SID/DSCC 2022ハイライト~TV市場と技術動向

冒頭部和訳

Bob O’Brien, DSCC

本講演では、最初にFPD業界にとってのTVの重要性について概説し、次にTV市場におけるブランドとテクノロジーの戦いの状況と展望を確認、最後にDSCCのTV予測を提示した。

TVは面積ベースでFPD業界の圧倒的最大セグメントであり、2022年にはFPD出荷面積の70%を占め、業界の今後の成長はTV画面サイズの拡大が主な推進要因となる。TVは需要に対する貢献度が非常に高く、FPDバリューチェーン全体に影響を与えるクリスタルサイクルを推進する存在である。歴史的に見て、FPDメーカーの利益はTV用LCDの価格と高い相関関係があり、業界に対するクリスタルサイクルの影響がいかに支配的かを示している。OLEDが業界でシェアを獲得するにしたがい、一部のパネルメーカーの業績にはOLED事業の収益性の差違によって分散が見られるようになっている。

パンデミック需要はTV用LCDの価格にこれまでで最大の上昇をもたらしたが、LCD供給が増加し需要が減少するにつれて、史上最速の価格下落ももたらした。FPD供給はQ1’20からQ1’22にかけて24%増加し、2021年初頭の需要のピークは高かったものの、そのピークは今年までにとうの昔に過ぎており、供給は需要を大幅に上回っている。TV用LCD価格は史上最低値まで下がり、依然として下落を続けている。パンデミックではFPD価格急騰でTV価格が史上初の上昇となり、米国消費者物価指数 (CPI) の測定によれば、TV価格のインフレ率はピーク時には13.3%に達した。

トップ3ブランド (Samsung、LG、Sony) のTV事業はパンデミックまでの数年間で出荷金額が減少していたが、その後急増し、2021年の出荷金額はパンデミック前の2019年より27%増加した。TVメーカーは過去6年間で歴史的な高水準の利益率を享受しており、パンデミックの間、利益は大幅に増加した。世界第4位のTVブランドTCLは、成長を優先しながら一貫した利益を生み出しており、まもなくSonyから第3位の座を奪う可能性がある。

SID/DSCC 2022 Business Conference Highlights - TV Market and Technology Outlook

The TV Display Market and Technology Outlook session featured presentations from three analysts of the industry plus the CEO of a critical material supplier and an executive from a leading display maker. The presenters included:

- Bob O’Brien, Co-Founder, DSCC

- Paul Gagnon, Vice President and Industry Advisor, The NPD Group

- Paul Gray, Senior Research Manager, Omdia

- Jason Hartlove, President and CEO, Nanosys

- Chirag Shah, Director of Go-To-Market Marketing, Samsung Display

Bob O’Brien, DSCC

In my talk, I first outlined the importance of TV to the display industry, then reviewed the status and prospects for the brand and technology battles in the TV market and wrapped up with DSCC’s TV forecast.

TV is by far the largest segment of the display industry as measured by area, representing 70% of flat panel display area shipments in 2022, and industry growth will be primarily driven by increasing TV screen sizes. Because of its huge contribution to demand, TV drives the Crystal Cycle, which affects the whole display value chain. Historically, panel maker profits are highly correlated to LCD TV panel prices, showing the dominant effect of the Crystal Cycle on the industry. As OLEDs gain share in the industry, some panel maker results are diverging based on the varying profitability of the OLED business.

Pandemic demand drove the biggest price increase ever for LCD TV panel prices, but also the fastest price declines in history as LCD supply increased and as demand ebbed. Flat panel supply increased by 24% from Q1 2020 to Q1 2022 and while the demand peak in early 2021 was even higher, by this year that peak was long past, and supply greatly exceeds demand. LCD TV panel prices have fallen to new all-time lows and are still declining. The pandemic surge in panel prices drove the first-ever increase in TV prices, as measured by the US Consumer Price Index (CPI) with TV price inflation peaking at 13.3%.

