AMOLED部材市場、2026年には29億ドルに成長

冒頭部和訳

AMOLEDスタック材料 (全アプリケーション向け) の出荷金額が2020年の10億7000万ドルから2026年には29億ドルに、年率18%で成長する見通しである。DSCCが Semi-Annual AMOLED Materials Report (一部実データ付きサンプルをお送りします) 最新号で明らかにしている。Universal Display Corporationがすでに発表しているように、同社が青色燐光エミッタードーパントの商品化に成功すれば、2026年の出荷金額は30億ドルを超える可能性もある。同レポートは、各種アプリケーション、サプライヤーのマトリックス図、コスト比較など、AMOLED部材のあらゆる側面を詳しく解説している。

今期発行のレポートには、AMOLEDの生産能力と稼働率に関するDSCCの最新予測が収録されている。TV、携帯電話、その他のアプリケーションにおけるAMOLEDの成長が部材出荷の成長を推進する状況が今後も続くと予測される。同レポートには、業界が引き続き青色発光蛍光材料を使用することを前提としたベースケースシナリオのほか、青色燐光材料による出荷金額の増分の概要を示した特別な追加シナリオが含まれている。レポート購読者は燐光シナリオの詳細を見ることができるが、本稿ではベースケースシナリオに焦点を絞っている。

