Seasonal Slowdown in Mobile Display Fab Utilization Expected

Seasonal Slowdown in Mobile Display Fab Utilization Expected

With the seasonal sales peak for smartphones behind us, utilization at mobile display fabs is expected to decrease in Q1 but remain at a higher level than a year ago, according to the latest release of DSCC’s Quarterly OLED and Mobile LCD Fab Utilization Report (一部実データ付きサンプルをお送りします), issued last week. In Q4’21, total TFT input for all display makers was up 3% Q/Q and 16% Y/Y at 6.5M square meters, and in the current Q1’22, we expect total TFT input to be down 3% Q/Q but still up 15% Y/Y at 6.3M square meters.

The report details capacity, TFT input and utilization for every OLED and LTPS LCD display fab in the industry, more than 40 fabs in all and includes pivot tables to allow segmentation by supplier, country, TFT fab generation, backplane, frontplane or substrate type. The report provides historical utilization back to Q1’17 and a forecast by month for through the first half of 2022.

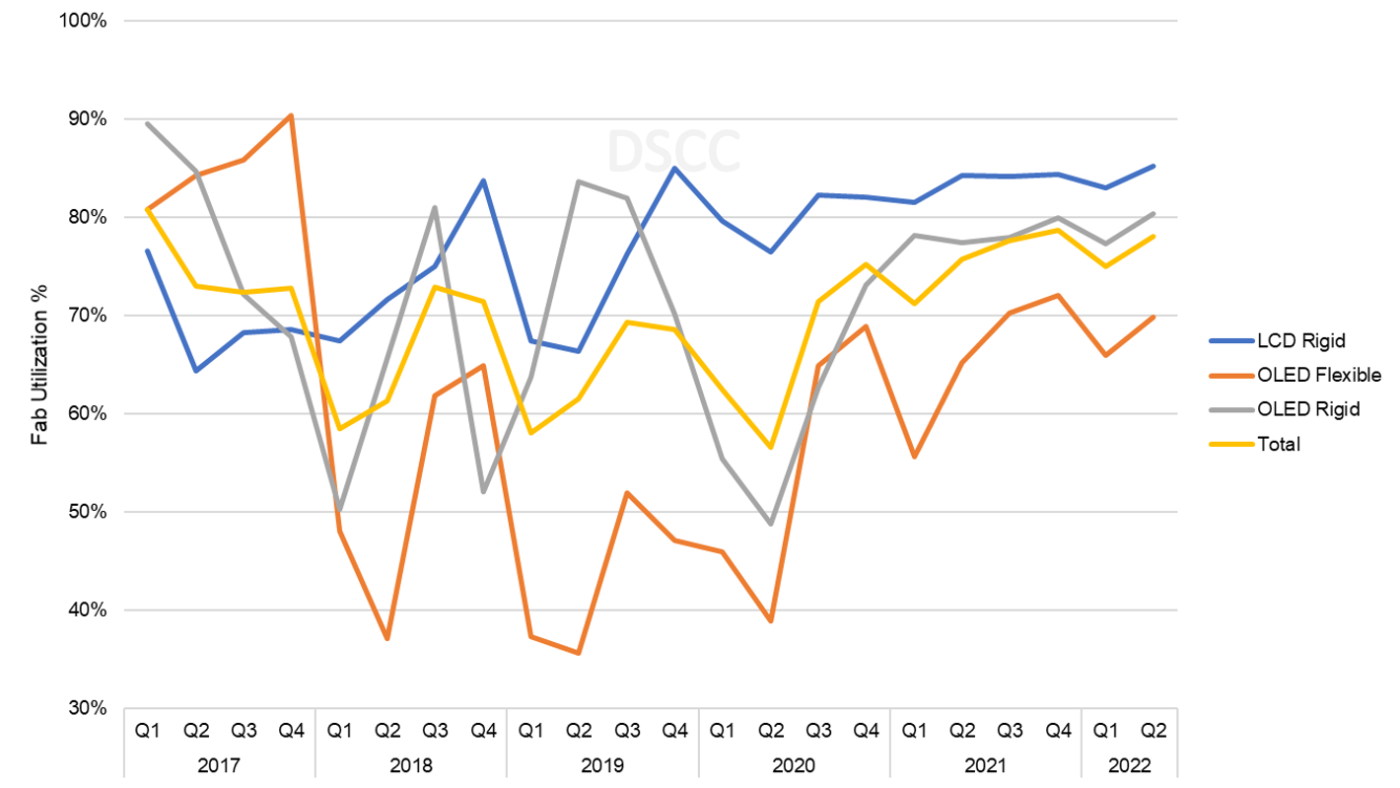

Fab utilization varies substantially by display technology and substrate as shown in the chart here. Flexible OLED fabs have a strong seasonal component but generally ran at very low utilizations in 2018-2019. While there remains a seasonal component, flexible OLED fab utilization has increased substantially in 2021 and into this year.

