Advanced (先端技術FPD搭載) TV市場の出荷実績編~2022年も引き続き成長

冒頭部和訳

FPD業界にとって今年は厳しい年となっているが、Advanced (先端FPD技術搭載) TV市場はQ1’22も前年比成長を続けており、業界でもこのセグメントは引き続き展望が明るい。LCDとOLEDの間のテクノロジー競争は、双方が出荷台数を伸ばしたためシェアにはほぼ変化がなく、このラウンドは引き分けとなった。DSCCが発行した Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) の最新版によると、ブランド別ではSamsungが2020年初頭以降、Advanced TV市場におけるシェアを縮小しているが、台数ベースではシェアポイントを失ったにもかかわらず、金額ベースでは2シェアポイントの回復に成功した。

本レポートは、最先端TVテクノロジー (WOLED、QDディスプレイ、QDEF、4Kおよび8K解像度のMiniLED) を含む、世界のプレミアムTV市場を対象としている。テクノロジー/地域/ブランド/解像度/サイズの各項目別に現在と将来のTV出荷台数と出荷金額を調査、これら全てのテクノロジーの成長について予測している。今回発行の最新版には、Q1’22の出荷実績と2026年までの最新の出荷予測を収録している。本稿ではQ1’22の出荷実績を取り上げる。また来週の記事では最新の出荷予測を確認する予定である。

DSCCでは「Advanced TV」を、全てのOLED TV、8K LCD TV、および量子ドット技術搭載の全てのLCD TVを含む、先端ディスプレイ技術機能を備えたTVと定義している。本レポートに収録の実績データにより、以下を含む先端技術LCD TVの機能別分析が可能となっている。

- QDEF TV: 量子ドットエンハンスメントフィルムを使用したTV。Samsung、TCL、その他のメーカーから「QLED」として販売されている。

- MiniLED: MiniLEDバックライト搭載のLCD TV。2019年にTCLが発売、2021年にSamsung、LG、Hisenseなども導入している。

2021年までのOLED TVの実績データにはLGDのWhite-OLED (WOLED) テクノロジーという1つの製品構成しか含まれていないが、Q1’22にはSamsung DisplayのQD-OLED TVの出荷台数が初めて確認され、ごく少数ながらMicroLED TVの販売も初めて見られた。

