TV用LCD価格月報~第2四半期も引き続き上昇

本記事は、毎週火曜日 (日本時間) に発刊される有償商品 DSCC Weekly Review 4月1日号の掲載データを小改訂したものです。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

2月に始まり3月も続いているTV用LCD価格の上昇は第2四半期も継続の見通しで、FPDメーカーにとっては明るい兆しとなっている。価格上昇は劇的と言うには程遠いものの、採算が厳しいFPDメーカーにとっては一息つける状況だ。

Q4'23とQ1'24にはFPDメーカー各社が稼働率を抑制、各種スポーツイベントによる年央の需要に対する期待感も重なり、価格上昇圧力につながっている。DSCCの Quarterly All Display Fab Utilization Report (2月1日発刊) によると、LCDメーカーの稼働率はQ3’23の85%からQ4’23は76%に、Q1’24には72%に抑えているものと推定される。LCD TFT総投入量はQ4’23に前期比11%減となり、Q1’24にはさらに前期比5%減と見込まれてる。今年の旧正月休暇は複数のFPDメーカーが通常1週間の操業停止を2週間に延長している。

LCD TV Panel Price Increases Continuing into Q2

The rally in LCD TV panel prices which started in February is continuing in March and into Q2, a favorable sign for panel makers. While the price increases are far from dramatic, they represent a respite for panel makers challenged for profitability.

The restraint in utilizations by panel makers in Q4’23 and Q1’24 has combined with some anticipation of mid-year demand from sports events, leading to upward pressure on prices. Based on DSCC’s Quarterly All Display Fab Utilization Report, LCD makers slowed their utilization from 85% in Q3’23 to 76% in Q4’23 and an estimated 72% in Q1’24. Total LCD TFT input declined 11% Q/Q in Q4 and is expected to decline another 5% Q/Q in Q1’24. This year several panel makers have extended the normal one-week shutdown for the Lunar New Year holiday and have taken a two-week shutdown.

Although TV demand has remained weak, panel makers have been disciplined to keep their own inventory low and with low shipment numbers in Q4, the downstream inventory has been reduced. In the lean inventory environment, the closure of the Red Sea shipping lanes from war in the Middle East has resulted in longer shipping times to Europe. TV makers have pushed to get shipments earlier to prepare for promotions for two big sporting events there: Euro Cup in June and the Paris Olympics in August.

