Panel Maker Q4 Earnings Preview

Panel Maker Q4 Earnings Preview

In the next few weeks, we will see the Q4 earnings announcements for flat panel display makers, starting with LG Display on Wednesday, January 26th. Although price declines will likely bring profits down from historically high levels during the summer, we expect that panel makers will report continued profits to close out the most profitable year in the history of the industry.

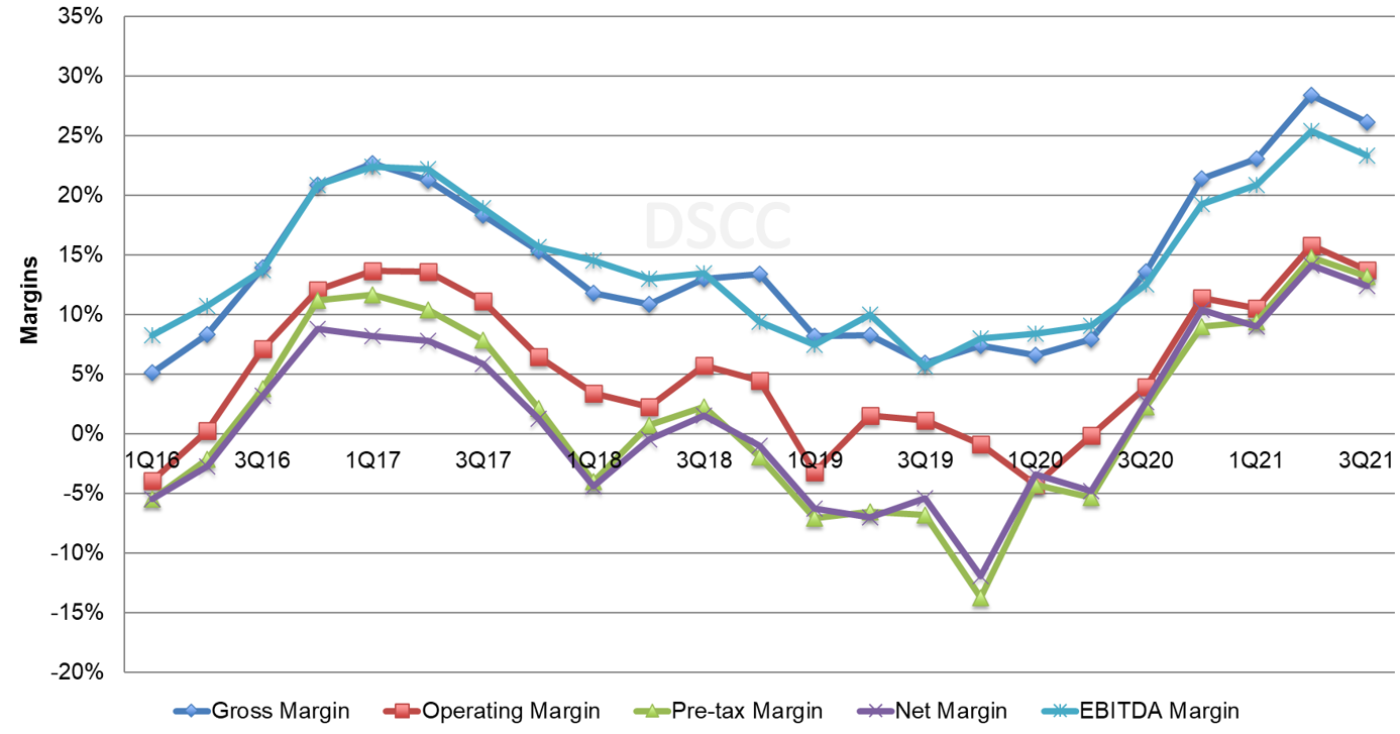

First, let’s set the stage with an industry overview of margins in the first chart here. Margins peaked in Q2 2021, capping a five-quarter run from the bottom of the Crystal Cycle to the top, as shown in the chart here. In Q4 2021, we expect that these margins will be reduced, especially for the companies focused on LCD, as LCD TV panel prices declined by an average of 32% Q/Q, the largest Q/Q price decline ever, in Q4.