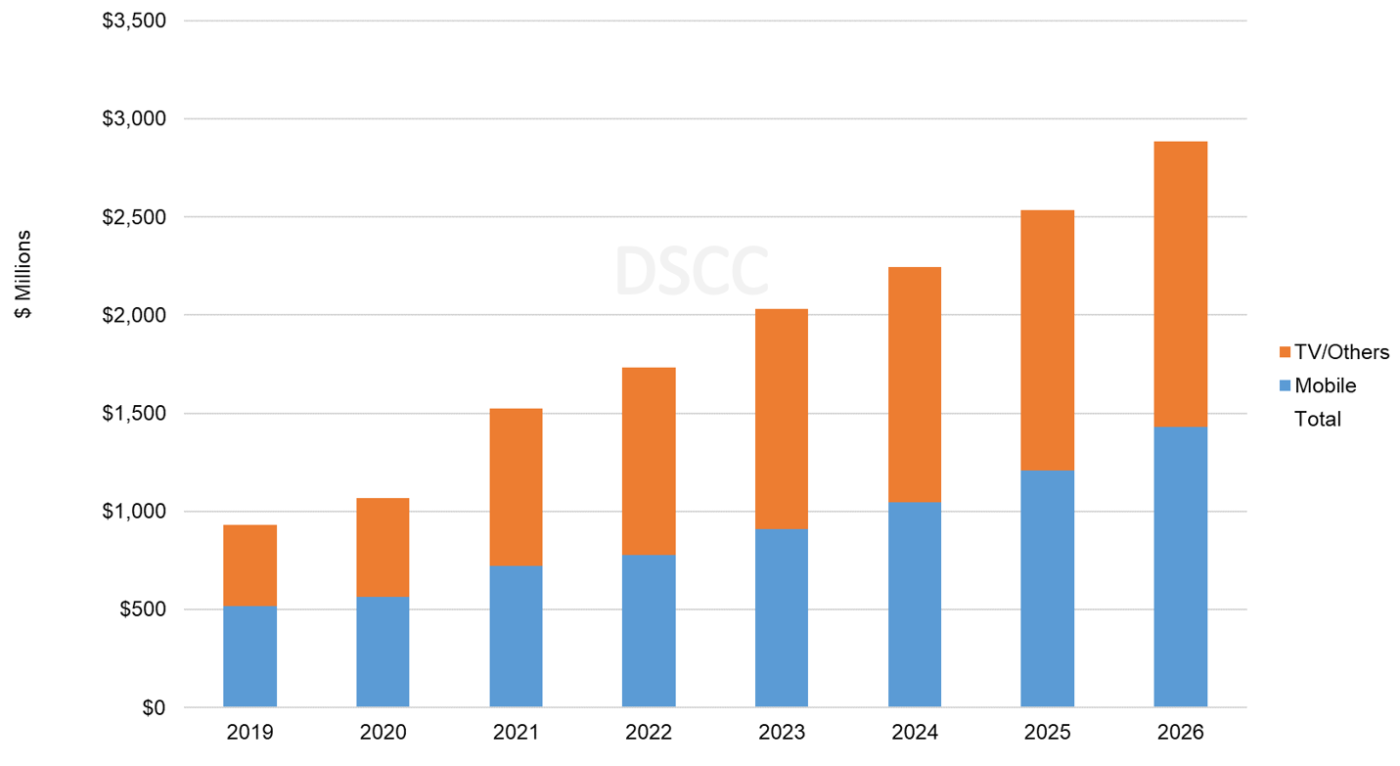

アプリケーション別のAMOLED部材出荷金額予測を示すのが以下の1つ目のグラフである。2022年から2025年までの出荷金額の大部分はTVやその他の大画面アプリケーション向けになると予測されるが、モバイルITアプリケーション向けの大型生産ラインが増加するにしたがい、2026年にはモバイルアプリケーション向けパネルの出荷金額がAMOLED部材出荷金額全体の50%にシェアを拡大すると見られる。TV用パネルの出荷金額の伸びが限定的なのは、QD OLEDやインクジェット印刷OLEDなど、OLED TVの新たな能力ではパネル1枚当たりの部材出荷金額が低くなるという事実によるものである。

第8.5世代以上サイズの新たなVTE RGB OLED生産ラインの能力はITを対象としている。この新たな能力は同じ材料を使用できることから、触媒であるタンデムスタックの利点とともに、UDCその他のVTE材料サプライヤーに利益をもたらす。追加能力の詳細情報は、DSCCの Quarterly Display Capex and Equipment Market Share Report に収録されている。

AMOLED Materials Market to Grow to $2.9 Billion by 2026

Sales for AMOLED stack materials for all applications are expected to grow at an 18% annual rate from $1.07B in 2020 to $2.9B in 2026, according to the last update of DSCC’s Semi-Annual AMOLED Materials Report (一部実データ付きサンプルをお送りします). Revenues can even exceed $3 Billion in 2026 if Universal Display Corporation successfully commercializes a blue phosphorescent emitter dopant as they have announced. The report details all aspects of AMOLED materials, including multiple applications, supplier matrices and cost comparisons.

This quarter’s report incorporates the latest update to DSCC’s capacity and utilization outlook for AMOLEDs. We expect that the growth of AMOLED in TV and phones, as well as other applications, will continue to drive material sales growth. The report includes a base case scenario that assumes the industry continues to use fluorescent blue emitters and includes a special additional scenario outlining the additional revenue generated by phosphorescent blue. Subscribers to the report can see details of the phosphorescent scenario, but for this article we will focus on the base case scenario.

Our forecast for AMOLED material revenues by application is shown in the first chart here. We expect revenues from TV and other large screen applications to generate the majority of revenues from 2022-2025, but that revenues from panels in mobile applications increase to 50% of all AMOLED material revenues in 2026 as larger fabs for mobile IT applications ramp up. A limitation to the growth of revenues for TV panels stems from the fact that the new capacity for OLED TV, such as QD OLED and Inkjet Printed OLED will have lower material revenue per panel.

New capacity for VTE RGB OLED fabs in G8.5+ sizes will be targeted at IT. This new capacity will benefit UDC and other VTE materials suppliers since the same materials can be used, with the benefit of tandem stacks as a catalyst. Details of the capacity additions can be found in DSCC’s Quarterly Display Capex and Equipment Market Share Report (一部実データ付きサンプルをお送りします).

AMOLED Material Revenues by Application

The report details the OLED stack configurations of all the major AMOLED product architectures, including Small/Medium panels with RGB pixel structure, White OLED (WOLED) by LGD for TV panels, QD-OLED by Samsung and OLED EX by LGD. The stack profiles, along with estimates of material thickness, material utilization and material prices, form a picture of the unyielded stack cost for each AMOLED product architecture.

