Q4’22のAdvanced (先端技術FPD搭載) TV市場~SamsungとLGがシェアを回復、引き続き市場を支配

冒頭部和訳

プレミアムTV市場では韓国の2大ブランドであるSamsungとLGの支配が続いており、Q4’22は両社ともシェアを回復した。DSCCが Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) の最新版で明らかにしている。DSCCの共同創業者兼プリンシパルアナリストのBob O’Brienは次のように述べている。「TV市場全体がパンデミック後の凪 (なぎ) の状態で苦戦しており、欧州の出荷にウクライナでの戦争の影響が続いているため、Advanced (先端技術FPD搭載) TV市場の成長は減速している。一方で、欧州以外ではAdvanced TV市場は引き続き健全な成長を遂げている」

Q4’22市場のハイライトは以下の通り。

・Samsungの出荷数は前年比で横ばい、数量シェアは1%減となった。Samsungの出荷額は前年比 3%減となったが、金額シェアは42%に増加している。対Q3’22比では、Advanced LCD TV市場におけるSamsungのシェアは数量ベースで2%、金額ベースで3%回復している。

・LGの出荷数は前年比14%増で、数量シェアはQ4’21の23%からQ4’22には25%に増加した。LGの出荷額は前年比5%減、シェアは30%に増加した。対Q3’22比では、OLED TV市場におけるLGのシェアは数量、金額とも7%回復している。LGはOLED TVで支配的地位を維持しており、数量シェアは61%、金額シェアは60%である。MiniLEDでは数量、金額ともシェア4%の小さなポジションを確立している。

・Sonyの出荷数は前年比で横ばい、数量シェアは8%から7%に減少した。Sonyの出荷額は前年比 17%減だった。

・TCLの出荷数は前年比35%増で、シェアは前年の6%から7%に増加した。TCLの出荷額は前年比6%増だった。

Samsung and LG Continue to Dominate Advanced TV Market and Regained Share in Q4’22

※ご参考※ 無料翻訳ツール (DeepL)

The premium TV market continues to be dominated by the two Korean brands Samsung and LG, and both brands regained some market share in the fourth quarter of 2022, according to the latest update of DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします), now available to subscribers. According to DSCC Co-Founder and Principal Analyst, Bob O’Brien, “Growth in the Advanced TV market slowed as the TV market overall struggles through a post-pandemic lull and as shipments in Europe continue to suffer from the impact of the war in Ukraine. Outside of Europe, the Advanced TV market continues healthy growth.”

In Q4’22:

- Samsung shipments were flat Y/Y and Samsung unit share decreased by 1% Y/Y. Samsung revenues decreased 3% Y/Y but revenue share increased to 42%. Compared to Q3’22, Samsung regained unit/$ share of Advanced LCD TV by 2%/3%.

- LG shipments increased by 14% Y/Y and unit share increased from 23% in Q4’21 to 25% in Q4’22. LG revenues decreased 5% Y/Y and LG gained share to 30%. Compared to Q3’22, LG regained 7% unit and revenue share of OLED TV. LG continues to dominate OLED TV with 61%/60% unit/revenue share and has established a small position in MiniLED with 4%/4% share.

- Sony shipments were flat Y/Y and Sony unit share decreased from 8% to 7%. Sony revenues declined 17% Y/Y.

- TCL shipments increased 35% Y/Y and TCL gained share Y/Y from 6% to 7%. TCL revenues increased 6% Y/Y.

