[新着] 液晶テレビパネル価格は2025年第4四半期も引き続き下落

[ご案内] カウンターポイント TECHセミナー 2025

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

LCD TV Panel Prices Continue to Slide in Q4 2025

LCD TV panel prices are heading down again as we approach the holiday sales season. The recent pattern of more gentle price fluctuations seems to be holding, but pricing pressure is on the downside.

After some positive demand signals in the first months of 2025, the global TV market has become stagnant. High panel maker utilization in August and September has left the supply chain with inventory on the high side, and the major TV set OEMs are pushing for lower prices to improve their own margins, which have been decimated by fierce competition.

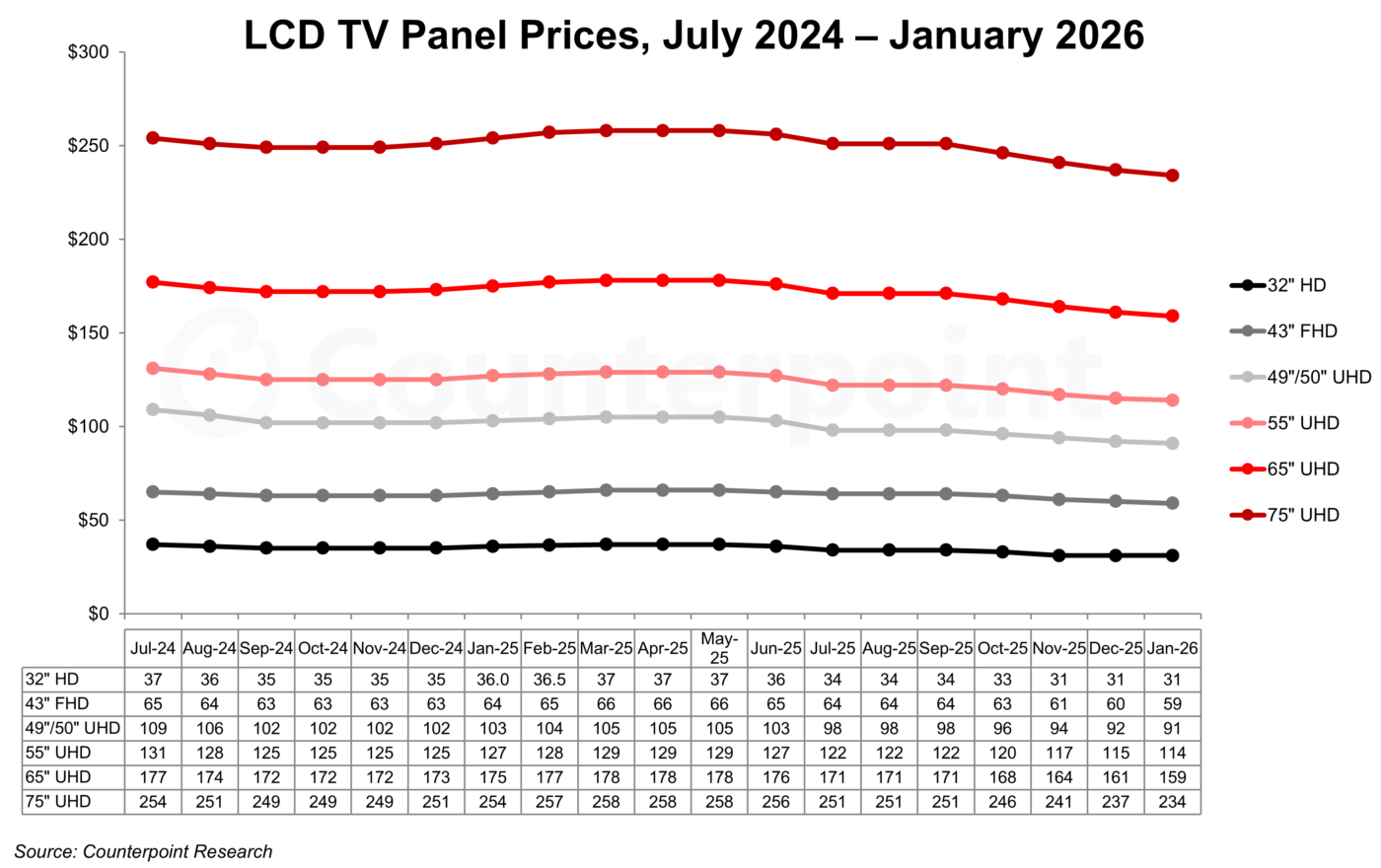

The first chart here highlights our latest TV panel price update with a forecast through January 2026. The chart starts with the summer of 2024, well into this period of stability. Since 2023, we have seen three mild rallies and three mild slumps, and we are in the middle of the third slump. At this point, we cannot see the end of the slump and expect it to extend into 2026.

Most prices in October came in right in line with our expectations. We expected prices to decline MoM for all screen sizes, and we were right about that, but prices for the largest sizes – 75” and 85” – declined more than we expected, while the price for 49”/50” declined slightly less than we expected.

Q1 2025 prices were an average of 2.8% higher QoQ, and the average price in Q2 2025 was 0.5% higher than Q1. Prices in Q3 2025 were lower sequentially by 4.5% on average, the largest QoQ decline since 2022. We expect Q4 2025 prices to be down by another 4.4% on average.