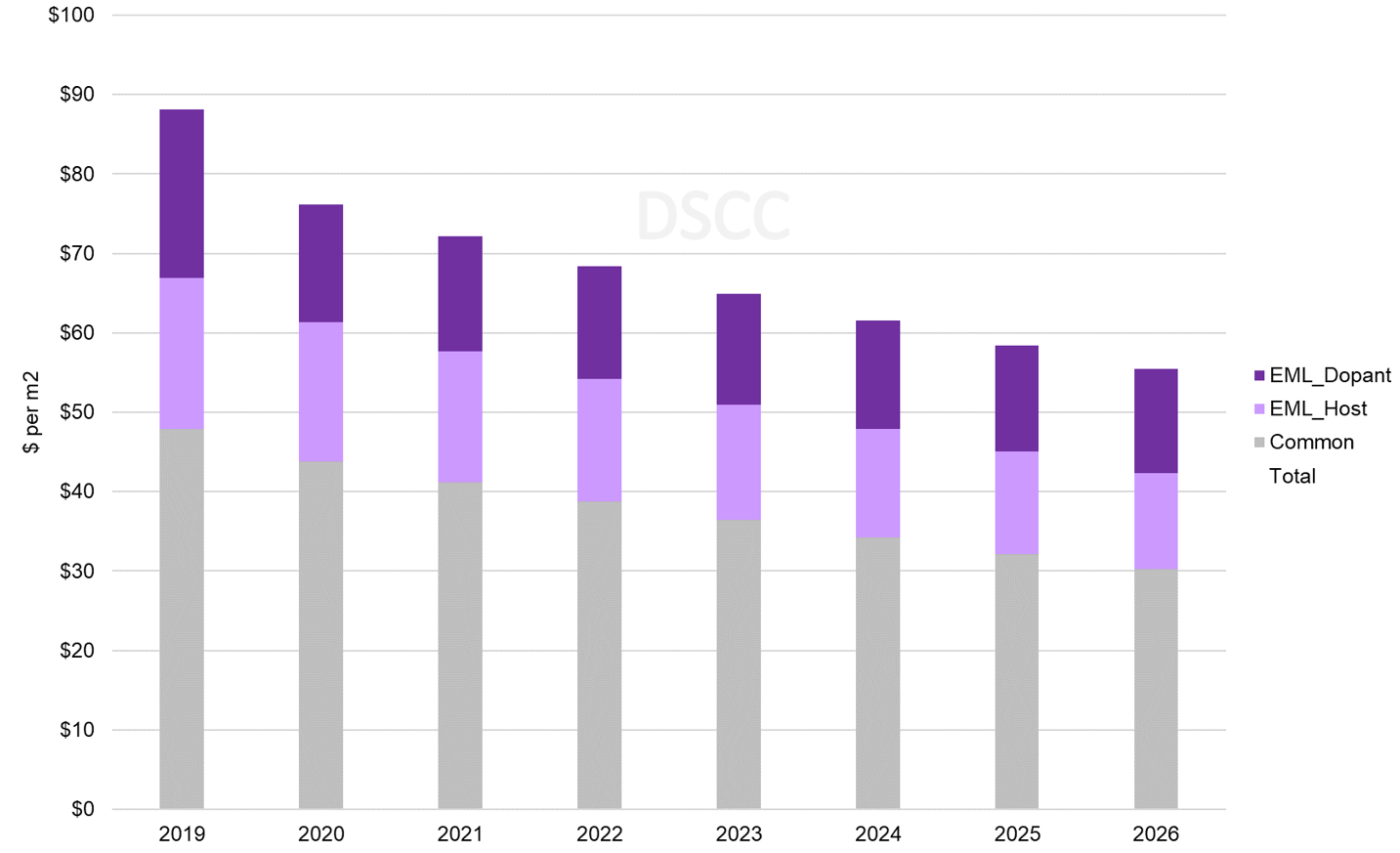

The following chart here shows our outlook for the material cost for LGD’s White OLED panels. We expect that steady, incremental improvements in material utilization and price will help LGD drive the unyielded stack cost of its standard WOLED panels from $68.4 per square meter in 2022 to $55.4 per square meter in 2026, an average decrease of 5% per year. For LG Display, with increased volume and experience we expect that yields will also improve over time, so that the cost declines of yielded OLED stack materials will be even greater.