Display Maker Quarterly Margins, Q1’16-Q3’21

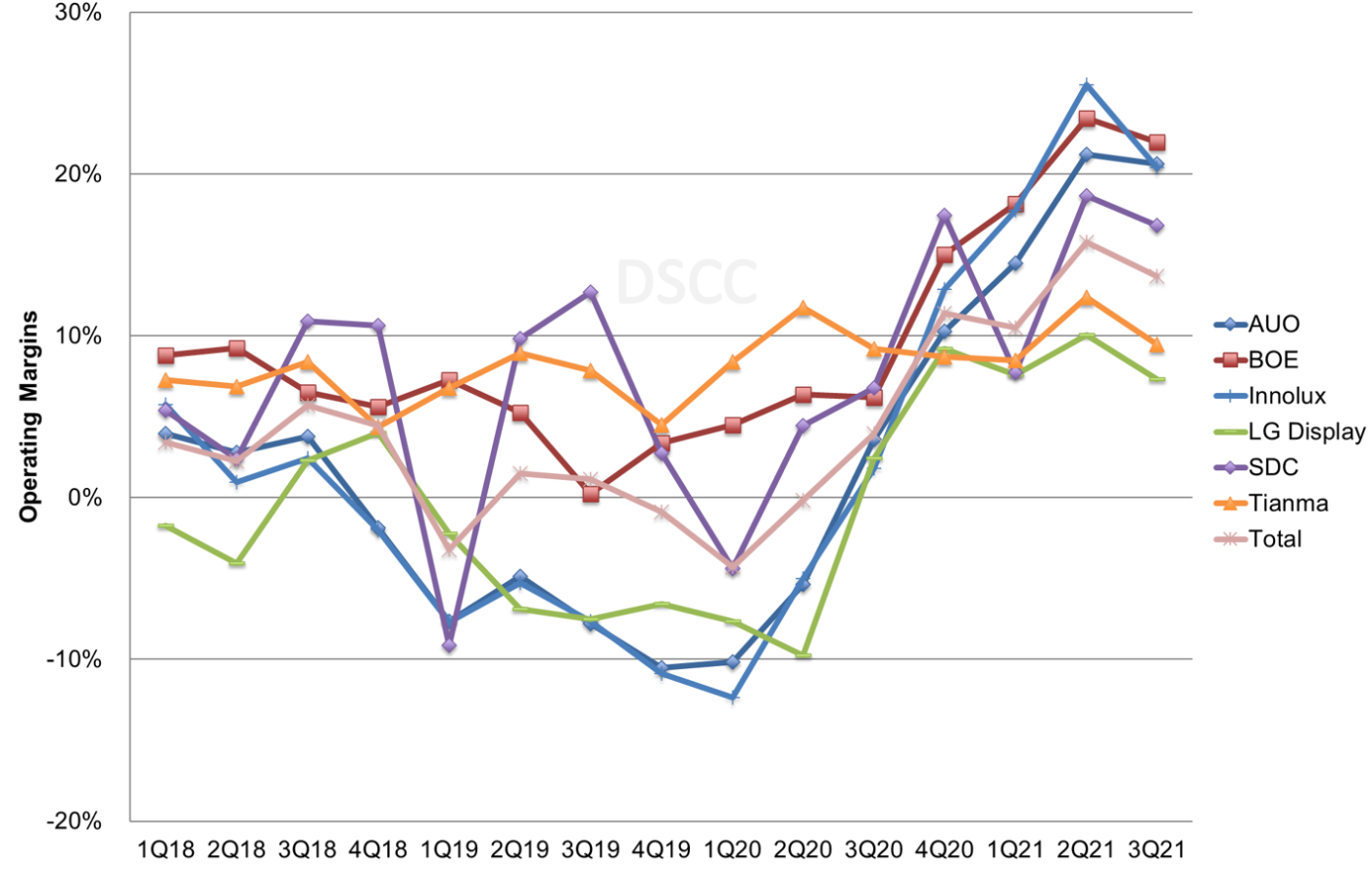

The second chart shows the operating margins of the larger companies in the industry on a shorter timescale of 2018-3Q21. While the trend of the Crystal Cycle is clearly seen, there is a wide divergence of outcomes. Tianma went from outperforming most of the industry in the down cycle to underperforming during the Crystal Cycle peak. SDC also generally sustained positive operating margins during the downturn but did not benefit much from the upswing in LCD panel prices, while AUO, Innolux and LGD have been more sensitive to the cycle.

Display Maker Quarterly Operating Margins, Q1'18-Q3'21

In terms of guidance, companies expressed caution around guidance in their Q3 earnings calls in late October and early November:

- LGD expected area shipments to increase by mid-teen % Q/Q, and area ASPs to increase by mid-single digit % based on increased mobile shipments;

- AUO expected area shipments down by low-single digits % and ASPs down by mid-single digit %;

- Innolux expected large panel shipments down by mid-single digits % Q/Q, small/medium panel shipments down mid-single digits % and blended ASP down by mid-single digits %.

For the Taiwan players, because they report monthly revenues and shipments, we now know that AUO’s revenues decreased by 6% Q/Q, which would be roughly in line with their guidance or perhaps slightly better. Innolux’s revenues declined by 14%, roughly in line with guidance or perhaps slightly worse.

