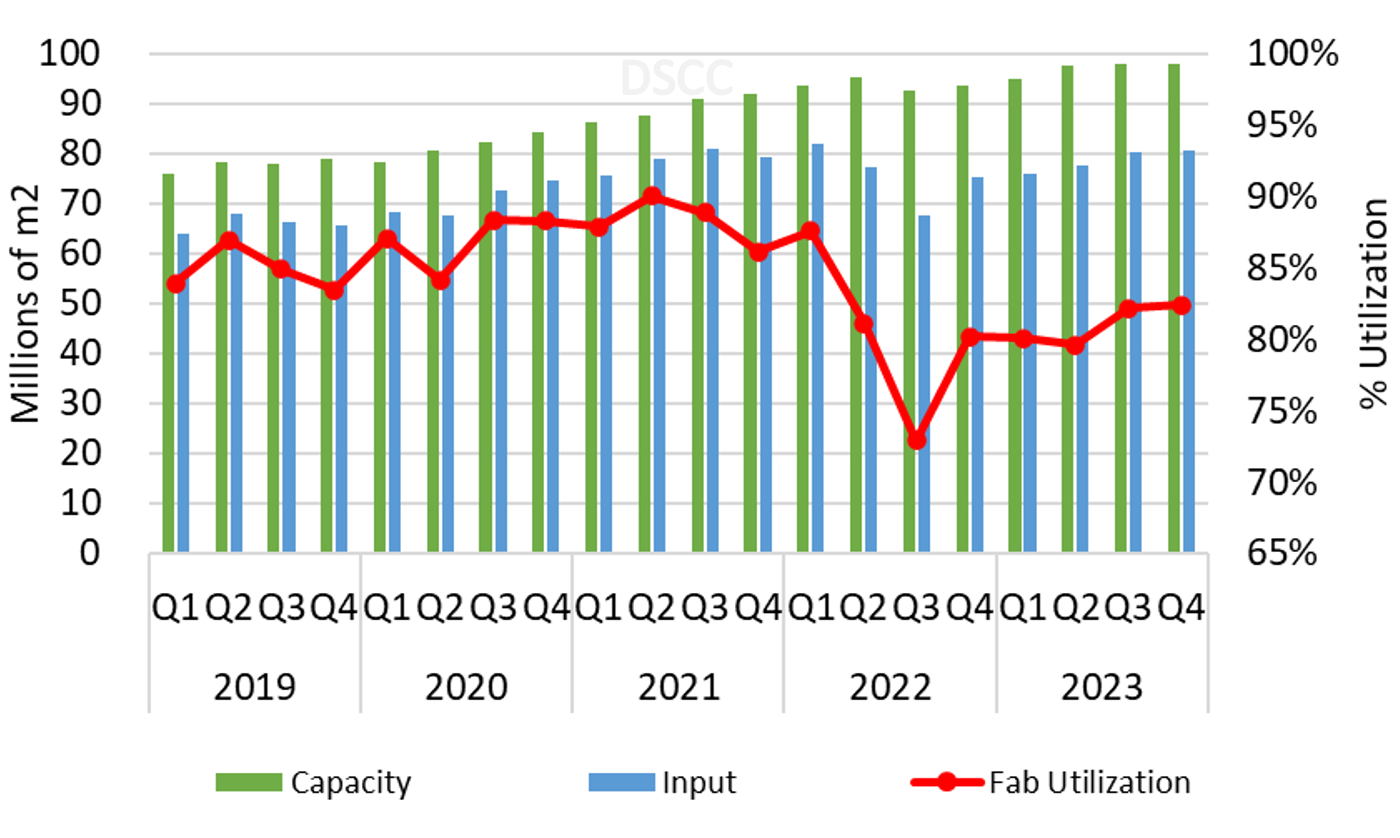

In an article last month covering DSCC’s Quarterly Display Fab Utilization Report (一部実データ付きサンプルをお送りします), we described the sharp downturn in utilization in 2022. That covers the short-term view, while in the FPD Supply/Demand Report, we cover the mid-term and long-term view. The mid-term perspective out to the end of 2023 is shown in the next chart here. While the most acute downturn is limited to the current quarter, the expected recovery in the fourth quarter and into 2023 will be anemic at best. LCD fab utilization is expected to remain under 85% for the full year 2023, a level even lower than the downturns in Q4’19 and Q2’20.

LCD Fab Utilization

As these charts indicate, the direction of change for both supply and demand favor the eventual absorption of the industry oversupply. Demand is increasing in 2023-2026 while supply growth is slowing down. This suggests that eventually the industry will return to balance, and the history of the Crystal Cycle suggests that eventually that balance will turn into a shortage, leading to price increases and a return to prosperity for LCD makers. However, this analysis makes clear that the road to industry recovery is long.

As noted above, the DSCC’s Quarterly FPD Supply/Demand Report (一部実データ付きサンプルをお送りします) provides a comprehensive listing of historical panel shipments in LCD and OLED for eight different applications, plus a forecast of units, area, and revenues for each application. The report also covers DSCC’s outlook on capacity for both LCD and OLED, with summary charts showing splits by manufacturer, gen size and region. Finally, the report covers fab utilization and supply/demand for LCD, mobile OLED and OLED TV. Readers interested in subscribing to the DSCC’s Quarterly FPD Supply/Demand Report should contact info@displaysupplychain.com.

本記事の出典調査レポート

Quarterly FPD Supply/Demand Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。