テレビ用液晶パネル価格は2025年第4四半期に下落へ

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

8月と9月に小康状態が続いた後、年末商戦に向けて液晶テレビパネルの価格は再び下落傾向にあります。最近の緩やかな価格変動の傾向は維持されているようですが、価格圧力は下向きです。

いくつかの好調な需要シグナルを受け、パネルメーカーは2025年上半期に稼働率を引き上げました。中国で実施された補助金制度によりテレビ販売台数は緩やかに増加しましたが、一方で、トランプ大統領の関税導入を見越してOEM各社が在庫確保に奔走したため、特にITセクターでは需要が前倒しされました。TFT液晶パネルの投入量は2025年第1四半期に前期比6%増加し、第2四半期は前期比横ばいになると予測しています。6月と7月は減速したものの、8月と9月には稼働率が増加し、サプライチェーンの在庫は高水準に留まりました。

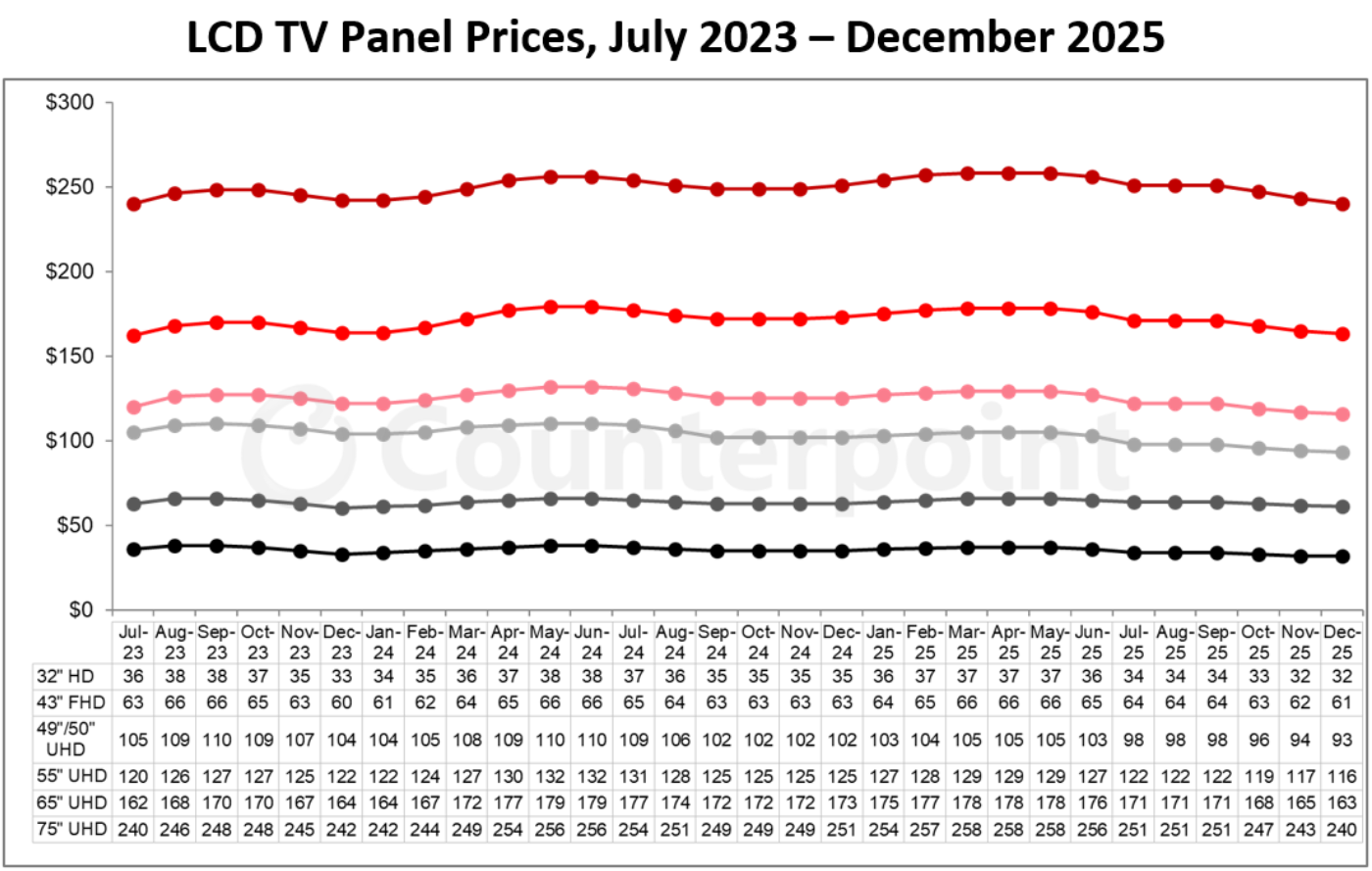

最初のチャートは、2025年12月までのテレビパネル価格予測を含む最新のアップデートを示しています。チャートは2023年夏から始まり、安定期の始まりとなります。3回の緩やかな上昇と3回の緩やかな下落を経験し、現在は3回目の下落の真っ只中にあります。現時点では、この下落の終わりは見えず、2025年末まで続くと予想されます。

LCD TV Panel Prices Heading Down in Q4 2025

After a brief respite in August and September, LCD TV panel prices are heading down again as we approach the holiday sales season. The recent pattern of more gentle price fluctuations seems to be holding but pricing pressure is on the downside.

Some positive demand signals led panel makers to increase utilization in the first half of 2025. A subsidy program implemented in China led to a modest uptick in TV sales, while there was some demand pulled forward, especially in the IT sector, as OEMs rushed to stock inventory in anticipation of Trump’s tariffs. We estimate that TFT LCD input increased 6% QoQ in Q1 2025 and was flat QoQ in Q2 2025. A slowdown in June and July was followed by increasing utilization in August and September, and that has left the supply chain with inventory on the high side.

The first chart here highlights our latest TV panel price update with a forecast through December 2025. The chart starts with the summer of 2023, the beginning of this period of stability. We have seen three mild rallies and three mild slumps, and we are in the middle of the third slump. At this point, we cannot see the end of the slump and expect it to extend to the end of 2025.

Most prices in September came in right in line with our expectations. While we expected prices to be stable MoM for all screen sizes except 85”, we were right about all screen sizes except 85”, which also stayed stable. The prices in our survey were all unchanged in September.

Q1 2025 prices were an average of 2.8% higher than Q4 2024 prices, and although prices started to decline in Q2, the average price was still 0.5% higher than Q1. Prices in Q3 2025 were stable from July to September, but that level was lower than the Q2 prices by 4.5% on average, the largest QoQ decline since 2022.