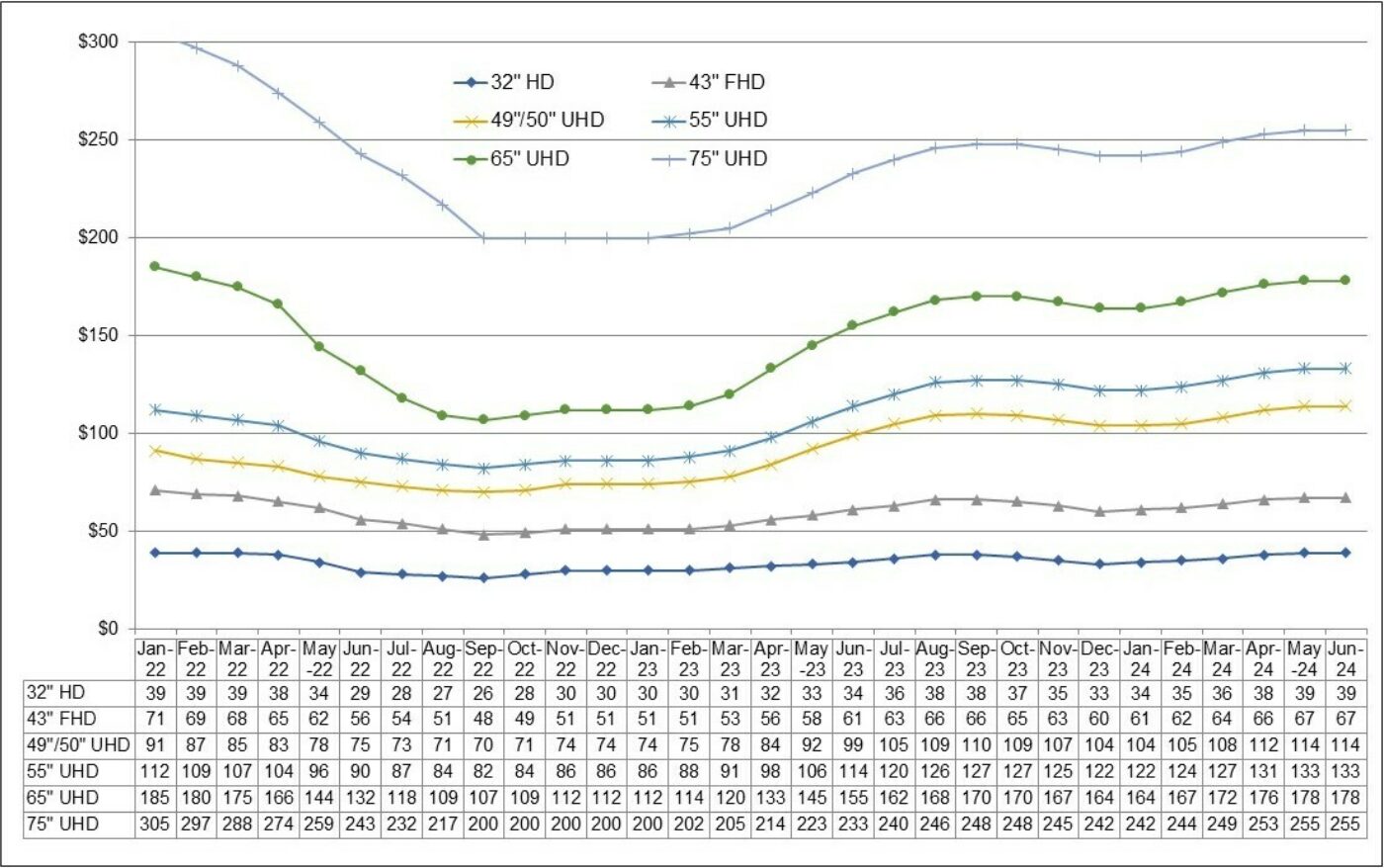

The first chart here highlights our latest TV panel price update with a forecast to June 2024, starting with the tail end of the post-pandemic price plunge which ran from mid-2021 to summer 2022. Prices hit their all-time lows in September 2022 and increased modestly in Q4’22 and Q1’23 before larger price increases covered Q2’23 and Q3’23. Some prices for March came in higher than our expectations, and prices for April are continuing to increase. We expect the upward trend to continue in May but then to plateau heading into Q3’24.

LCD TV Panel Prices, January 2022 – June 2024

After double-digit percentage increases on average for LCD TV panel prices in both Q2’23 and Q3’23, we saw panel prices decline in Q4’23 by 1.9% on average, with smaller panels showing larger declines while larger panels were close to zero change Q/Q.

Prices in Q1 were nearly flat on average Q/Q, with some sizes showing small Q/Q declines and a few showing small Q/Q increases, but the pattern of prices in Q4 and Q1 implies a robust average price increase in Q2. Prices in Q4 and Q1 conform to a “V” shape, with prices declining from October to December, reaching a bottom in December/January, and increasing from January to March. Prices in Q2 start at the top of the “V” and increase from there, so we now estimate that average Q2 prices will be 6.9% higher than Q1, with larger increases for smaller sizes.

As we look at pricing on an area basis, we are seeing a pattern characteristic of a supply constraint. The smallest TV panel size in our index, 32”, is the ‘canary in the coal mine’ of pricing in the industry. The prices for 32” panels are the first to go up with a supply constraint and are the first to go down in an oversupply. We are seeing that pattern bear out in the current rally and the premium for large screens compared to 32” is narrowing.

At the most recent low point in December 2023, 32” and 43” panels had the lowest area price at $117 and $118 per square meter, respectively, but area prices were higher for 65” ($141), 55” ($146), 75” ($156) and 49/50” ($157). The area price premium for 65” panels over 32” panels was 21% in December, but with our current forecast it is reduced to 11% in May.