LGD’s OLED EX panels have two changes that boost brightness but also add cost to the OLED stack. The OLED EX panels have an additional green emitting layer to generate more light, and LGD employs deuterium in the host materials of the blue emitting layers to extend the lifetime of the panels. With these two changes, we estimate that the unyielded stack cost of the OLED Evo panel adds nearly $40 per square meter in cost. Although this figure also declines over time, we estimate the cost adder in 2026 remains more than $30 per square meter. With this continuing cost adder, we expect that OLED EX will continue to be positioned as a premium product, positioned to compete directly with Samsung’s QD-OLED.

Unyielded Material Cost per m2 for WOLED Panels

Our report provides an estimate of AMOLED stack material costs for QD-OLED, which we expect will be lower than those for WOLED. When compared with the standard WOLED panels, the cost advantage of the QD-OLED stack is modest because QD-OLED requires three blue emitting layers plus an additional green emitting layer to boost brightness. We estimate that in 2022, the unyielded stack costs for QD-OLED are expected to be ~25% lower than the standard WOLED. Of course, for QD-OLED, the unyielded stack cost is only a part of the picture. The yields on the mature WOLED technology are certainly higher than those for QD-OLED in these initial stages, and the front end of the QD-OLED display includes both a color converter and a color filter, and therefore will be substantially more expensive than the simpler color filter used in WOLED. While we estimate that the OLED stack cost of QD-OLED is lower than that of WOLED, we expect the total product cost of QD-OLED to be higher. For a more detailed comparison of the full panel costs for QD-OLED and WOLED, please see DSCC’s Semi-Annual Advanced TV Panel Cost Report (一部実データ付きサンプルをお送りします).