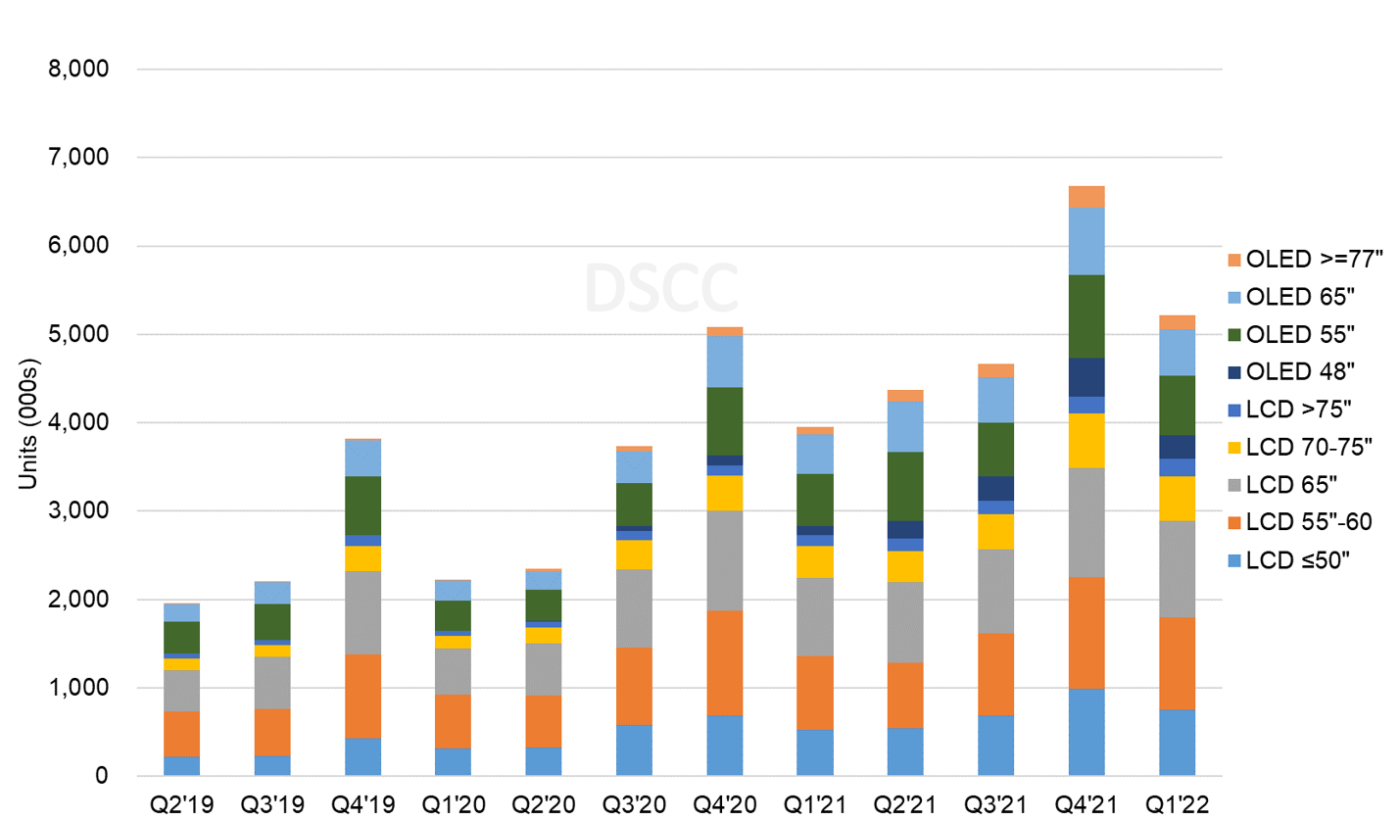

以下の1つ目のグラフが示すように、Q1’22のAdvanced TV出荷台数は前年比32%増の520万台だった。台数はOLED TVが前年比33%増、Advanced LCD TVが前年比32%増で、出荷増分は均等に分散している。OLED TVは全ての画面サイズグループで前年より出荷が増加したが、最も成長が大きかったのは48インチで前年比258%増、また77インチ以上は前年比85%増となった。OLED TVの48インチモデルが導入されたのはQ2’21が初めてだが、Q1’22にはすでにOLED TVの出荷台数全体の16%を占めている。同様に、83インチのOLED TVもQ2’21に導入され、77インチ以上の成長を促進している。LCDカテゴリーでは、全ての画面サイズグループで出荷台数が前年比2桁成長を記録し、最も成長が大きかったのは75インチ超で前年比58%増となっている。

Advanced TV Market Continues to Grow in 2022

Although the display industry is having a difficult year, the Advanced TV market continued to grow Y/Y in Q1 2022, and this segment of the industry continues to look promising. In this round of the battle between LCD and OLED technologies the two sides played to a draw, with both sides gaining volume and share largely unchanged. The latest update of the DSCC Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) is now available to subscribers. On a brand level, Samsung has lost share in the Advanced TV market since early 2020, but managed to regain 2 share points of revenue share despite losing a share point of unit share.

This report covers the worldwide premium TV market, including the most advanced TV technologies: WOLED, QD Display, QDEF and MiniLED with 4K and 8K resolution. The report looks at current and future TV shipments and revenues by technology, region, brand, resolution and size, and forecasts the growth of all these technologies. This update includes the shipment results for Q1 2022 and an updated forecast out to 2026. In this article, we will review the historical results of Q1 2022; in an article next week we will review the updated forecast.

We define an “Advanced TV” (capitalized) as any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology. The historical data in the report allows analysis by feature for Advanced LCD TVs, including:

- QDEF TV: TV using a Quantum Dot Enhancement Film; these TVs are sold as “QLED” by Samsung, TCL, and others;

- MiniLED: LCD TVs with a MiniLED backlight, as sold by TCL starting in 2019 and introduced by Samsung, LG, Hisense and others in 2021;

The historical data through 2021 for OLED TV includes only one product configuration, LGD’s White-OLED (WOLED) technology, but in Q1 2022 we saw the first volumes for Samsung Display’s QD Display or QD-OLED TVs and also the first sales of MicroLED TVs in very small volumes.

Advanced TV shipments in Q1 2022 increased by 32% Y/Y to 5.2M units, as shown in the first chart here. In volume terms, the gains were spread equally as OLED TVs increased 33% Y/Y while Advanced LCD TVs increased 32% Y/Y. All screen size groups for OLED TVs increased Y/Y, with the biggest gains in 48”, up 258% Y/Y and 77” and larger, up by 85%. The 48” OLED TV models were introduced only in Q2 2021, but already represented 16% of OLED TV volume in Q1 2022. Similarly, 83” OLED TV sets were introduced in Q2 2021 helping to drive growth in 77”+. Within the LCD category, shipments increased by a double-digit % Y/Y across all screen size groups, with the biggest gains in >75” which increased by 58% Y/Y.

