Advanced (先端技術FPD搭載) TV市場~2023年は出荷減少も、24年に成長再開の見通し

[ご案内] 4/11火 TCC品川で開催!DSCC Japan セミナー 2023年前期版~底を脱し上昇に転じたFPD市場を徹底解説!

コロナ禍からの夜明けと共に、いち早く対面式セミナーを復活 (昨年10月) させたDSCC Japanセミナー、ご来場者様からの大歓迎のお声を受けて、今年から通常体制の年2回・品川会場に戻ります!今回もお客様のビジネス戦略をご支援すべく、1日でFPD産業の必聴ポイントを把握できる最新分析データをご提供!みずほ証券・中根康夫シニアアナリスト⇔当社アジア代表・田村喜男の「言いたい放題」オフレコ対談枠も、本セミナーの名物企画として再演決定!徹底的に「ご来場者様満足」にこだわるDSCC Japanセミナーならではのバリューにご期待ください!

冒頭部和訳

DSCCが発刊した Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) 最新版によると、Advanced (先端技術FPD搭載) TV出荷は2023年に台数、金額とも減少するものの、2024年には再び成長を始めると予測されている。本レポートでは最先端のTV技術 (WOLED、QD-OLED、QDEF、MicroLED、4Kおよび8K解像度のMiniLED) を含む、世界のプレミアムTV市場を対象としている。技術、地域、ブランド、解像度、サイズなどの項目ごとに、現在と将来のTV出荷台数と出荷金額を調査、これらすべての技術の成長を予測している。先月は最新実績を取り上げたが、本稿では最新予測を取り上げる。

Advanced TV Market Expected to Decline in 2023; Growth to Resume in 2024

※ご参考※ 無料翻訳ツール (DeepL)

Advanced TV shipments are expected to decline in both units and revenue in 2023, but are forecast to resume growth in 2024, according to the latest update to DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします), now available to subscribers. This report covers the worldwide premium TV market, including the most advanced TV technologies: WOLED, QD-OLED, QDEF, MicroLED and MiniLED with 4K and 8K resolution. The report looks at current and future TV shipments and revenues by technology, region, brand, resolution and size, and forecasts the growth of all these technologies. Last month, we covered the most recent historical results and this week we will cover our updated forecast.

In this report, we define an “Advanced TV” (capitalized) as any TV with an advanced display technology feature, including all OLED TVs, 8K LCD TVs and all LCD TVs with quantum dot technology. The forecast in the report allows analysis by feature for Advanced LCD TVs, including:

- QD LCD TV: TV using a Quantum Dot Enhancement Film (QDEF); these TVs are sold as “QLED” by Samsung, TCL and others;

- MiniLED: LCD TVs with a MiniLED backlight, as sold by TCL starting in 2019 with many brands following. Note that we expect that all MiniLED TVs will also have QDEF, but not all QDEF will have MiniLED;

- QD-OLED: Samsung Display’s large-screen OLED technology. Our forecast also uses this term for potential successor technologies, such as QNED and EL-QD;

- MicroLED: Samsung has introduced direct-view MicroLED TVs with sizes from 88”-110”, marketed as TVs for wealthy consumers. Our report excludes larger MicroLED products such as the 146” and 292” “The Wall” products sold by Samsung, as these are primarily business displays.

Two Advanced TV technologies appear in our historical data but are not included in our forecasts, because both technologies appear to be discontinued.

- Dual Cell: LCD TVs employing dual-cell technology, as introduced by Hisense in 2019. Dual Cell appears to be phased out in TV, we forecast zero volume for this technology starting in 2022;

- Rollable OLED TV: introduced by LG in 2021, has been discontinued in 2022.

In our latest update, our forecast for OLED TV has been reduced in 2023-2026 due to disappointing sales in 2022 and intense competition with lower-priced LCD TVs.