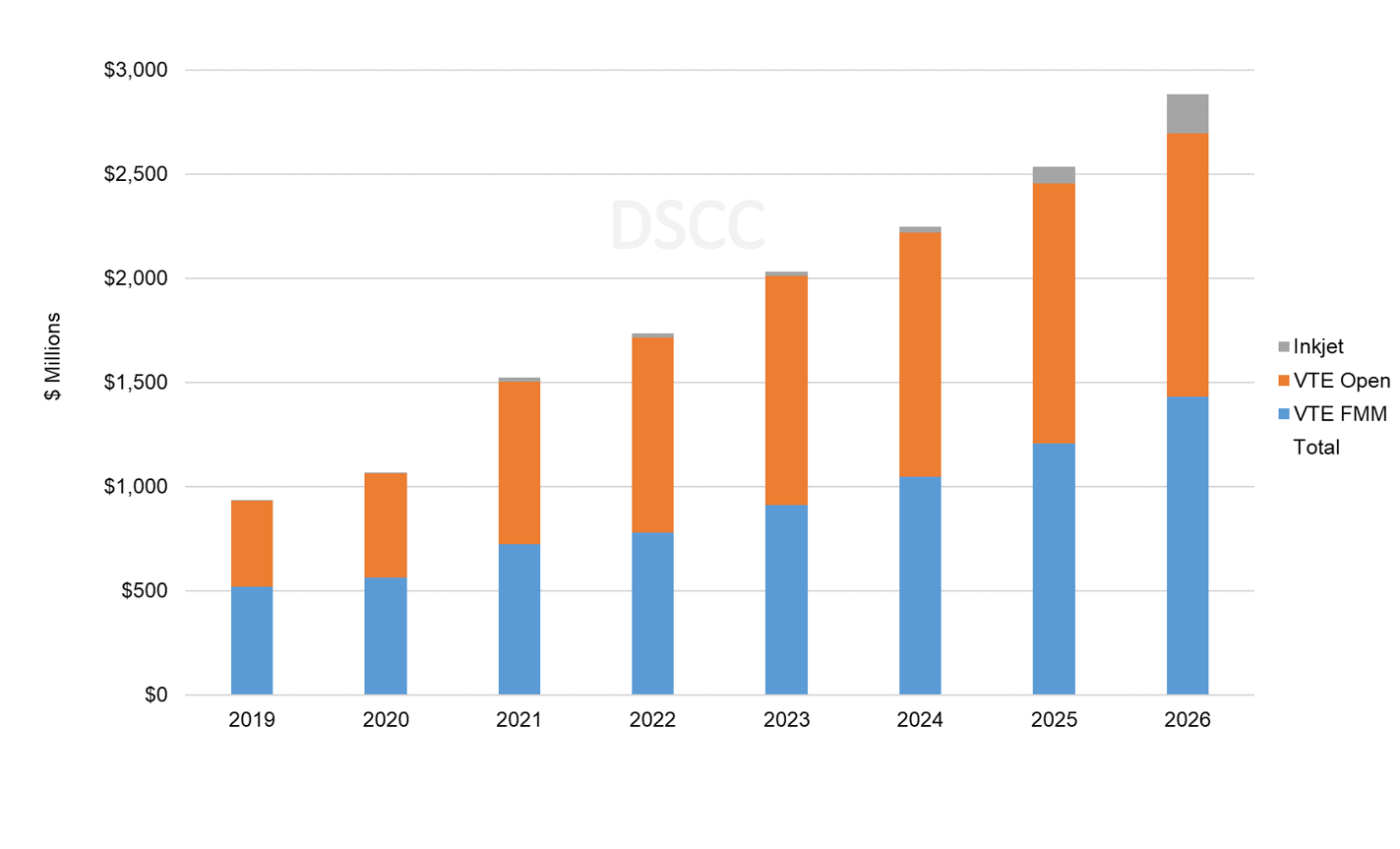

With CSOT’s planned investment in a Gen 8.5 AMOLED fab using Inkjet printing with production starting in 2025, the revenues for soluble materials for Inkjet-Printed OLED will increase rapidly in 2025. Nevertheless, the AMOLED materials market in terms of overall revenues will continue to be dominated by evaporated materials, and this dominance will be accelerated by additional RGB FMM VTE Gen 8.5 fabs for IT and TV. Evaporated materials will remain the only type used for smaller AMOLED panels for smartphones and will continue to dominate the market for OLED TV panels. We expect revenues from soluble materials for Inkjet-Printed OLED will grow from less than $1M in 2019 to $188M in 2026, when they will represent 13% of the TV/Other segment but still only 6% of the overall AMOLED materials market.