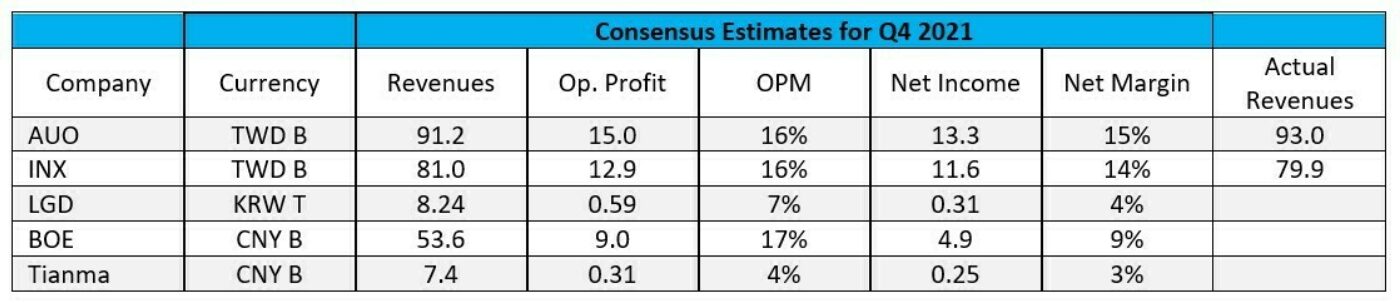

The table below shows analyst expectations for Q4 for the panel makers with analyst coverage, according to marketscreener.com. The analyst expectations for margins seem to be conservative estimates, only slightly lower than Q3, and at least in Taiwan, the panel makers outperformed the expectations for revenue. On the other hand, the consensus expectation for BOE net profits appears to be exactly at the mid-point of the profit range given by the company’s preliminary announcement.

AUO beat consensus revenue estimates by 2%, while Innolux missed consensus by 1%; it is likely that the rest of the income statement will follow the same pattern. LGD’s guidance implies an increase in revenues of about 20%, but consensus estimates predict only a 14% revenue increase Q/Q, so if LGD performed to their guidance they will beat consensus.

According to DSCC’s Quarterly OLED Shipment Report, LGD revenues for OLED shipments increased by 44% Q/Q in Q4, driven mostly by an 86% increase in mobile OLED displays for smartphones and smart watches. Even so, LGD would need to have kept LCD revenues close to flat to beat the consensus revenue estimates.

Perhaps just as important as the results will be the guidance given about 2022. With panel prices declining in the second half of 2021 and continuing concerns about the pandemic, we believe that panel makers will again be cautious about prospects for the new year.