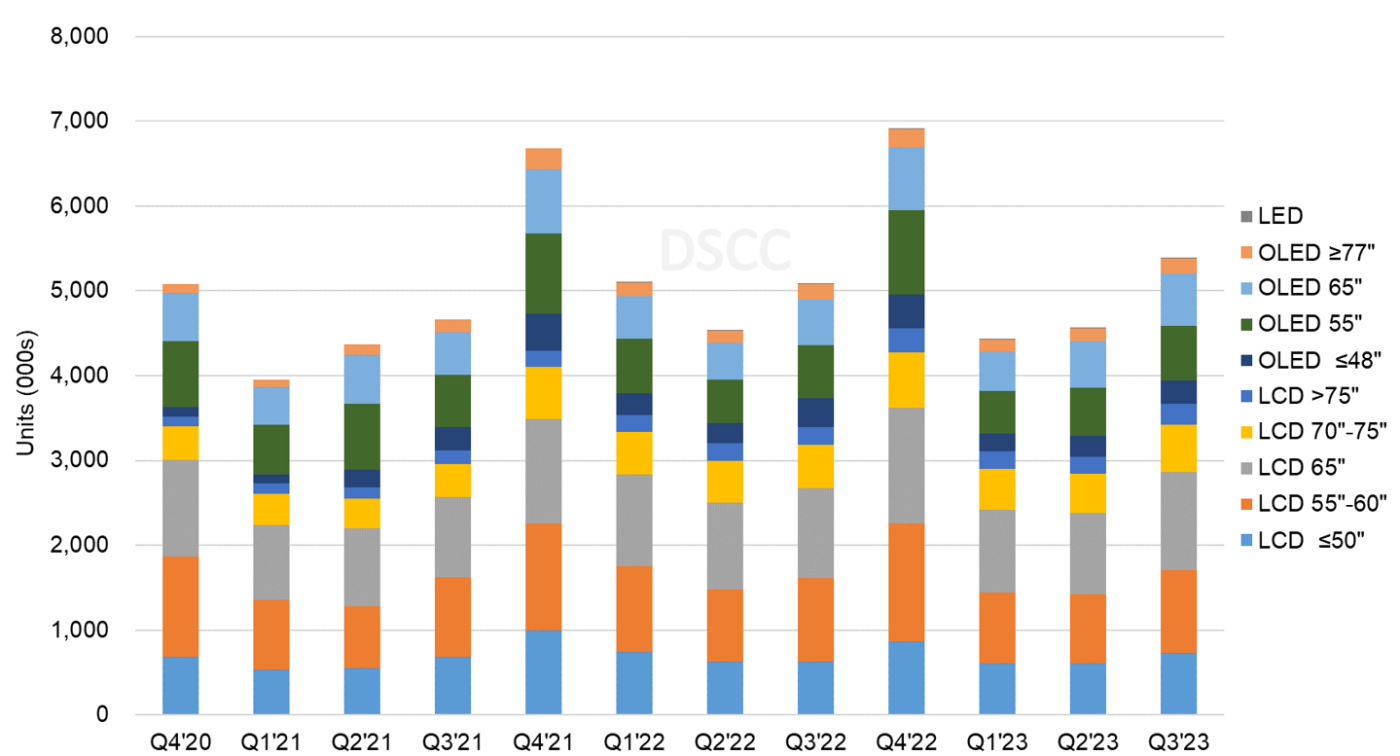

The first chart here shows our outlook for Advanced TV shipments by quarter and by technology and screen size group.

For 2022, we estimate that Advanced TV shipments increased by 10% Y/Y to 21.6M units and estimate Advanced TV revenues decreased by 3% to $26.4B. After an estimated 14% Y/Y decline in Q1’23, we forecast total Advanced TV shipments will increase 1% Y/Y in Q2 and 6% Y/Y in Q3’23.

Quarterly Advanced TV Shipments by Screen Size and Technology

OLED TV units are estimated to decline 16% Y/Y in Q1’23 but are expected to resume growth at 14% Y/Y in Q2 and 2% Y/Y in Q3. Advanced LCD TV units are estimated to decline 13% Y/Y in Q1’23 and forecast to decline 5% Y/Y in Q2 but increase 9% Y/Y in Q3.

We forecast Advanced TV revenues for the first three quarters of 2023 to decline by 11% Y/Y. Revenues for all screen sizes of Advanced LCD TV are forecast to decline Y/Y. 55” and smaller OLED TV revenues are forecast to decline but 65” and 77”+ OLED TV revenues are expected to be flat Y/Y. LED TV revenues are forecast to grow 48% Y/Y but still make up only 0.05% of TV revenues.