Quarterly TFT Utilization by Display Technology and Substrate, 2017-2022

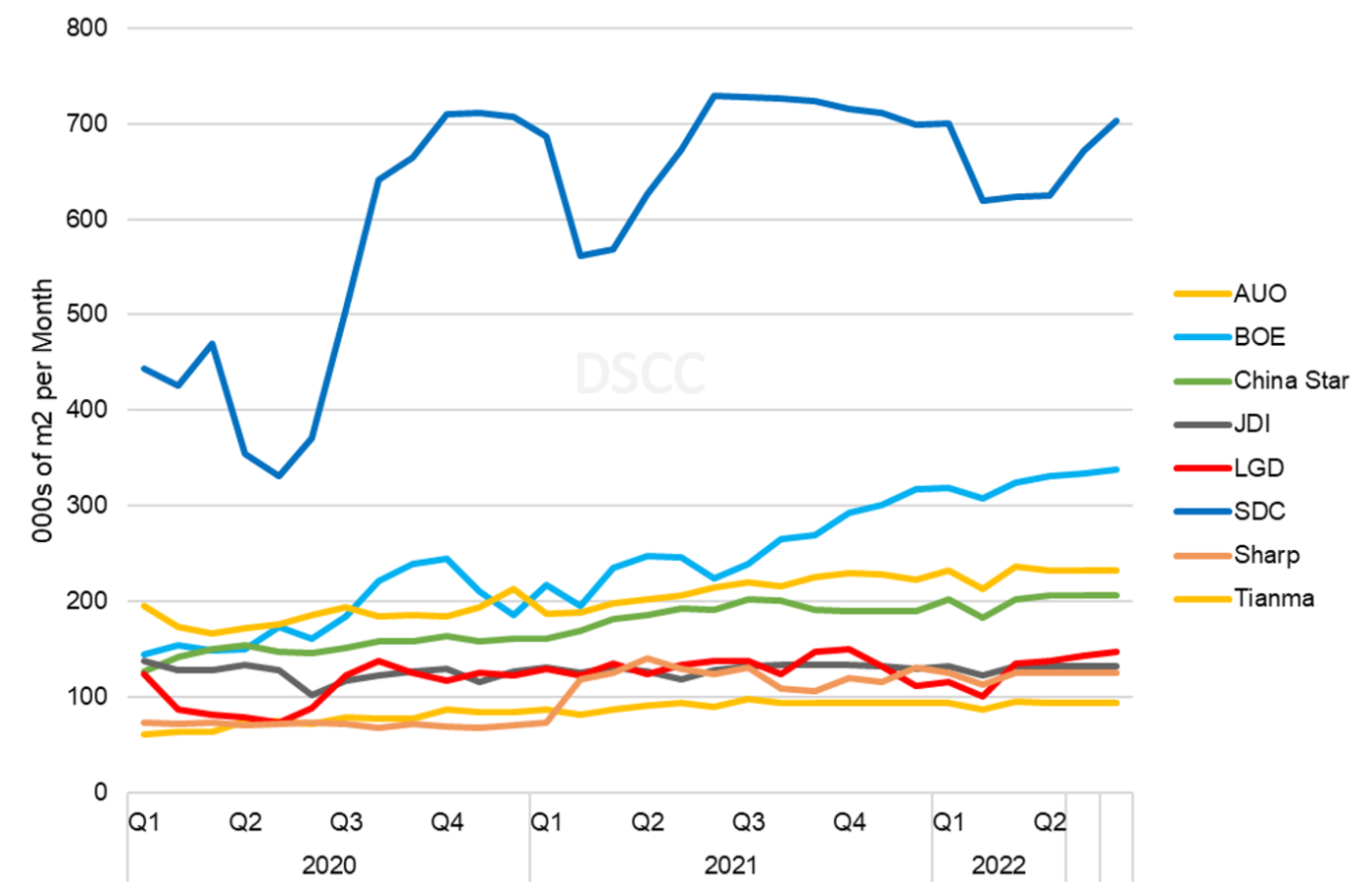

A view of TFT input by panel maker shows the leading position of Samsung Display in this sector, but also the growth of BOE as the Chinese giant continues to add capacity. Although Samsung clearly has the top position, its share of TFT input in Q4’21 was only 33%, and the sector remains competitive with only two other panel makers (BOE and Tianma) exceeding 10% of the market on a TFT input basis.

As seen on the chart, Samsung’s input will decrease Q/Q in Q1’22 but will remain substantially higher than a year ago. As related on Samsung’s earnings call (see separate story in this issue), they see continued strong demand for OLED panels resulting from new product introductions (such as the Galaxy S22 and S21FE) and foldable phones to multiple customers. For its part, although BOE struggled with low utilization on OLED lines after losing Huawei business in 2020, it recovered steadily during 2021 and is bringing new capacity in 2022 with B12 Chongqing.

Monthly TFT Input by Panel Maker, 2020-2022

DSCC’s Quarterly OLED and Mobile LCD Fab Utilization Report (一部実データ付きサンプルをお送りします) provides historical utilization back to Q1'17 and a forecast by month through the first six months of 2022. Readers interested in subscribing to these reports should contact info@displaysupplychain.co.jp.