Advanced TV Shipments by Size and Display Technology

Advanced TV revenue growth in Q1 2022 was higher than unit growth at 39% Y/Y, and for the second quarter in a row the revenue growth was driven by LCD. Revenues for Advanced LCD TVs grew 45% Y/Y driven by general price increases, a bigger screen size mix and the growth of MiniLED TVs at higher prices. Revenues for Advanced LCD TVs larger than 75” grew 150% Y/Y, the fourth consecutive quarter of triple-digit revenue growth for that category. OLED TV revenues increased 32% Y/Y and OLED revenue share decreased from 41% in Q1 2021 to 38% in Q1 2022.

The report’s pivot tables allow an analysis of brand share by screen size, region, technology, resolution and other variables. In Q1’22, among all Advanced TV products, Samsung maintained its leading position but lost 1 point of unit share with shipments up 29% Y/Y, slightly less than the market growth. Breaking a streak of five consecutive quarters of Y/Y share gains, LG Electronics lost 2 share points Y/Y in Q1 2022 as shipments increased by 19% Y/Y and unit share fell from 21% to 19%. The numbers 3 and 4 brands fared better: TCL’s Advanced LCD shipments increased 43% Y/Y and TCL gained share Y/Y from 7% to 8%, while Sony shipments increased by 84% Y/Y and Sony share increased Y/Y from 5% to 6%.

While Samsung lost share on a unit basis, it held share Y/Y and regained 2 share points Q/Q on a revenue basis as revenues increased 40% Y/Y. LG revenues increased 15% Y/Y and share decreased from 28% in Q1 2021 to 23% in Q1 2022. Sony took the #3 spot in revenues with 9% share with 93% revenue growth Y/Y and TCL followed with 8% on 48% revenue growth.

The report divides worldwide shipments into eight geographic regions. Western Europe and North America have continued to be the largest regions for Advanced TV. These two regions represented a combined 63% of Advanced TV units and 59% of revenue in Q1 2022. Shipments to Western Europe increased 46% Y/Y in Q1 2022 and revenues increased by 26% Y/Y. Shipments to North America increased 24% Y/Y and revenues increased 49% Y/Y as sales of big TVs surged. China shipments increased 31% Y/Y in Q1 and revenues increased 77%.

