2024年の車載用FPD出荷、数量・金額・面積のいずれも過去最高を記録

出典調査レポート Semi-Annual Automotive Display Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

- 車載用FPD出荷数が車両出荷数とともに緩やかに成長した一方、車載ディスプレイの大型化と高機能化により、出荷額と出荷面積が急速に成長している。特に、電気自動車 (EV) とハイブリッド車は内燃機関車 (ICE) に比べて搭載ディスプレイの平均画面サイズがかなり大きく、ディスプレイの成長をけん引している。

- 搭載ディスプレイの金額ベースでは、Toyotaが3年以上連続で第1位ブランドの座を維持、TeslaのModel Yが2年連続で第1位モデルの座を維持した。

- Counterpoint ResearchがQ1'22からQ4'24の乗用車向けFPDのモデル別出荷数に関する最新レポートを発刊した。このレポートはデジタル・インフォメーション・クラスタ (DIC) およびセンター・インフォメーション・ディスプレイ (CID) を対象としている。乗用車搭載パネルの価格情報も掲載している。

車載用FPDは、自動車メーカーによる車両1台あたりのディスプレイの大型化・高機能化・搭載数の増加といった流れを背景に、今後の成長が期待される分野である。2024年、デジタル・インフォメーション・クラスタ (DIC) およびセンター・インフォメーション・ディスプレイ (CID) の出荷は、車両出荷タイミングに基づく数量ベースでは2%増にとどまった一方、金額ベースでは5%増、面積ベースでは12%増を記録した。Counterpoint Researchが発刊した、乗用車向け車載用FPD出荷 (車種別・DICおよびCID単位) に関するレポートで明らかになった。このレポートはQ1'22からQ4'24の期間を対象としている。

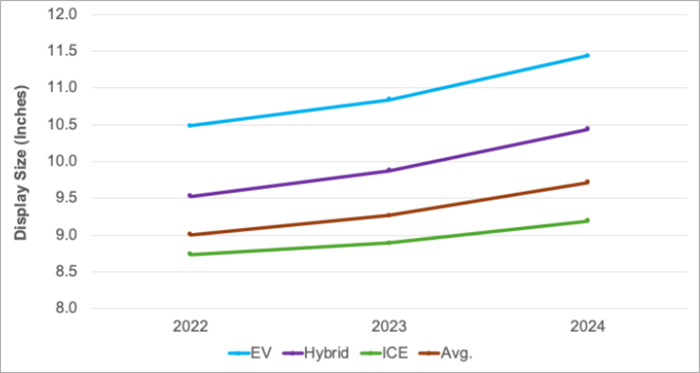

ディスプレイの平均サイズは9インチから10インチに拡大しており、成長著しいハイブリッド車や電気自動車 (EV) の搭載ディスプレイは内燃機関車 (ICE) よりも1-2インチ大きくなっている (下図参照) 。EVおよびハイブリッド車向けディスプレイの合計シェアは、数量ベースでは2022年の23%から2024年には32%に、金額ベースでは2022年の31%から2024年には43%に上昇している。自動車ブランド各社は、同乗者がドライバーの運転を妨げることなくお気に入りのコンテンツを視聴できるよう、プライバシースクリーン付き大型ディスプレイを乗用車に採用している。このレポートの次期版では、DICおよびCID以外の乗用車向けやその他車種向けのディスプレイも追加予定となっており、これらも車載ディスプレイの成長加速に貢献すると見られている。

車載ディスプレイの平均サイズ推移 (パワートレイン別)

Source: Counterpoint Research's Semi-Annual Automotive Display Shipment Report

車載ディスプレイは性能も向上している。Counterpoint Researchでは、自動車ブランド各社が低性能の旧式a-Si TFT LCDから高性能のLTPS LCD、MiniLED LCD、およびOLEDへと移行している状況を観測している。a-Siのシェアが2022年の81%から2024年には74%に低下した一方、LTPS LCDのシェアは数量ベースで19%から26%に上昇している。車載用LTPSはQ4'24に初めてa-Siを金額ベースで上回り、LTPSは3-4インチ大きいサイズが主流となっている。

Counterpoint ResearchのバイスプレジデントであるRoss Youngによると、LTPS LCDは移動度が高くトランジスタが小さいため、解像度や輝度が高く、日光の下で読みやすく、消費電力や表面温度は低く抑えられるため、シェアが拡大している。LTPSバックプレーンは、バッテリー寿命を延ばす手段の一つとして、電気自動車での採用率が非常に高くなっている。自動車ブランド各社はOLEDやMiniLEDも採用しており、より優れたディスプレイ性能を実現するとともに、OLEDでは他のモデルや競合他社との差別化を図る目的で革新的なフォームファクターが採用されている。OLEDとMiniLEDの2024年のシェアは数量ベースでわずか1%強だが、金額ベースでは8%以上を占めている。