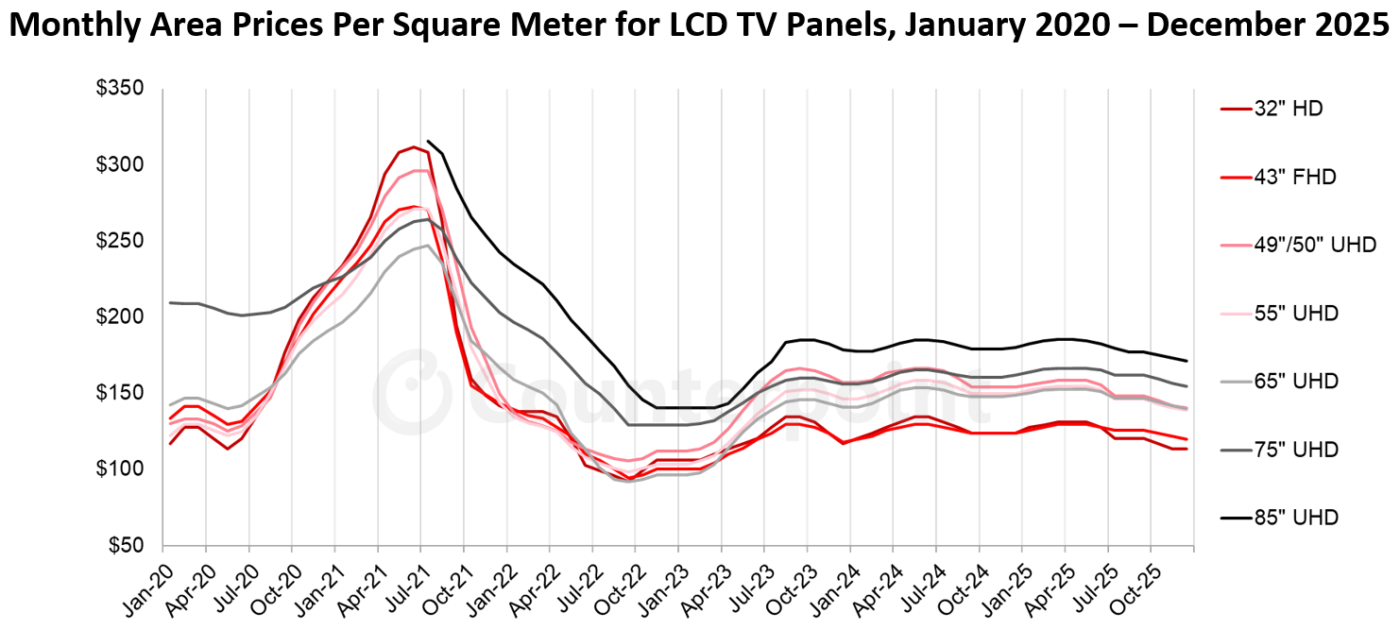

As we look at pricing in terms of area, it has now been more than two years after the pandemic boom and bust that prices have stayed within a narrow range. In this period of stability, the products fall into three levels:

- The lowest-priced products are 32” and 43”, the most commoditized sizes. 32” panels seem to get a kick when prices increase, but then fall back when prices decline. These two products are efficient 18 cuts per substrate on Gen 8.5 (32”) and Gen 10.5 (43”). During the whole period from July 2023 to our forecast out to December 2025, the price of 43” panels has stayed between $118 and $129 per square meter. We forecast that the 32” panel will drop below its most recent minimum of $117 per square meter set in December 2023 and hit a new post-pandemic low of $113 in November and December.

- The mid-tier products are 49”/50”, 55” and 65”, with the largest size usually coming at the highest price. These sizes are also made efficiently on Gen 8.5 (49”/50” and 55”) and Gen 10.5 (65”). These panels have fluctuated between $139 and $167 per square meter and we expect them to fall to the lower end of that range, but not below it.

- The premium products are 75” and 85”. The 75” panel briefly fell to the mid-tier level in 2023 but appears to have regained a premium of ~$15 over the smaller sizes. The 85” panel has fluctuated between $176 and $185 during this period, a premium of $15-$20 per square meter over the 75” panel, but we forecast that it will break through the lower end of that range to $171 per square meter in December, still $16 above the 75” price.