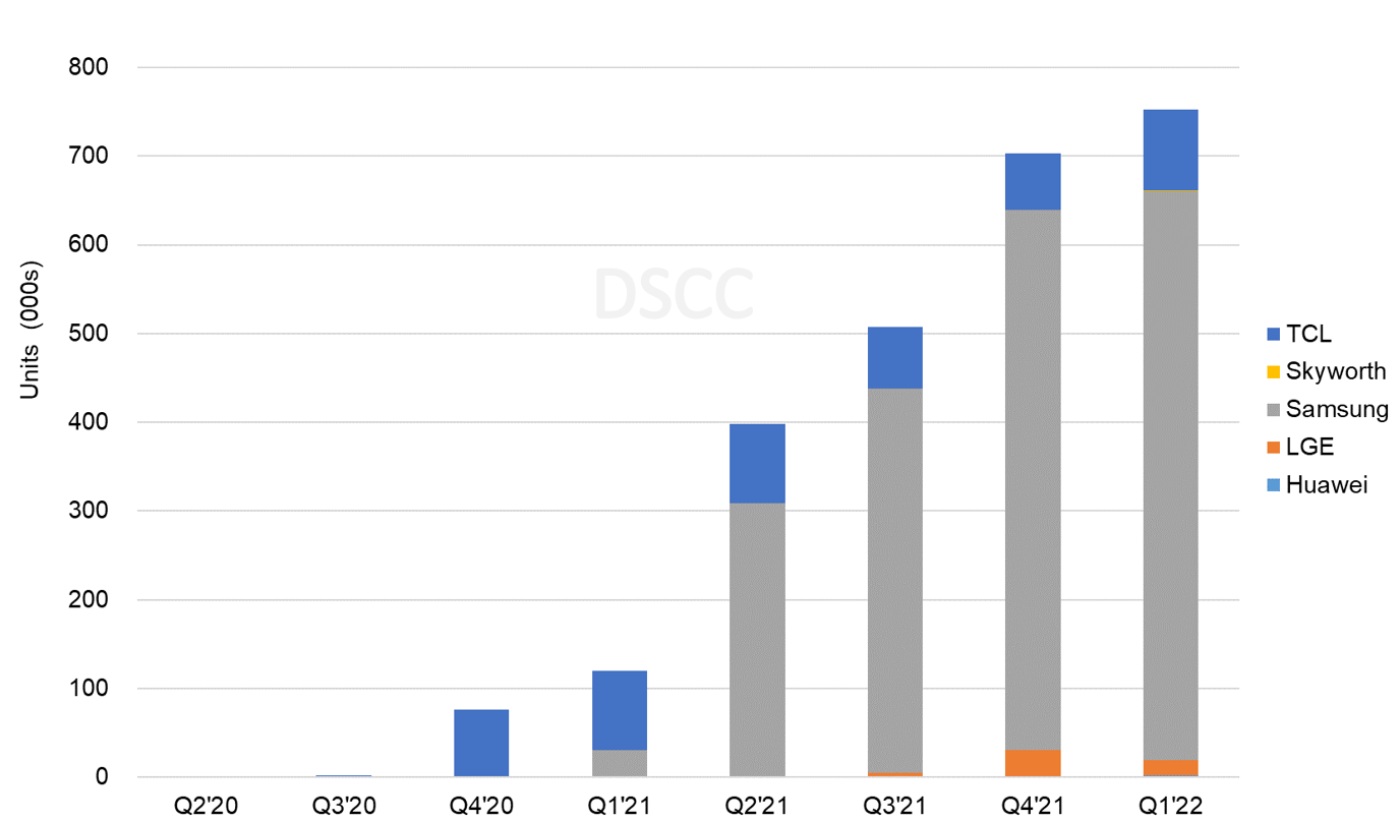

The report tracks the emergence of MiniLED as a competitor to OLED TV in the premium space. The next chart here shows MiniLED TV shipments by brand. While TCL introduced MiniLED in late 2019 and recorded some sales in 2020, the category remained tiny until Samsung and other brands introduced products with MiniLED technology in Q1 2021. From less than 100K units in 2020, MiniLED TV shipments grew to more than 1.7M units in 2021, and revenue grew from $73M in 2020 to $3.5B in 2021. Although it’s not a fair comparison because Samsung was just introducing MiniLED a year ago, shipments increased by an impressive 629% Y/Y to 753K in Q1’22 and revenues increased 533% Y/Y to $1.4 billion.

MiniLED TV Shipments by Brand

In North America, Samsung enjoys a dominant position on the strength of its large-screen product portfolio but has seen its share erode as competitors in both Advanced LCD and OLED TV grow share. In Q1 2022 Samsung maintained the #1 position but unit share declined by 2 share points Y/Y to 49%. With a richer mix of MiniLED, though, Samsung revenue share increased by 5 points Y/Y to 49%. On the other hand, LG stumbled in the quarter as it lost 5 share points Y/Y in units and 9 share points in revenue. Both TCL and Sony gained share, but Vizio’s unit and revenue share decreased Q/Q and Y/Y and Vizio has lost 10 share points since peaking in Q1 2020.