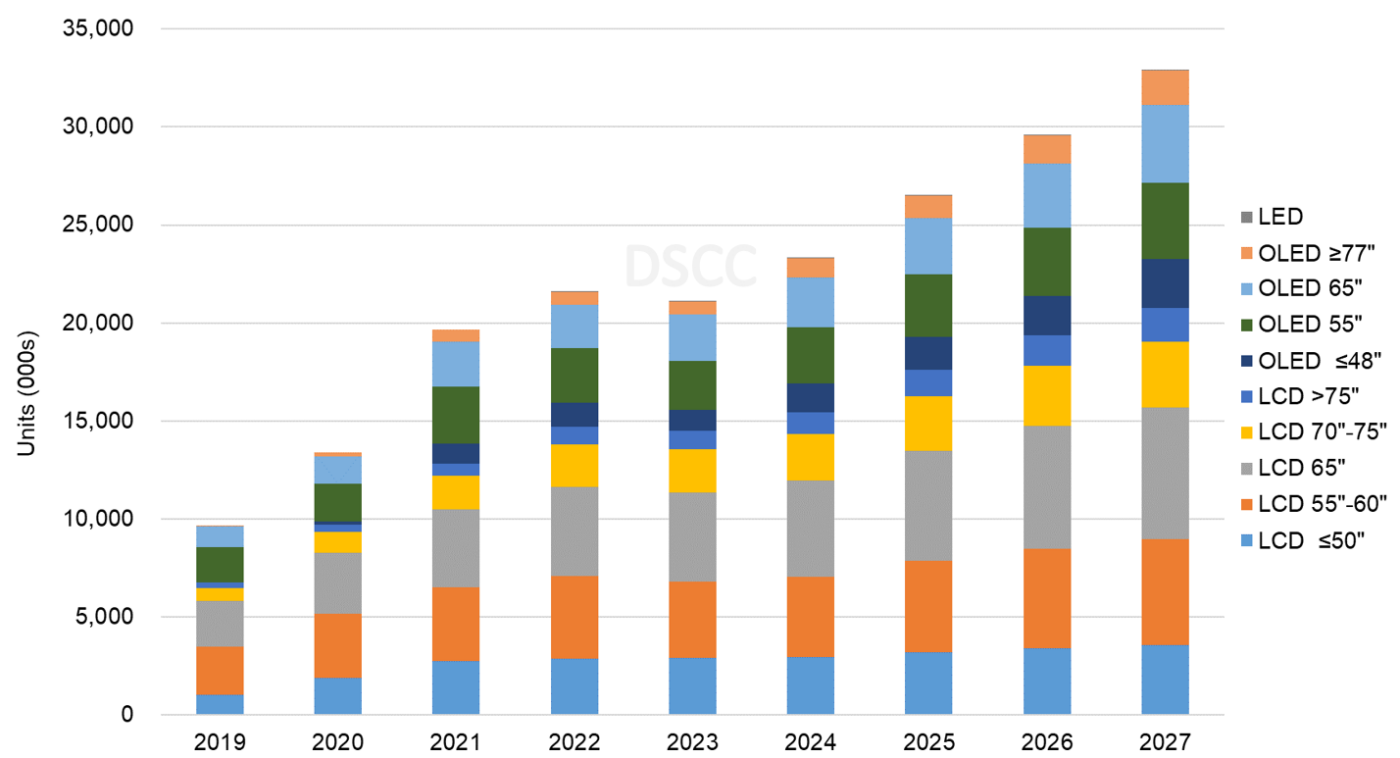

In our updated long-term forecast, after a 2% Y/Y decline in 2023, total Advanced TV shipments are expected to grow by a 12% CAGR from 2023 to 2027 to 32.9M units. OLED TV units are expected to grow at a 16% CAGR from 2023-2027 to 12.1M units, while Advanced LCD TV units are expected to grow at a 9% CAGR from 2023-2027 to 20.8M units. Including QD-OLED, OLED TV will increase share to 37% of Advanced TV by 2027.

Advanced TV Shipments by Screen Size and Technology

Advanced TV revenues jumped in 2021 with pandemic-fed demand and higher prices. Revenues declined in 2022 by 3% as price declines overwhelmed volume increases, and we expect revenues to decline further in 2023 by 11% as prices continue to decline with soft demand. We expect revenue growth to resume in 2024 and expect revenues to grow at a 7% CAGR from 2023-2027 to $30.9B, driven by increasing volumes, larger screen sizes and new technologies. We forecast that OLED TV revenues, including QD-OLED, will grow by 9% to $13.5B in 2027 and that Advanced LCD TV revenues will grow by 4% to $16.3B, with the Advanced LCD TV revenue share declining to 52% in 2027. We expect that MicroLED will emerge as the super-premium TV to capture $1.1B or 4% of Advanced TV revenues with only 0.1% of units.