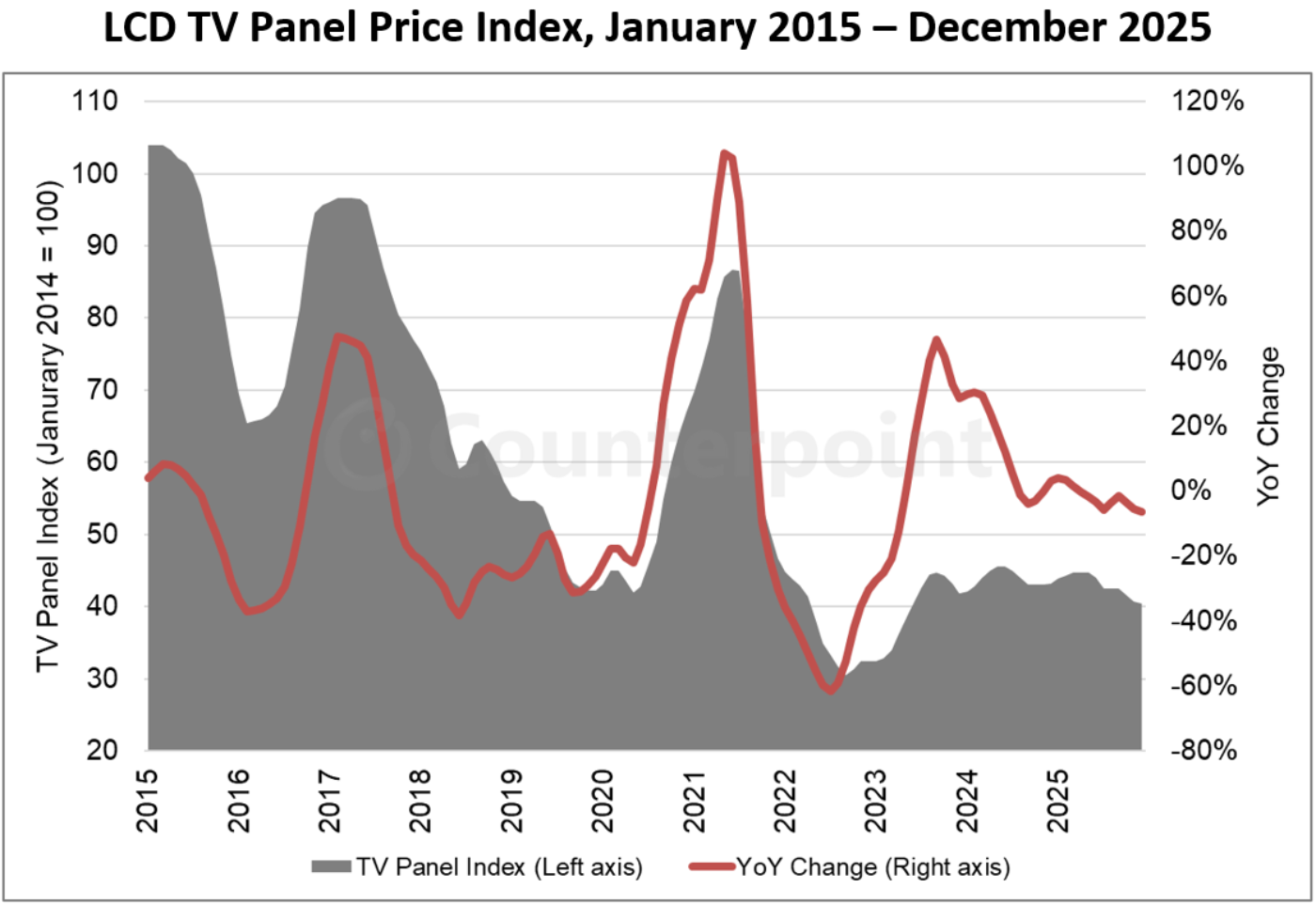

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through June 2025. The price increases in Q1 2025 brought our index up to a peak of 44.8 in March 2025, not quite as high as the peak in 2024 but still 47% higher than the all-time low of September 2022. Q3 2025 prices stabilized at 42.5, but we see prices declining in Q4 to 40.4, the lowest point since June 2023.

Following the red line in the chart, we can see that the period from mid-2023 to today is radically different than the period from 2015 to 2023. We no longer have wild swings in prices. As of September 2025, our price index remained within a relatively tight range of 40.7 to 45.6 for 26 months, and we expect that prices will stay within this range at least through December 2025.

Overall, prices seem to be fluctuating around a level that allows the Chinese panel makers, with a cost advantage from government subsidies, to make a small profit, while Taiwanese panel makers come close to breakeven. With Q3 2025 prices down by 4.5% QoQ, we expect that profits for these panel makers will be squeezed.

[ご案内] FPD産業分析セミナー 2025年後期版