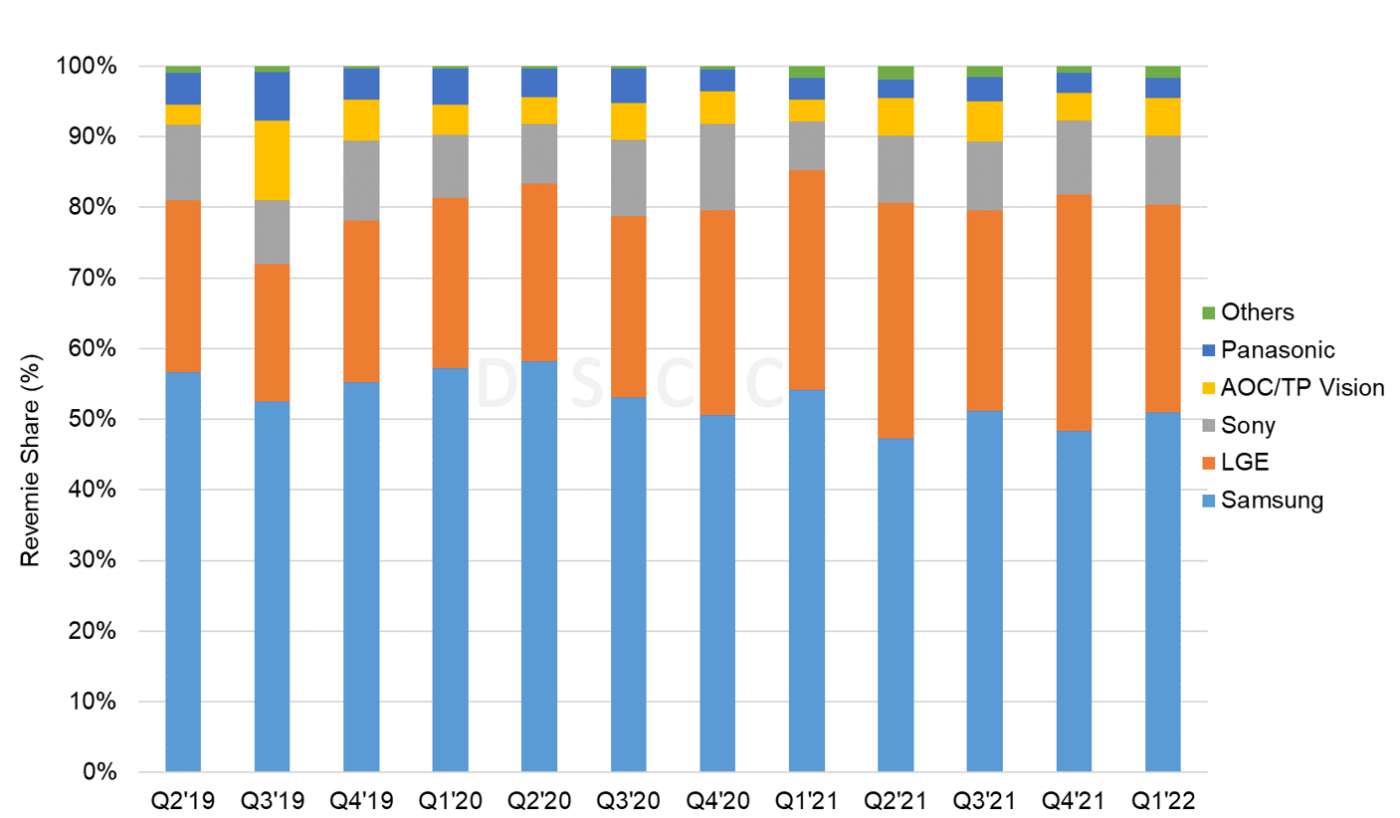

In Western Europe, Samsung fared worse as it lost 3 points of both unit share and revenue share Y/Y. LG lost one point of unit share and revenue share Y/Y in the #2 spot. Sony fared better as it gained two points of unit share and three points of revenue share, and both Panasonic and Philips each improved their small share positions Y/Y.

Advanced TV Revenues - Western Europe

China remains a true battleground with four companies with double-digit % share in both units and revenues. Huawei has established itself as the leading player in Advanced LCD TVs and has taken the #1 position in units for five consecutive quarters. TCL is tied for the #2 position in units with Hisense but holds that position alone in revenue share.

Another interesting cut of the brand data is the battle by screen size. In 55” worldwide unit shipments, Samsung continues to lead and increased its unit share by two points and its revenue share by four points Y/Y to 48% and 37%, respectively. LG faltered, losing five points of unit share and seven points of revenue share to 23% and 31%, respectively.

In the largest size category of 70”+, Samsung has seen its position erode from a near-monopoly in 2018 to 2019 to mere dominance in 2020-2021 as LG and Sony sales of 77” and 83” OLED and TCL sales of 75” and larger LCD have increased dramatically. In Q1 2022, Samsung still captured 54% unit share and 50% revenue share of 70”+ Advanced TVs, but these figures were down from 64% and 60%, respectively, in Q1 2021. Meanwhile, LG maintained its unit share Y/Y at 13% but lost three points of revenue share to 15%, while Sony, Huawei, Hisense and TCL gained share.