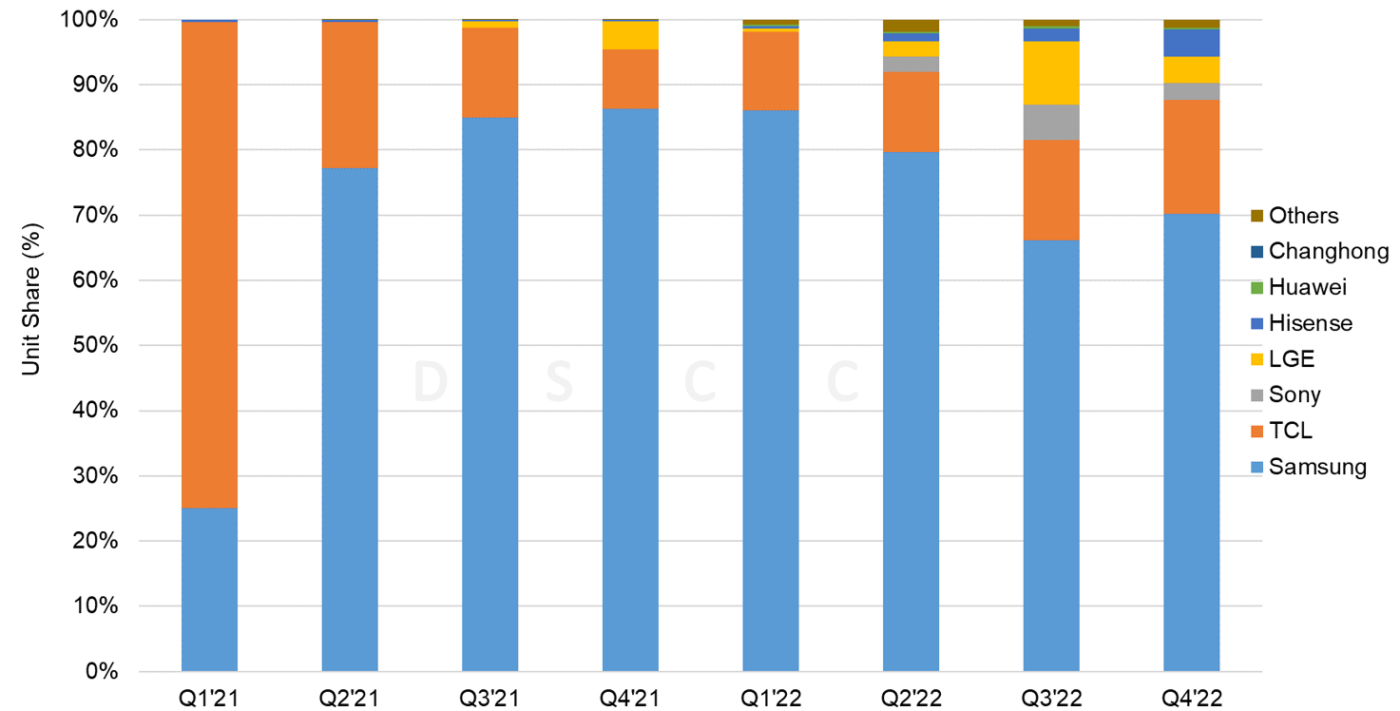

MiniLED LCD TV Shipments by Brand

Growth accelerated for MiniLED TV shipments in Q4’22 with 40% growth Y/Y to 990k units but revenues increased only 7% as ASPs fell by 24% Y/Y. Samsung continues to dominate the MiniLED TV category with 69%/71% unit/revenue share even as the number of competitors in the space continues to increase. TCL managed to regain some of its share as shipments increased by 167% Y/Y and revenues increased by 113% Y/Y. TCL unit share recovered to 17% and its revenue share increased to 16%.

Despite strong growth in Q4’22, MiniLED remained much smaller than OLED in both units and revenues. Total MiniLED TV shipments in Q4’22 were 990K compared to 2.35M OLED TV shipments, while total MiniLED TV revenues in Q4’22 were $1.35B compared to $3.57B for OLED TV.