The TV business for the top three brands (Samsung, LG, Sony) had seen declining revenues in the years up to the pandemic, but revenues surged and 2021 revenues were 27% higher than pre-pandemic 2019. TV makers have enjoyed historically high profit margins in the last six years, and profits increased handsomely during the pandemic. The #4 global TV brand TCL has generated consistent profits while prioritizing growth and could soon catch Sony for the #3 position.

While the global TV industry exceeds 250M units, the vast majority of sales are made in TVs sold under $500. The brand and technology battles focused on the Advanced TV market. Samsung has dominated the Advanced TV market but saw its share erode in 2021. The technology battle in Advanced TV appears to be shaped by three key technologies:

- MiniLED enjoys the diversity and huge scale of the LCD industry, has the widest range of product configurations including 8K models and is offered by all top brands, but MiniLED cannot match OLED for pixel-level contrast.

- White OLED has a wide range of screen sizes and brands but limited 8K and relies on a single panel supplier, LGD.

- QD-OLED offers superior picture quality but a limited product range for only two brands.

MiniLED LCD cost is on par with White OLED for 65” but has a cost advantage in 75” and larger sizes. QD-OLED 4K cost is even higher than MiniLED 8K.

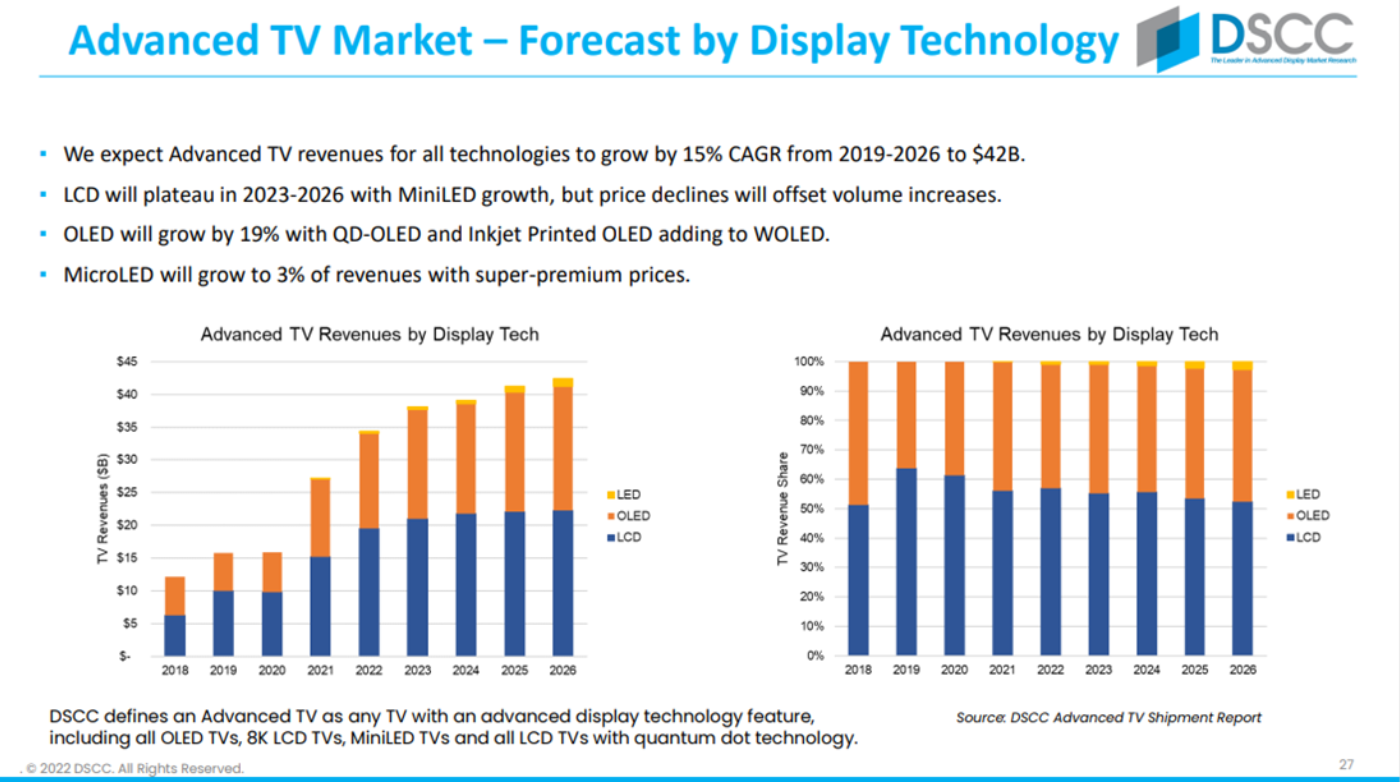

DSCC expects growth in Advanced TV to 38M units in 2026 and revenues exceeding $40B. Revenues for advanced LCD TVs will plateau in 2023-2026 as price declines offset volume increases, but OLED will continue to grow with expanded capacity and MicroLED will emerge in small volumes at super-premium prices.