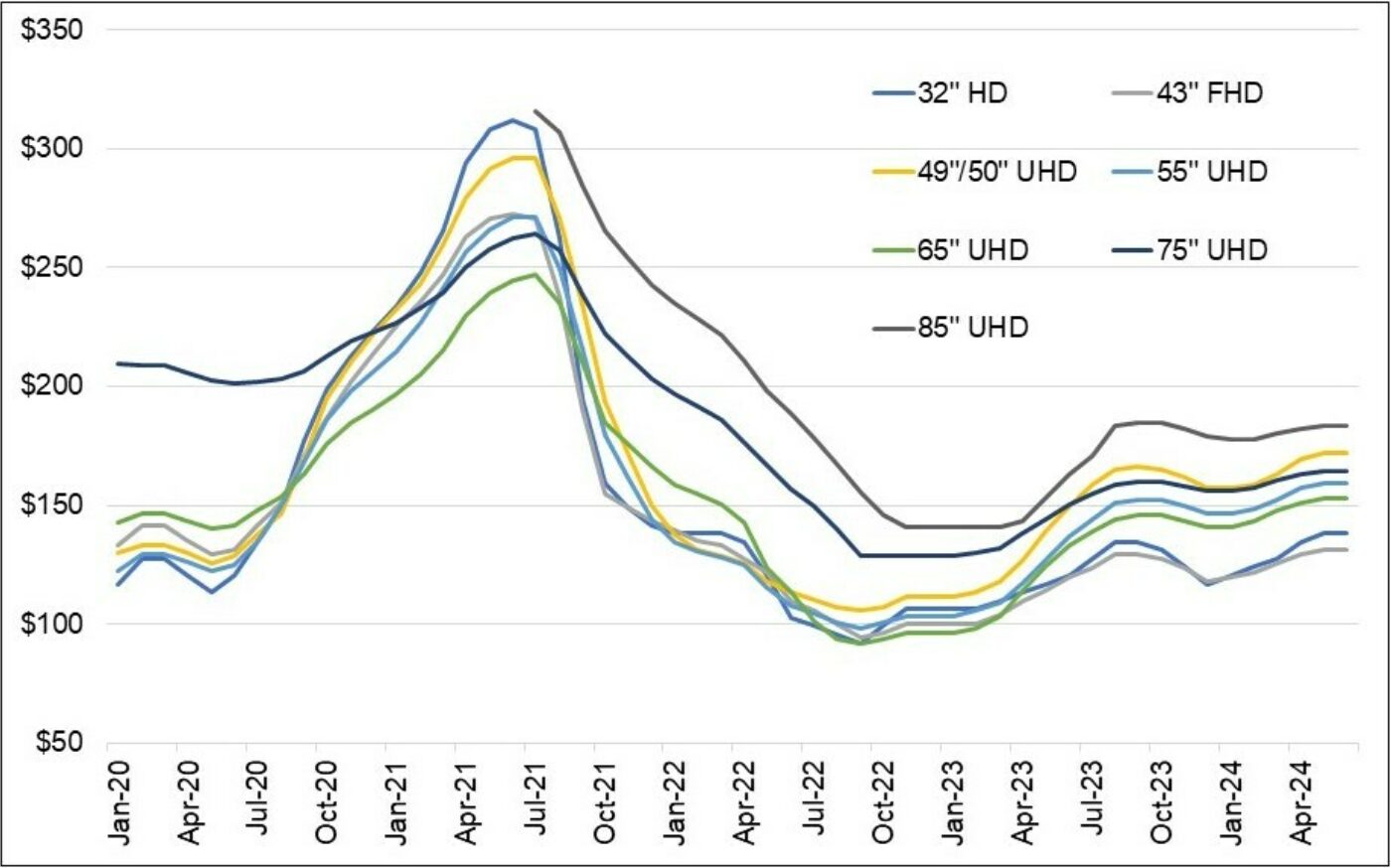

Monthly Area Prices per Square Meter for LCD TV, January 2020 – June 2024

The prices for 49”/50” have been especially strong in this up-cycle, while prices for 43” panels are now the lowest in the industry. The premium for 49”/50” over 43” is expected to increase to 31% in May, which favors panel makers with Gen 8.5 capacity at the expense of those with Gen 10.5 capacity. Gen 10.5 fabs can make 43” very efficiently with an 18-up configuration, but do not have an efficient cut for 49”/50”, while Gen 8.5 fabs can make 49”/50” panels efficiently with an 8-up configuration.