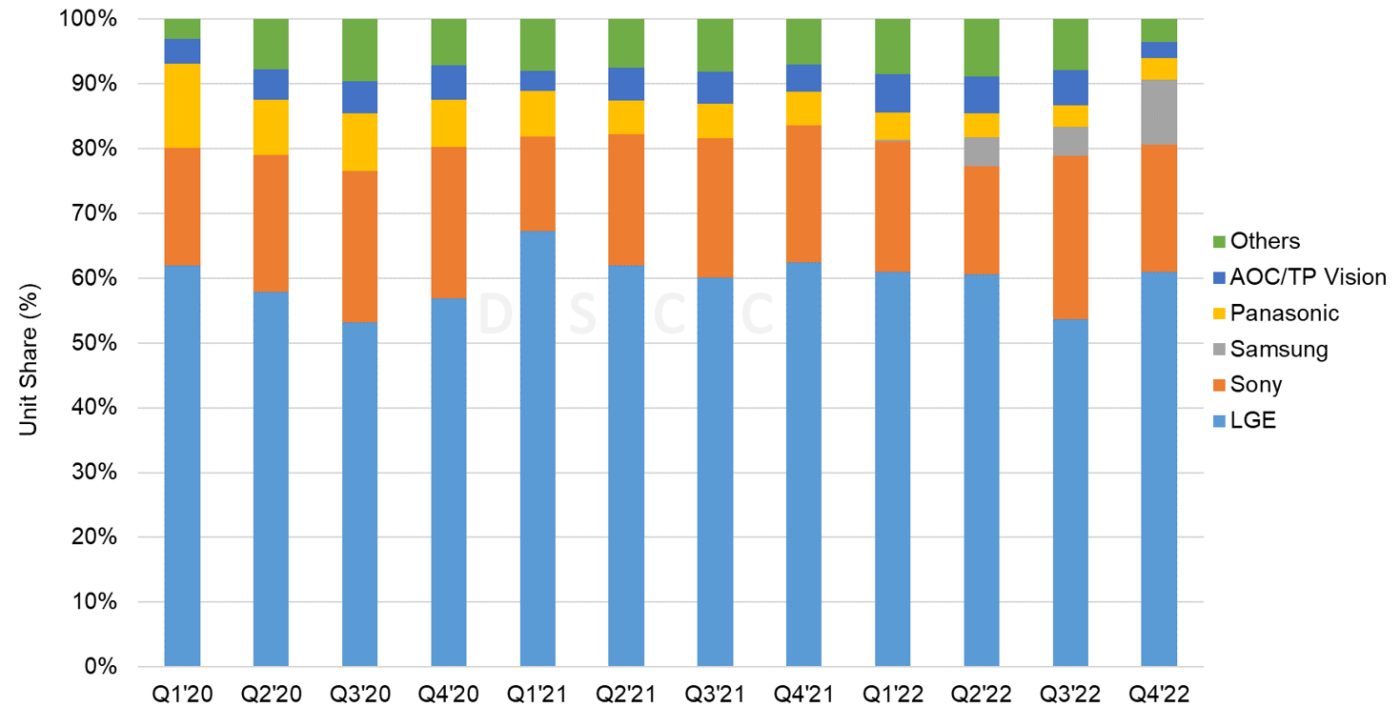

For the second time in 2022 and the second time ever, OLED TV shipments decreased Y/Y in Q4’22, falling 1% to 2.3M units. For the full year 2022, OLED TV shipments increased just 1% Y/Y to 6.9M units. Within the OLED TV category, QD-OLED grew from nothing in 2021 to represent 12% of OLED TV units and 15% of OLED TV revenue in Q4’22. With the increased competition from QD-OLED, White OLED TV shipments declined by 13% Y/Y in Q4’22, and revenues declined by 21% Y/Y. With a limited QD-OLED product portfolio, Samsung gained 10% of the OLED TV market in Q4.

OLED TV Shipments by Brand

The report’s pivot tables allow an analysis of brand share by screen size, region, technology, resolution and other variables. In the brand battle, Samsung maintained the top spot in both units and revenue and regained some share in Q4 compared to Q3’22.

DSCC’s Quarterly Advanced TV Shipment and Forecast Report (一部実データ付きサンプルをお送りします) tracks the emergence of MiniLED LCD as a competitor to OLED TV in the premium space. While TCL introduced MiniLED in late 2019 and recorded some sales in 2020, the category remained tiny until Samsung and other brands introduced products with MiniLED technology in Q1’21. From less than 100K units in 2020, MiniLED TV shipments grew to more than 1.7M units in 2021, and revenue grew from $73M in 2020 to $3.5B in 2021. For the full year 2022, MiniLED TV shipments grew by 82% Y/Y to 3.15M units and revenues increased by 42% to $4.9B.

The report also includes technical descriptions of all major advanced TV display technologies, plus quarterly shipment results from Q1 2018 through Q4’22, sortable by technology, region, brand, resolution and size, and includes pivot tables for analysis of units, revenues, ASPs and other metrics. The report includes DSCC’s quarterly forecast for five years across technology, region, resolution and size. Readers interested in subscribing to the DSCC Advanced TV Shipment Report should contact お問い合わせ窓口.

本記事の出典調査レポート

Quarterly Advanced TV Shipment and Forecast Report

一部実データ付きサンプルをご返送

ご案内手順

1) まずは「お問い合わせフォーム」経由のご連絡にて、ご紹介資料、国内販売価格、一部実データ付きサンプルをご返信します。2) その後、DSCCアジア代表・田村喜男アナリストによる「本レポートの強み~DSCC独自の分析手法とは」のご説明 (お電話またはWEB面談) の上、お客様のミッションやお悩みをお聞かせください。本レポートを主候補に、課題解決に向けた最適サービスをご提案させていただきます。 3) ご購入後も、掲載内容に関するご質問を国内お客様サポート窓口が承り、質疑応答ミーティングを通じた国内外アナリスト/コンサルタントとの積極的な交流をお手伝いします。