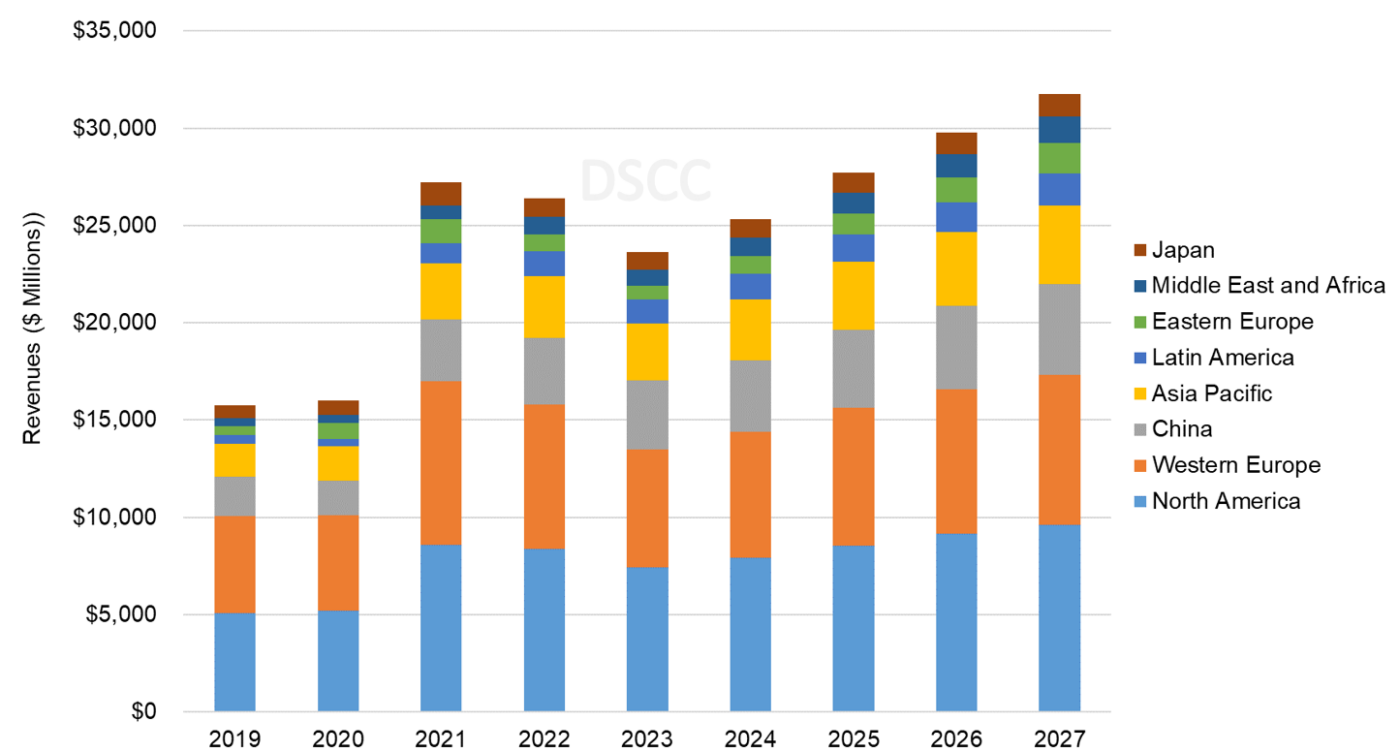

The report divides worldwide shipments into eight geographic regions, and we expect that Western Europe and North America will continue to be the largest regions for Advanced TV, but their combined share will slowly decline as growth is faster in Asia. Revenues in Western Europe declined by 13% Y/Y in 2022 while Eastern Europe declined by 31% as a result of war and inflation. We expect both regions to decline further in 2023.

Advanced TV Revenues by Region

In contrast with Europe, China and Asia Pacific remain healthy growth regions for Advanced TV. We expect the China market to grow by a 7% CAGR from 2023-2027 to $4.6B and expect the Asia Pacific market to grow by 8% to $4.1B.