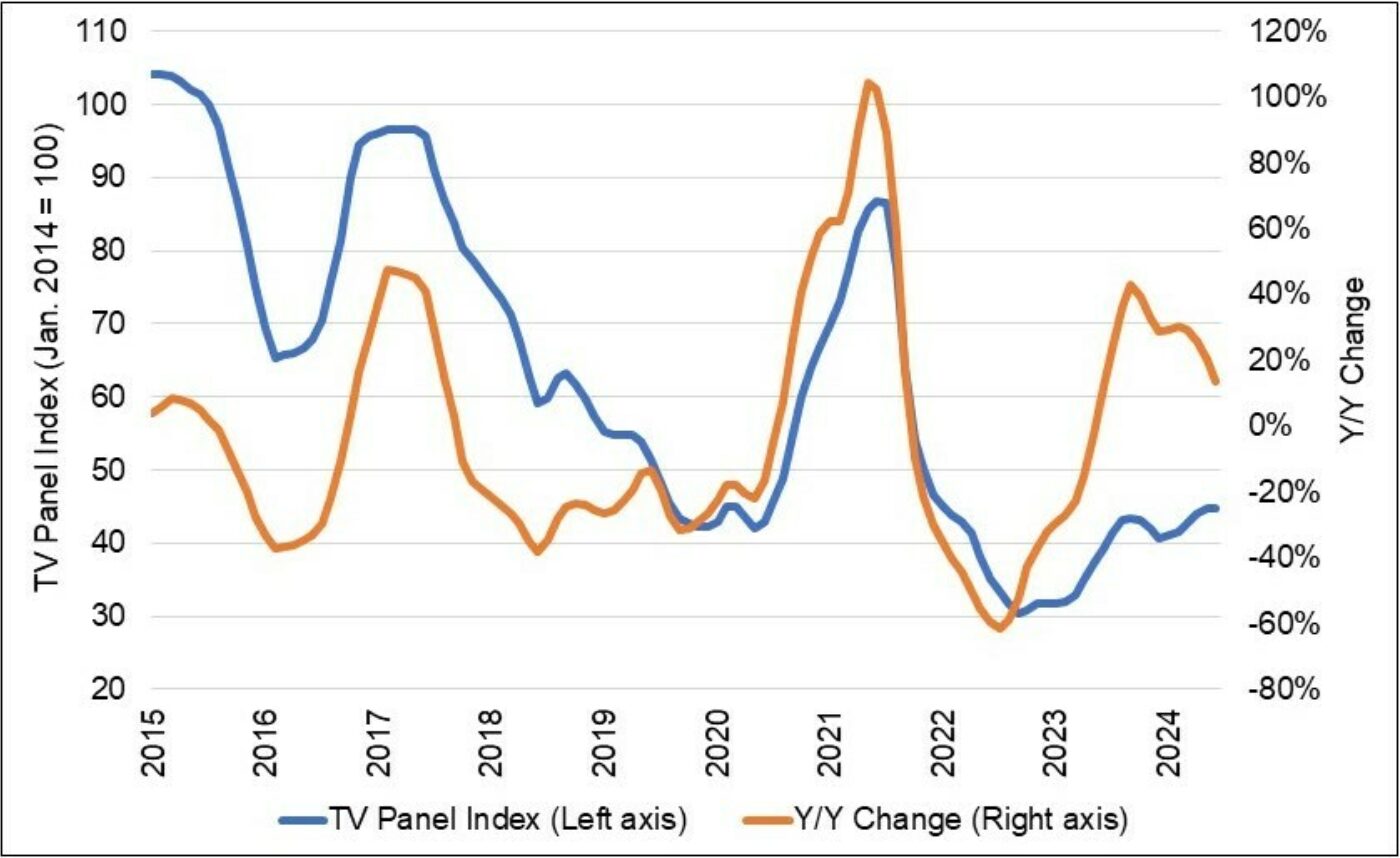

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through April 2024. The price increases in Q3 2023 brought our index up to a peak of 43.4 in September 2023, an increase of 42% compared to the low of 30.5 in September 2022. The index declined to 40.7 in December, which was down 6% from the recent peak but still up 29% Y/Y and up 34% compared to the all-time low. We now expect that by May 2024 the price index will increase to 44.7, surpassing its recent high of September 2023 and 47% higher than its all- time low of September 2022.

LCD TV Panel Price Index, January 2015 – June 2024

Since the average price in Q1 did not have a big increase compared to Q4, we expect that panel maker earnings for the first quarter will remain bleak. However, the price momentum into Q2 is likely to lead to bullish expectations for second quarter profits for panel makers.

The price increases in 2024 need to be kept in perspective. A glance at the charts above shows that in the long down-cycle from 2017 to 2020 there were several periods with modest price increases followed by another down- ward trend. Restraint in utilization has allowed panel makers to generate a short-term uptick, but the industry’s capacity still far outstrips the likely demand for the foreseeable future. Panel makers will need to continue their disciplined ways to avoid another down cycle in the second half of the year.