ブランド別では、Toyotaが車載用FPD調達シェア (金額ベース)で3年以上連続の首位となった。中国のBYDは2023年にVolkswagenを抜いて第2位に浮上、2023年と2024年ともにトップ10ブランドのなかで最も高い成長を記録している。トップ20の内訳を見ると、中国ブランドが6、次いで米国が5、欧州が4、日本が3、韓国が2という顔ぶれである。

モデル別では、大型の15.4インチ LTPS LCDを搭載しているTeslaのModel Yが金額ベースで首位を維持している。BYDのSongとBuickのEnvisionが僅差で続く。2024年のトップ20には米国ブランドから8モデルがランクイン、次いで中国ブランドから5モデル、日本ブランドから3モデル、韓国と欧州から各2モデルがランクインしている。

------------------------------------

Counterpoint Researchは5月13-14日にSan Jose Convention Centerで2025 SID Business Confereを開催します。同カンファレンスでは、Counterpoint Researchのほか、Tianma Microelectronics、Elektrobit、GlobalFoundries、VueRealを含む参加企業の皆様より、豊富な車載ディスプレイ関連コンテンツが提供されます。カンファレンスの詳細と登録については、以下のウェブページをご覧ください。

出典調査レポート Semi-Annual Automotive Display Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Automotive Display Shipments, Revenues, Area Reach New Heights in 2024

- While display unit shipments grew slowly along with vehicle shipments, display revenues and display area grew much faster due to vehicle displays becoming bigger and more advanced. In particular, electric vehicles (EVs) and hybrids are driving display growth as they adopt significantly larger displays on average than internal combustion engine (ICE) vehicles.

- Toyota remained the #1 brand on a display revenue basis for at least the third straight year, while Tesla’s Model Y remained the #1 car model on a display revenue basis for the second straight year.

- Counterpoint Research has released its latest shipment report on automotive displays for passenger vehicles on a model-by-model basis, covering the Q1 2022-Q4 2024 period. The report covers the digital information cluster (DIC) and center information displays (CID). Prices are provided for each panel used in passenger vehicles.

Automotive displays are well positioned for future growth as car manufacturers incorporate bigger, better and more displays per car. While the digital information cluster (DIC) and center information displays (CID) grew 2% in 2024 in terms of units based on a vehicle shipment timeline, they grew 5% in terms of display revenue and 12% in terms of display area, according to Counterpoint Research’s latest shipment report on automotive displays for passenger vehicles on a model-by-model, DIC and CID basis. The report covers the Q1 2022-Q4 2024 period.

The average display size has grown from 9” to 10” with faster-growing hybrids and electric vehicles (EVs) adopting displays 1”-2” larger than those found in internal combustion engine (ICE) vehicles (see graph below). EV and hybrid displays rose from a combined 23% share on a unit basis in 2022 to 32% in 2024 and from 31% in 2022 to 43% in 2024 on a display revenue basis. Car brands are also adopting large passenger displays with privacy screens to allow passengers to view their favorite content without engaging the driver. Passenger and other types of vehicle displays besides DICs and CIDs will be added to the next version of this report, which should help accelerate automotive display growth.

Automotive displays are also getting better. Counterpoint is seeing car brands migrating from lower-performance, legacy a-Si TFT LCDs to better-performing LTPS LCDs, MiniLED LCDs and OLEDs. The a-Si share has fallen from 81% in 2022 to 74% in 2024 while LTPS LCDs have grown from 19% to 26% on a unit basis. LTPS automotive panels overtook a-Si panels on a revenue basis for the first time in Q4 2024 and they tend to be 3”-4” larger.

According to Ross Young, Vice President at Counterpoint Research, LTPS LCDs are gaining share for their higher mobility and smaller transistors, which translate to higher resolution, higher brightness, improved sunlight readability, lower power and lower surface temperatures. LTPS backplane adoption is very high in EVs as another way to extend battery life. Car brands are also adopting OLEDs and MiniLEDs to deliver even better display performance as well as innovative form factors in the case of OLEDs to differentiate from other models and competitors. OLEDs and MiniLEDs accounted for just over 1% of units in 2024 but over 8% of revenues.

Toyota was the top buyer of automotive displays on a revenue basis for at least the third straight year. China’s BYD overtook Volkswagen for the #2 spot in 2023 and rose the fastest among the top 10 brands in both 2023 and 2024. Overall, there were six Chinese brands in the top 20 followed by five from the US, four from Europe, three from Japan and two from South Korea.

Tesla’s Model Y remained the #1 model on a display revenue basis due to its large 15.4” LTPS LCD. It was closely followed by BYD’s Song and Buick’s Envision. Overall, there were eight models from US brands in the top 20 in 2024, followed by five from Chinese brands, three from Japanese brands and two each from South Korea and Europe.

Counterpoint Research is hosting the SID Business Conference on May 13 and 14 at the San Jose Convention Center where there will be plenty of automotive display content from Counterpoint Research, Tianma Microelectronics, Elektrobit, Global Foundries and VueReal. For more information, please visit https://display.counterpointresearch.com/events/2025-sid-business-conference-powered-by-counterpoint-research.