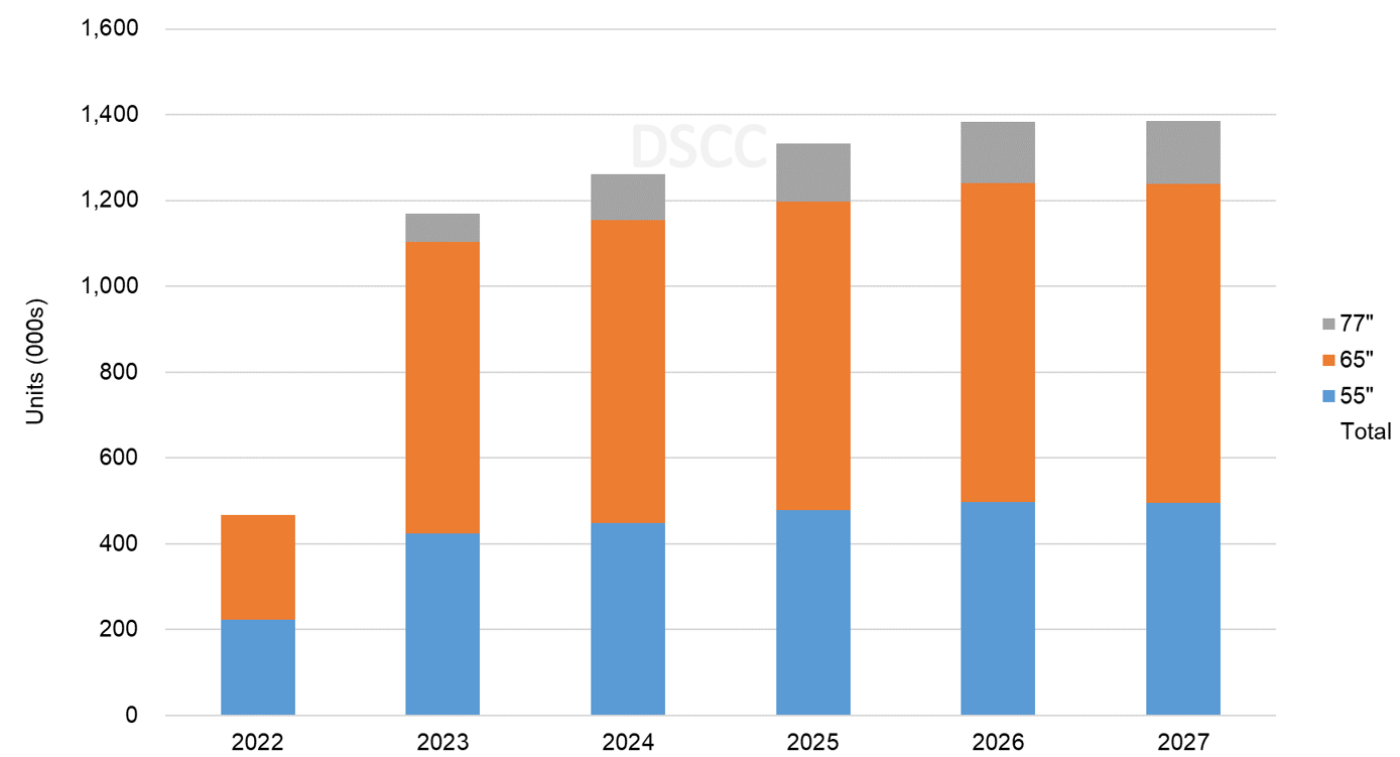

With the first year since Sony and Samsung launched TVs with QD-OLED panels, we are seeing how this technology competes with other Advanced TV display technologies. Our forecast for QD-OLED TVs by screen size is shown in the next chart here. We estimate that these two brands shipped 467K QD-OLED TVs in 2022, and we expect shipments to increase to 1.2M in 2027, but after 2023, further growth will be limited by SDC’s capacity. The product portfolio will be limited to 4K resolution panels, but 77” TVs and 49” monitors have been added in 2023 as SDC will make these in a Multi-cut Mother Glass (MMG) configuration, 2-up 77” and 2-up 49” on each Gen 8.5 substrate. SDC will also make 34” QD-OLED monitor panels, but monitors are not covered in the Advanced TV report.