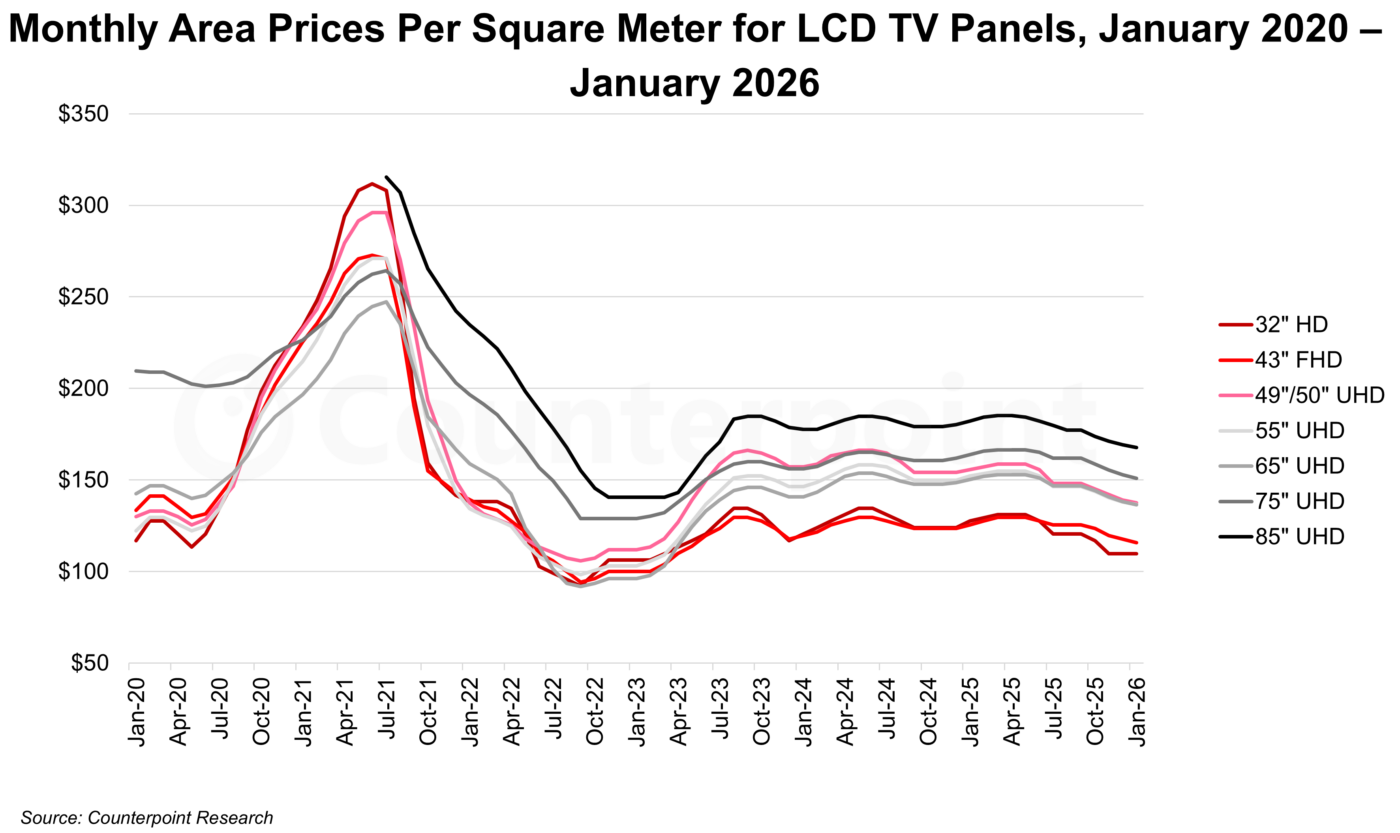

As we look at pricing in terms of area, it has now been more than two years after the pandemic boom and bust that prices have stayed within a narrow range. In this period of stability, the products fall into three levels:

- The lowest-priced products are 32” and 43”, the most commoditized sizes. 32” panels seem to get a kick when prices increase, but then fall back when prices decline. These two products are efficient 18 cuts per substrate on Gen 8.5 (32”) and Gen 10.5 (43”). During the whole period from July 2023 to our forecast out to December 2025, the price of 43” panels has stayed between $118 and $129 per square meter, but the price drops to $116 per square meter in January 2026 in our forecast. We forecast that the 32” panel will hit a new post-pandemic low of $110 in November and then plateau at that level through January.

- The mid-tier products are 49”/50”, 55” and 65”, with the largest size usually coming at the highest price. These sizes are also made efficiently on Gen 8.5 (49”/50” 8-up and 55” 6-up) and Gen 10.5 (65” 8-up). These panels have fluctuated between $139 and $167 per square meter and we expect them to fall to the lower end of that range, but not below it.

- The premium products are 75” and 85”. The 75” panel briefly fell to the mid-tier level in 2023 but appears to have regained a premium of ~$15 over the smaller sizes. The 85” panel has maintained a premium of $15-$20 per square meter over the 75” panel, and we expect that premium to continue. But the 85” price will decline to a new post-pandemic low of $168 per square meter.