Jason Hartlove, Nanosys

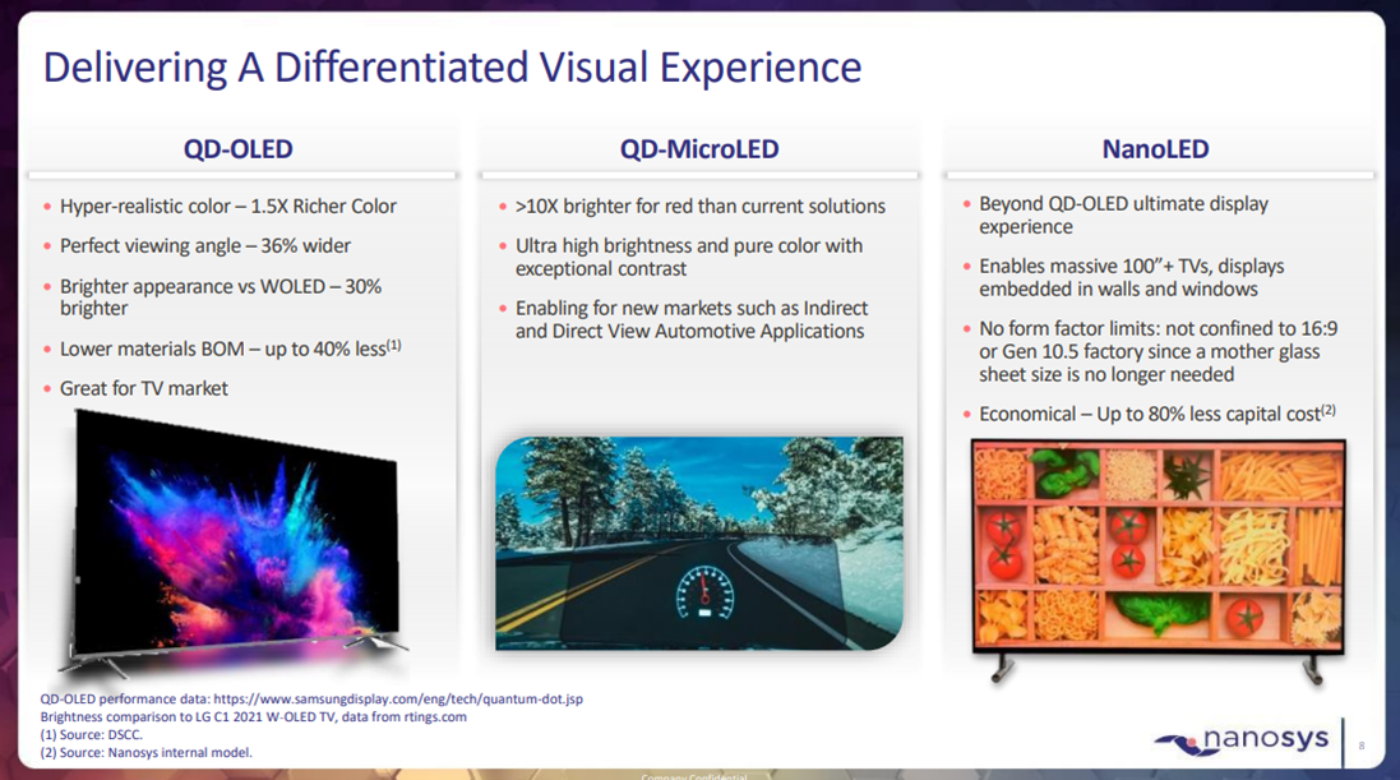

Hartlove started by introducing his company, reminding the audience that with its acquisition of glo in 2021, Nanosys’ product portfolio includes MicroLEDs as well as its quantum dot products. The company’s roadmap addresses the future of display, from the QDEF products which have been on the market since 2013 to QD-OLED in 2022 and future products including MicroLED and nanoLED.

Nanosys won a 2022 SID Display Component of the Year with its xQDEF product. Nanosys has improved the stability of its quantum dots to eliminate the need for barrier layers, and xQDEF is formed with high-temperature extrusion, allowing a single-piece combination diffuser plate + quantum dot RGB backlight film.

In addition to QD-OLED which was detailed later by Chirag Shah of SDC, Hartlove outlined the future QD-MicroLED and NanoLED products. QD-MicroLED will be based on blue MicroLED with quantum dot color conversion, allowing a great increase in red brightness efficiency. Nanosys has developed both inkjet printable and photolith compatible formulations for quantum dots.

The long-term dream for quantum dots is electroluminescent QDs which Hartlove believes will provide the “ultimate display experience,” and Hartlove indicated that nanoLED is “coming sooner than you might expect.” Electroluminescent quantum dot efficiency, as measured by external quantum efficiency (EQE) is already approaching OLED performance and lifetime is rapidly improving.

Chirag Shah, SDC

Chirag Shah outlined the features and performance of Samsung Display’s highly-anticipated QD-OLED displays, which were prominent in the Display Week exhibition. SDC refers to this technology as QD Display. He showed a diagram of the product architecture with the blue OLED emitting layer and a printed quantum dot color conversion layer yielding vivid colors and dimming at a sub-pixel level.