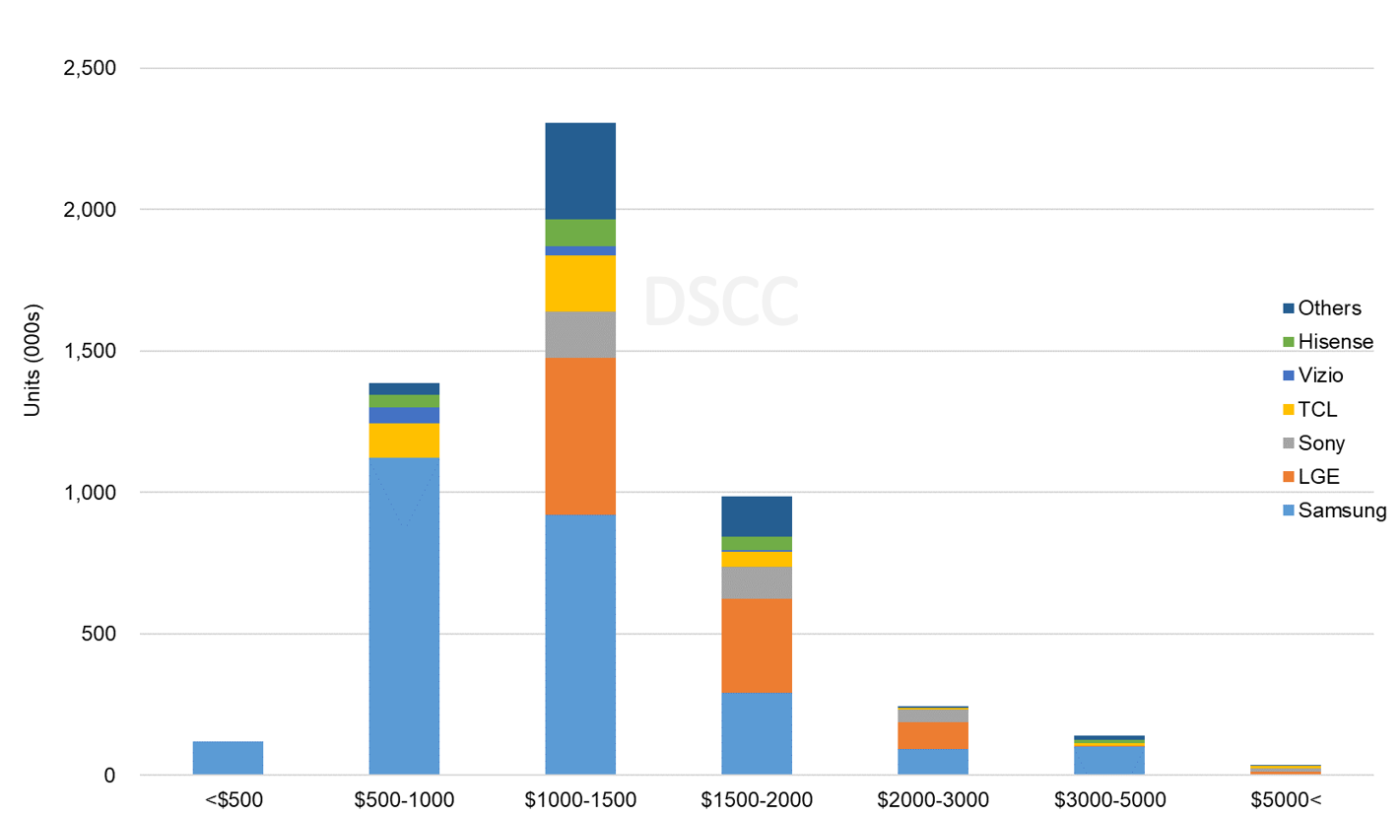

The last chart here shows one last valuable cut of the data, units by brand by price band. The pivot tables allow for this analysis by any time period, and the chart here shows the market by price band for Q1 2022. The chart shows that Samsung’s leading position in Advanced TV is mostly a function of its dominance in Advanced TVs under $1000. Samsung’s strategy of pushing its QLED product line toward mainstream price points has allowed it to thrive, but LG, Vizio and TCL also appear as competitors at these lower prices. LG’s OLED TVs give it the leading position in the range of $1500-$3000, and Sony holds a solid #3 position in price points above $1000. Sales volumes at price points over $5000 form only a tiny slice of the market.

Worldwide Advanced TV Units by Price Band (Q1 2022)

DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) includes technical descriptions of all major advanced TV display technologies, plus quarterly shipment results from Q1 2018 through Q1 2022, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The most recent update includes technology insights on QD-OLED, MiniLED and White OLED learned from recent product announcements and observations at SID Display Week 2022. The report includes DSCC’s quarterly forecast for five years across technology, region, resolution and size. Readers interested in subscribing to the DSCC Advanced TV Shipment Report should contact info@displaysupplychain.co.jp.

本記事の出典調査レポート

Quarterly Advanced TV Shipment and Forecast Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。