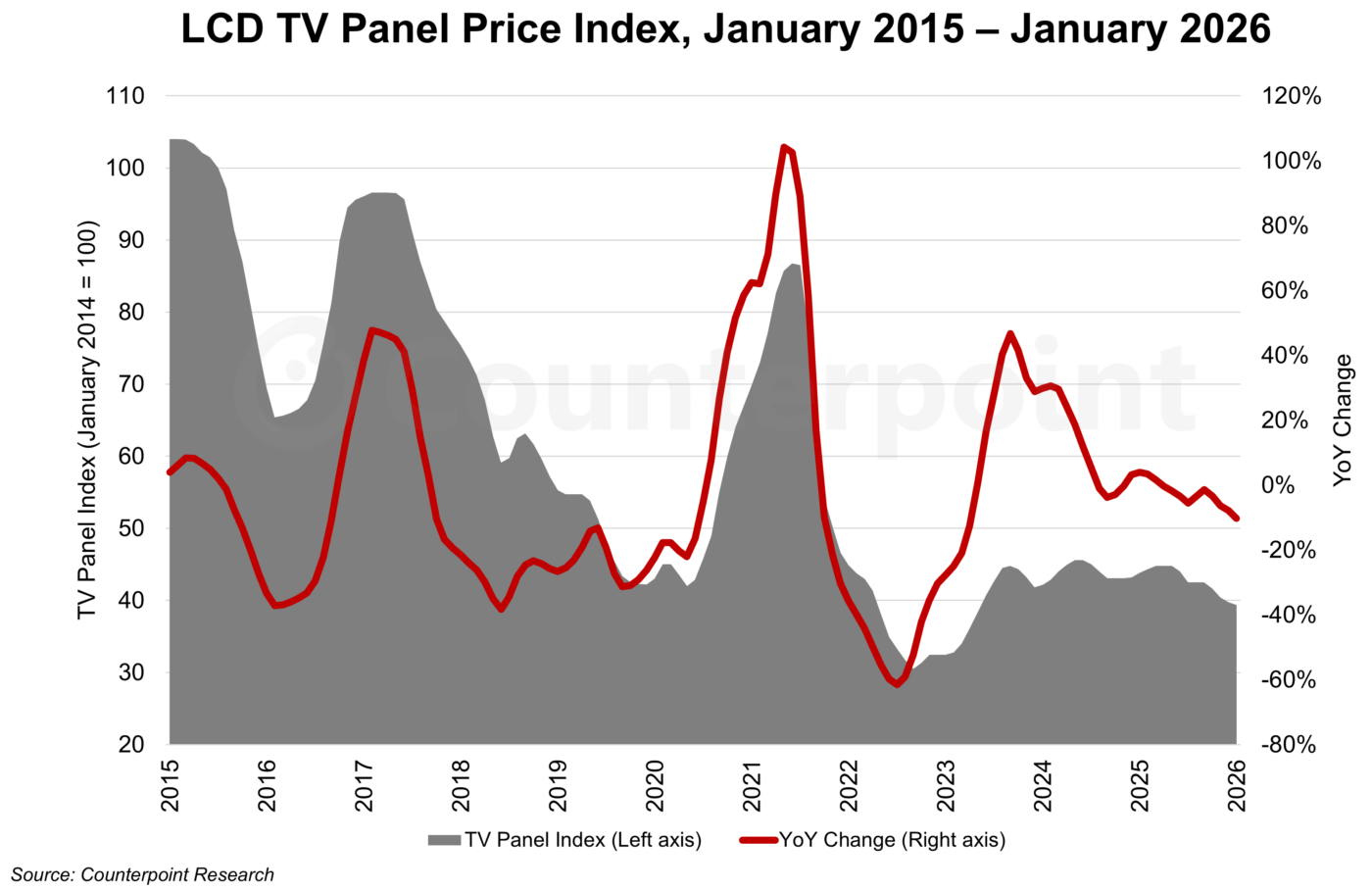

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through January 2026. The price increases in Q1 2025 brought our index up to a peak of 44.8 in March 2025, not quite as high as the peak in 2024 but still 47% higher than the all-time low of September 2022. Q3 2025 prices stabilized at 42.5, but we see prices declining to 39.4 in January, the lowest point since May 2023.

Following the red line in the chart, we can see that the period from mid-2023 to today is radically different than the period from 2015 to 2023. We no longer have wild swings in prices. As of October 2025, our price index remained within a relatively tight range of 40.7 to 45.6 for 27 months, but we expect that prices will break through the lower end of this range in November and continue to fall through January.

Panel makers have dialed back their utilization in Q4 2025 in an effort to slow the price decline, but the “tap on the brakes” seems to be insufficient to reverse the downward trend. Panel prices have been fluctuating around a level that allows the Chinese panel makers, with a cost advantage from government subsidies, to make a small profit, while Taiwanese panel makers come close to breakeven. The profitability of the Chinese panel makers may be tested in the fourth quarter.

[ご案内] FPD産業分析セミナー 2025年後期版