Material Revenues by Deposition Type

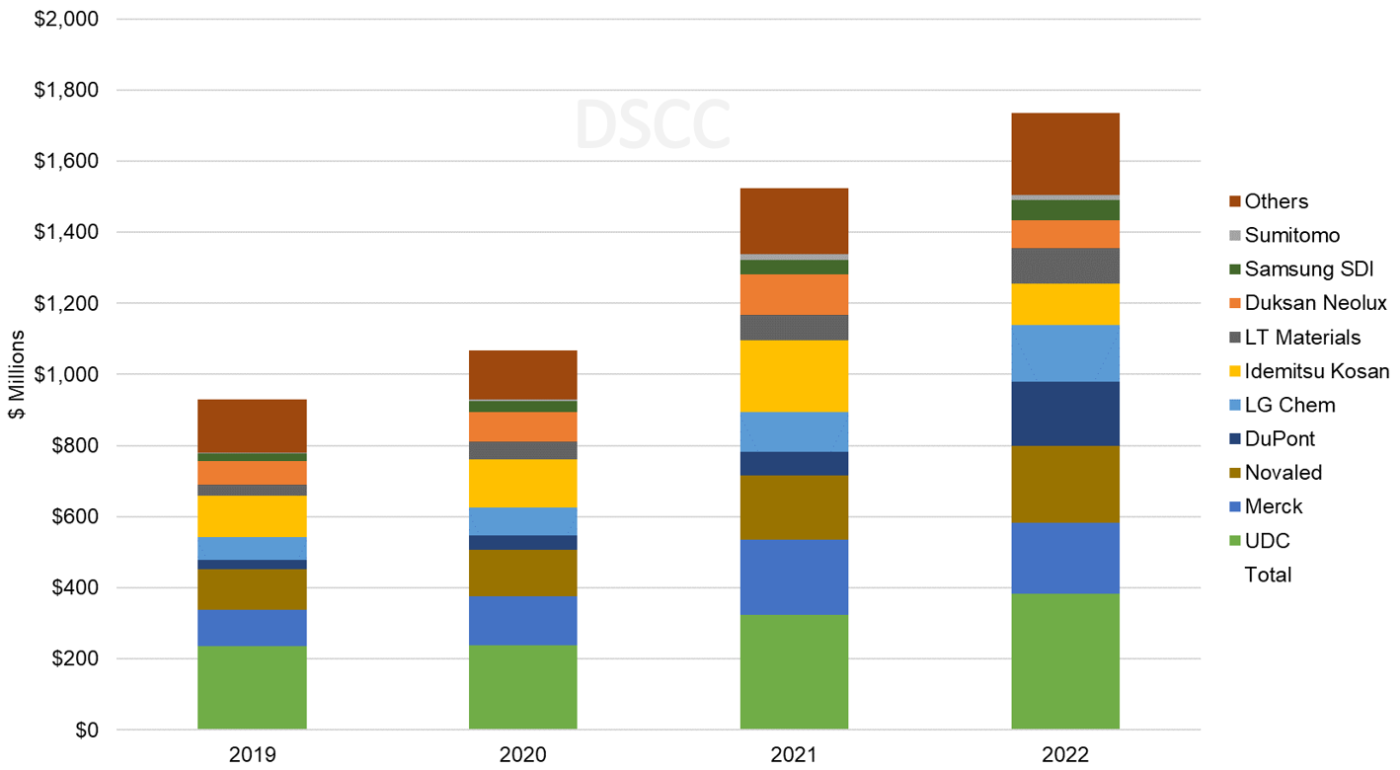

Based on the existing supplier matrix including some shifts in suppliers in 2022, the report includes a projection of AMOLED material revenues by supplier, as shown on the next chart. Universal Display Corporation (UDC) has been the #1 supplier in revenues for the industry, and we expect that to continue. DuPont, Novaled and Merck hold the number two through four positions among materials suppliers. These four companies are expected to capture 56% of industry revenues in 2022, but as the chart indicates, there is a long tail of companies supplying materials into the industry.

AMOLED Materials Revenues by Supplier

This most recent edition of the report includes a scenario estimating the additional OLED material revenues generated from the potential shift from fluorescent to phosphorescent blue emitters. After refusing to describe a timeline for many years, Universal Display Corporation in February 2022 announced that it was on track to meet preliminary target specs for phosphorescent blue by year-end, which should enable the introduction of phosphorescent blue OLED into the commercial market in 2024. This shift, if it happens, will act as an accelerant for the growth of the entire OLED industry.

For mobile devices, it will allow a rebalancing of the pixel structure, reducing the size of the blue sub-pixel and increasing the size of the red and green sub-pixels and therefore improving light efficiency overall. This improved light efficiency can be used for higher brightness premium displays, or it can be traded off for lower power consumption, improving battery life. Either way, OLED panels with phosphorescent blue emitters will have a higher value to device makers, and we expect they will command a substantial price premium.

For TV applications, the improved efficiency can be used to boost brightness or to reduce the number of emitting layers. LGD uses two blue emitting layers in its WOLED stack, and SDC uses three blue emitting layers in its QD-OLED stack. Reducing a single emitting layer reduces the total number of layers by four, because it removes the need for electron and hole transport layers and p/n charge generation layers.

Because of the substantial value added by phosphorescent blue emitters, we expect that Universal Display will be able to generate significantly more revenue from sales of its blue dopant materials compared to the corresponding revenue from fluorescent blue dopants. Our report makes assumptions about the time for the industry to transition from fluorescent to phosphorescent and how that varies by panel maker and by application. The report also makes assumptions about the revenue premium to be generated by phosphorescent to come to an estimate of phosphorescent blue dopant revenues. Subscribers to the report can see all the detailed assumptions and the conclusion, but for readers of this newsletter it will suffice to say that the increased revenue would be a substantial boost to revenues for UDC.

The DSCC Semi-Annual AMOLED Materials Report (一部実データ付きサンプルをお送りします) includes profiles for all major AMOLED stack architectures, supplier matrices for the main OLED panel makers and revenue projections for 18 different material types and 20 material suppliers. For more information about the report, please e-mail info@displaysupplychain.co.jp.