QD-OLED TV Shipments by Screen Size

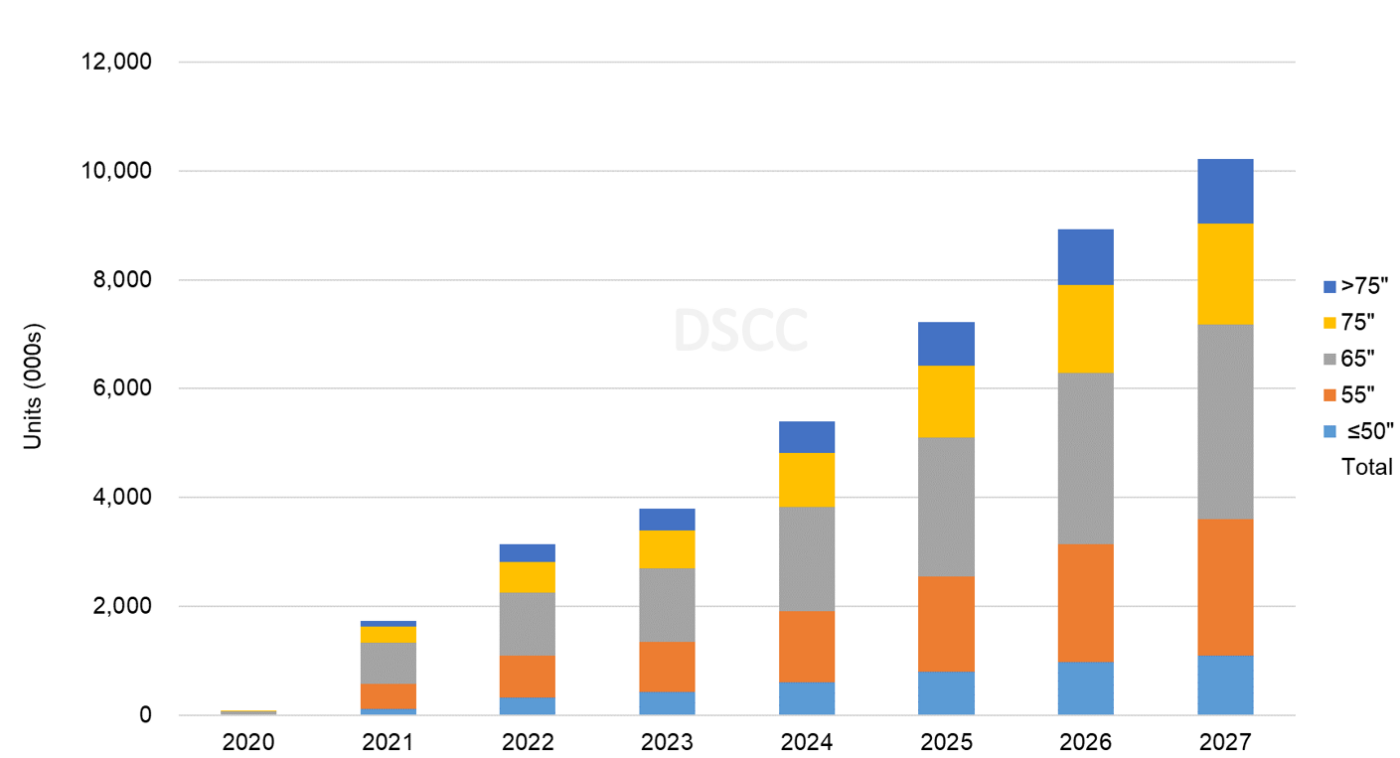

The category of Advanced TVs represents only a small fraction of the total TV market in unit terms, but it represents where all “the action” is in the technology battle. The champion for the LCD camp is MiniLED, and our forecast for MiniLED TV sets by screen size is shown in the final chart here. MiniLED TV was introduced by TCL in 2019 but sold only in very small volumes in 2020. However, TCL has been followed by most other major brands introducing MiniLED TVs, including Samsung and LG in 2021 and Sony and others in 2022. We expect an ongoing battle between MiniLED, White OLED and QD-OLED for the premium TV market. Because of the Gen 10.5 LCD fabs, we expect that MiniLED will have a cost and price advantage over OLED in the largest screen sizes. MiniLED and big screens will also be the main pathway to 8K TVs; a majority of 8K TVs have employed MiniLED technology starting in 2022.

MiniLED TV Shipments by Screen Size

Overall, we expect that the volume for OLED TVs (including QD-OLED) to continue to exceed that of MiniLED, but that LCD TV (both MiniLED and standard backlit models) will continue to maintain >50% unit share of Advanced TV.

DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) includes technical descriptions of all major advanced TV display technologies, plus quarterly shipment history through Q4’22, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast out to 2027 across technology, region, resolution and size. Readers interested in subscribing to the DSCC Advanced TV Shipment Report should contact お問い合わせ窓口.

本記事の出典調査レポート

Quarterly Advanced TV Shipment and Forecast Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。