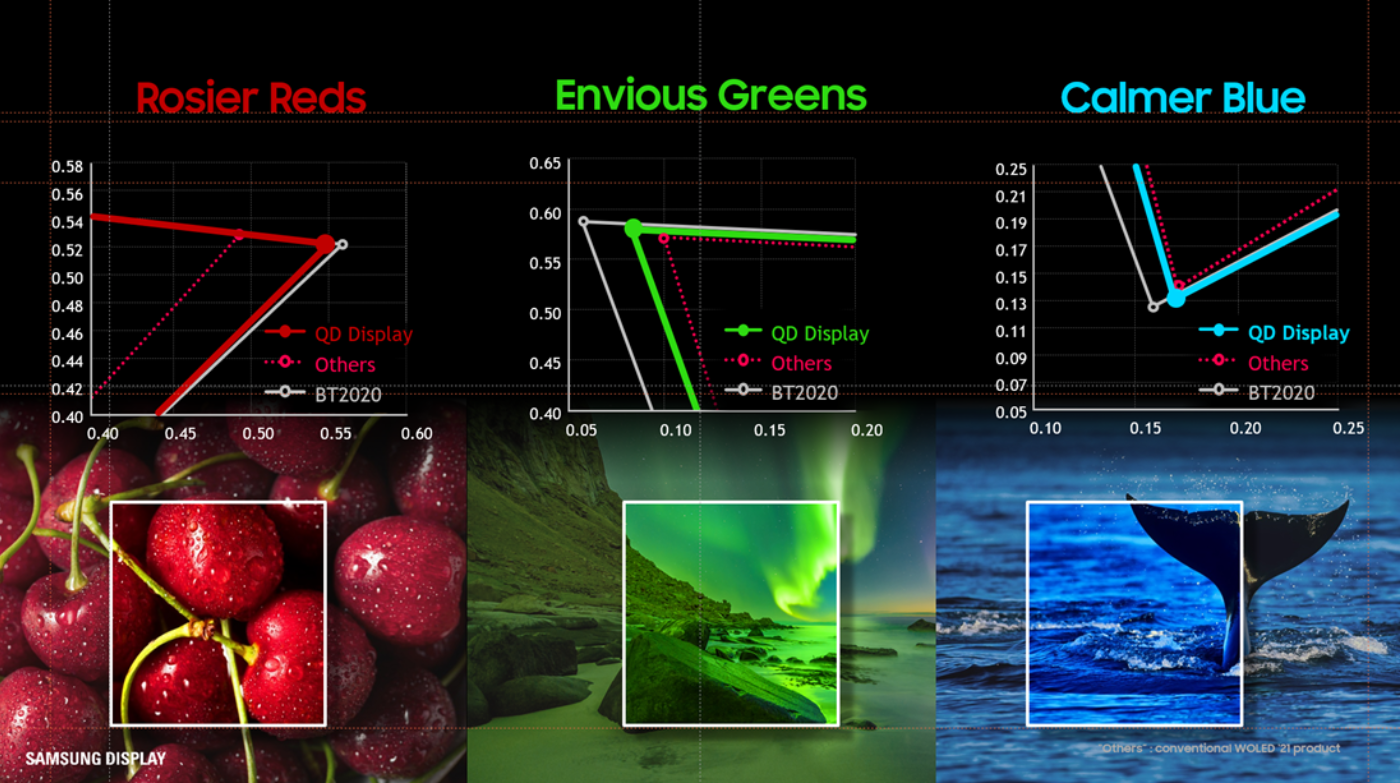

Shah showed a color triangle using the less-familiar 1976 CIE u’v’ space and indicated that QD-OLED achieved 90.3% of the BT-2020 color space while “Others” (presumably white OLED) reached only 75.5%. He showed how for each color QD-OLED surpassed existing products in coming closer to the BT-2020 standard.

Shah then turned to color volume, which in my personal opinion based on the viewing comparison is the key advantage of QD-OLED technology. Because White OLED has limited primary color peaks, QD-OLED can greatly excel in color volume. Shah referred to a color volume metric labeled “IDMS 1.2 CAPL 10% Color Volume DCI P3 ICtCp” and indicated that QD-OLED achieved 125% of the standard while Others achieved only 71%.

The exceptional color volume performance of QD-OLED relates to the advantage in peak brightness in primary colors. QD-OLED achieves peaks for R/G/B of 230/740/89 nits on a 10% window, compared to 85/282/41 for Others.

Shah went on to describe additional benefits of QD-OLED, including black level and contrast performance, viewing angle luminance and color shift, high refresh frequency and an image-sticking protection algorithm.

In the Q&A session following the presentations, the five speakers were joined by Stephen Baker of The NPD Group. Baker is retiring in June from NPD after more than 20 years and his responsibilities will be largely assumed by Paul Gagnon. In response to a query on technology, Baker had insights to share. While admitting that he was uneducated compared to the audience on technology issues, he has great experience in understanding consumer behavior. Baker noted that the term “OLED” has been established as the mark of a premium TV, and the general consumer knows this term. He said that with Samsung’s launch of its QD-OLED TVs, they do not use the term QD-OLED but rather simply “OLED TV”, and he said he thought that was wise of Samsung because the consumer will immediately recognize the term. I have known Stephen Baker for decades and have great respect for his opinion on consumer insights such as this.

To see a review of the additional presentation highlights, readers can subscribe to the DSCC Weekly Review by contacting info@displaysupplychain.co.jp.